- Francis Généreux

Principal Economist

Essentials of Monetary Policy

Federal Reserve Cuts Rates and Signals Further Easing Ahead

September 17, 2025

According to the Federal Reserve (Fed)

- The Fed lowered its policy rates by 25 basis points. The target range for the federal funds rate now stands between 4.00% and 4.25%.

- Recent indicators suggest that growth of economic activity moderated in the first half of the year. Job gains have slowed, and the unemployment rate has edged up but remains low. Inflation has moved up and remains somewhat elevated.

- Uncertainty about the economic outlook remains elevated. The Committee is attentive to the risks to both sides of its dual mandate and judges that downside risks to employment have risen.

Comments

The stage was set for a first policy rate cut in 2025. First, markets were positioned accordingly, and a strong majority of forecasters surveyed by Bloomberg were expecting a 25‑basis-point reduction—exactly what Fed officials delivered. Second, the timing was favourable, as recent labour market indicators pointed to increasingly evident weakness. This opened a window for the Fed to act, even though inflation remains relatively high and tariff-related price pressures are still a concern. The decision was nearly unanimous, with the only dissent coming from newly appointed Governor Stephen Miran, formerly an economic advisor to President Trump, who advocated for a 50‑basis-point cut (his former boss would likely have preferred an even larger reduction).

It’s worth noting that today’s rate move was announced even though the Fed’s economic projections for 2025 have changed very little since the June update. Forecasts for inflation and unemployment remain unchanged, while the projection for year-end GDP growth was revised upward from 1.4% to 1.6%. Even more surprising, the Fed now expects stronger real GDP growth by the end of 2026, accompanied by slightly higher inflation (from 2.4% to 2.6%) and a modest decline in the unemployment rate compared to June’s outlook. These improved projections would not typically justify lower policy rates. Nonetheless, the Fed’s updated forecast includes two additional 25‑basis-point rate cuts by the end of 2025, followed by one rate cut per year in 2026 and 2027.

Today’s decision—and those expected in upcoming meetings—should be viewed as part of a risk management strategy and a form of insurance against a more pronounced deterioration in labour market conditions. The slowdown in job creation over the past few months and the recent uptick in unemployment claims are likely weighing on Fed officials. In his press conference, Chair Jerome Powell stated: “With downside risks to employment having increased, the balance has shifted. Accordingly, we judged appropriately at this meeting to take another step toward a more neutral policy stance.” On the inflationary risks stemming from tariffs, he added: “A reasonable base case is that the effects on inflation will be relatively short-lived.”

Implications

Chair Powell also reiterated that monetary policy is not on a preset course, and that the evolution of economic indicators will remain central to future decisions. That said, both today’s move and the Fed’s projected path align well with our own forecasts. We expect monetary easing to continue for a little while longer this year. However, with inflation likely to show renewed strength in early 2026, a pause in rate cuts will probably be warranted.

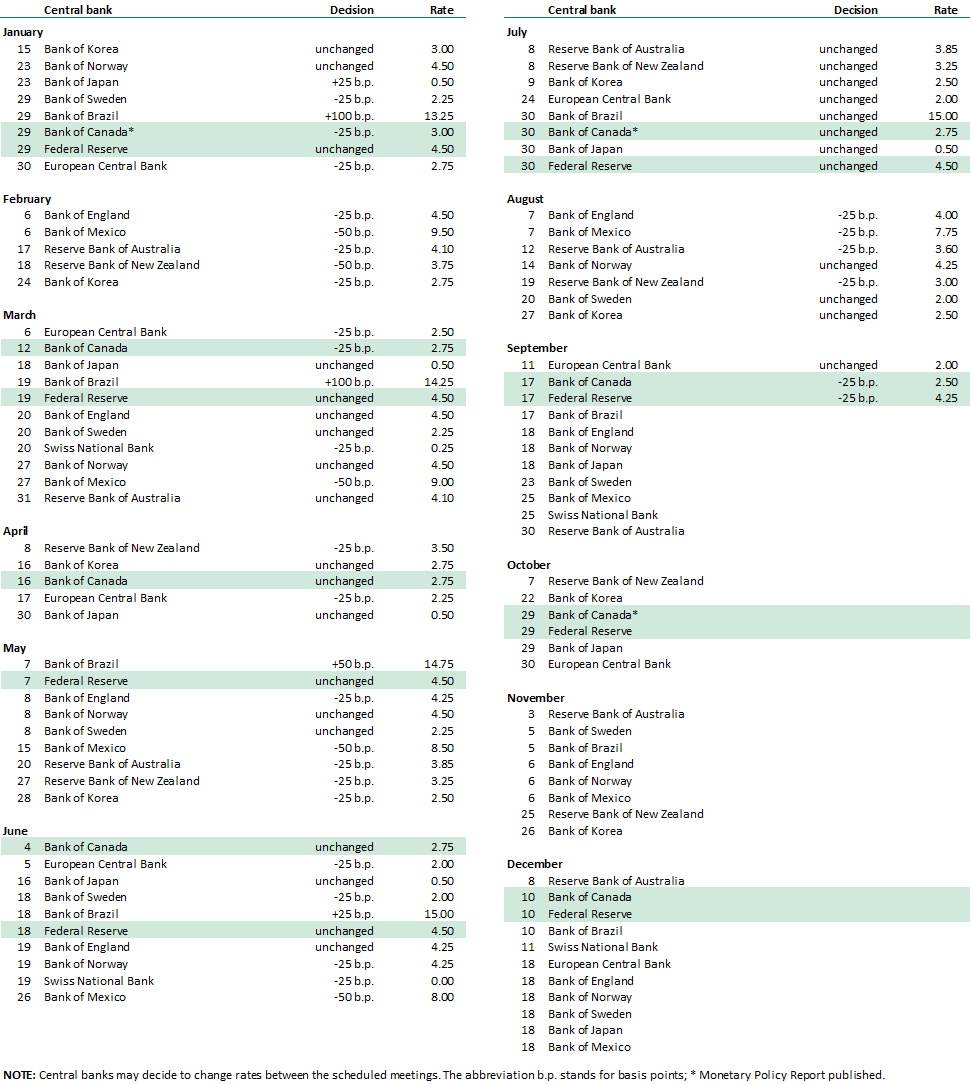

2025 Schedule of Central Bank Meetings