- Hélène Bégin, Principal Economist • Maëlle Boulais-Préseault, Economist

Economic News

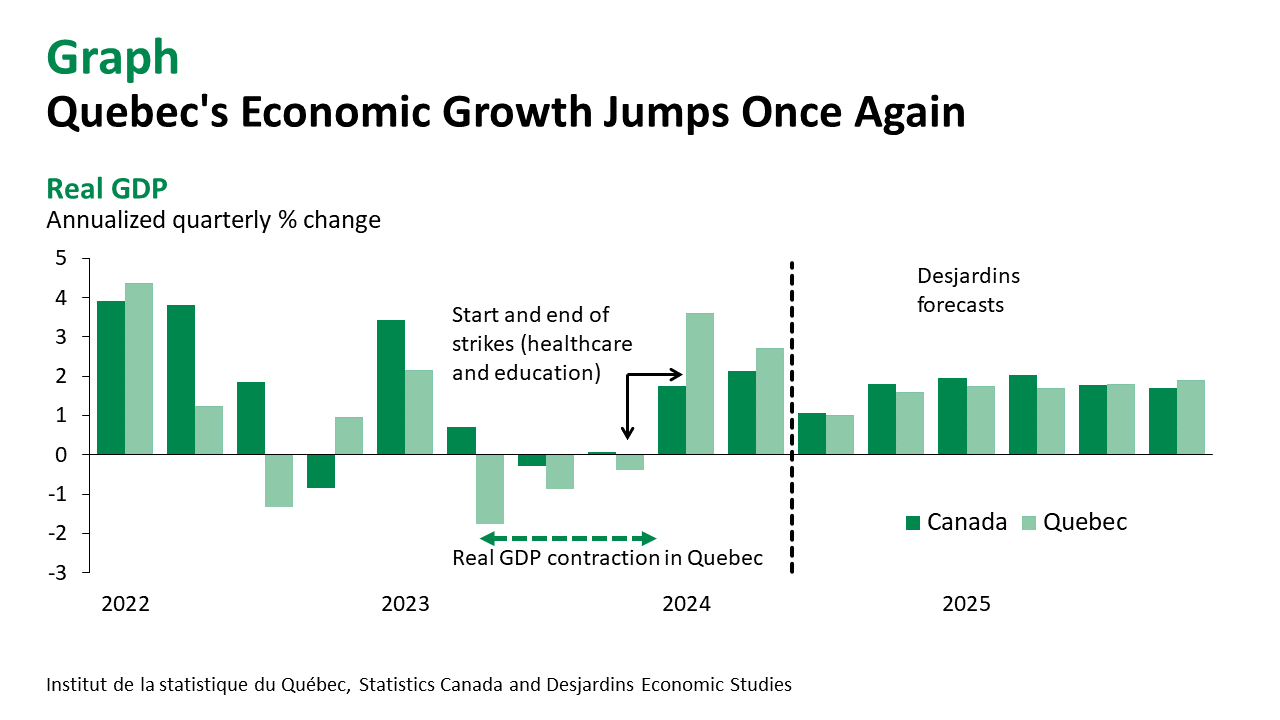

Quebec Real GDP Beats Expectations

September 25, 2024

Highlights

- Quebec's economy is still growing at a rapid pace after recovering this spring.

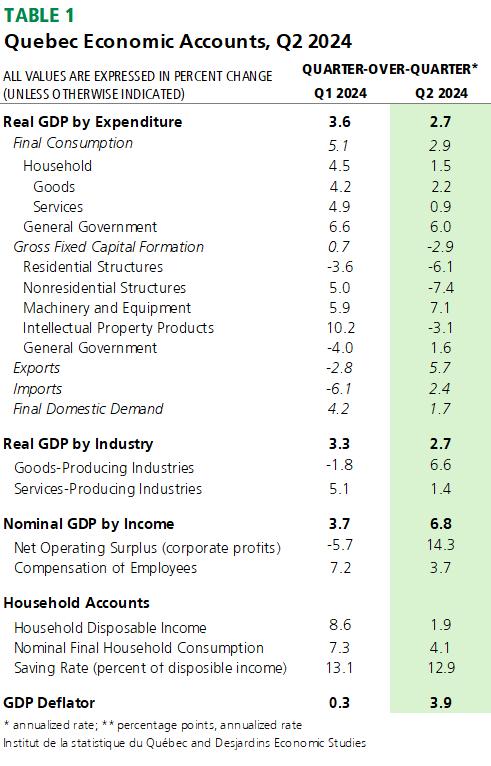

- Real GDP advanced at an annualized 2.7% in the first quarter of 2024 after a 3.6% gain in the first quarter.

- This continues to be better growth than in Canada as a whole over the same period (2.1% at an annualized rate).

- Household spending posted a second straight gain, while the savings rate dipped slightly from 13.1% to 12.9% between the first and second quarters of 2024. Durable goods consumption accounted for much of the increase in household spending.

- The housing market appeared to be losing steam, while renovations spending remained on a downtrend. The rally in the resale market nevertheless kept boosting commissions for real estate brokers.

- Total exports jumped by about 5.7% in the second quarter, outstripping the 2.4% rise in imports. The trade balance improved, helping fuel real GDP growth.

- Business investment shrank by 2.7% in the second quarter of 2024. Most of this decline was due to investment in non-residential structures, which has fallen for the past four quarters.

- See table 1 for more details.

Comments

As expected, Quebec's economy has stayed on track after a robust recovery early this year. At an annualized 2.7%, second-quarter real GDP growth even came in slightly higher than expected.

Household spending has proved astonishingly strong after an extraordinary first quarter. Given the substantial run-up in real disposable income, the savings rate stayed high at 12.9% in the second quarter, compared to 7.2% for Canada as a whole. Consumer confidence is gradually improving now that inflation seems to be under control and interest rates are starting to come down, which bodes well for the next few quarters.

Residential investment faltered, primarily due to muted renovation spending. New construction also appears to have lost some momentum in the second quarter. Meanwhile, the resale market has been on an uptrend since early 2024.

The pullback in business investment is due to lower investment in buildings and structures. The good news is that modernization efforts have continued to ramp back up since early 2024. Annualized growth in machinery and equipment investment climbed from 5.9% in the first quarter to 7.1% in the second quarter. SMEs are regaining their confidence, inflation is cooling and borrowing conditions have eased, encouraging many businesses to move forward with their projects.

Implications

The strength of Quebec's economy is in line with our forecasts, which predict continued growth over the coming quarters. Consumers are driving these gains, and some businesses are gradually showing signs of recovery. Although global geopolitical uncertainties persist, Quebec's economy is supported by solid fundamentals that should allow it to stay on course. We nevertheless expect GDP growth to moderate over the next few quarters.