- Sonny Scarfone

Principal Economist

Current economic conditions in Quebec and Ontario

Quebec Quarterly GDP

The sharpest quarterly contraction (excluding the pandemic)

since 2009

September 24, 2025

Highlights

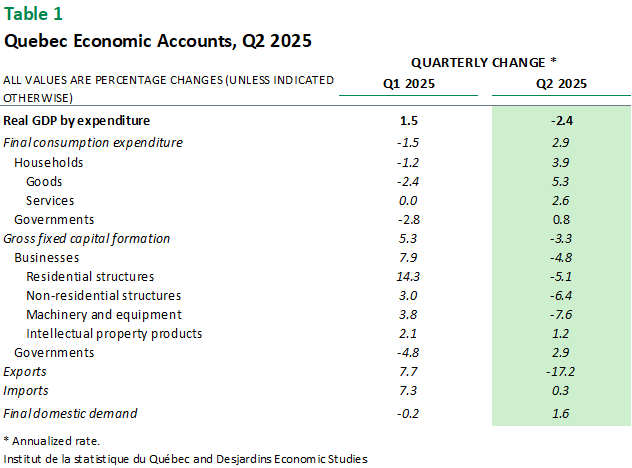

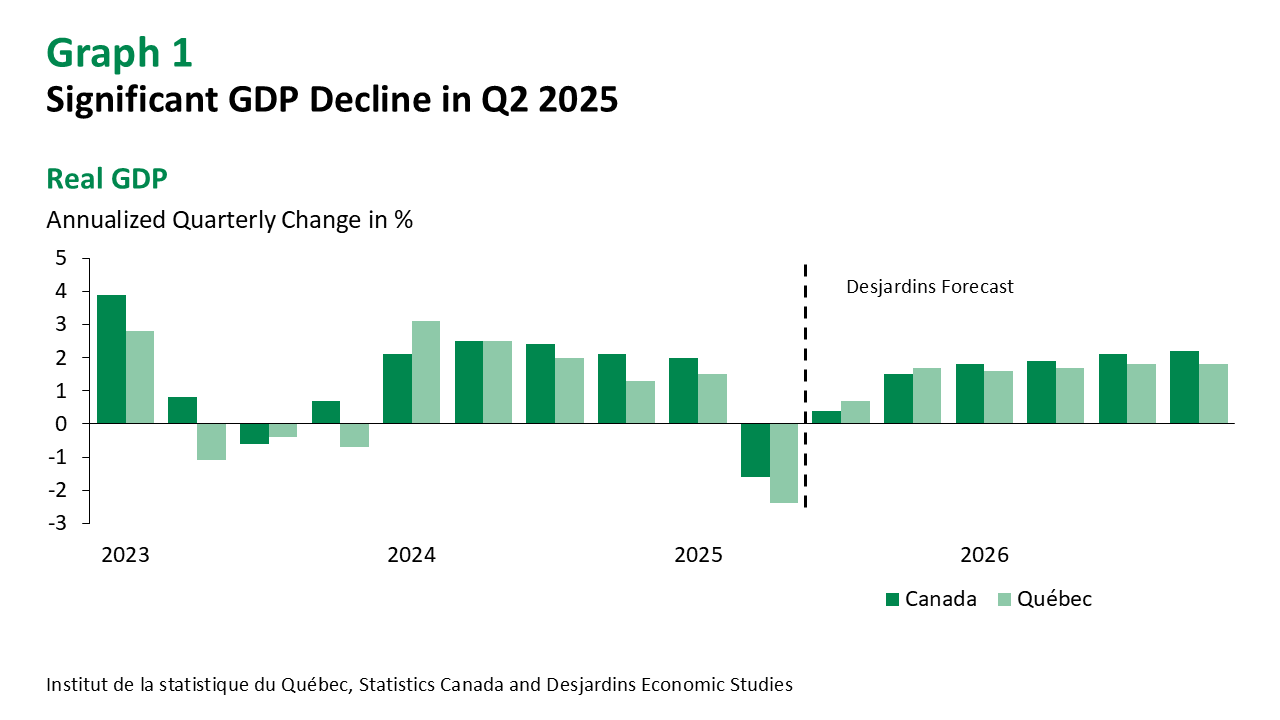

- In the second quarter of 2025, Quebec’s real GDP fell by an annualized 2.4%, marking the steepest decline outside of the pandemic period since the first quarter of 2009. By comparison, Canada’s overall real GDP contracted by 1.6%.

- As expected, international trade was the main drag on growth. Exports dropped by 17.2%, while imports edged up by 0.3%. International exports plunged by 28%, whereas interprovincial exports posted a modest gain of 2.9%.

- Domestic demand, however, returned to positive territory with a 1.6% increase, supported by strong household consumption (3.9%) and higher public sector investment spending (2.9%). Business investment declined by 4.8%, reflecting a pause in certain projects amid heightened uncertainty (see Table 1).

Comments

Quebec’s economy was not spared. The 1.5% growth recorded in the first quarter (revised down from the initial estimate of 2.1%) was largely driven by a temporary increase in exports ahead of anticipated tariffs that were expected to take effect in early April (see Graph 1). Although the cumulative tariffs imposed to date have been lower than forecast, thanks in large part to exemptions under CUSMA, the front-loading of shipments combined with the negative impact of heightened uncertainty led to a sharp 28% drop in international exports of Quebec goods (all figures annualized).

On the industrial production front, the most affected sectors included manufacturing (-11.6%), wholesale trade (-4.9%), and transportation and warehousing (-1.5%), all impacted by the unfavourable trade environment. Mining extraction (-10%) and utilities (-20.7%), mainly electricity generation, transmission, and distribution, also weighed on GDP.

Quebec consumers helped soften the impact by increasing their spending on durable goods (15.2%), semi−durable goods (7.2%), and services (2.6%). In contrast, consumption of non-durable goods declined by 0.6%, reflecting the effects of slowing demographic growth.

The labour market is showing signs of stagnation External link., which is also evident in private investment, as several projects have been put on hold. As a result, business investment declined by 4.8%. In contrast, public administrations ramped up their investment spending (2.9%), in line with commitments made in the Quebec government’s latest budget.

Implications

Quebec’s open economy, which relies heavily on international trade, was inevitably affected by the rise in protectionist measures from its main trading partner. While the direction of this policy remains uncertain and continues to impact strategic sectors such as aluminum, preliminary data for the third quarter suggest that the cyclical trough was reached in Q2. Our updated forecasts, to be released tomorrow, outline the factors supporting the moderate rebound expected over the remainder of 2025, which is projected to extend into early 2026.