- Marc-Antoine Dumont

Senior Economist

Economic News

United States: Inflation Slows Slightly

October 24, 2025

Highlights

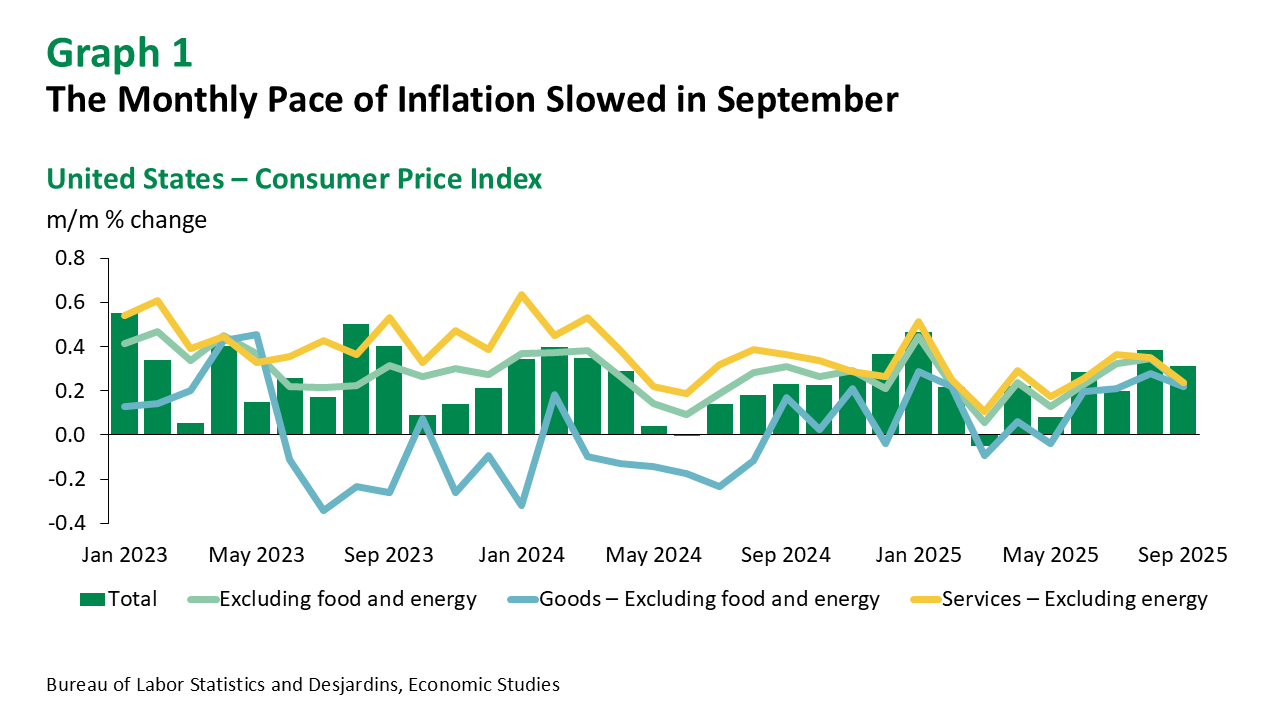

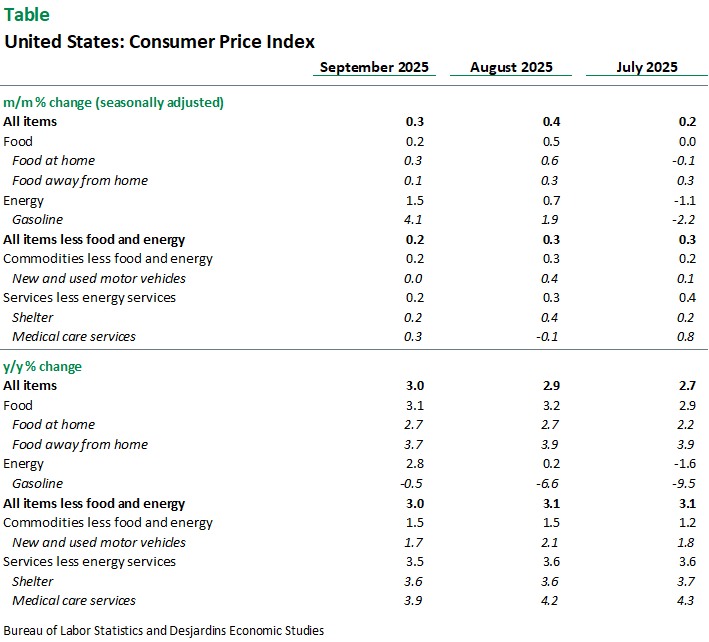

- The Consumer Price Index (CPI) rose by 0.3% in September, following a 0.4% increase in August. Core CPI, which excludes food and energy, grew by 0.2% in September, down from 0.3% the previous month. Price growth in September came in below consensus expectations, which were at 0.4%.

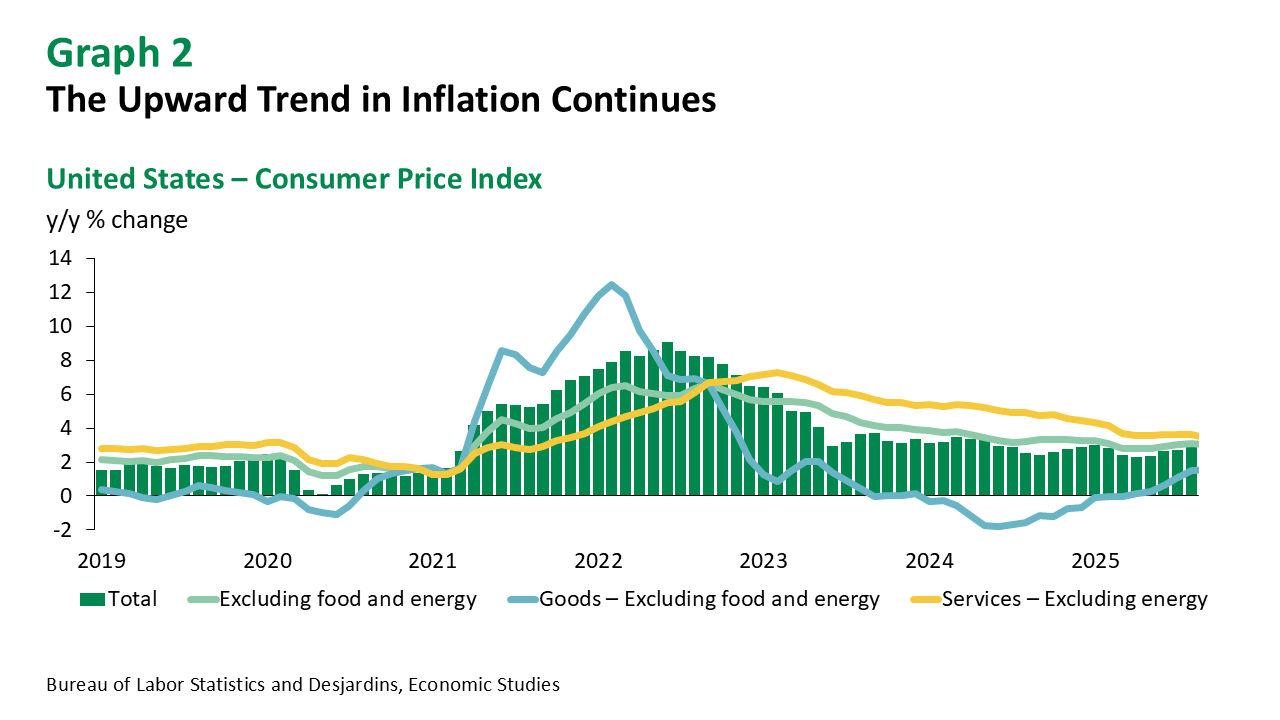

- On a year-over-year basis, headline CPI edged up from 2.9% to 3.0%, while core inflation eased slightly to 3.0%.

Comments

Although September’s inflation reading came in slightly below expectations, upward pressure on consumer prices remains evident. The increase was driven primarily by food—particularly groceries (+0.3%)—and gasoline (+4.1%). However, seasonal adjustments played an outsized role, as the unadjusted rise in gasoline prices was only 1.1%. On a year-over-year basis, gasoline prices actually declined by 0.5% in September.

Meanwhile, there are some signs that tariff effects are beginning to filter through to consumer prices. Producer price indices have posted modest gains in recent months, and the CPI for goods excluding food and energy has followed a similar trajectory. Year-over-year, this component accelerated from 1.2% in July to 1.5% in September. That said, prices for goods were flat between August and September—a reassuring short-term development. Still, the broader trend remains concerning, and the impact of the trade war—limited so far—is expected to intensify in the coming months.

In services, the housing index stabilized after August’s unexpected surge. This pause does not alter the fact that year-over-year services inflation, excluding food and energy, remains elevated at 3.5%—a key concern for the Federal Reserve (Fed) policymakers.

Overall, September’s CPI data offers some relief despite persistent inflationary pressures. Consumer prices were more stable than forecasters anticipated, which is encouraging. Tariff-related effects are starting to emerge, but their pass-through to overall prices remains gradual.

Implications

The latest inflation figures reinforce our view that the Fed will cut its policy rate two more times this year, as attention shifts toward the weakening labour market. However, as tariffs are expected to exert more pronounced upward pressure on goods prices in the coming months, we anticipate that US central bankers will be forced to remain on the sidelines during the first half of 2026.