- Maëlle Boulais-Préseault

Senior Economist

Spotlight on Housing

Quebec’s Real Estate Market Continues to Stand Out, Deepening the Affordability Crisis

July 24, 2025

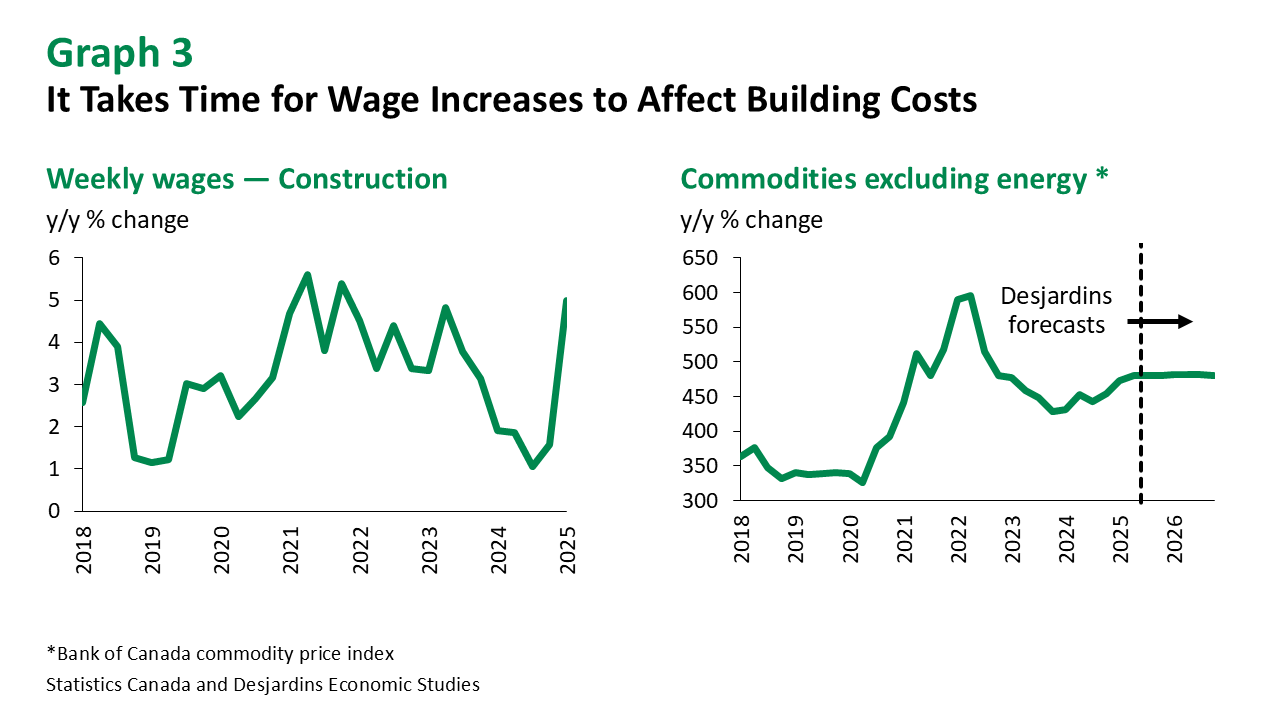

Highlights

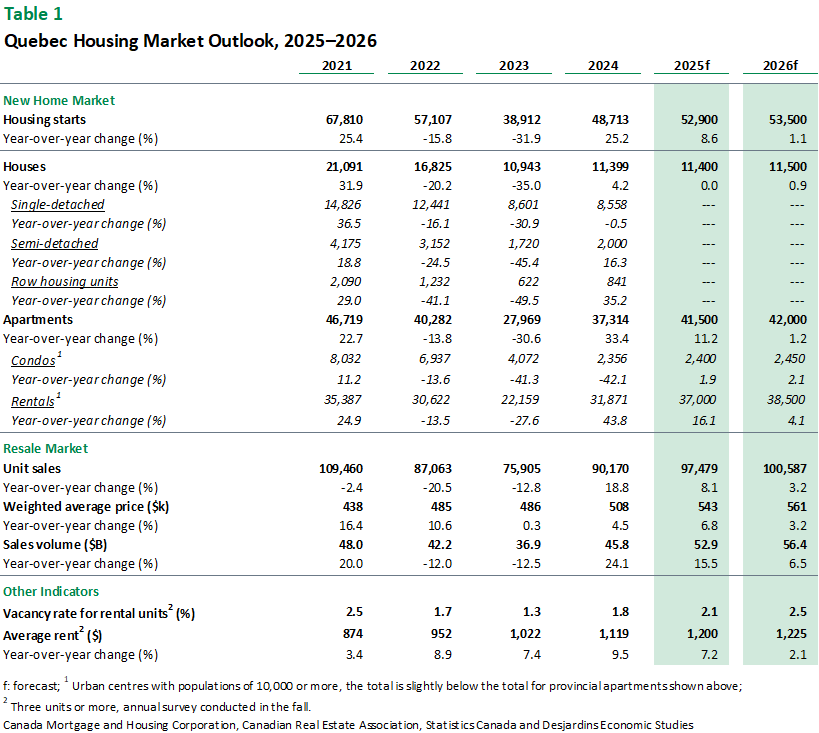

- Despite the considerable uncertainty sparked by the trade war and plummeting business and consumer confidence, Quebec’s real estate market is holding up. It continues to buck the national trend, maintaining its momentum as activity slows in the other provinces. For the first time since 1991, average housing starts in Quebec and Ontario have been about the same over the past six months, even though Ontario’s population is much larger (graph 1). But regional differences are starting to appear in Quebec. Montreal’s real estate market is gradually narrowing the gap with Toronto and Vancouver, as market conditions are shifting towards a balanced market. This stands in stark contrast to the rest of Quebec, where market conditions remain somewhat subdued.

- While housing supply continues to expand across the province, demand is expected to taper off as population growth and the economy slow. Although this dip in demand isn’t expected to last, it may give housing supply a chance to regain some of the ground lost in recent years. But residential construction will have to ramp up even more to restore affordability to previous levels.

Housing Starts

In the residential construction sector, Canada’s retaliatory tariffs on imports from the US are gradually starting to affect costs for builders who rely on materials sourced from that country. Almost half of construction-related goods imports come from the United States External link.. These include engineered wood products, drywall, certain steel and aluminum components and finished goods such as large appliances. Even though many of these items are currently exempt from Canadian counter-tariffs, this may very well change. If that were to happen, higher costs for these materials could lead to increased project budgets and potential delays. The homebuilding industry will likely need to adjust by diversifying supply chains, finding local substitutes and improving its productivity.

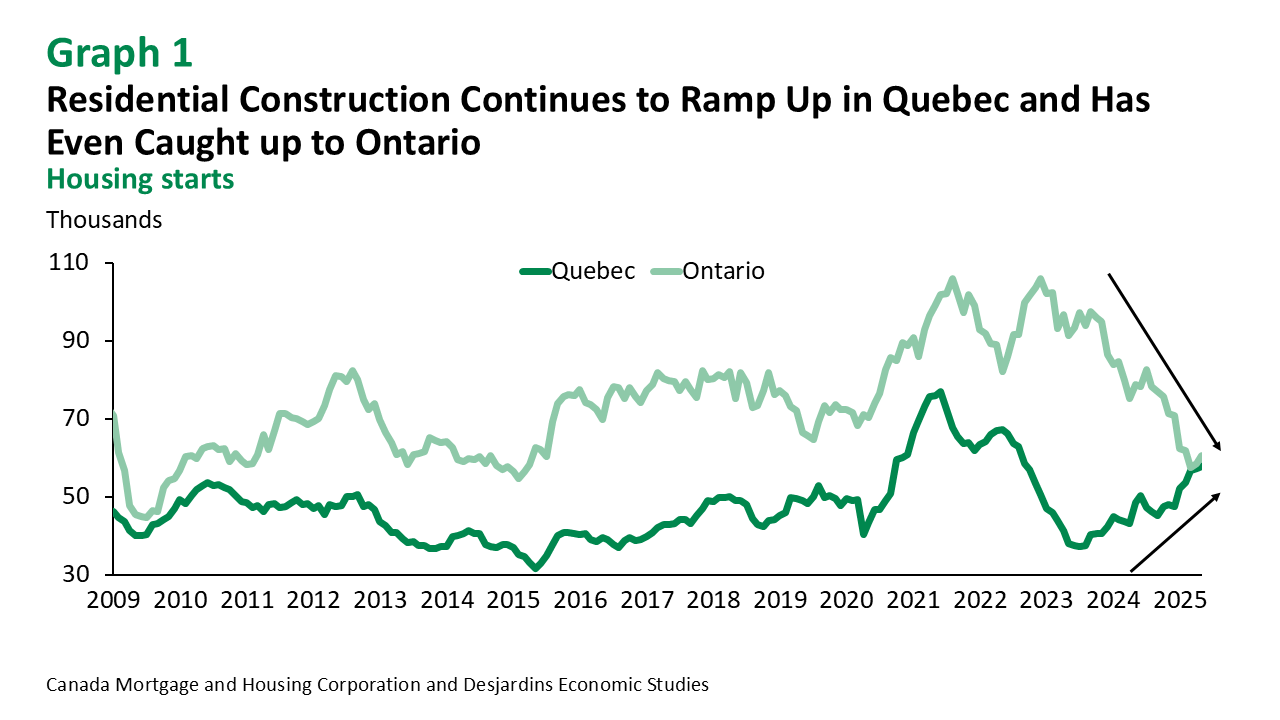

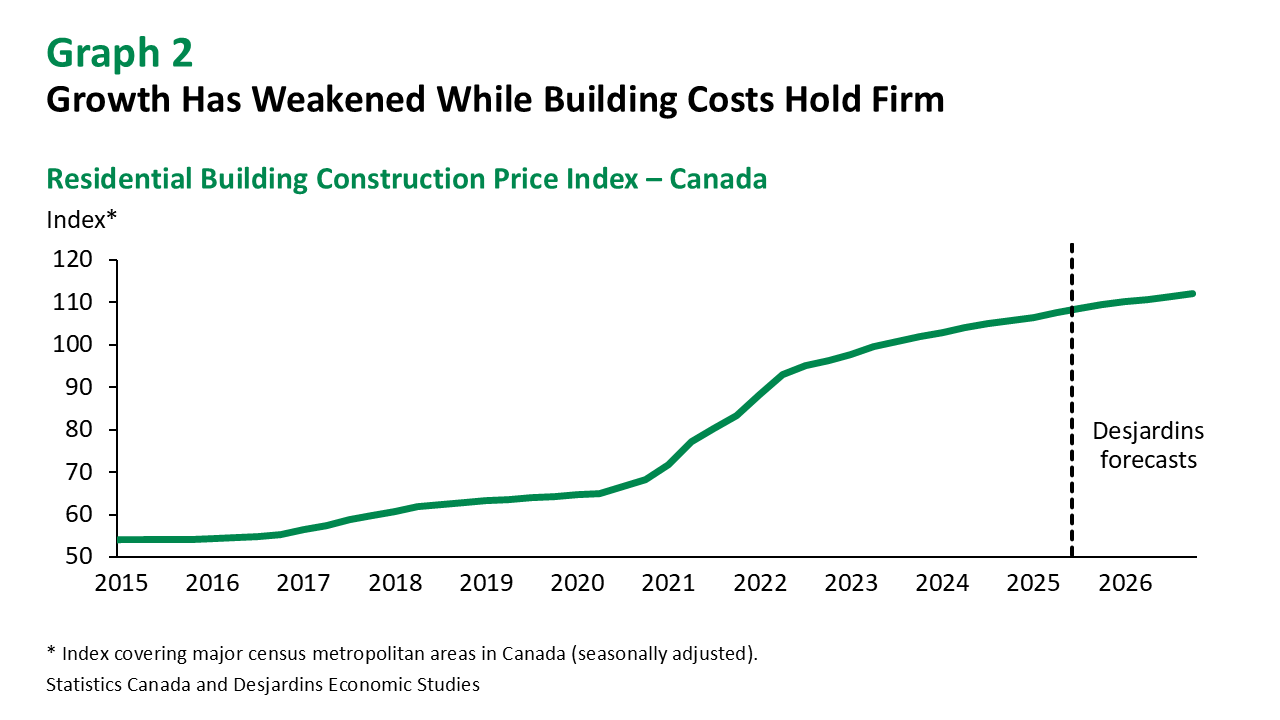

Aside from all that, building costs have stabilized at significantly higher levels than those seen in 2019 (graph 2). In addition, the collective agreements recently reached in the construction industry will increase wages, which will be yet another factor driving up the cost of housing construction (graph 3).

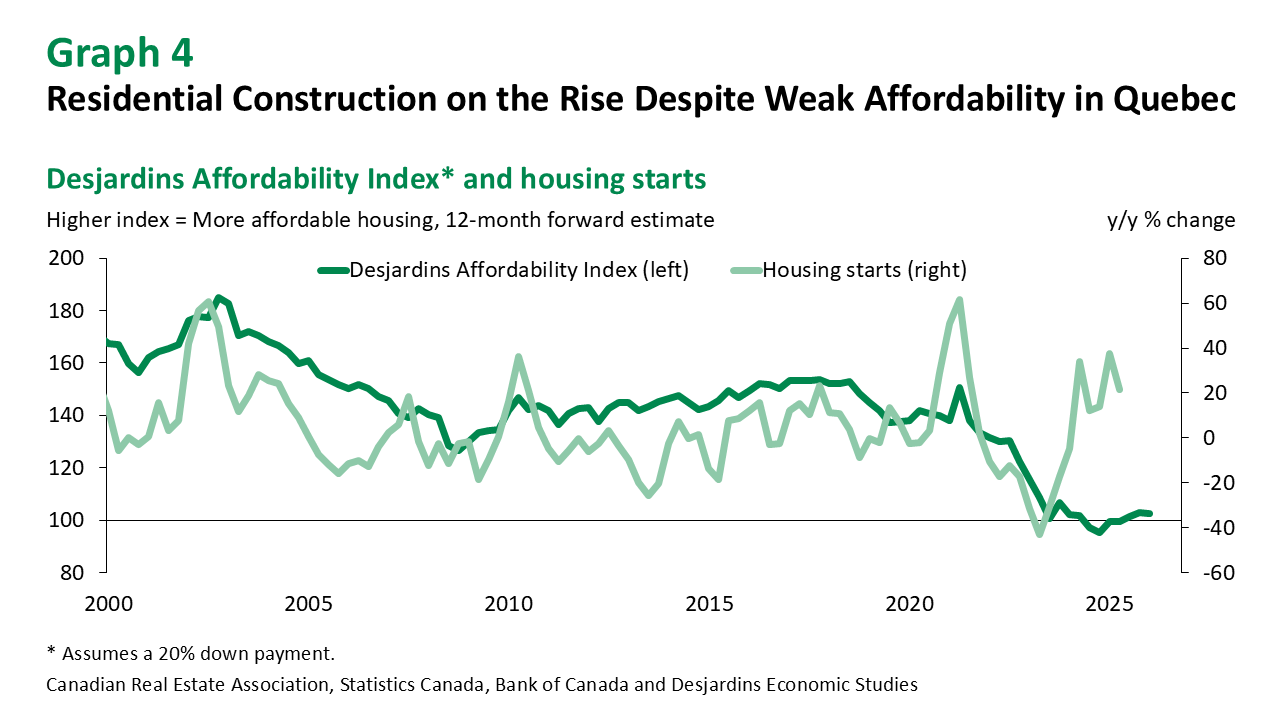

Despite the loss of affordability, housing starts remain robust for now. But that may not last if the market proves unable to absorb less affordable homes, which could deter some builders (graph 4).

While greater supply should help restore balance to the market and ease price pressures over the medium term, an enormous number of homes will need to be built to bring affordability back to pre-pandemic levels.

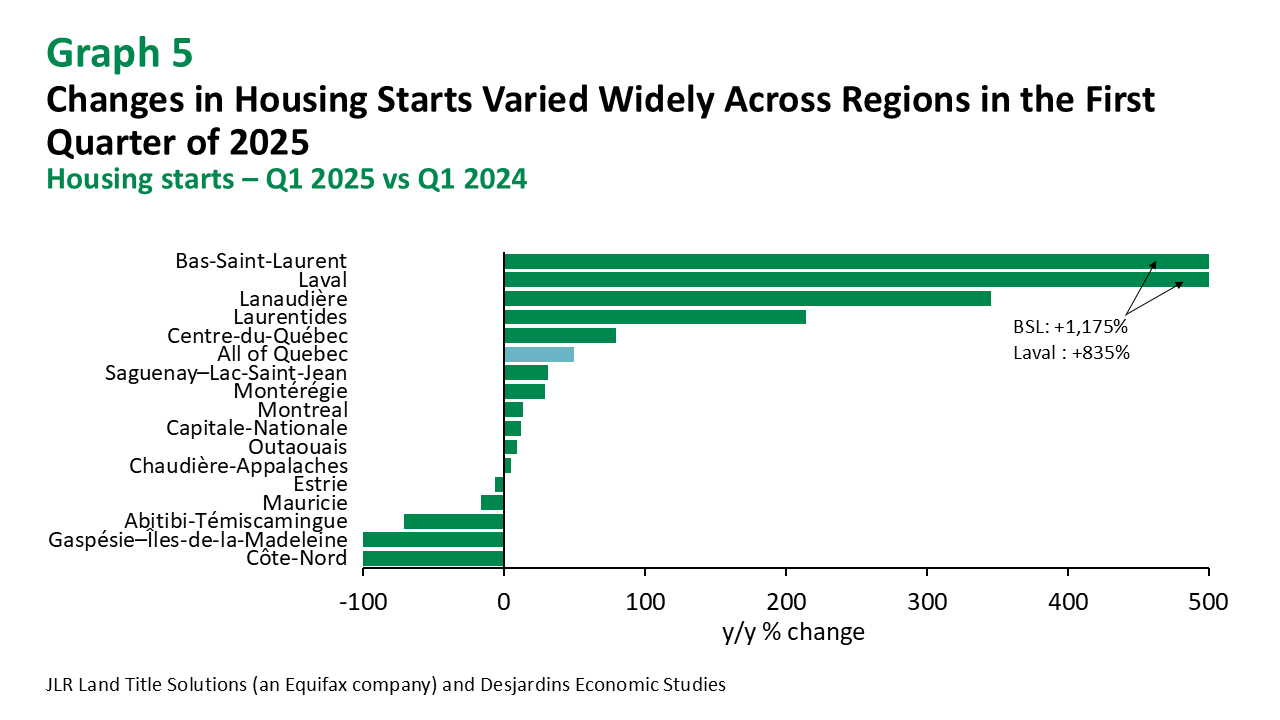

Quebec housing starts vary widely across the regions (graph 5). Municipal involvement affects builders’ eagerness to launch new projects. For example, municipalities that offer tax credits for certain types of construction or other incentives will attract more builders and developers than those that charge development fees. This can be seen in the cities of Rimouski and Rivière-du-Loup, which are both located in Bas-Saint-Laurent. They’re working with a wide range of community members to build large numbers of units, as we can see in the massive upsurge in this region’s housing starts in the first quarter of 2025.

But this kind of rapid construction presents other challenges for cities. For example, many of them don’t have enough water infrastructure for all the new housing units, which is slowing down the pace of construction. Other challenges—such as labour shortages, regulatory constraints and limited land availability—also stand in the way of new housing development.

Quebec’s current pace of residential construction is expected to slow in the coming months as economic uncertainty takes hold. However, measures to increase housing supply have been taken by many municipalities, Canada Mortgage and Housing Corporation and the federal government, like the GST/HST new residential property rental rebate. These measures should stay in place, which will boost residential construction wherever they’re implemented. All things considered, we expect Quebec housing starts to climb nearly 10% in 2025 and then level off in the following years.

Resale Market

The current rate-cutting cycle is encouraging many potential homebuyers, but the shortage of houses for sale is pushing prices to new highs. Bidding wars have even reappeared in the Quebec census metropolitan area (CMA). A lack of inventory appears to be the main reason for higher selling prices in the Quebec CMA.

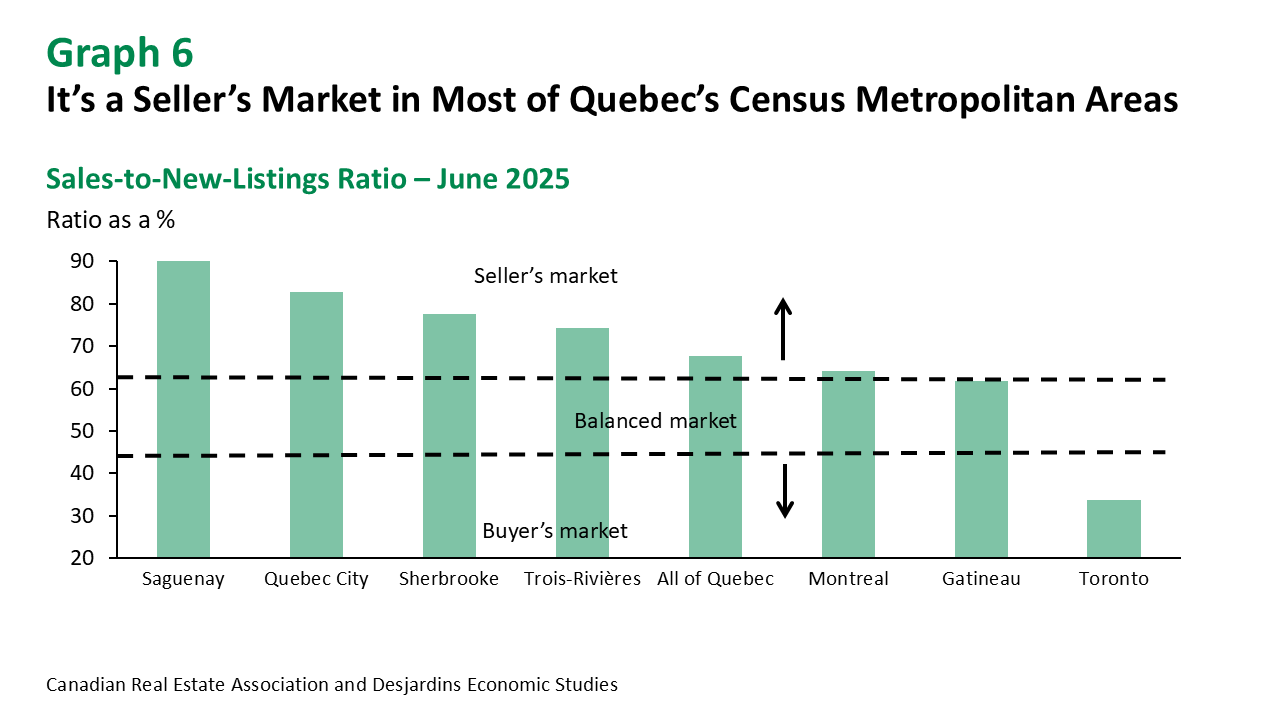

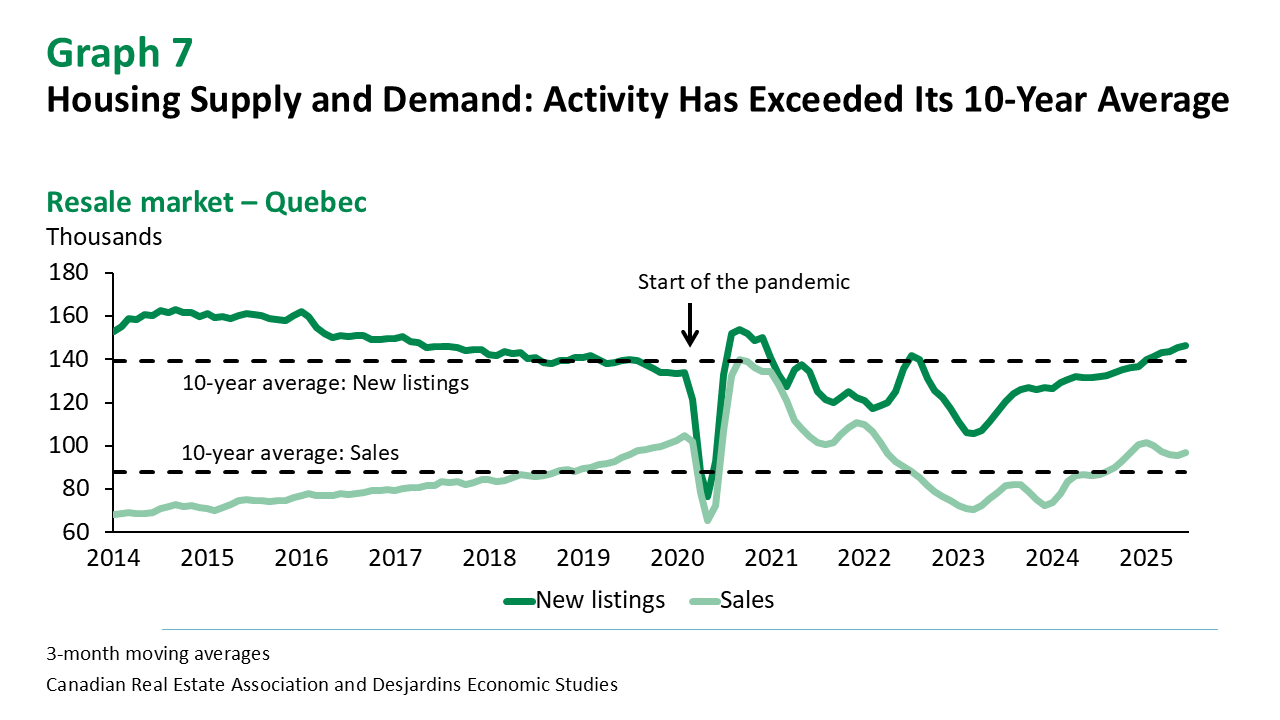

Market conditions remain relatively balanced in the Montreal and Gatineau metropolitan areas, but it’s a seller’s market in most other Quebec regions (graph 6). Sales have outpaced new listings since the start of the year, but now appear to have stabilized. However, listings have been rising since January and have finally exceeded their 10-year average (graph 7).

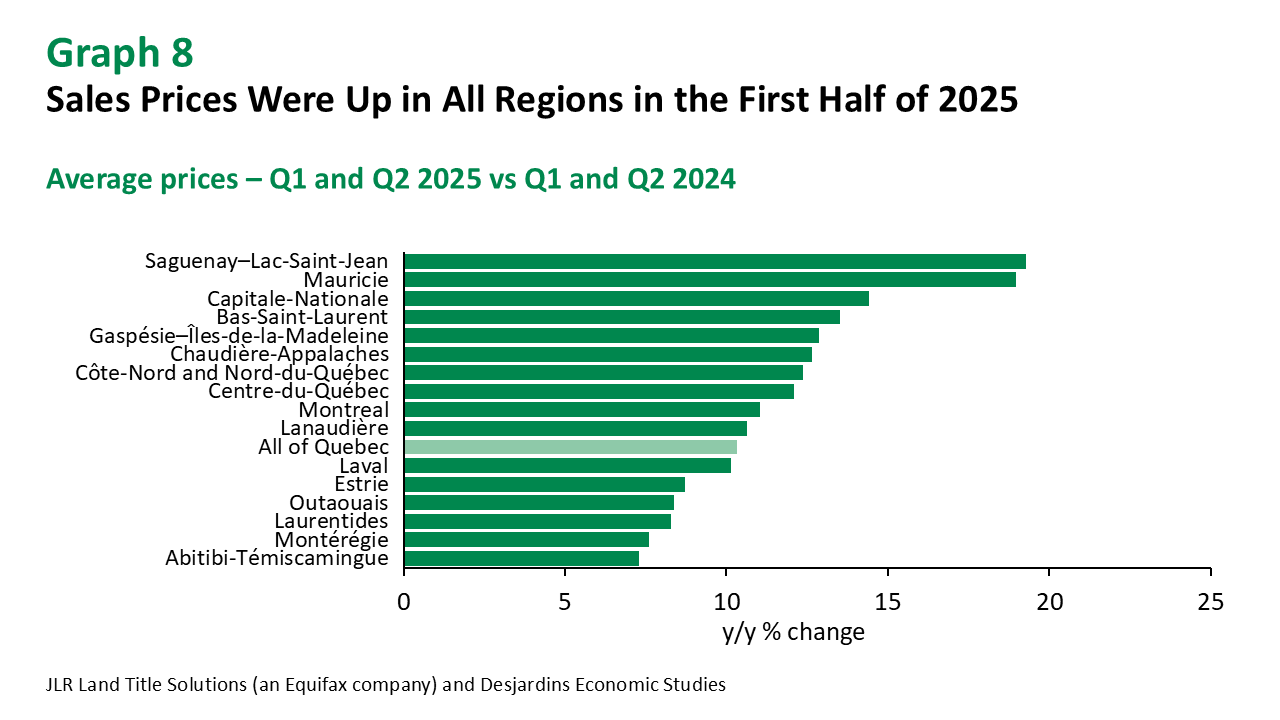

Days on market have also decreased since last year, which is more good news for owners intent on selling their homes. In addition, unlike national home prices, which have fallen, average home prices in all regions of Quebec have climbed significantly in recent months (graph 8).

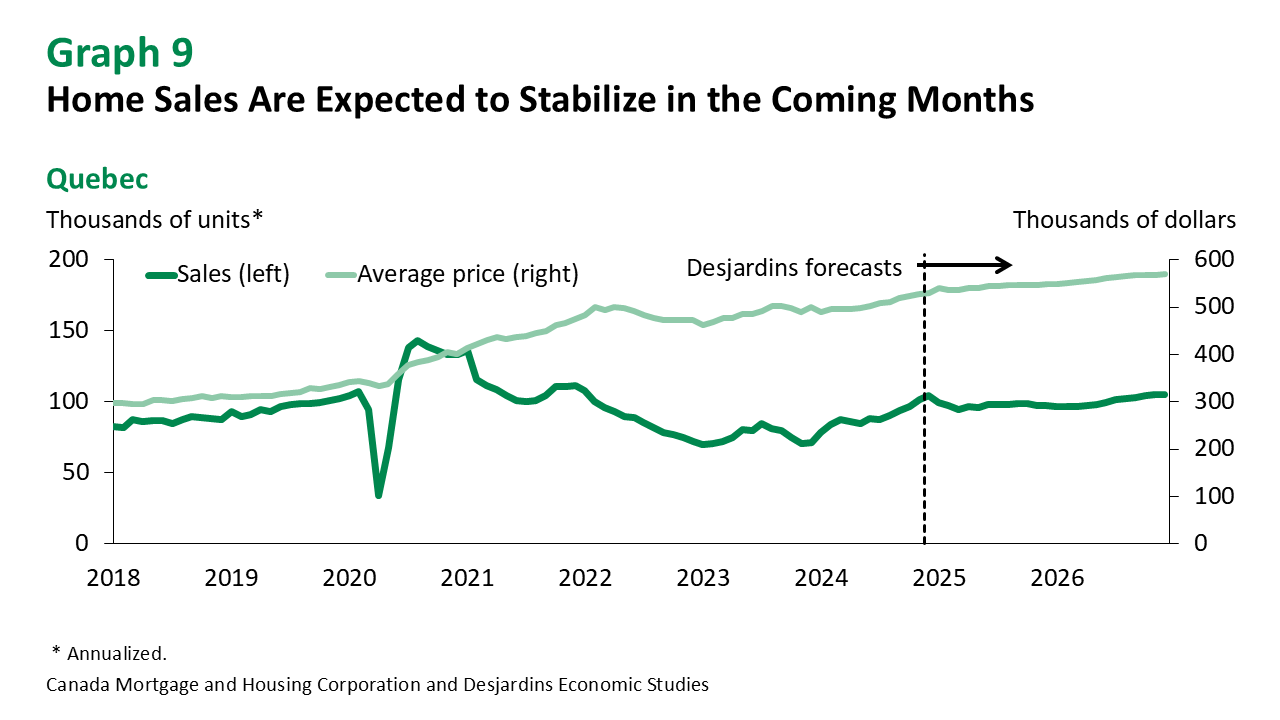

Fading consumer confidence nevertheless suggests resale market activity may slow, resulting in fewer transactions by the end of 2025. The rise in new listings is expected to ease price pressures. Yet prices are expected to remain high and continue to climb, albeit at a more modest pace, through the end of 2025 and into 2026 (graph 9).

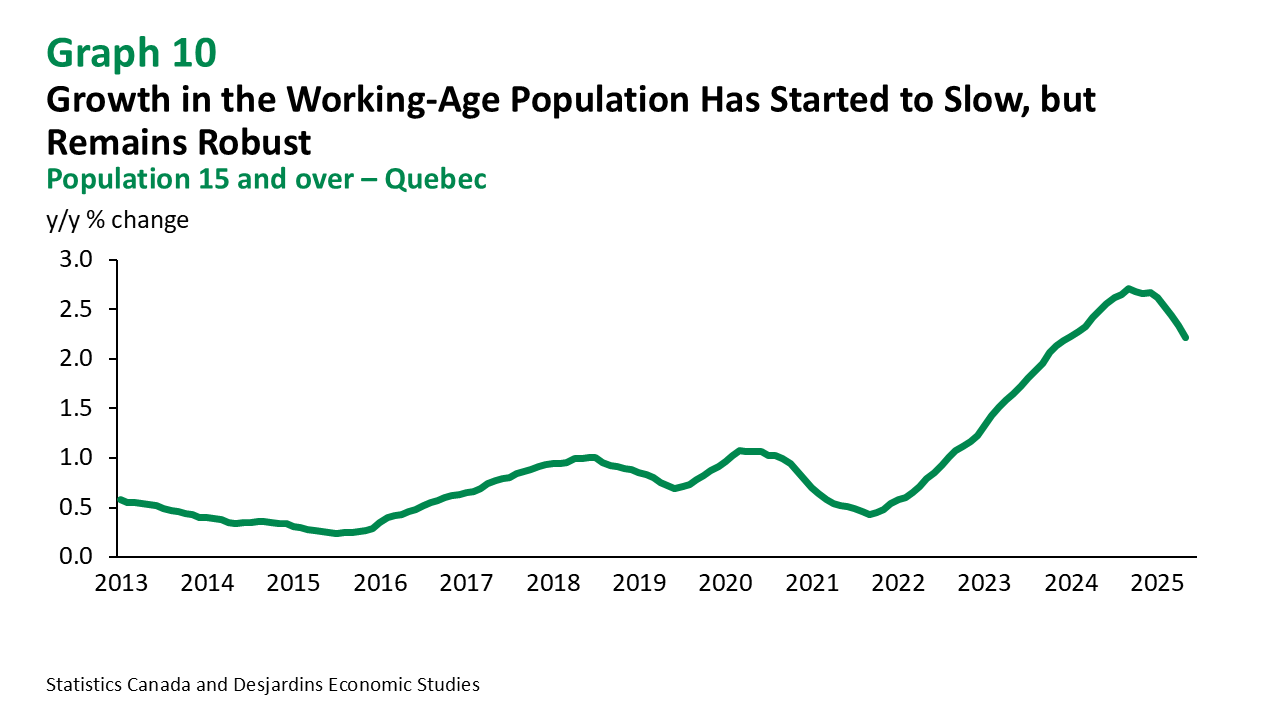

Meanwhile, new federal and provincial regulations on temporary immigration are gradually being implemented, slowing population growth across the country (graph 10). Quebec experienced zero population growth in the second quarter of 2025. This trend will likely continue into 2026, which suggests housing demand will cool over the next several months.

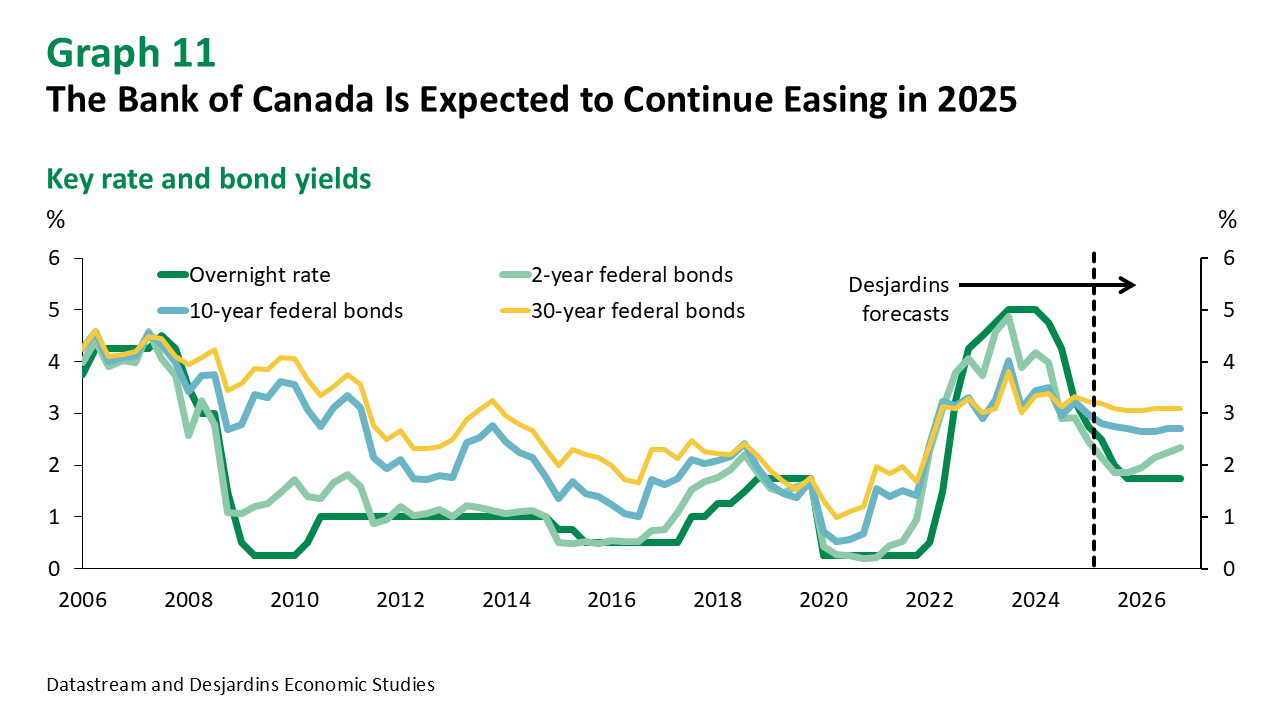

And while our forecasts point to three more Bank of Canada rate cuts by the end of 2025, mortgage rates don’t necessarily move with policy rates.

Usually, variable mortgage rates are immediately affected by changes to key rates. They should therefore decrease if the Bank of Canada cuts its policy rate as expected over the rest of the year.

But fixed rates track government bond yields, which are the benchmark. The bond market tends to move in anticipation of key rate movements, based on investor expectations. Canadian bond yields, and therefore fixed mortgage rates, are also influenced by global events, especially what’s happening in the United States.

Our forecast sees fixed mortgage rates coming down slightly in 2025, but then expects them to stabilize and possibly even go up slightly next year (graph 11). We therefore don’t expect lower mortgage rates to trigger a steep rise in demand over the next year.

Rental Market

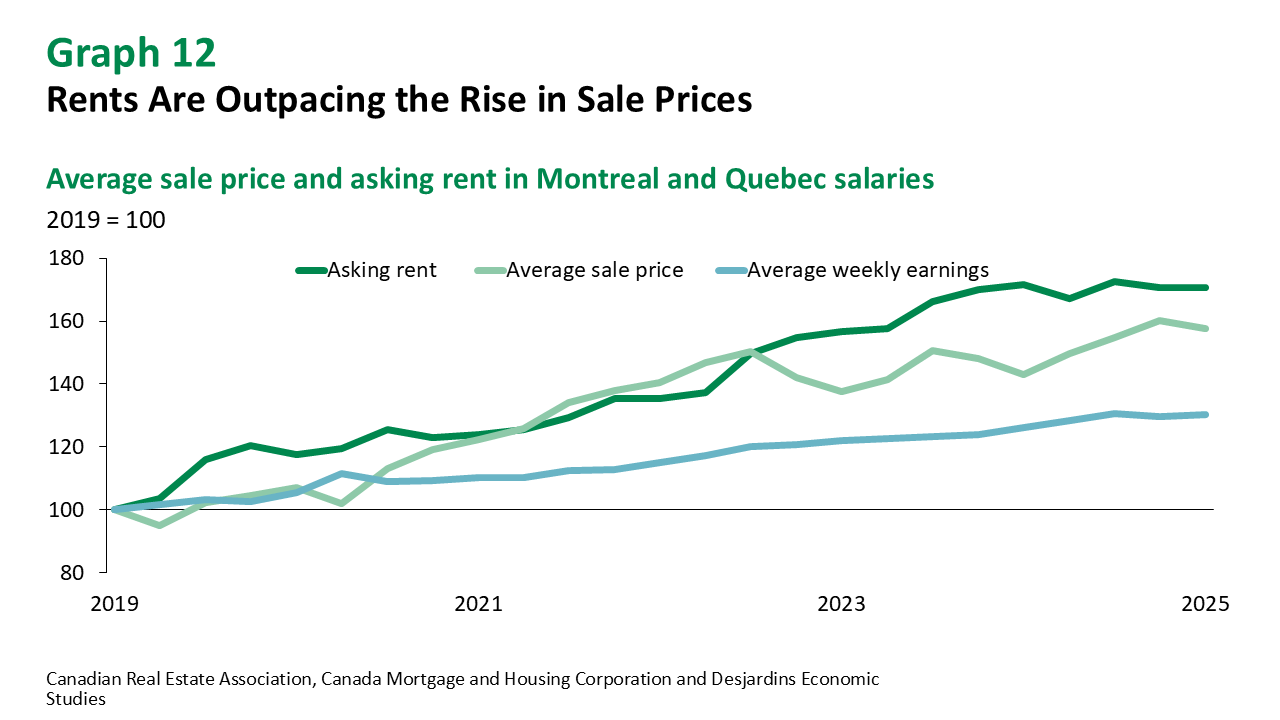

Although the average selling price for homes is going up, rents are rising even faster across Quebec. In Montreal, average asking rents have soared by approximately 71% since 2019, while average sale prices increased by 58% over the same period. Meanwhile, wages have increased by just 30% (graph 12).

The imbalance between supply and demand in the rental market is partly responsible for skyrocketing rents. But the supply of rental units is expanding. More than 80% of housing starts in the first quarter of 2025 were for purpose-built rental units. Greater supply should improve market equilibrium and slow the pace of rent increases from one year to the next.

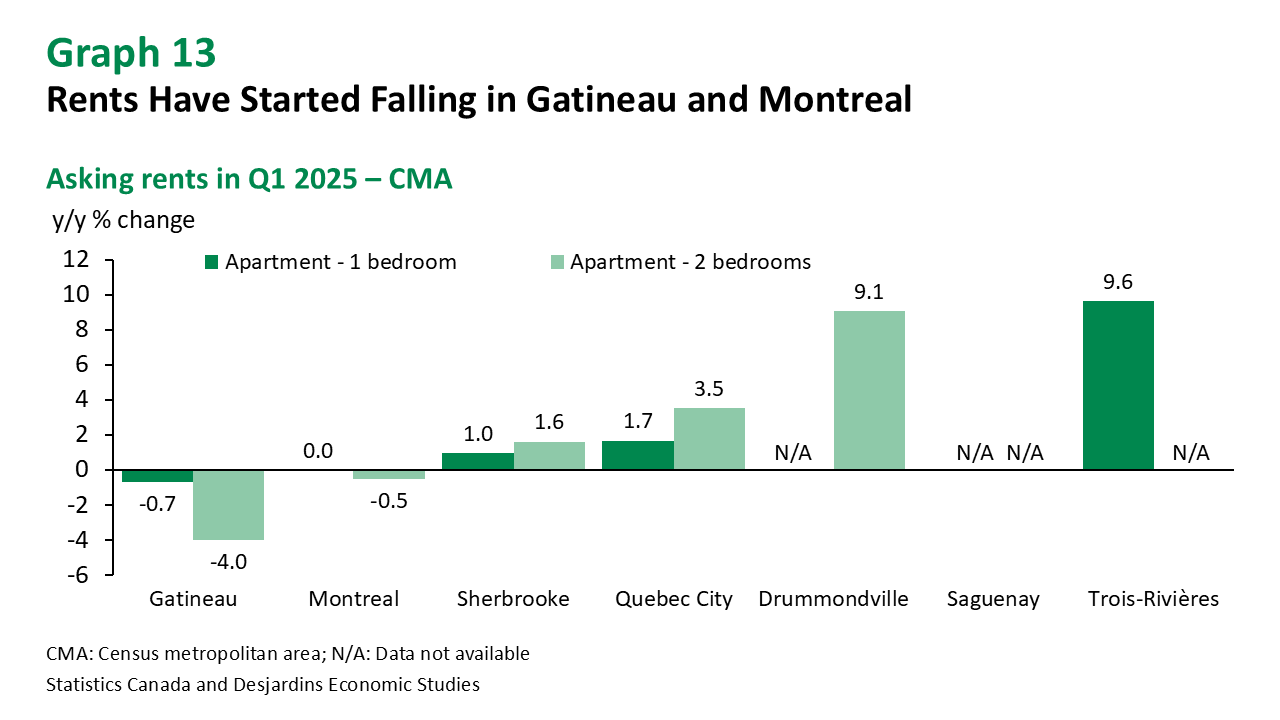

Although rental vacancy rates are gradually rising in Quebec, vacancies for the most affordable units continue to fall. Consequently, affordable rental housing is becoming increasingly scarce across Quebec. But the costs of building rental developments are high, making it hard for builders to fill this gap. Landlords have nevertheless had difficulties renting out higher-priced apartments over the past few months. This has led average asking rents to fall in the first quarter of 2025, especially in the Montreal and Gatineau CMAs (graph 13). This trend has also been observed in several other provinces.

According to Statistics Canada, non-permanent residents, including temporary workers, foreign students and asylum seekers, tend to rent when they first arrive in Canada. This means that when their numbers increase, it drives up demand for rentals. In general, rental unit occupancy rates—defined as the number of dwellings rented per 1,000 people—are higher for non-permanent residents than Canadian-born individuals. But non-permanent residents tend to move out of the rental market the longer they stay in Canada. The population decline mentioned above is expected to reduce demand for rental units in the coming months. Softer demand should help restore balance to the rental market. Meanwhile, slack in the job market—especially among young people, who face higher unemployment rates—will also help cool demand for rental housing over the next two years.

For these reasons, rents could decrease somewhat in the coming months. Landlords will have to adjust their asking rents to the shift in demand.

Conclusion

Quebec’s real estate market seems to be holding up, despite the slowdown in activity elsewhere in Canada. Residential construction is still going strong, as is the existing home market. Despite all this, many challenges remain.

First, the measures implemented to boost housing supply are necessary, but they won’t be enough to improve affordability. The cost of development will keep rising due to the various building costs, labour scarcity, red tape and weak productivity in the construction industry. Although we expect the housing market to naturally return to equilibrium over the longer term, near-term affordability is rapidly deteriorating.

Forecast Table