- Francis Généreux

Principal Economist

Economic News

United States: First Decline in Real GDP in Three Years

April 30, 2025

Highlights

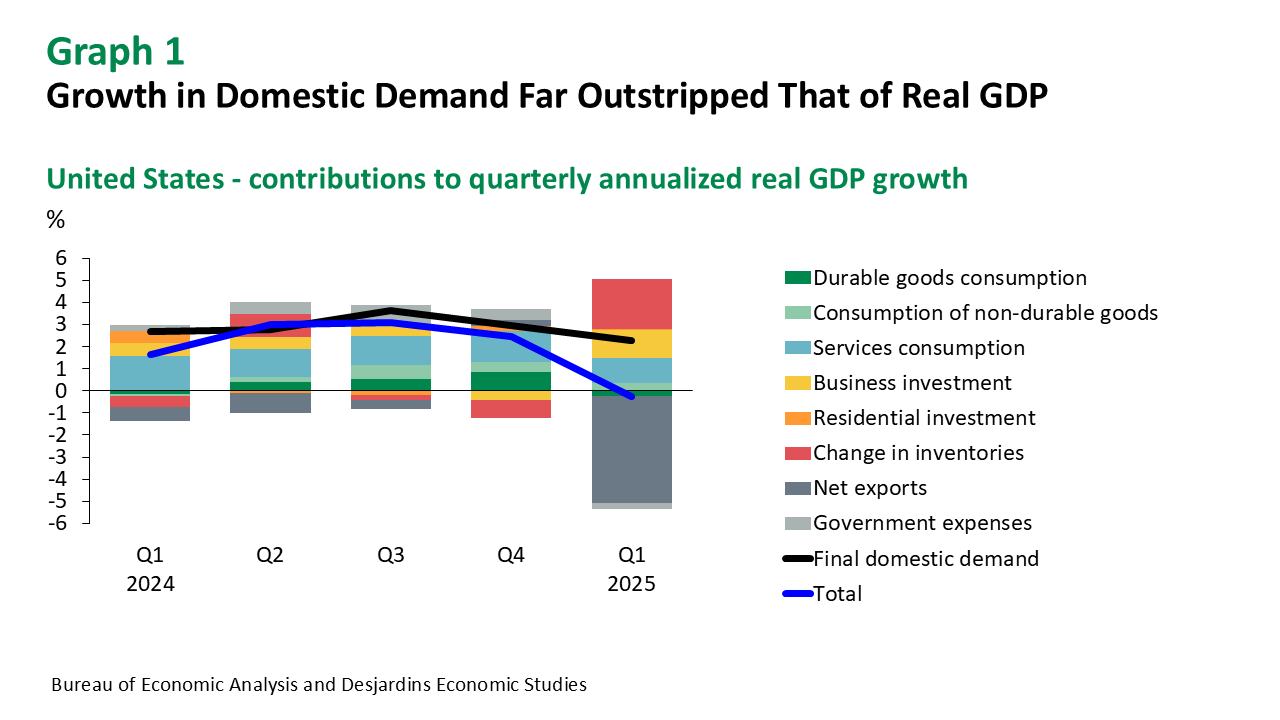

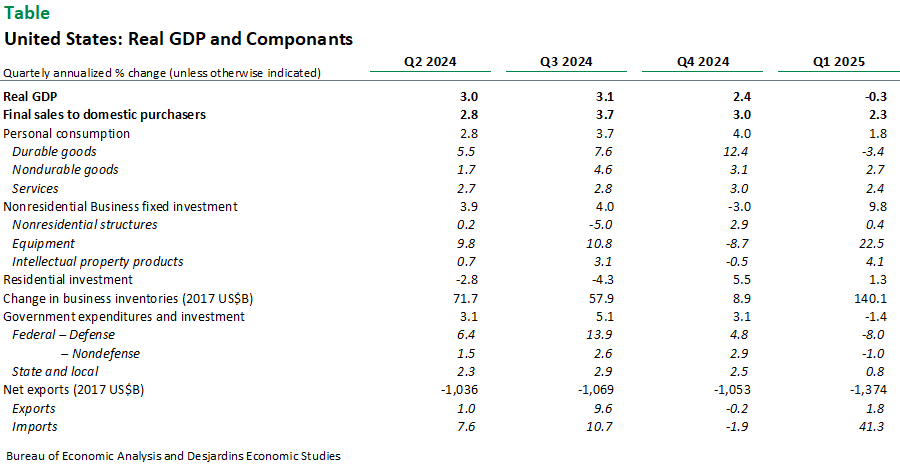

- Real GDP fell by an annualized 0.3% in the first quarter of 2025, according to the advance estimate of the national accounts. This contrasts with annualized gains of 2.4% in the fourth quarter and 3.1% in the third quarter of 2024.

Comments

This is the first time since the winter of 2022 that the US economy has recorded a quarterly contraction. That said, as then, the change in real GDP paints too bleak a picture of economic activity. As in 2022, the fall in real GDP conceals further growth in final domestic demand which grew at an annualized rate of 2.3%. This is relatively slow compared with previous quarters, but it's not catastrophic. It also means that the US economy was not in recession in the first quarter. Despite weakness in durable goods, consumption continued to grow, as did residential and non-residential construction and business investment.

In the latter case, we note the 22.5% gain in equipment investment, the strongest since summer 2011 if we disregard pandemic-related movements. Clearly, however, this momentum is rather artificial and will not last. It must be seen as a significant advance in activity as companies sought to avoid future tariffs announced by the Trump administration. These investments, as well as the US$140.1 billion jump in the change in inventories, are reflected in the 41.3% gain in real imports. However, this frontloading effect is expected to reverse in the second quarter.

Among the weakening factors was a decline in federal government spending. Most of the decline has been in defense, but the 1.0% contraction in non-military spending may be a reflection of DOGE and cuts in certain departments since the arrival of the Trump administration.

What can we expect in the coming quarters? If the recession doesn't seem to have started at the beginning of 2025, it could soon be catching up with the United States. The advance in activity caused by the fear of tariffs will give way to their real consequences. Mirroring what we saw in the first quarter, a foreseeable drop in imports, probably especially from May onwards, will trigger a decline in both inventories and investment. Added to this is the deterioration in confidence and real personal income, which should further undermine consumption. As a result, the next few quarters could also see declines in real GDP, but this time the negative sign will be more consequential.

Implications

The decline in real GDP in the first quarter is not too concerning, but what happens next could be. For the time being, the Federal Reserve is likely to remain on the sidelines again, especially as the consumer spending deflator came in higher than expected in the first quarter. However, when the economic deterioration becomes more evident, rate cuts can be expected.