- Sonny Scarfone

Principal Economist

Weekly Commentary

Graduating into Uncertainty: A Cruel Summer for Canadian Youth

August 1, 2025

Today’s economy is fragile amid the ongoing trade war, the outcome of which remains uncertain at the time of writing. Real gross domestic product (GDP) edged down in April and again in May. Based on the Bank of Canada’s latest projections, released this Wednesday, the economy is set to stagnate External link. on a net basis in the second and third quarters of the year. This scenario is in line with our most recent forecasts External link..

There are growing signs that the labour market is slowing, notwithstanding a surprising report External link. published in June. Employment is mostly concentrated in part-time positions and in sectors less sensitive to economic cycles, which suggests that businesses are taking a wait-and-see stance. While we have yet to see waves of layoffs, employers—many of whom grappled with labour shortages in recent years—seem to be exercising caution before trimming their workforces. This means the issue is sluggish new hires, and it’s hitting one segment of the population particularly hard: young people at the beginning of their careers. Many are finding that the road to employment is riddled with obstacles in what has become an increasingly challenging labour market.

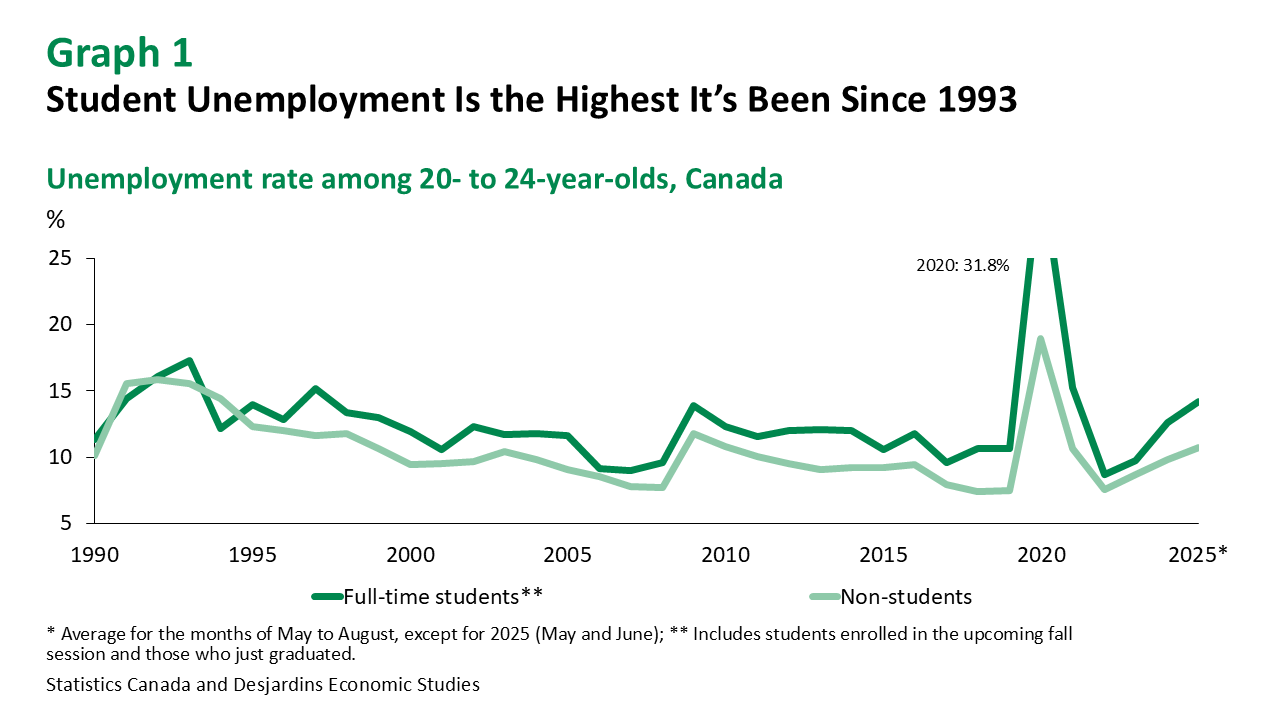

The unemployment rate for young people ages 15 to 24 pushed past 14% this summer. This is higher than it was in 2022 and 2023, but similar to the levels seen in the years before the pandemic. A closer analysis of the data shows that the decline has been especially sharp among 20- to 24-year-olds, whose unemployment rate has remained above 11% since last summer. Outside the pandemic, we haven’t seen this level over a sustained period since the 2009 recession. Looking closer still, we find that students in this age group are facing even greater challenges. Among those enrolled in a study program last spring, the unemployment rate has climbed to 14%—a level not seen outside the pandemic since 1993, when Canada was still recovering from a prolonged recession (graph 1).

The Scarring Effect

All this is particularly concerning given the well-documented long-term impacts of entering the labour market during periods of limited opportunity. An empirical study External link. conducted in Canada on the scarring effect found that young people who started their careers during a recession had annual wages that were about 9% lower in the first year after graduation. This wage gap halves after 5 years and is eliminated by the 10-year mark. But that decade playing catch-up makes it harder for these workers to accumulate savings and assets, and the chasm widens when you consider the decades of compound interest they might have earned on these unrealized savings.

Several economists have suggested that Generation X’s struggle to accumulate assets is partly due to the fact that they faced a less favourable economic environment. This hypothesis was recently cited (along with meager stock market returns in the 2000s) in an article External link. in The Economist. This underscores the fact that the effects of labour market entry conditions can be long-lasting, even if they aren’t necessarily permanent.

Indicators Point to Structural Changes

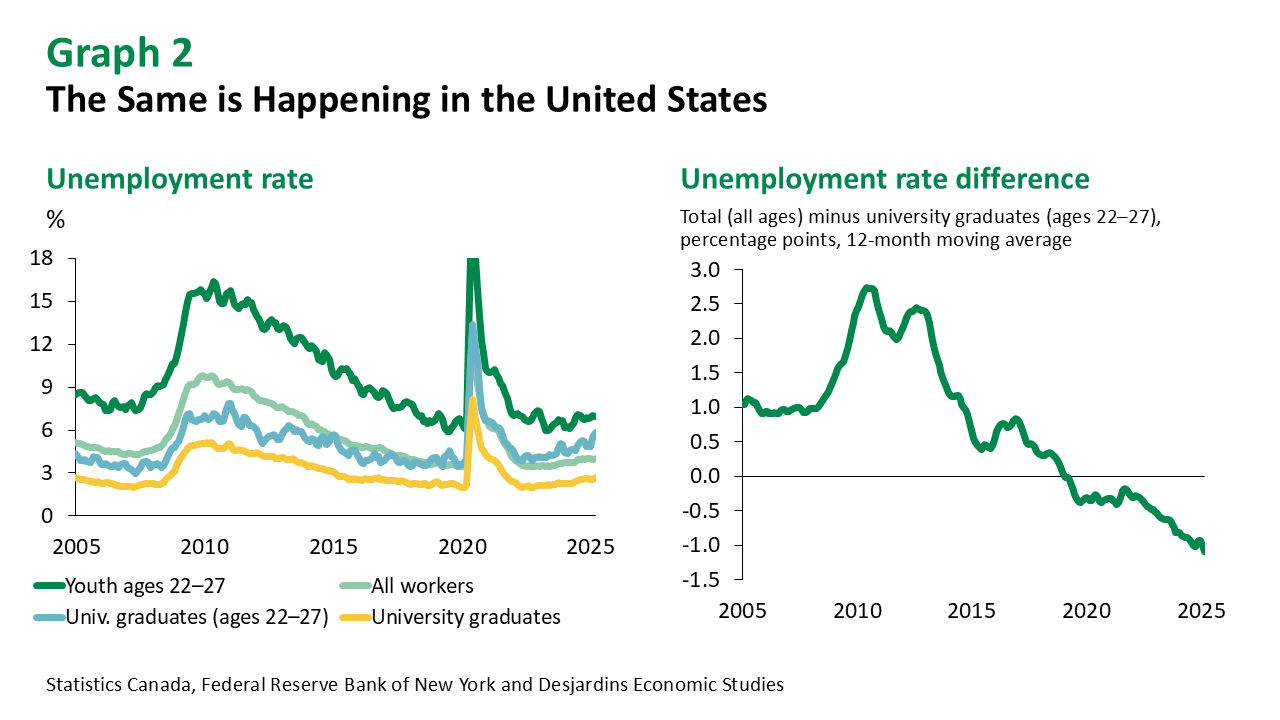

Today’s challenges may go beyond Canada’s economic cycle. In the United States, the unemployment rate for university graduates ages 22 to 27—a group that is still early in their careers but has some experience—is now higher than that of the overall workforce. While similar reversals have been observed in recent years, this is the sharpest recorded since the beginning of the data series. As shown in graph 2, the gap has widened significantly over the last few years, challenging some traditional labour market dynamics.

Many people are wondering if the increase in unemployment is partially due to recent technological developments, such as the rise of artificial intelligence (AI). Given the pace of change, it’s possible that some entry-level roles in certain fields will either disappear or be redefined. However, it’s too early to conclude that AI is the main driver. The rise in unemployment among recent graduates is largely due to a slowdown in hiring, as job vacancies return to more typical levels amid ongoing post-pandemic economic uncertainty—including inflation, tighter monetary policy and trade tensions. Young adults trying to enter the workforce are being disproportionately affected. While the impact of AI remains uncertain, its rapid advancement raises important questions about future job prospects in specific professions.

AI: A Risk Worth Watching

Young people today are encountering considerable challenges, and some traditional pathways to employment may need to be rethought. A feature article External link. published this week in The Wall Street Journal offered a hopeful perspective: collectively, we’re learning to combine human skills and AI more effectively. Since some repetitive tasks could be automated, recent graduates will need to be prepared to jump into more advanced roles that involve refining, interpreting and enhancing machine output. This shift will redefine what’s expected of new hires, who will have to be more productive from day one.

This new reality will also bring about a new set of risks, including increased precariousness, job insecurity and more frequent retraining as workers are required to adapt. Governments will play a critical role in supporting the transition—whether through hiring incentives, reskilling programs or other targeted measures. Navigating this transition period will be tricky but important in order to limit the long-term fallout for younger cohorts. Otherwise, they could face stalled career progression, reduced savings potential and lower overall life satisfaction.

Fundamentally, education is about shaping engaged citizens. But given the high costs—and levels of student debt—often associated with post-secondary studies, we may need to revisit our expectations for certain fields based on career prospects.