- Maëlle Boulais-Préseault

Senior Economist

Spotlight on Housing

Quebec’s Real Estate Market Showed Unexpected Resilience in 2025

December 2, 2025

Highlights

- Residential construction in Quebec has surged by 26% so far in 2025, well above the national average, thanks to provincial and municipal measures and a focus on rental housing.

- Rental supply in Quebec is growing quickly, but demand is expected to ease. This shift should help balance the market and limit rent increases.

- Although the economic outlook is uncertain and the rate-cutting cycle appears to be at an end, demand for existing homes remains strong. This continues to push prices higher and reduce affordability, especially in segments popular with first-time buyers.

Comments

As 2025 draws to a close, Quebec’s housing market is still going strong despite the economic turmoil and uncertainty of the past few months. In contrast, several provincial markets elsewhere in Canada have proved less resilient, creating wide disparities across the country External link. even though the national average has remained relatively stable. But activity appears to be gradually picking up in Ontario and British Columbia, two provinces that had been dragging down the Canadian average.

The resilience of Quebec’s housing market has been one of the few bright spots throughout this past year. However, as at the national level, the aggregate data conceals disparities within the province, with activity varying widely from region to region.

Housing Starts

Residential Construction Remains Surprisingly Strong

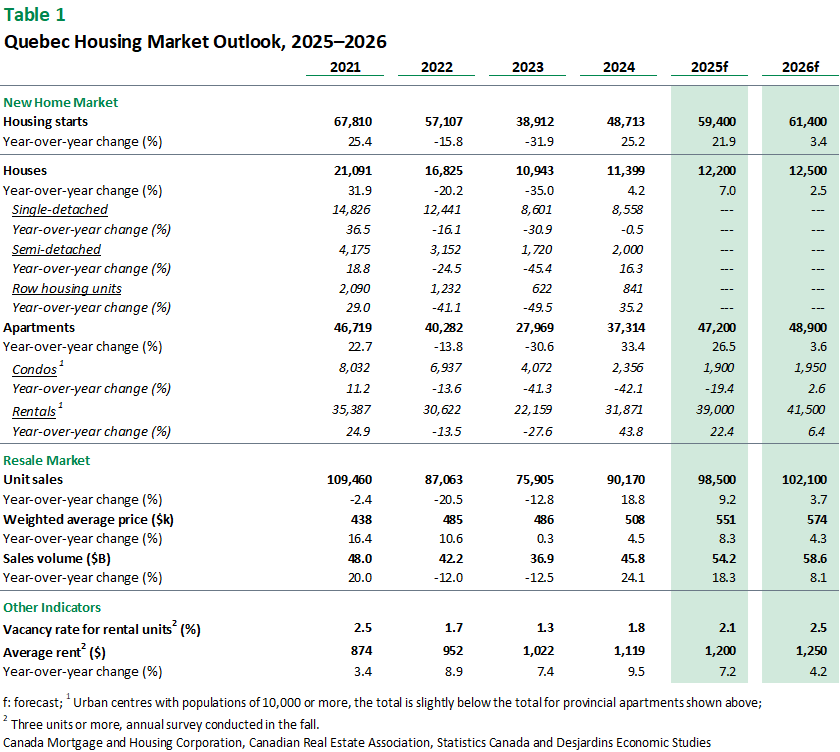

Residential construction has been the most resilient segment in Quebec since the start of the year. It has revved up sharply in the province, with housing starts rising 26% in the first three quarters of 2025 compared to the same period in 2024. This growth stands in sharp contrast with the other provinces. The national average was 6.0% for this period, or just 1.4% if we exclude Quebec. While housing starts appear to be rising again in Ontario and British Columbia, residential construction in both provinces was already so far behind Quebec’s that there’s still a significant lag (graph 1).

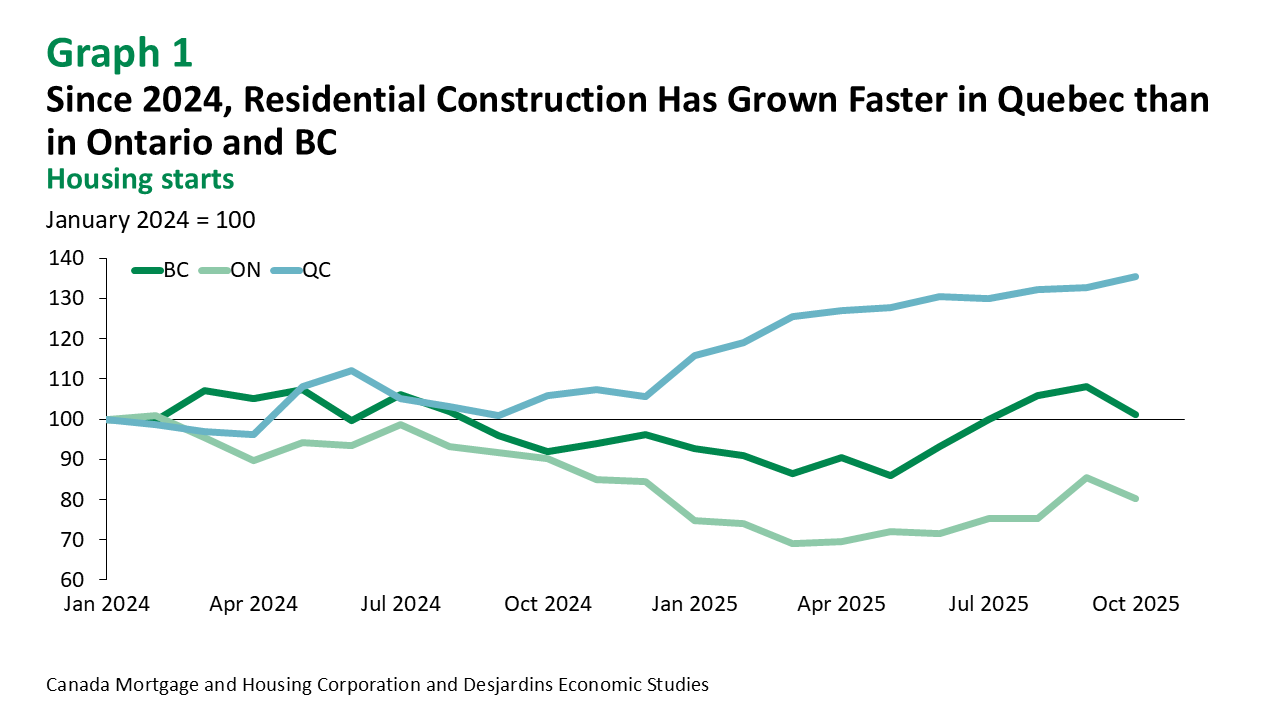

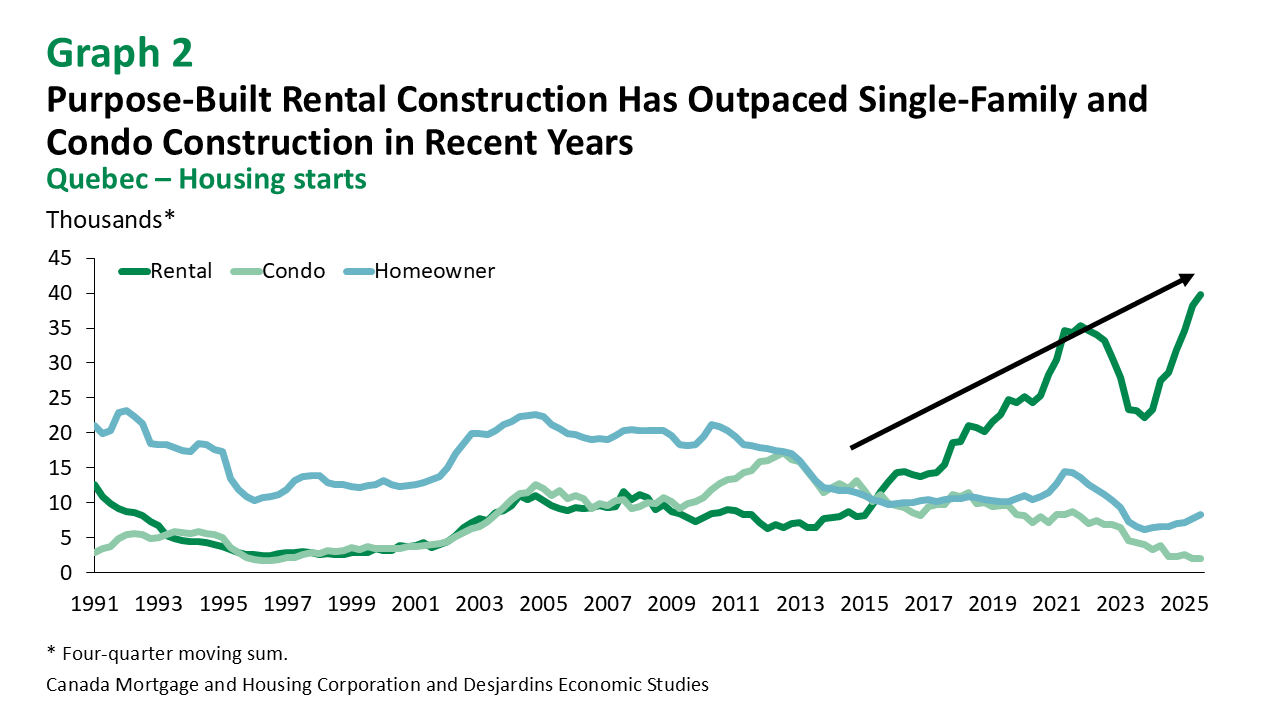

It’s hard to identify exactly why the situation in Quebec is so different from the rest of Canada, but several factors suggest it may be due to the wide array of measures taken by the provincial government, as well as the powers granted to municipalities. Most of this support has targeted the rental market, with nearly 80% of new units built in Quebec intended for rental (graph 2). In Ontario, this figure is closer to 40%. The prevalence of condos in Ontario and British Columbia partly explains Quebec’s stronger performance (graph 3), as purpose-built rentals don’t face the same construction challenges as condominiums.

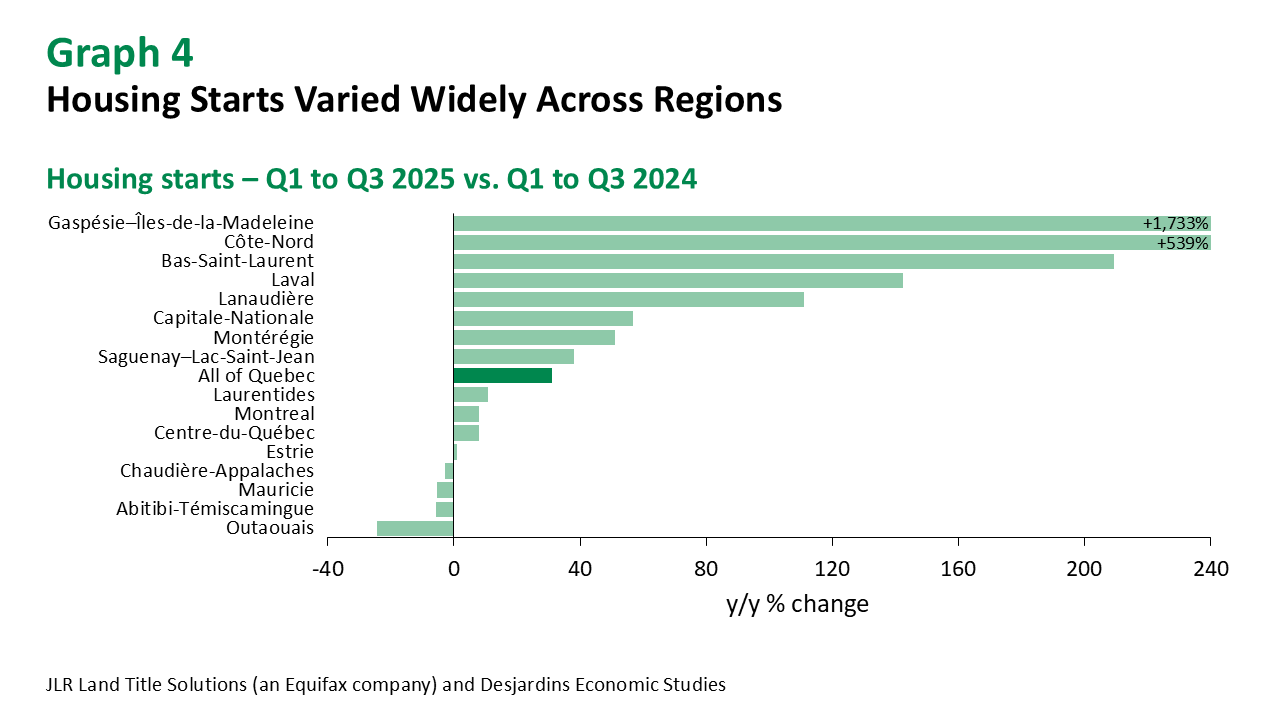

The powers that the Quebec government has granted to municipalities to fast-track approvals of projects that go against their own zoning bylaws have also had an impact. The Ministère des Affaires municipales et de l’Habitation reports that 21 cities used these powers in 2024, leading to the construction of 3,857 units. In 2025, housing starts rose significantly in several cities that have adopted similar measures (graph 4). But the impact of various municipal measures related to residential construction should fade as they expire. The provincial law granting these powers is also slated to expire in 2027.

Barriers to Residential Construction

Another constraint that could slow down construction in many Quebec municipalities is limited infrastructure. Cities like Gatineau, Lévis and Sherbrooke have already imposed moratoriums in some neighbourhoods due to inadequate infrastructure for new housing. The federal government’s latest budget included additional funding for municipal infrastructure, including water and other infrastructure needed to enable housing development.

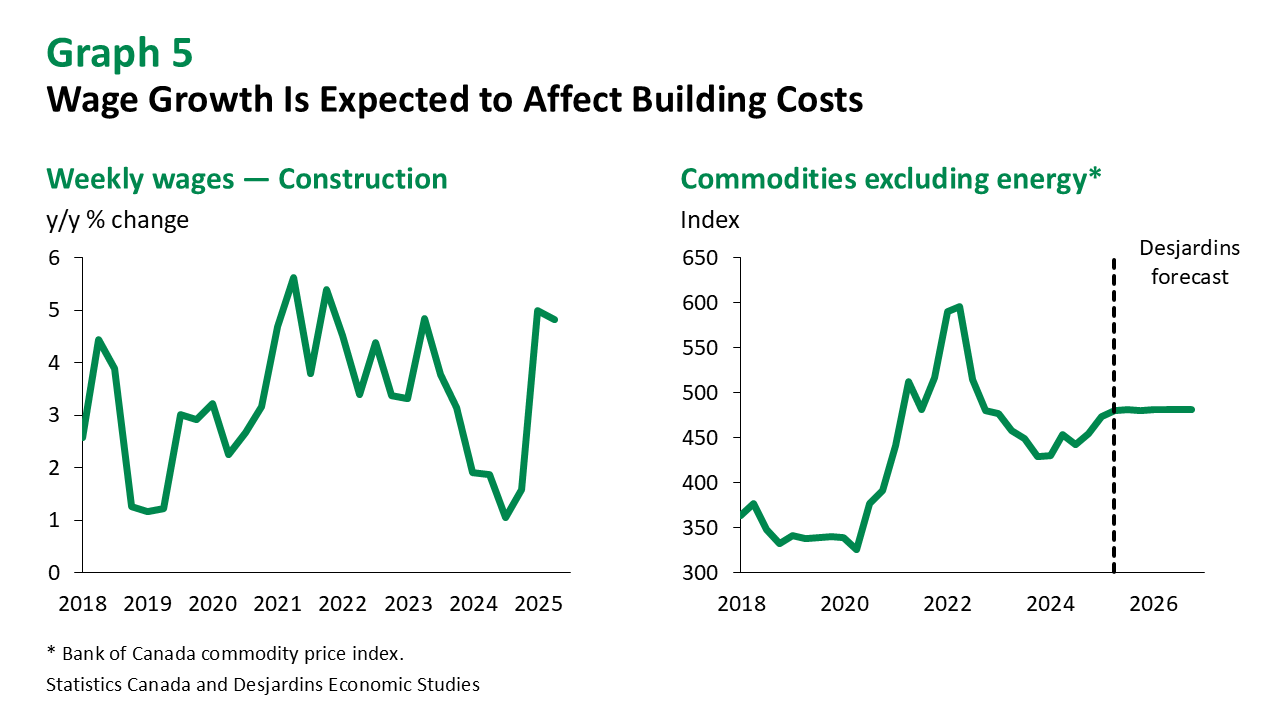

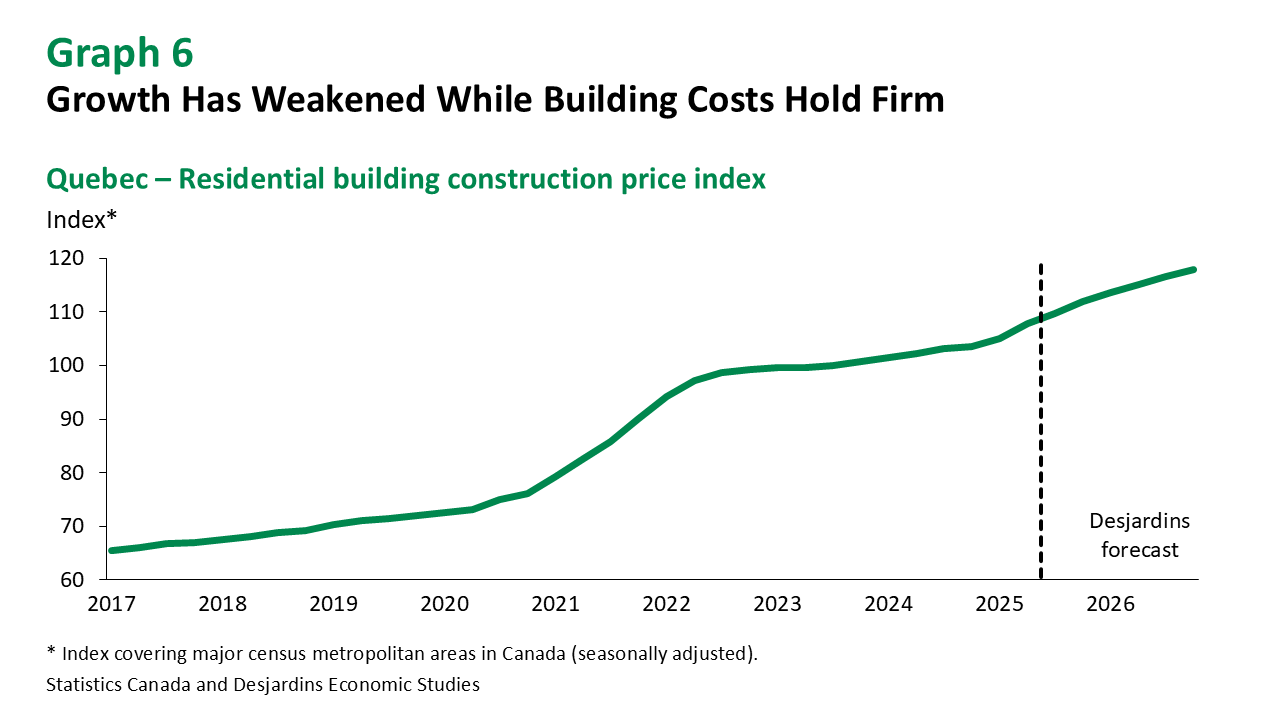

High construction costs External link. may also dampen activity. These costs have recently surged in Quebec, partly due to wage growth driven by strong labour demand and the renewal of collective agreements (graph 5). Although the cost of materials is expected to fall slightly, overall construction costs will remain elevated due to rising wages and strong competition for skilled workers. We see the residential building construction price index (BCPI) increasing by approximately 2% by the end of 2025, followed by a further 5% in 2026 (graph 6).

Technology May Offer a Lasting Fix

New construction technologies should help housing starts remain robust over the long term. Prefabricated and modular construction are becoming increasingly popular. These techniques are less expensive than traditional methods because they use materials and labour more quickly and efficiently, as much of the work is done in a factory setting. Cégep de l’Abitibi‑Témiscamingue is even launching a 3D printing lab to make prefab housing modules.

AI-powered software to improve project planning is also emerging. For example, building information modelling (BIM) is increasingly used in Quebec to improve planning and project management. These tools should boost the industry’s productivity in the coming years and help maintain a brisk pace of residential construction.

Rental Market

A Rapidly Shifting Rental Market

With so many new builds, supply in Quebec’s rental market is growing faster than in other segments. Supported by government incentives, rental housing stock rose nearly 4% in 2024—the biggest jump since 2014. Given that rental housing starts went up by more than 35% in the first nine months of 2025 compared to the same period last year, inventory in the rental market should grow even more this year.

Rental demand is expected to ease over the same period. Non-permanent residents typically rent when they first arrive in Canada, since they’re often not sure how long they’ll stay. Their numbers will fall over the next few years due to recently announced federal and provincial measures to curb immigration. Regions like Montréal and Laval, which have the highest concentrations of non-permanent residents, will feel this shift the most. Further changes to immigration policy could influence future plans for housing projects and increase builder uncertainty.

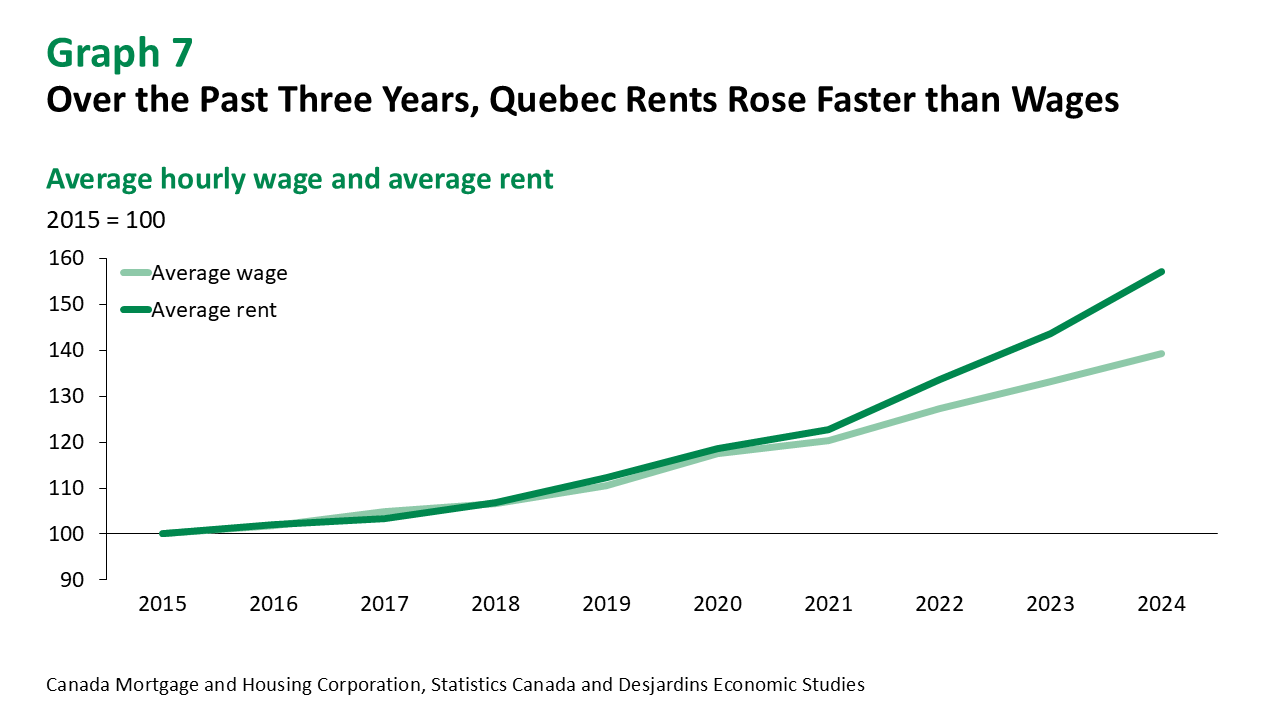

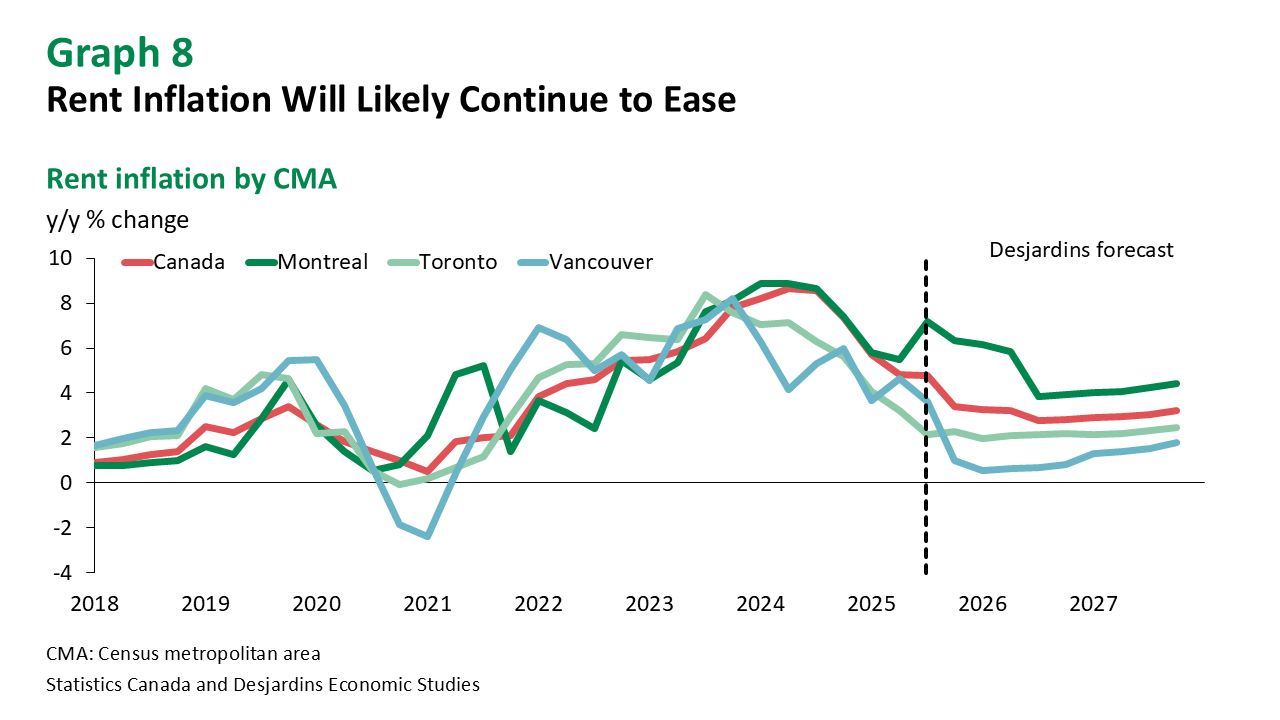

As a result, the Quebec rental market will likely become more balanced, easing rent inflation. Slower population growth and expanding rental supply have already started moderating growth in average asking rents, especially in Montreal. This is welcome news, as the gap between rents and income has widened over the past year (graph 7). Rent inflation is expected to continue to slow External link. through mid‑2026 before gradually accelerating as demand rebounds and new housing supply shrinks due to cost and regulatory challenges. Rent control measures taken by the Tribunal administratif du logement (TAL) will also affect the pace of rent rises across the province and partly explain why slightly higher increases are expected in Montreal (graph 8). Although the TAL has yet to issue its recommended rent adjustment for 2026, its new formula should result in smaller increases going forward.

Resale Market

The Resale Market Could Be the First to Cool

Demand was expected to slow in early 2025 due to weaker consumer confidence resulting from the trade dispute with the United States. But over the past year, prospective buyers in Quebec seemed less concerned than elsewhere in the country, as home sales held up. Transactions continue to rise, and while new listings are also up, strong demand is still pushing prices higher. Although mortgage rates have declined, affordability remains weak.

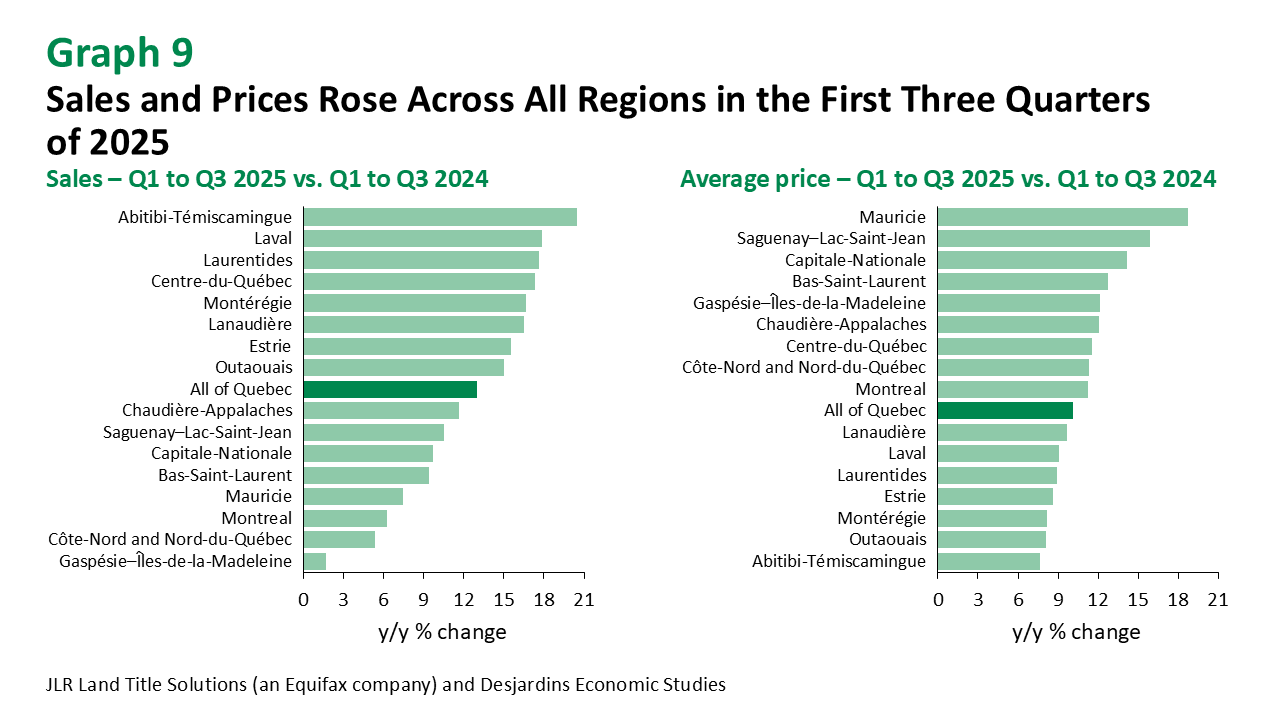

Sales and prices are climbing across Quebec. Inventory is gradually improving in most regions, but price increases are sharper in places where the market has been slower to rebalance, such as Mauricie, Capitale‑Nationale or Saguenay–Lac‑Saint‑Jean (graph 9).

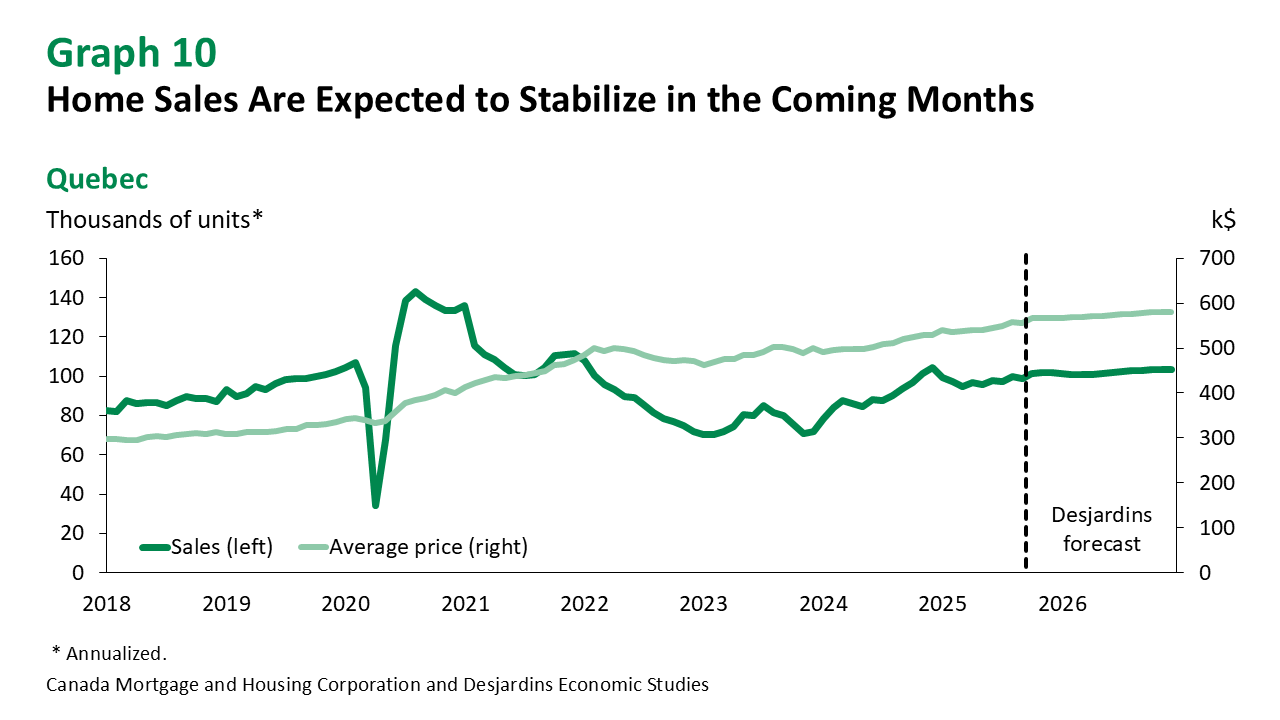

Activity has moderated in recent months, suggesting that uncertainty is finally starting to affect the resale market. Limited supply and affordability challenges are also contributing to this slowdown, which should persist in the coming months (graph 10)—especially now that mortgage rate cuts are no longer boosting demand.

Meanwhile, Affordability Is Taking a Hit

Increased supply should ease price pressures somewhat, but affordability remains very low. Housing starts are concentrated in the rental market, with only 20% of the new units built so far in 2025 destined for sale. That’s why supply in this segment isn’t growing as fast as rental housing. What’s more, the kinds of homes sought by first-time buyers—such as duplexes, triplexes and townhouses, which are usually bigger than condos in towers—are increasingly scarce. Few new builds target this segment, keeping supply tight and prices high. This means home ownership remains out of reach for many potential buyers.

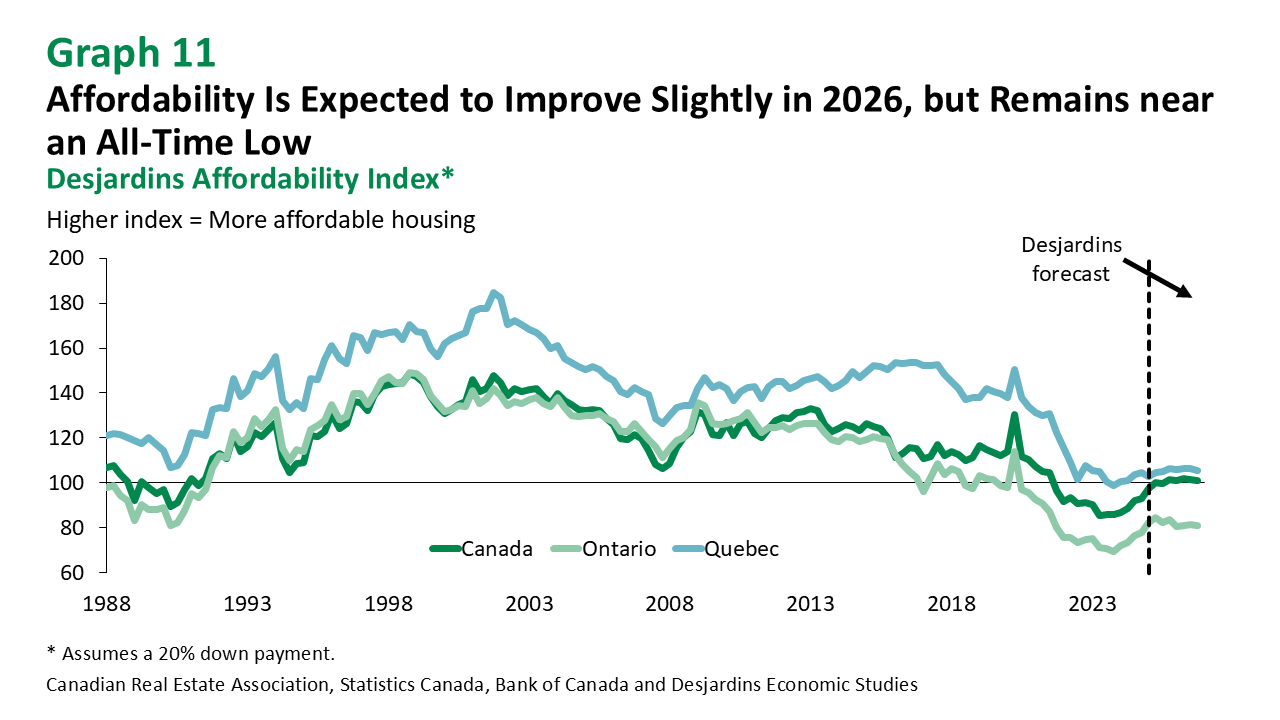

The economic uncertainty of the past year has also pushed up unemployment and slowed growth in household incomes. These factors should also limit any improvement in the affordability index over the next year (graph 11).

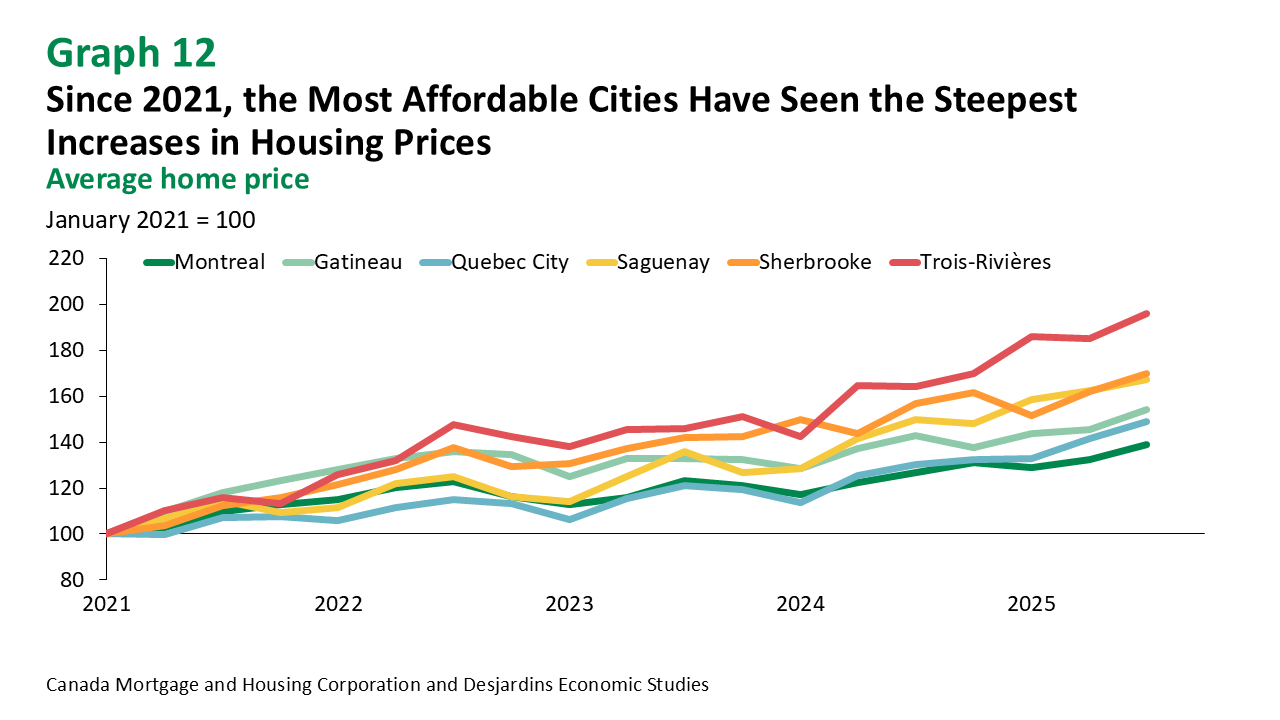

Strong demand has driven especially steep price increases in Quebec’s most affordable cities (graph 12). Between the third quarters of 2021 and 2025, average home prices in the Trois‑Rivières census metropolitan area (CMA) jumped about 70%, compared to 26% in the Montréal CMA. This deterioration in affordability could curb demand in the coming years. The solution is to boost housing supply, focusing on segments that best meet market needs.

Conclusion

The residential construction and resale markets have both shown surprising resilience so far in 2025. Yet Quebec’s strong real estate market should moderate in the coming months given current economic conditions and uncertainty. High construction costs, worsening affordability and inadequate infrastructure in many municipalities will also limit activity.

Price growth should ease in the months ahead, creating opportunities for buyers looking to get on the property ladder. However, persistently high costs and a limited supply of units destined for sale may keep some segments, such as single-family homes and plexes, under pressure. The current economic uncertainty also entails risks that could change our forecast. The way federal and provincial governments implement their immigration policies will directly influence housing demand. As for supply, high construction costs and persistent trade tensions with the United States could discourage developers from investing despite incentives to boost new residential construction.

In the medium term, the market’s trajectory will depend as much on governmental ability to support residential investment and improve infrastructure as it does on changing economic conditions.

Forecast Table