- Francis Généreux

Principal Economist

Weekly Commentary

Trump and Powell: A Fragile Truce

May 9, 2025

In April, President Donald Trump launched a series of attacks on the Federal Reserve (Fed) and its chair, Jerome Powell. While repeatedly urging the Fed to enact “pre-emptive” rate cuts, Trump also took to Truth Social, his self-launched social media platform, to insult Powell, calling him “Mr. Too Late” and a “major loser.” On April 17, he posted, “Powell’s termination can’t come fast enough!” and White House advisors mentioned that they were looking into their legal options for firing the Fed Chair.

Since then, Trump has dialled down his remarks and stated that he has no intention of firing Powell. But while his tone may be less aggressive, he has continued to criticize Powell. During last week’s speech External link. celebrating the first 100 days of his second term, Trump took a moment to say, “I have a Fed person who’s not really doing a good job. But I won’t say that. I want to be very nice. I want to be very nice and respectful to the Fed. You’re not supposed to criticize the Fed; you’re supposed to let him do his own thing. But I know much more than he does about interest rates, believe me.” And this Thursday morning, after the Fed announced its decision to hold rates steady, Trump once again took a jab over Truth Social: “‘Too Late’ Jerome Powell is a FOOL, who doesn’t have a clue. Other than that, I like him very much!”

This is not the first time that Trump has attempted to influence Fed monetary policy. During his first term, in 2019, he repeatedly called for Powell to lower interest rates, as both the economy and stock markets struggled in the wake of his first trade war. Then as now, Trump’s attacks grew personal—even though he had selected Powell for the role of chair in 2017, with Senate confirmation in 2018.

In some ways, we can see why Donald Trump wants a more dovish Fed. The other major central banks, including the European Central Bank and the Bank of England, have continued to cut rates. And in recent months, US inflation has surprised to the downside more than the upside. Inflation is slower than it was in December 2024 when the Fed lowered rates, so one may well ask why rates aren’t going down. Especially since real GDP declined in the first quarter (Biden’s fault, if you ask Trump).

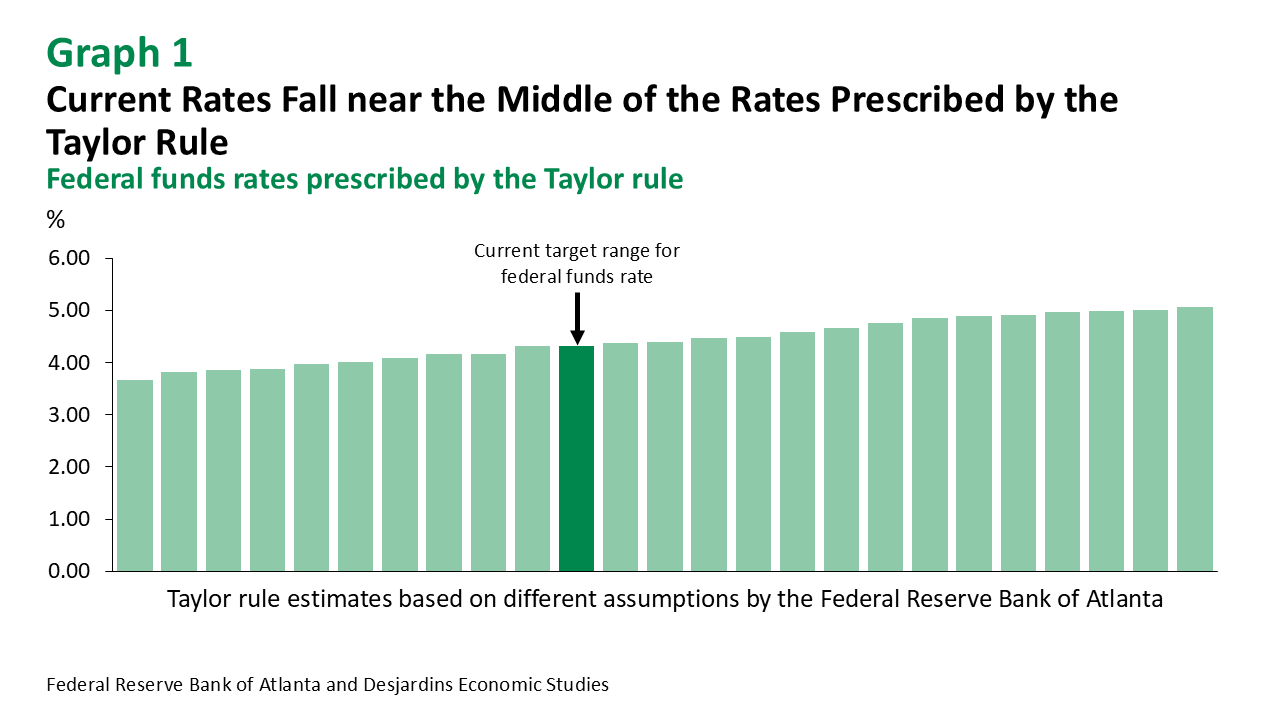

But the situation is obviously more nuanced. Up until now, the US labour market has shown some resilience. And while real GDP is down, there is still little unused capacity in the American economy. Furthermore, the current key rate falls roughly in the middle of the rates prescribed by different versions of the Taylor rule External link. (graph 1). This well-known rule and its alternative versions are used to calculate where the target federal funds rate should be based on the degree of slack in the economy and the gap between inflation and its target.

The S‑Word

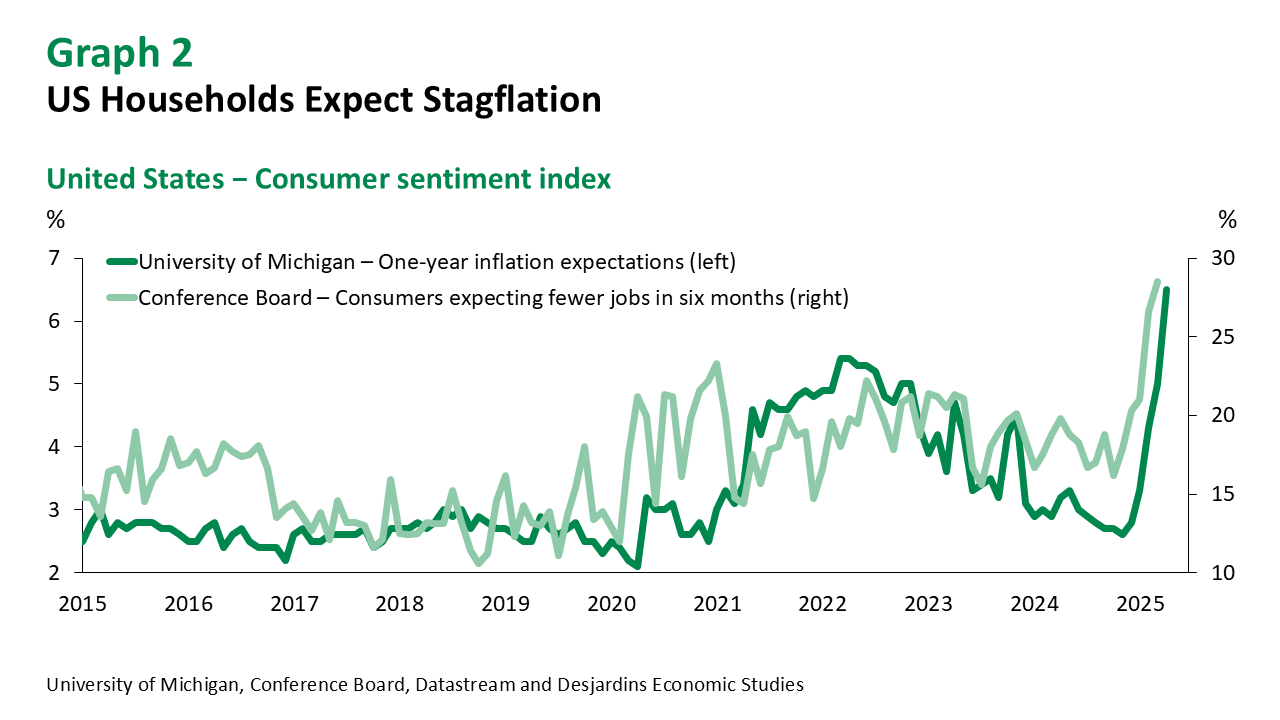

However, this situation is best viewed from the rear-view mirror. When we look ahead, things are far less certain. Economic indicators don’t yet reflect the full impact of Trump’s chaotic trade policy and the ongoing trade war with China, though confidence is already falling. Consumers in particular are worried about the possibility of runaway inflation and a sharp decline in the labour market (graph 2). If these fears become a reality, stagflation risks could take centre stage, leaving the Fed torn between the two halves of its dual mandate, controlling inflation and achieving maximum employment. The Fed statement released on Wednesday clearly noted the rising uncertainty and joint risks of overly high inflation and jobless rates, and those concerns were echoed by Jerome Powell during the FOMC press conference that followed. And all of this comes on the heels of Trump’s “Liberation Day” announcements, which seem to have eroded confidence in the US economy’s long-term resilience—and perhaps more importantly, in the dollar’s role as a safe-haven currency. From this angle, Donald Trump’s demands and attacks on the Fed and its chair are doing more harm than good.

Fed Independence Called into Question

Central bank independence is a key underpinning of modern macroeconomics. Monetary authorities must be able to make their decisions based on an objective assessment of the economic and financial conditions and outlook without letting political considerations cloud their view. For several decades now, it has been understood that independent central banks can stabilize economic cycles and better control inflation.

Trump’s remarks are obviously counter to this globally accepted truth. But his attacks may have more layers than initially appear. The president’s entourage has long been suggesting that the Fed is already not independent and that it leans in favour of the Democrats. If that were true, the White House’s efforts to sway the central bank could be seen as a “recentring.”

Other accusations toward the Fed are more explicit: Instead of saying it has a partisan bent, some believe the Fed has become too “woke” to play the role it’s been given by Congress and that it has made serious errors in its conduct of monetary policy. This line of thought was recently brought forward in a speech by Kevin Warsh External link., a former member of the Fed’s Board of Governors from 2006 to 2011. Trump is reportedly considering him as Powell’s successor at the head of the Fed. Warsh has accused the Fed of acting inappropriately in the name of “inclusive employment,” overstimulating the economy and driving up inflation to achieve higher rates of employment for certain socio-economic groups. He also believes that the Fed encouraged irresponsible government spending by adopting overly broad quantitative easing after the 2008–2009 financial crisis and after the pandemic. He further criticized the Fed for wanting to play a role in the fight against climate change, which is not part of its mandate. According to Warsh, these mistakes have undermined the effectiveness of monetary policy, damaged the central bank’s credibility and compromised its independence.

All these arguments must sound like music to Trump’s ears. Since his return to the Oval Office, he’s worked to dismantle any policies that favour inclusion or the energy transition. The president could use Warsh’s rhetoric to justify changes in Fed leadership and the way it works. It could also serve as a litmus test when choosing future governors, including Jerome Powell’s successor when his four-year term ends in May 2026.

If Donald Trump can’t wait that long, he will have to look into shortening the terms of current Fed officials. A recent order from the Chief Justice of the Supreme Court has temporarily authorized the president of the United States to fire the heads of so-called independent federal agencies. Trump’s expanded power over these agencies has not yet come before the Supreme Court. If this power is confirmed, and if it applies to the Fed, Trump could be tempted to oust several governors, including Powell. This act would send the financial markets reeling. It could be perceived as a serious threat to central bank independence and raise doubts about their ability to keep inflation under control.

But until it comes to pass—if ever—Trump will likely content himself with taking further swings at the Fed. Especially if, as we predict, the White House’s trade policy kicks off a recession in the United States. Having a scapegoat could be convenient if economic conditions deteriorate further. Joe Biden can only be blamed for so long. At some point, it will be time to lay the blame squarely on Jerome Powell.