- Sonny Scarfone

Principal Economist

Weekly Commentary

Quebec Is Meeting Its Fiscal Targets Despite Economic Softness

October 3, 2025

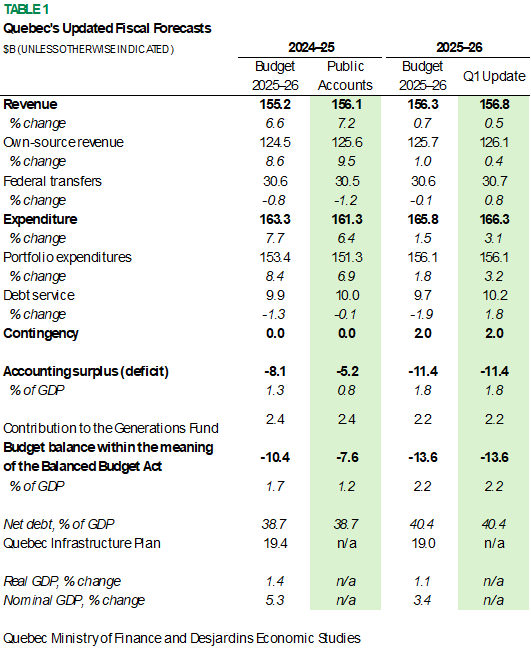

Last week, the Quebec government published its public accounts for the 2024–2025 fiscal year (FY25). The estimated deficit for that year narrowed, falling from $8.1 billion to $5.2 billion before contributions to the Generations Fund. This brings the deficit to 0.8% of GDP. This fiscal improvement, first hinted at in the preliminary results released in late June, is driven by both stronger own-source revenues and lower‑than‑expected spending (table 1). The province’s net debt remained unchanged at 38.7% of GDP.

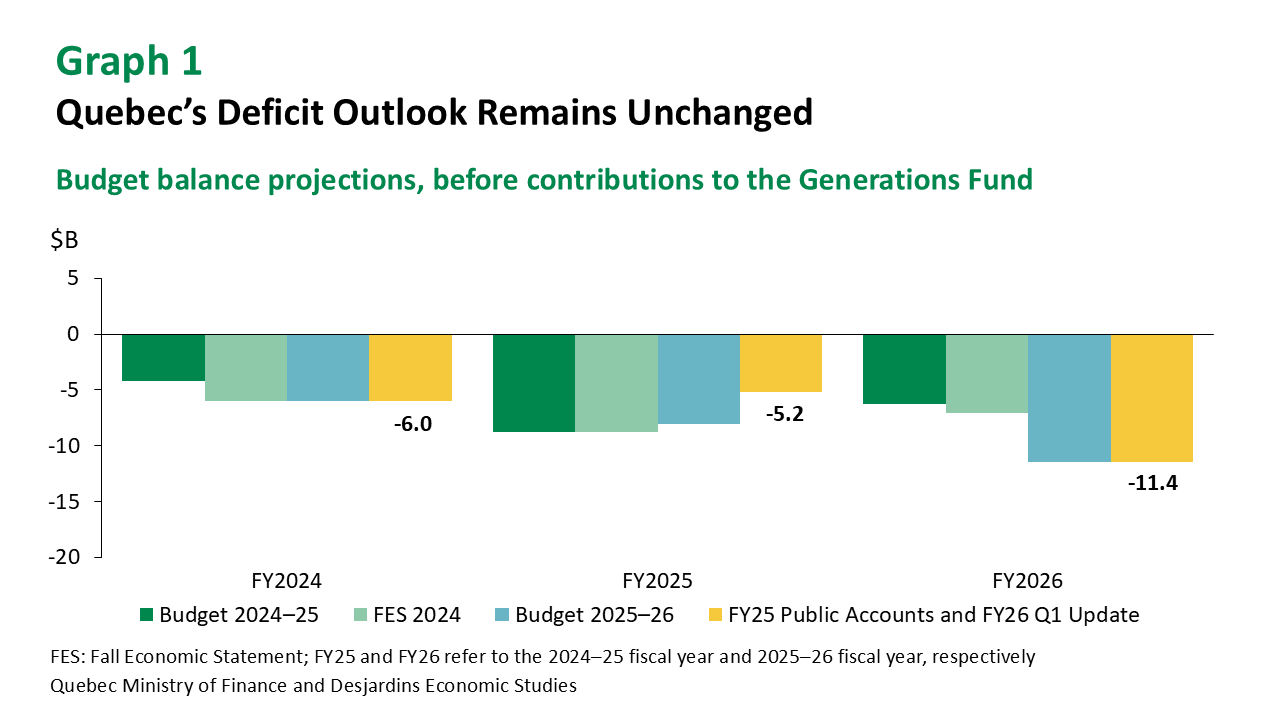

On the very same day, the Quebec government released its Q1 fiscal update (April to June) for the 2025–2026 fiscal year (FY26). The projected deficit remains unchanged at $11.4 billion, or 1.8% of GDP (graph 1). The steady headline deficit number reflects relatively modest revisions within its components: higher revenue projections are being offset by increased spending in the education sector and higher debt servicing costs.

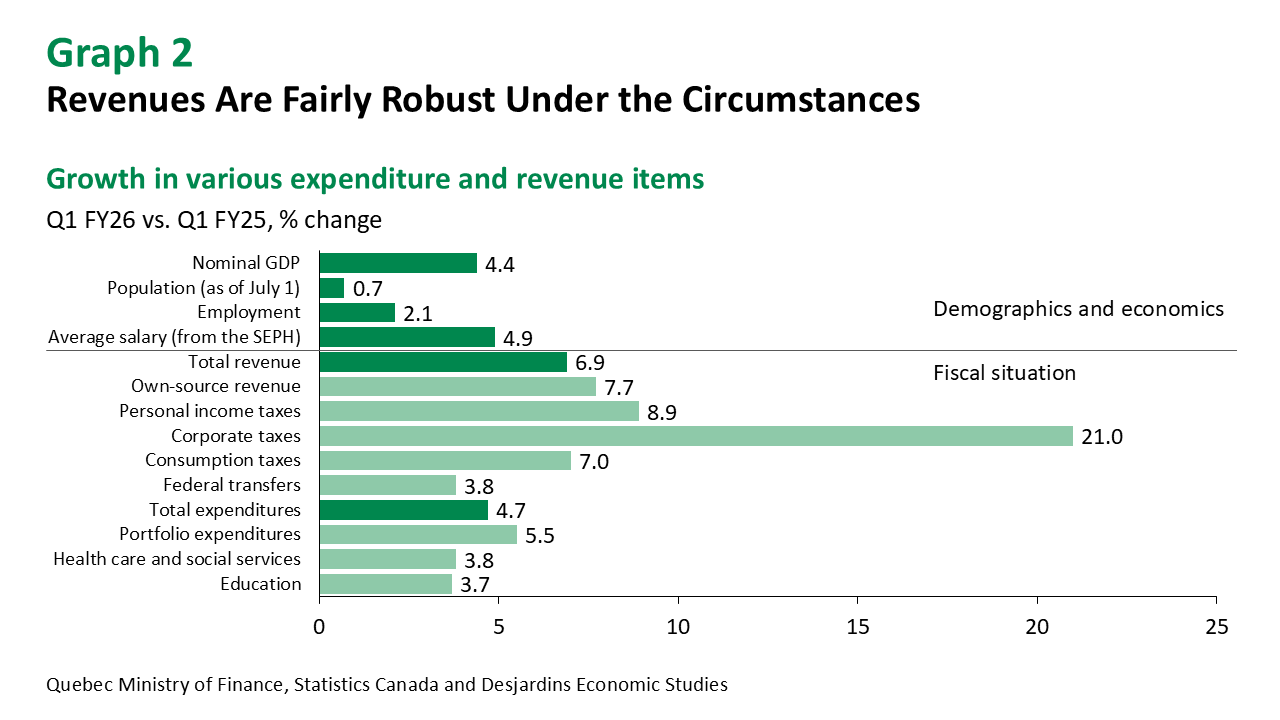

This fiscal stability stands in contrast to the economic softness observed in those months External link., when Quebec’s GDP contracted at an annualized rate of 2.4%. Despite this slowdown, government revenues have held up well, underpinned by a resilient labour market. From April to June, personal income tax revenues rose 8.9% year over year, in line with the cumulative growth in employment and wages in the preceding 12 months (graph 2). QST collections increased by 7.0%, reflecting strong domestic demand. Corporate tax revenues also posted a solid gain, up 21% compared to the same period last year. Altogether, revenue for FY2026 has been revised up by $480 million, including $350 million from own‑source revenues and $130 million from federal transfers.

Portfolio expenditures rose 5.5% year over year. However, the overall spending forecast for FY26 remains unchanged, as a $250 million increase in education from the March budget was offset by an equivalent, but unspecified, reduction in “other portfolios.” Meanwhile, debt service charges have been revised upward by $480 million, mirroring the increase in total revenue. This adjustment reflects changes in long‑term interest rates since the budget was tabled in March.

Looking ahead to the rest of FY26, the balance of risks appears skewed towards smaller deficits. Revenue has remained stable despite signs of economic contraction, and an economic upturn is plausible and remains our baseline scenario for the rest of the year. In the first quarter, expenditures followed their usual seasonal pattern and were on track to meet the targets set for March 2026. Based on this latest update, spending should still allow this year’s budget targets to be met in the midst of a marked slowdown in demographic growth (population up just 0.7% year over year as of July 1, graph 2).

The unchanged $2 billion contingency reserve should be sufficient to absorb remaining downside risks. But looking beyond FY26, substantial revenue and expenditure adjustments will still be needed to meet the balanced budget target by 2029–30 (FY30), as required under the Balanced Budget Act. Measures to close a $2.5 billion gap had yet to be identified when the budget was tabled back in March. We expect the upcoming fall update to provide greater clarity on the government’s strategy to achieve this objective.

That said, a provincial election is just 367 days away, and it will inevitably bring promises that lower revenue and increase spending. Let’s hope that the parties’ campaign platforms will focus on budgetary discipline, as the fiscal framework leaves little room for uncosted commitments.