- Marc-Antoine Dumont

Senior Economist

Economic News

US: Real GDP Rebounded in the Second Quarter

July 30, 2025

Highlights

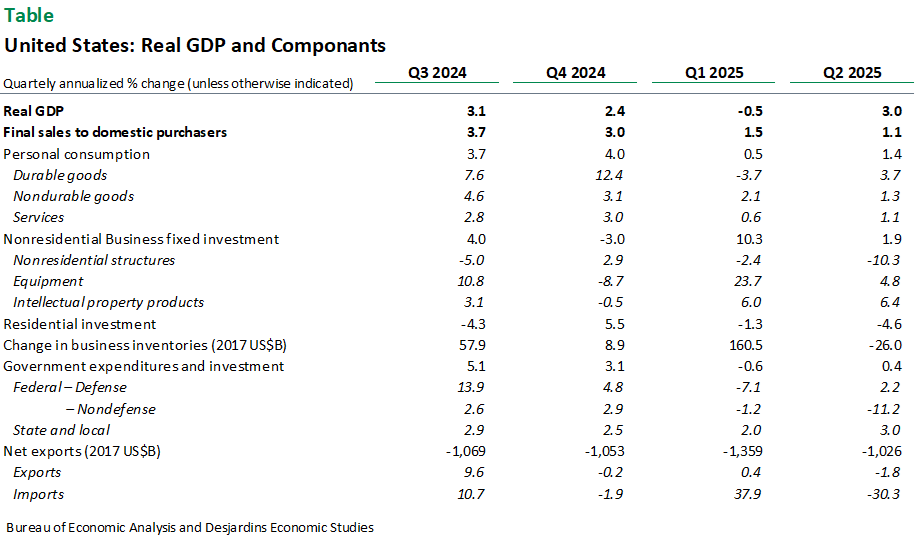

- US real GDP rose by an annualized 3.0% in the second quarter of 2025, according to the initial estimate of the national accounts. This increase contrasts with the annualized decline of 0.5% in the first quarter.

Comments

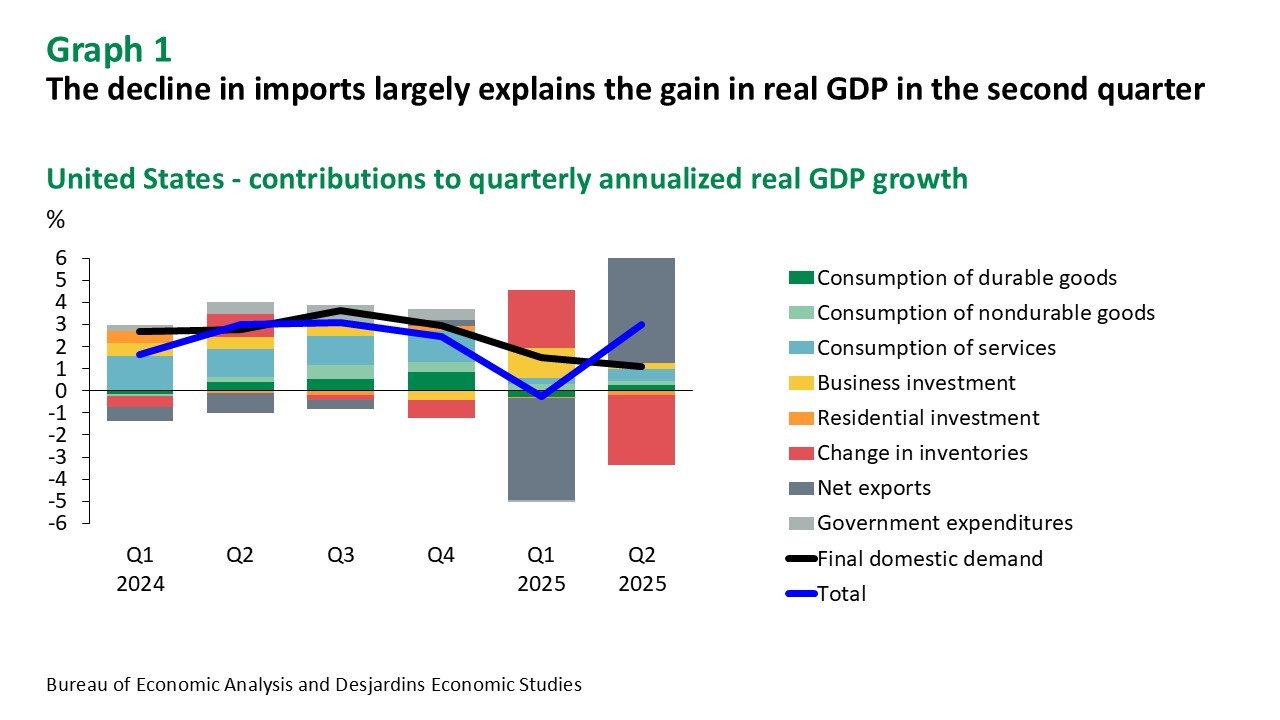

The strong performance of US real GDP in the second quarter is primarily due to a sharp drop in imports (-30.3%), which are subtracted in the GDP calculation. This seesaw pattern in real GDP and imports stems from the White House’s trade policy, which led to precautionary stockpiling during the winter, followed by a significant trend reversal in the spring.

As such, the 3.0% increase in US real GDP provides only a partial picture of the economic situation, as business investment and final demand growth slowed between the first and second quarters. The pace of growth remains modest compared to previous quarters, but does not indicate a collapse in activity. The weakness in investment is mainly due to a slowdown in equipment spending (+4.8%), following the strong gain in the first quarter (+23.7%) attributed to front-loaded economic activity. Non-residential structures investment (10.3%) and residential investment (4.6%) also contributed to the overall slowdown in investment in the second quarter. That said, consumption (+1.4%), particularly in services (+1.1%), rebounded in the spring.

The situation appears more reassuring on the personal consumption expenditures price index front, with the annual change easing from 2.5% in the first quarter to 2.4% in the second quarter. There is still little evidence that tariffs are fuelling inflation in the US. Part of the explanation seems to lie in the gap between the tariff actually collected at the border and the one announced by the White House.

Implications

The strong 3.0% (annualized) increase in real GDP partly masks a certain slowdown in economic activity. While not alarming, this moderation illustrates the repercussions of the trade war initiated by the White House. Today’s data further reinforces our view that the US Federal Reserve will likely wait until the fall before lowering its policy rate.