- Sonny Scarfone

Principal Economist

Economic News

Quebec: Rising Unemployment and Growing Job Market Precarity

July 11, 2025

Highlights

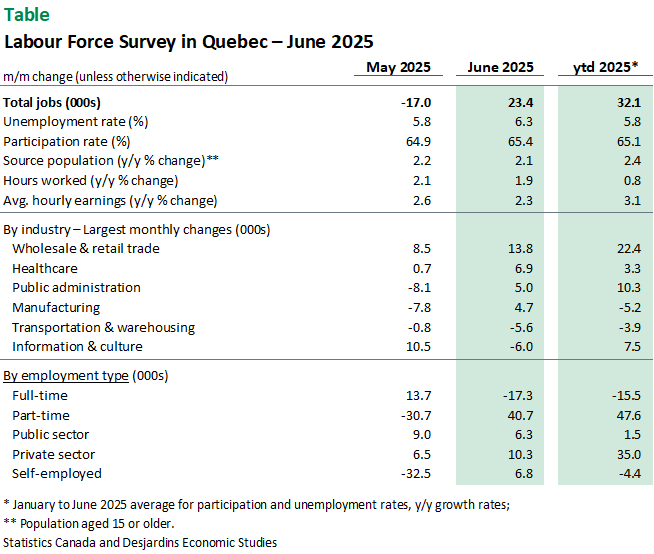

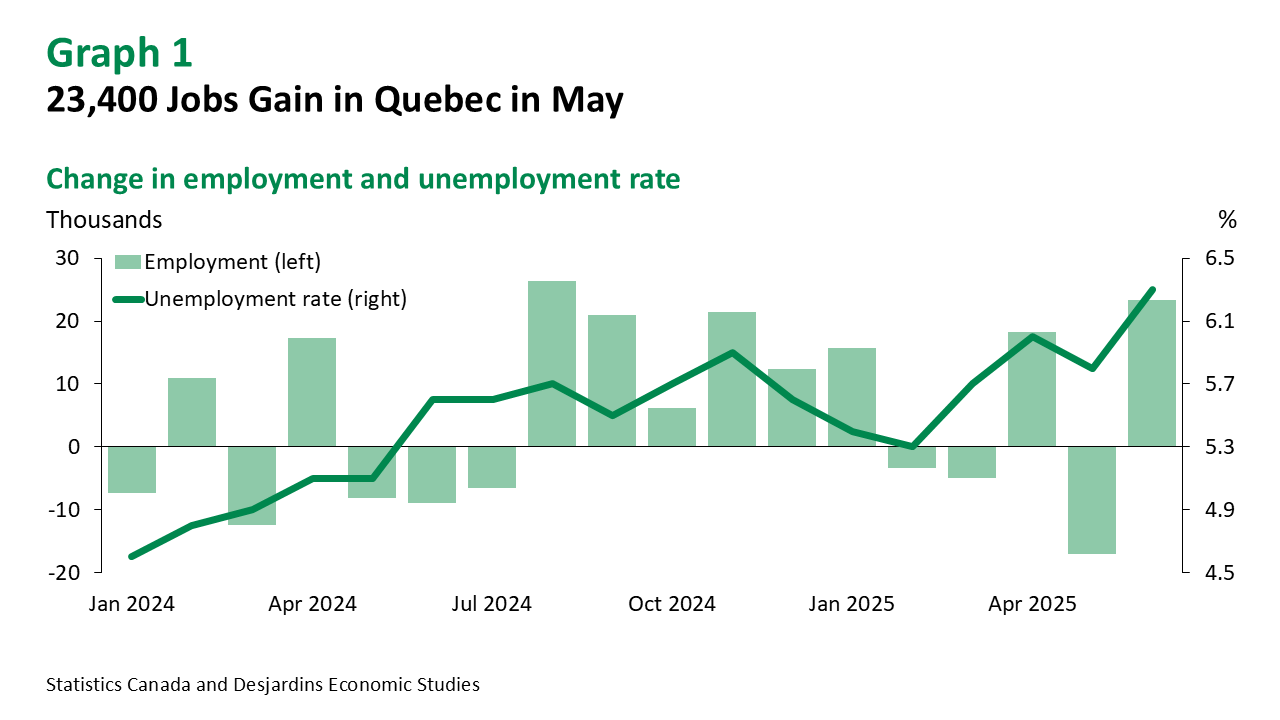

- Quebec’s job market added 23,400 positions in June, bringing total net job creation for the first half of the year to 32,100.

- However, the unemployment rate rose sharply from 5.8% to 6.3%, reaching its highest level since the pandemic. This increase is largely driven by a significant rise in the participation rate, which climbed to 65.4%—its highest since 2023.

- The composition of job gains remains less favourable. Full-time jobs have fallen by 15,500 since the start of the year, while all the growth (+47,600) has come from part-time jobs. On a more positive note, the private sector has performed better since January, with 35,000 jobs created.

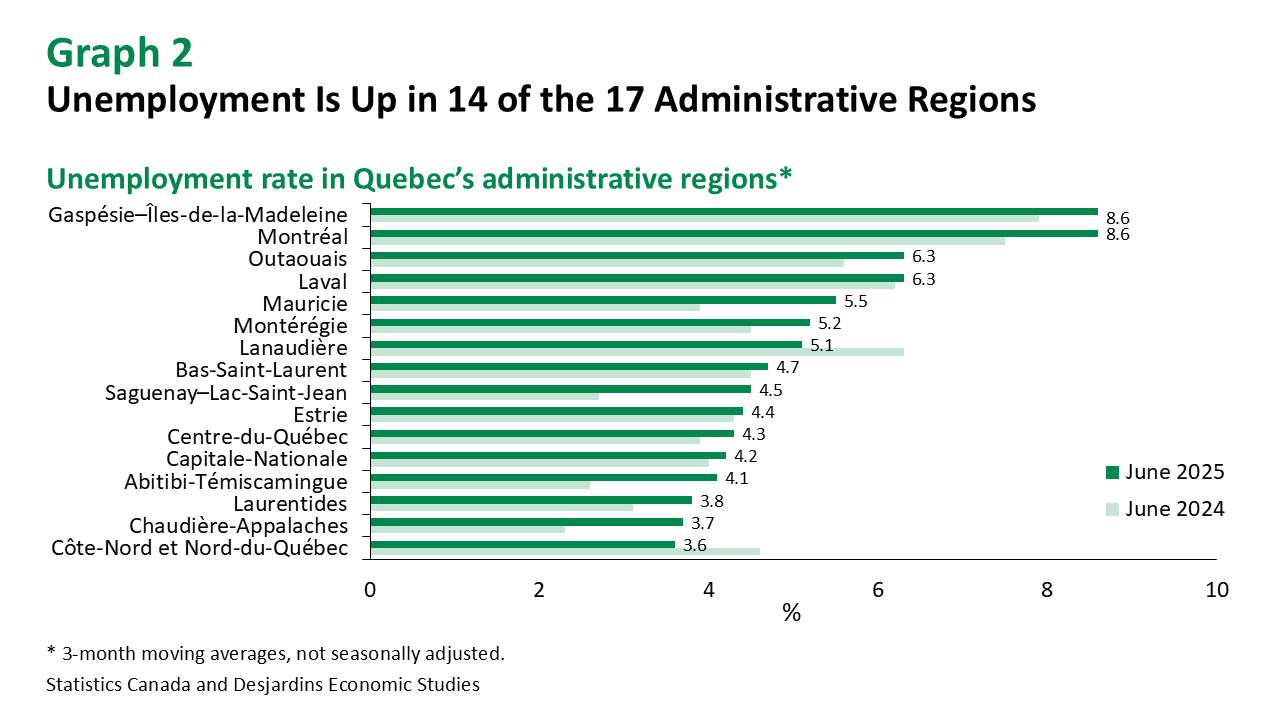

- At the regional level, most administrative regions posted a higher unemployment rate than at the same time last year. The increase was particularly pronounced in manufacturing- and resource-intensive regions such as Saguenay–Lac‑Saint‑Jean (+1.8 percentage points), Mauricie (+1.6), and Abitibi‑Témiscamingue (+1.5). In Montréal, the unemployment rate reached 8.6%—its highest level since the pandemic—and more than double that of the Capitale‑Nationale, which stood at 4.2%.

Comments

Employment growth is not the main takeaway from this month’s report. As the US administration renews its tariff threats ahead of August 1, signs of labour market fragility are becoming increasingly apparent.

Following a strong performance in 2024, the first half of 2025 paints a more mixed picture. Most of the jobs created were part-time, and the unemployment rate rose to 6.3%. When including discouraged workers and part-time workers seeking full-time employment, the broader unemployment rate climbs to 7.6%—the highest since the pandemic. Youth unemployment also rose to 11.5%, highlighting ongoing challenges in labour market entry for younger workers.

By industry, employment gains were largely concentrated in select service-producing sectors, notably wholesale and retail trade as well as finance and insurance. In contrast, all goods-producing industries posted declines, with construction experiencing the steepest drop (-17,800). The manufacturing sector, which remains more vulnerable to ongoing trade frictions, has seen relatively modest job losses totalling 5,200 since January.

With labour market conditions easing, wage growth has moderated. Average hourly earnings rose 2.3% year-over-year, outpacing Quebec’s inflation rate of 1.7%, but indicating a softening in wage pressures compared to previous periods.

Implications

The resurgence of trade tensions is drawing attention this week and suggests that economic uncertainty may extend beyond the first half of the year. In Quebec, although overall results for the first six months of 2025 were better than feared, the labour market is showing signs of strain. In this context, a significant economic slowdown in the province remains our base-case scenario, as outlined in our latest forecasts External link..