- Francis Généreux

Principal Economist

Essentials of Monetary Policy

Another Federal Reserve Rate Cut Despite Driving in the Fog

October 29, 2025

According to the Federal Reserve (Fed)

- The Fed lowered its policy rates by 25 basis points. The target range for the federal funds rate now stands between 3.75% and 4.00%.

- The Committee decided to conclude the reduction of its aggregate securities holdings on December 1.

- Available indicators suggest that economic activity has been expanding at a moderate pace. Job gains have slowed this year, and the unemployment rate has edged up but remained low through August; more recent indicators are consistent with these developments. Inflation has moved up since earlier in the year and remains somewhat elevated.

- Uncertainty about the economic outlook remains elevated. The Committee is attentive to the risks to both sides of its dual mandate and judges that downside risks to employment rose in recent months.

Comments

No surprise here—the Fed once again lowered its policy rates by 25 basis points. This move was widely anticipated by markets and most forecasters. It had also been signalled in advance through the projections released by Fed officials during the September meeting. Nonetheless, two dissenting views emerged around the monetary policy table. The newest member, Stephen Miran, would have preferred a 50‑point cut, as he did at the previous meeting. Meanwhile, Kansas City Fed President Jeffrey Schmid favoured holding rates steady.

The conditions under which Fed officials had to make their decision were rather extraordinary. Due to the federal shutdown, they lacked access to the usual array of economic indicators. The most recent official labour market data date back to August. Third-quarter GDP figures have not yet been released, and data on business activity are also missing. While September’s Consumer Price Index results were published, other price indicators—such as producer prices and import/export prices—are still unavailable. The overall picture is therefore more opaque than Chair Powell and his colleagues would have preferred. The latest Beige Book and indicators from non-federal sources suggest that the economic environment has not changed significantly, aside from the risks stemming directly from the shutdown.

This assessment is shared by the Fed. The statement reflects this view, and Chair Powell reiterated it during his press conference, referring to “driving through the fog.” He also noted that the budgetary impasse is likely to have negative consequences for growth, although these effects should reverse once an agreement is reached.

On the inflation front, the Fed maintains that higher tariffs are pushing up goods prices. It continues to expect these effects to be short-lived, while acknowledging the risk that they could prove more persistent. The Fed welcomed the slowdown in housing-related service prices but remains puzzled by prices of other service categories that have been moving sideways over the last few months.

Implications

We still see another 25‑basis point rate cut at the December meeting. That said, Chair Powell emphasized—and repeated—that another rate cut at the December meeting is not a foregone conclusion. Developments in the shutdown and the eventual release of missing economic indicators will provide greater clarity ahead of the next meeting. If the fog caused by the situation in Washington persists, the Fed may be inclined to wait for more visibility before taking further action.

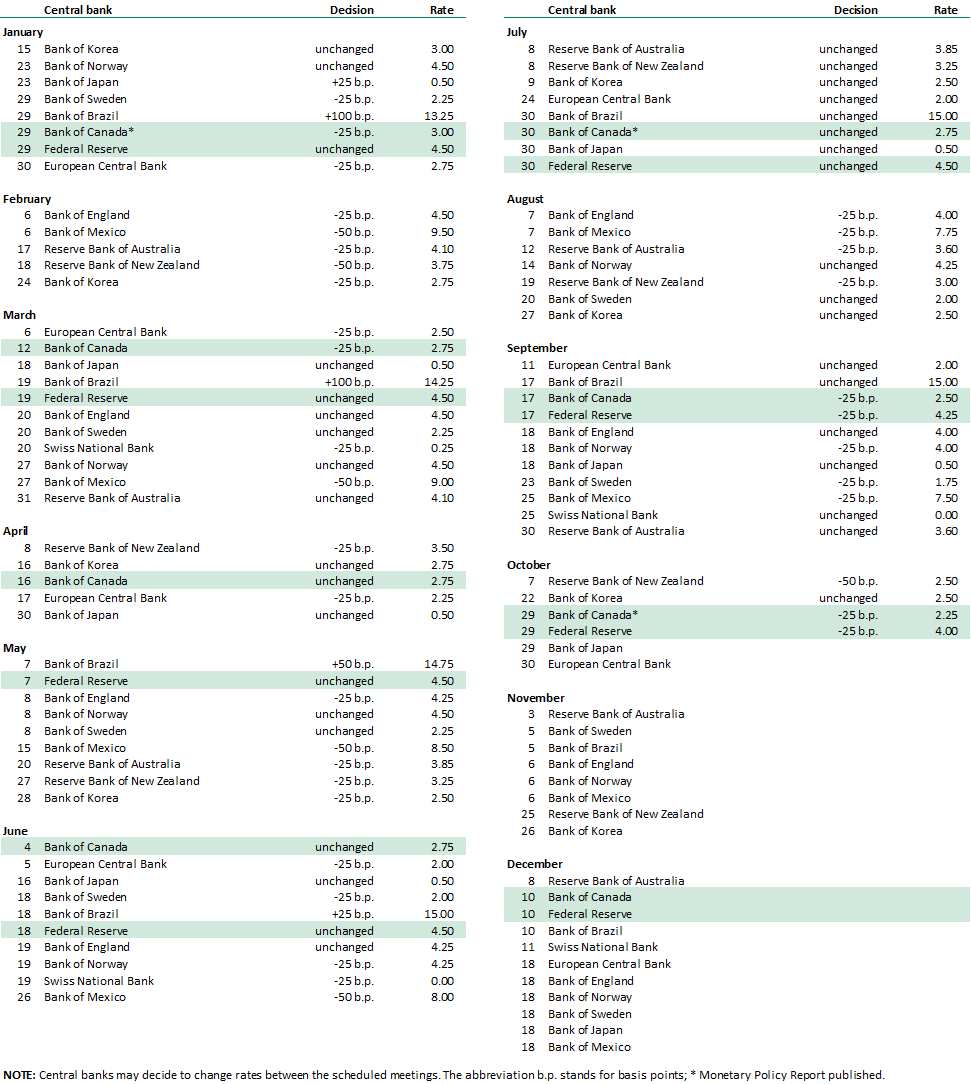

2025 Schedule of Central Bank Meetings