- Jimmy Jean, Vice-President, Chief Economist and Strategist

Tiago Figueiredo, Macro Strategist • Oskar Stone, Analyst

Investment Strategy and Interest Rate Analysis

More Rate Cuts Are on the Way

May 21, 2025

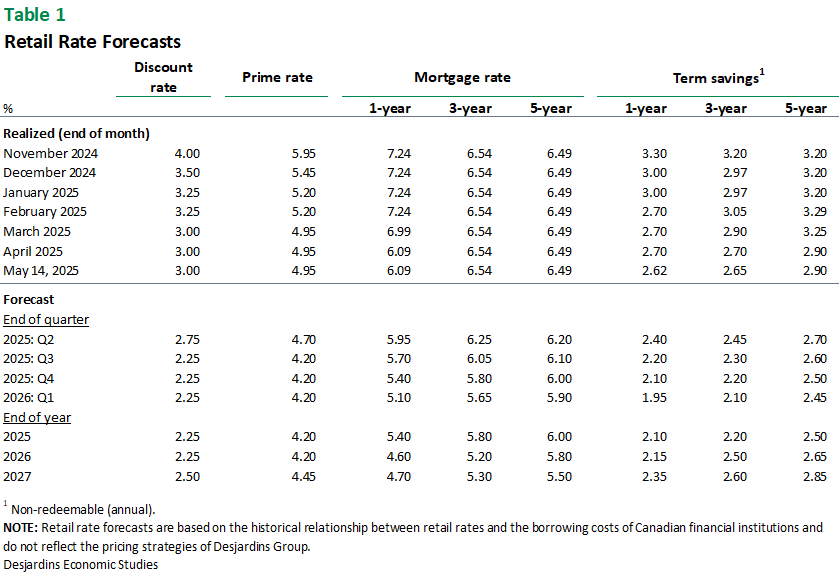

Economic Trends and Interest Rates

The Global Economy Has Entered Uncharted Territory, and the Waters Are Dark

The tariffs announced on Liberation Day increased the official levy on foreign products imported to the US to the highest level in over 100 years, sending global financial markets into a tailspin. While President Trump has since walked back most of those tariffs, the back and forth on trade policy is reducing confidence in the US administration. In many ways, the toothpaste is out of the tube; the US administration is pot committed to this protectionist strategy. The path forward involves leveraging tariffs to bring countries to the negotiation table and sign new trade deals. Signing a comprehensive trade deal is a lengthy process which, under optimal conditions, typically takes years to complete. So far, the US has only unveiled narrow, loosely defined and temporary agreements, notably with the UK and China.

If These Limited Agreements Constitute the Blueprint for Future Ones, the Effective Tariff Rate on US Imports Is Likely to Remain Significantly Higher than Before January 20

The starting point for the average US tariff rate was between 2% and 3%. Even with a compromise that leaves the effective US tariff rate at 10%—well below the initial estimates of around 25%—it would still be more than triple the pre-inauguration import duty. The read-through for the economy still carries undesirable undertones with a clear growth drag, but also an inflation tailwind, as we expect US inflation to reach 3.5% this year. Progress on trade reduces the left-tail risk of growth falling off a cliff, replacing it with a tamer but less-than-ideal “slide-into-the-ditch” outcome. Drastic swings in policy don’t inspire confidence and lingering uncertainty is weighing on global growth.

Expect Economic Activity to Slow

The weakness in economic data thus far has come from survey-based measures, which suggest that consumers are feeling less confident and businesses are sidelining hiring and investment as they wait for clarity. This will likely transition into more concrete signs of slowdown in the hard economic data over the coming months. While the softening of trade tensions with China is a welcome development, the damage from the initial barrage of tariffs has yet to be felt and any further progress on trade won’t eliminate the near-term downside risks facing the global economy. Even if a trade deal is struck, it’s possible that tariffs will remain in place. In fact, the drumbeat of the tariff parade might not be over, as many of the administration’s promised sectoral tariffs have yet to be announced.

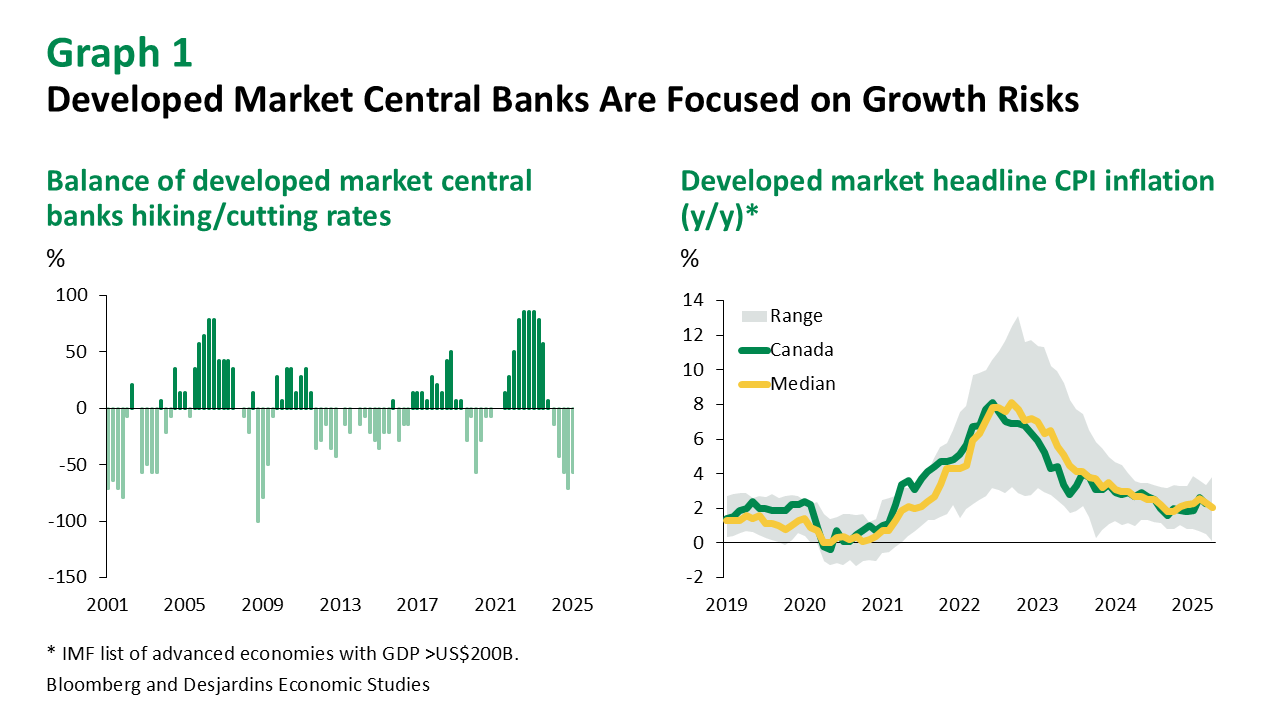

Central Bankers Remain Concerned About Downside Risks to Growth

Over half of developed-market central banks continued to lower their policy rates in the first quarter of 2025. While below the peak seen last year, that proportion is still elevated and will probably increase as incoming headwinds from trade materialize (graph 1, left). Inflation across most jurisdictions has normalized (graph 1, right), but the balance of risks is still fairly symmetrical in most jurisdictions.

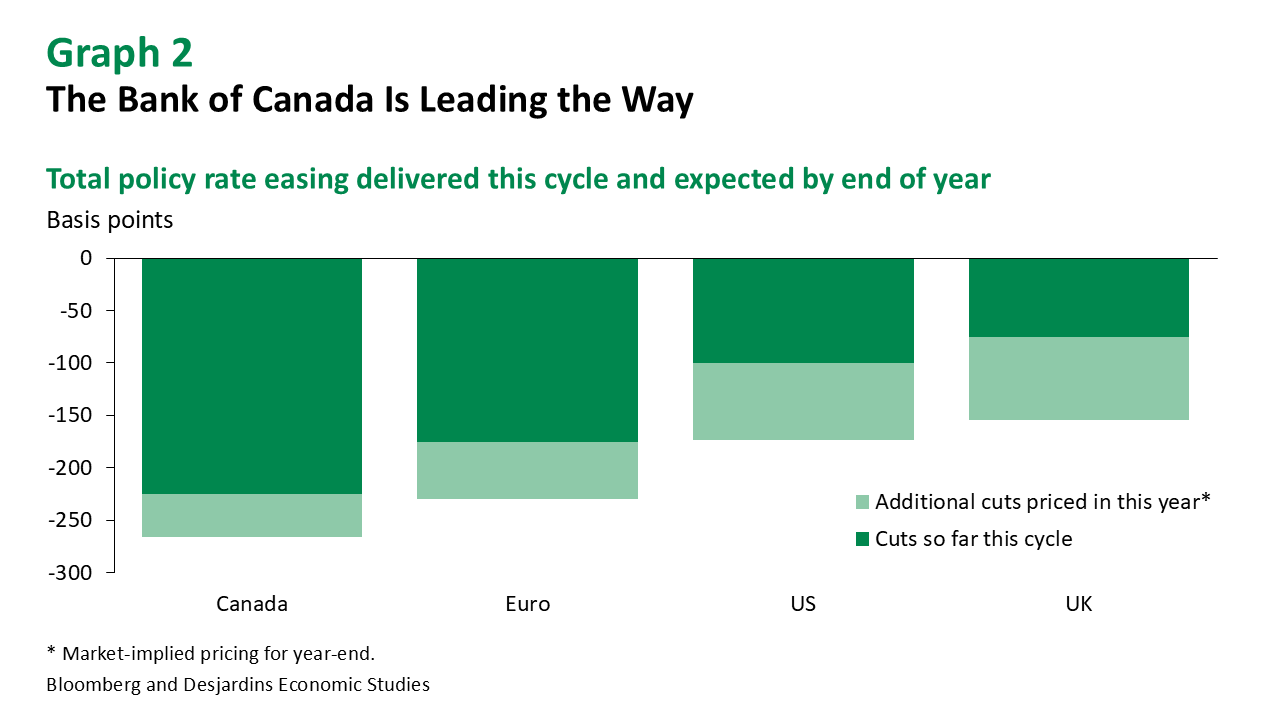

The Bank of Canada Has Eased Policy More than Any Other Developed-Market Central Bank

Having already cut rates by 225 basis points, Canadian policymakers had the flexibility to pause their easing cycle in April to assess incoming trade policies (graph 2). While that resulted in trimmed rate cut expectations, we believe that several idiosyncratic factors outside of trade uncertainty will keep Canadian central bankers lowering policy rates.

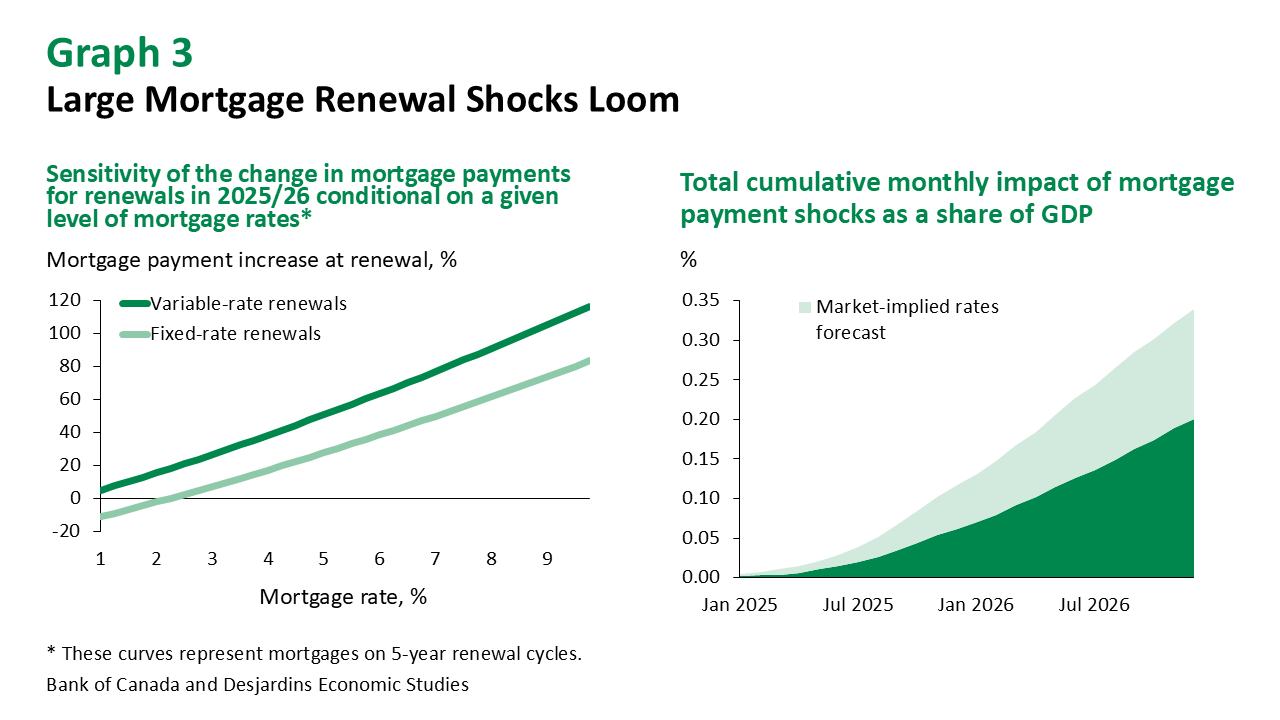

First, Headwinds from the Mortgage Renewal Cycle Are to Set Accelerate Even as Mortgage Rates Move Lower

Most mortgages renewing this year and next were taken out during the pandemic when interest rates were at cycle lows. As a result, mortgage payment shocks are set to increase notably. The mortgage rate decline that we expect won’t be enough to prevent mortgage payments from rising at renewal, particularly those on 5‑year terms (graph 3, left). Our latest estimates suggest that the cumulative drag on GDP from increasing mortgage payments is likely to be around 0.3 percentage points by the end of 2026. That’s assuming our more dovish rate path relative to what markets are pricing in. A rate path more in line with current market pricing could shave off an additional tick to GDP growth (graph 3, right).

Second, Canada is facing headwinds from a slowdown in population growth. Most of the decline has occurred in the number of residents aged 15–34, of whom many are believed to be non-permanent residents, particularly students. The government has whittled down its immigration targets, so we expect population growth to slow further.

Finally, there are early signs that depressed consumer sentiment and rising precautionary savings are starting to weigh on spending per capita, a concerning development given that the Bank of Canada is expecting per capita spending to rise over its forecast horizon.

We Continue to Expect the Bank of Canada to Lower Its Policy Rate Throughout the Year, but Our Forecasted End Point Is Now Higher

The softening tone on trade between the US and Canada has reduced the odds of the worst-case-scenario outcome for Canada. Fiscal policy will also help shoulder the load, with personal income tax cuts taking effect on July 1, and additional measures, such as the GST exemption for first-time homebuyers, providing further near-term support. Still, central bankers will need to manage a slew of headwinds. As a result, we now see the Bank of Canada lowering its policy rate to 2.00% this year.

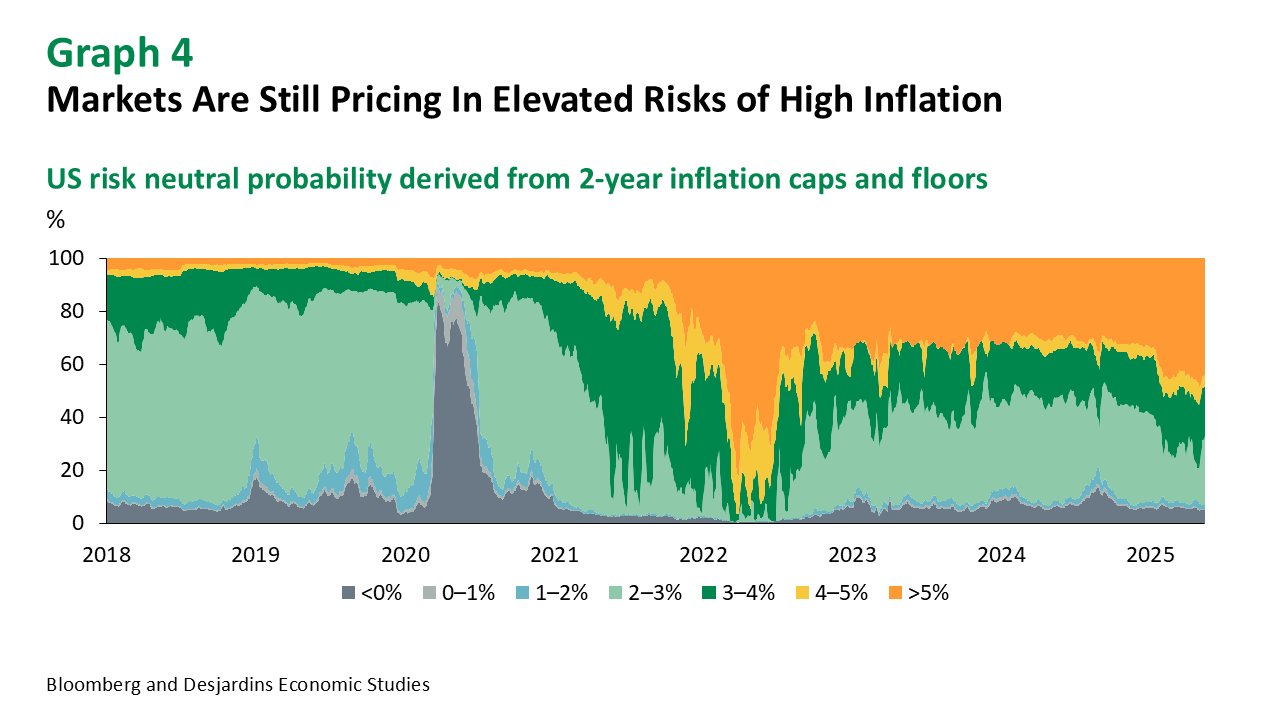

Expectations for Sticky Inflation Is Making It Challenging for the Federal Reserve to Lower Interest Rates

While inflation readings have been favourable recently, a sharp increase in inflation expectations has the market pricing in greater odds of higher near-term inflation (graph 4). The worst outcome for markets is that economic activity slows while inflation accelerates, putting policymakers in a tough position. That’s not our base case, but it remains a risk. Our view is broadly in line with the market’s current pricing, which sees three rate cuts from the Fed by year end.

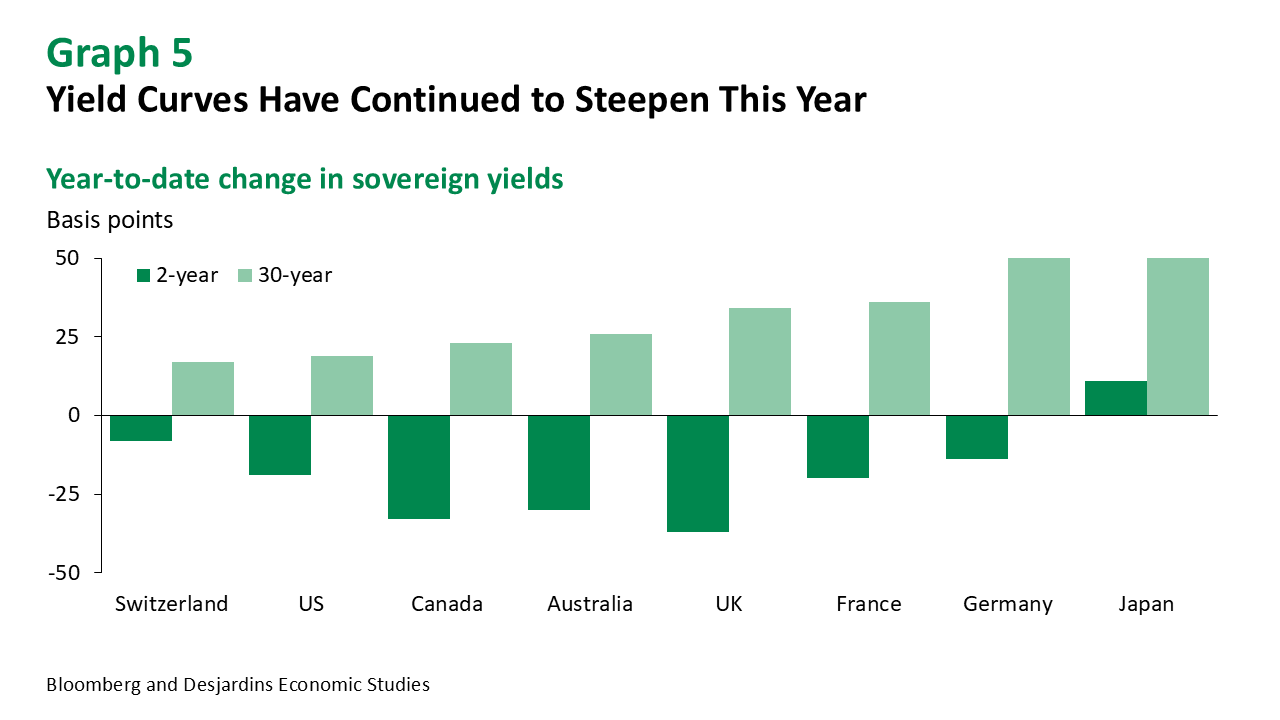

Against This Backdrop, Global Sovereign Rates Are Mixed and Curves Are Steeper

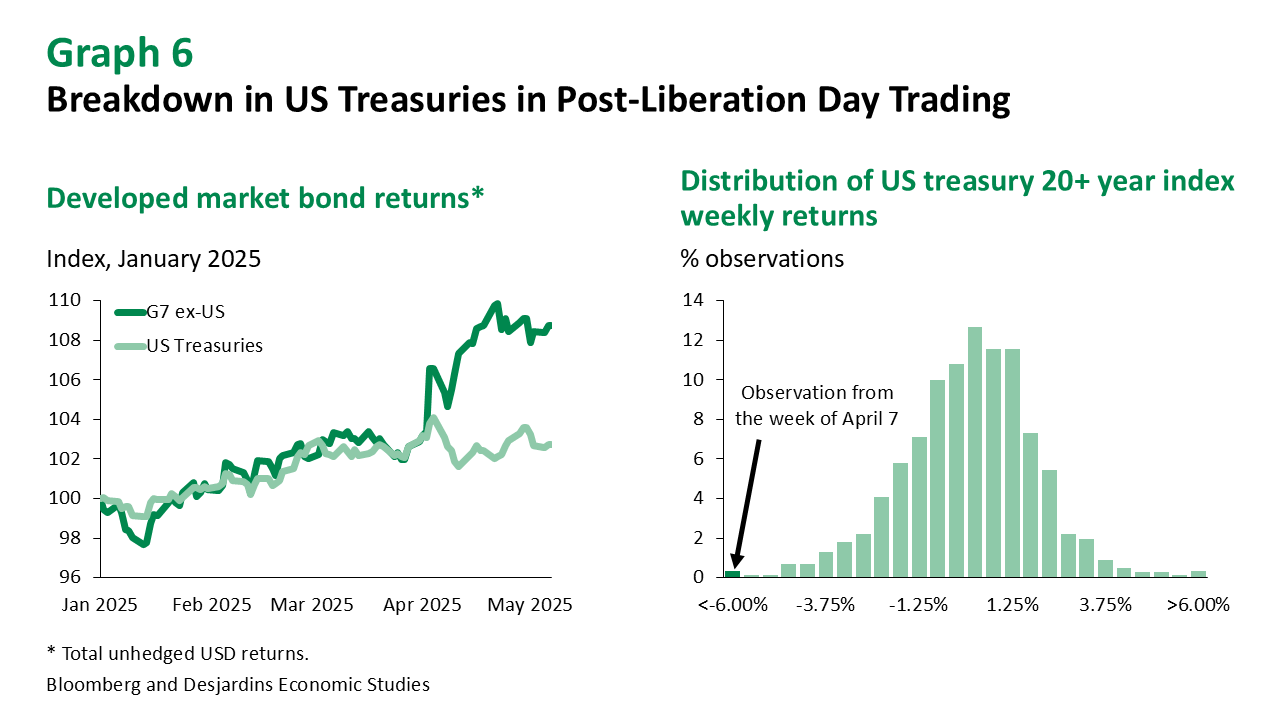

Most of that steepening has come from a combination of expectations for more policy easing and rising term premiums due to trade policy uncertainty (graph 5). Notably, the rise in term premium is much more pronounced in Europe than in North America. While some of the volatility in US fixed income was due to an unwinding of positions from speculators betting on regulatory changes, these dynamics are a catalyst rather than the culprit. The breakdown in correlation with US Treasuries and rest-of-world sovereign bonds came right after the reciprocal tariff announcement (graph 6, left) and led to one of the worst weeks on record for US long-end Treasuries (graph 6, right). Global investors are now considering whether it’s in their best interest to own long-term US assets in a world where policy shocks are originating in the US.

We’re More Agnostic on Term Premium but Still Expect Rates Across the Curve to Move Lower by Year End in North America

Markets continue to underappreciate the downside risks in Canada, and we believe they are underpricing the odds of a rate cut in June. Over the coming weeks, GDP and another Labour Force Survey release should show further weakness and push central bankers to cut policy rates. In the US, rates are likely to drift lower later in the year, although we continue to believe that economic activity will slow sufficiently for the Fed to be able to justify a rate cut as early as the July FOMC meeting.

Exchange Rates

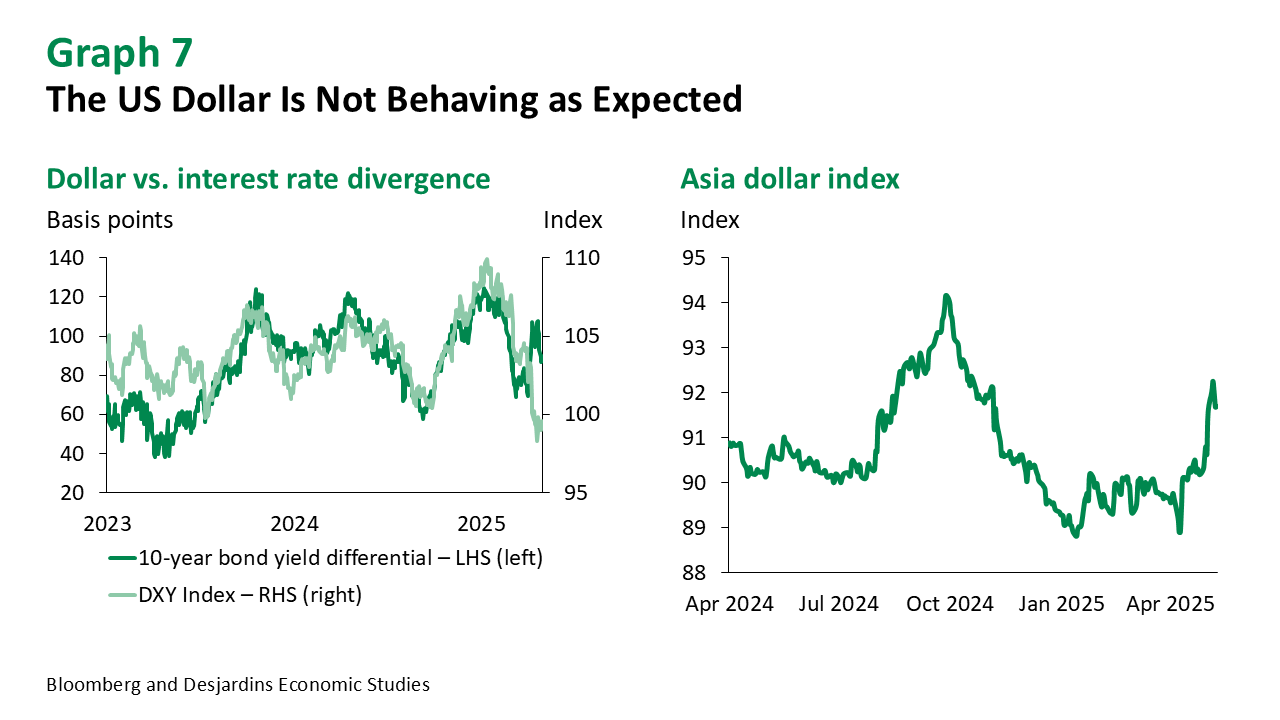

Market Participants Are Once Again Questioning the US Dollar’s Reserve Status

The rotation away from US assets accelerated in April, resulting in a breakdown in the typical correlation between the greenback and interest rate differentials (graph 7, left). In our view, the US dollar isn’t going to lose its reserve status overnight—though the US exceptionalism narrative that has supported high dollar valuations in recent years no longer holds.

Asian Currencies Have Seen Unusually High Volatility (Graph 7, Right)

The Taiwanese dollar has appreciated nearly 9% since Liberation Day, with most of that move occurring over just a few days. With the US administration cracking down on currency manipulation, some fear policymakers may be limited in their ability to curb unwanted currency appreciation.

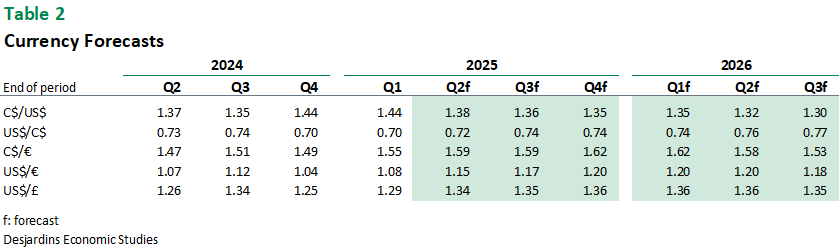

We Remain Optimistic on the Canadian Dollar

While the Bank of Canada is unlikely to offer much support to the currency, easing from the Fed should help bring interest rate differentials more in favour of loonie strength. The new government in Ottawa is expected to scale up fiscal support. If these new policies are successful in boosting labour productivity and improving the investment climate in Canada, the CAD should benefit. Negotiations and reforms surrounding the energy sector will be key to watch, with the new government pledging to move promptly on the file.

Equities and Credit

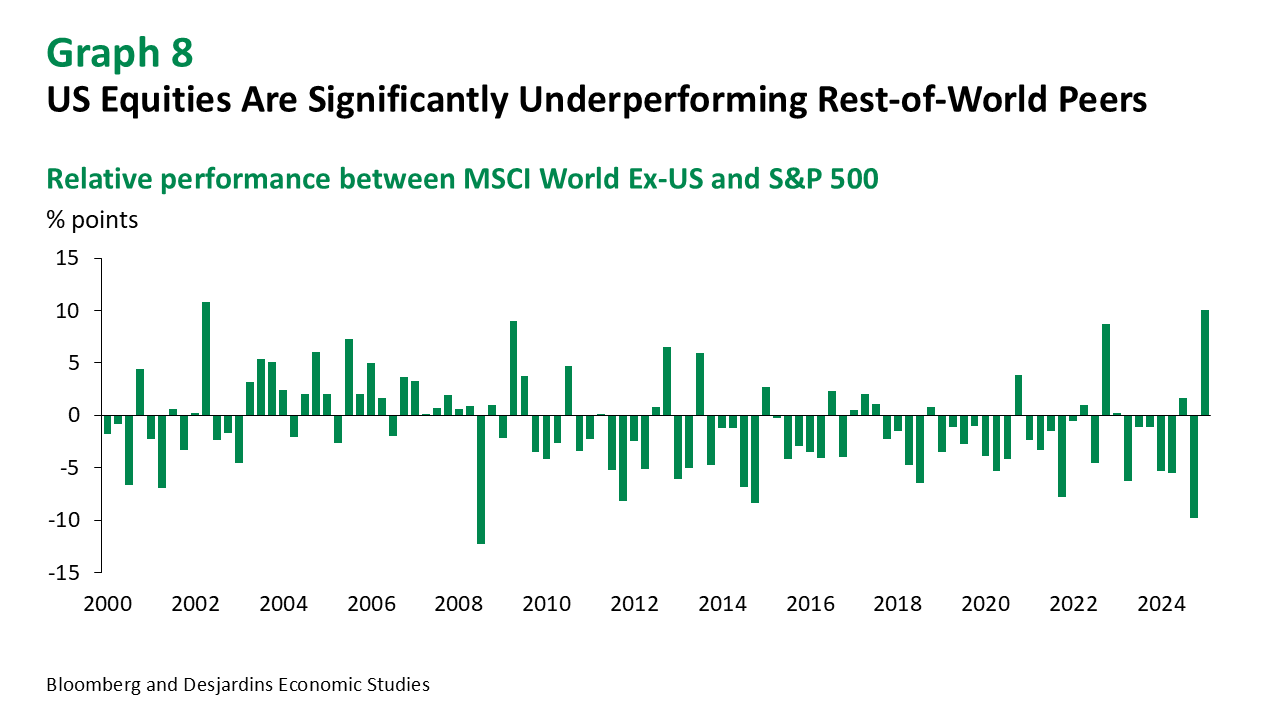

America’s “Golden Age” Has Seen US Exceptionalism Unravel

Adverse growth and inflation outcomes from protectionist trade policies are likely to overshadow any benefits that come from deregulation or tax cuts in the future. That outlook, coupled with a loss of confidence in US assets, meant that flows into US domiciled funds continued to slow in April and early May. This rotation, however, may have gone too far too fast (graph 8). Global investors who have diversified equity allocations and are now finding themselves overweight in rest-of-world equities will need to rebalance back into the US. Valuations are also relatively more attractive, which supports “buying America” again, at least in the near term. Looking beyond, the jury is still out on the extent to which there will be a structural shift away from US assets. Investors choosing to underweight the US must be buyers of the notion that Europe and China will deliver on fiscal policy. There’s also an implicit view that the US will continue to deteriorate over an extended period. With the rotation still in its infancy, we remain skeptical that this trend will continue through to year end.

Our Forecasts Still See Rest-of-World Equities Outperforming North America and Canadian Equities Outperforming the US by Year End

While we expect rest-of-world equity markets to outperform, this reflects smaller drawdowns in post-Liberation Day trading, rather than stronger price appreciation from now until year end.

Ongoing Trade Negotiations Have Reduced Downside Risks to Equities

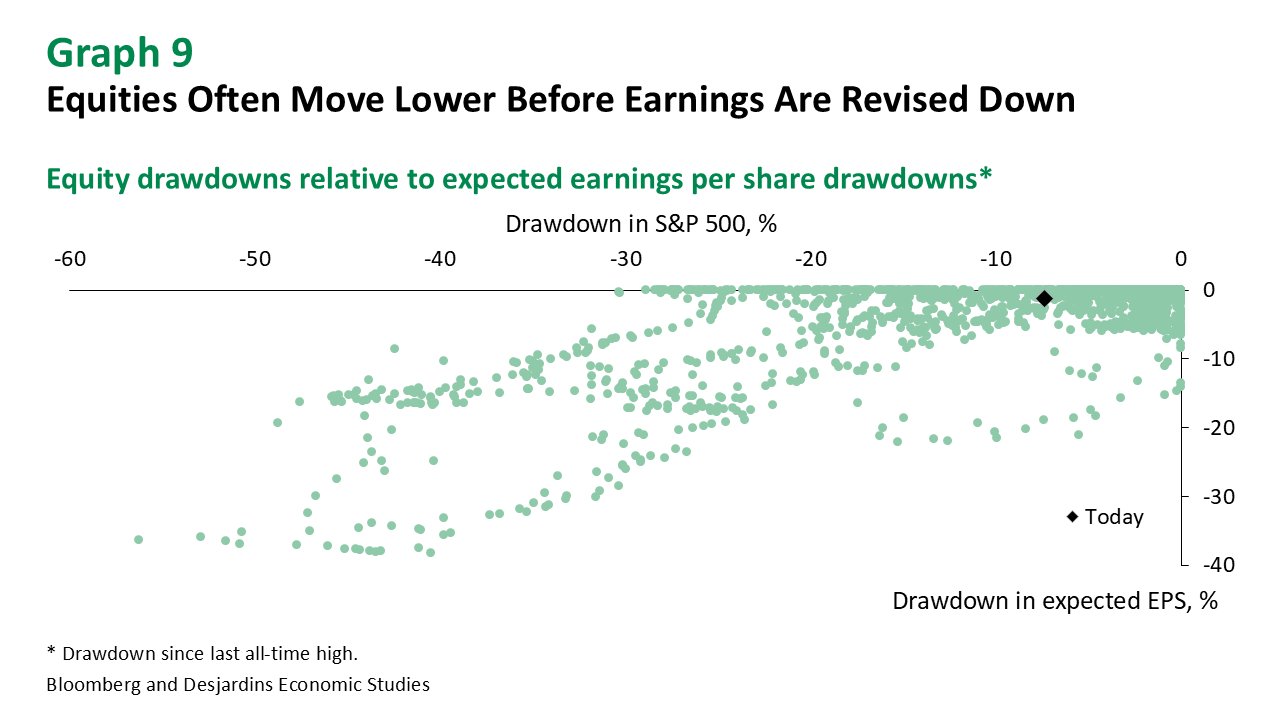

Our year-end equity price targets are slightly higher than our Economic and Financial Outlook update, partly reflecting a reduced drag from tariffs on earnings, but also lower odds of a US recession. We’re less optimistic relative to consensus on earnings and we do see scope for earning expectations to move lower. Note that consensus forecasts for earnings-per-share tend to lag moves in equity prices (graph 9).

Systematic Investors Could Become a Stabilizing Force in Late May and June

The distribution of daily equity returns is compressing relative to April. 1‑month realized volatility averaged over 40% in the preceding month, implying daily moves in excess of 2.5%. With market conditions normalizing, systematic investors should be allocating back into equities from very low exposure levels. This process will take time but could be a source of support for equity markets over the next month if volatility continues to normalize. Buybacks could be another leg of support as a large share of companies are set to exit their blackout windows.

Inflation Will Be a Key Watch Point for Cross-Asset Investors, as a Resurgence Would Be Painful for Portfolios

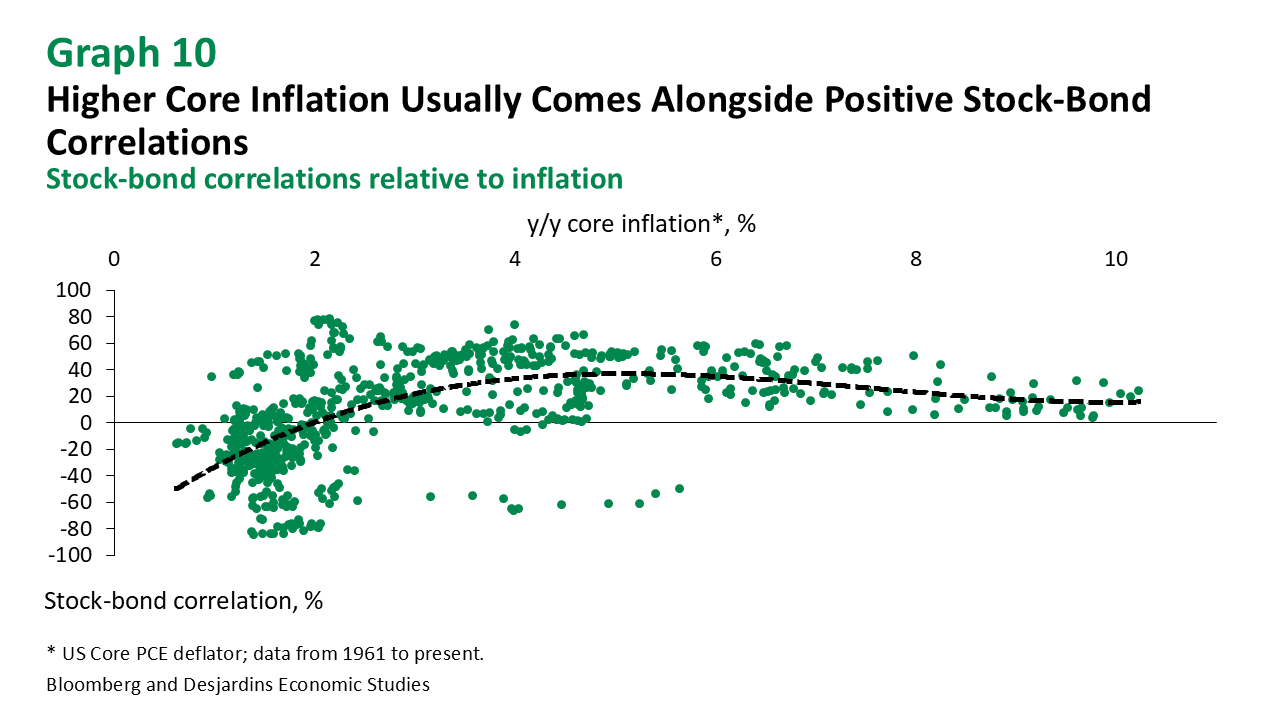

While downside risks to the economy will hurt equity markets, without an increase in inflation, correlations with bonds should remain negative. However, any scenario with higher inflation typically leads to positive stock-bond correlations (graph 10). If this relationship between inflation and asset correlations holds and tariffs cause more persistent inflationary shocks, the performance of traditional portfolios will be penalized considerably.

Meanwhile, Corporate Bond Markets Are Showing Resilience for Now

Despite recent volatility, corporate bond issuance remains solid, particularly in US investment grade, which has continued to track 2024 levels. Meanwhile, US high yield continues to lag relative to levels seen last year, reflecting reduced risk appetite amid high volatility.

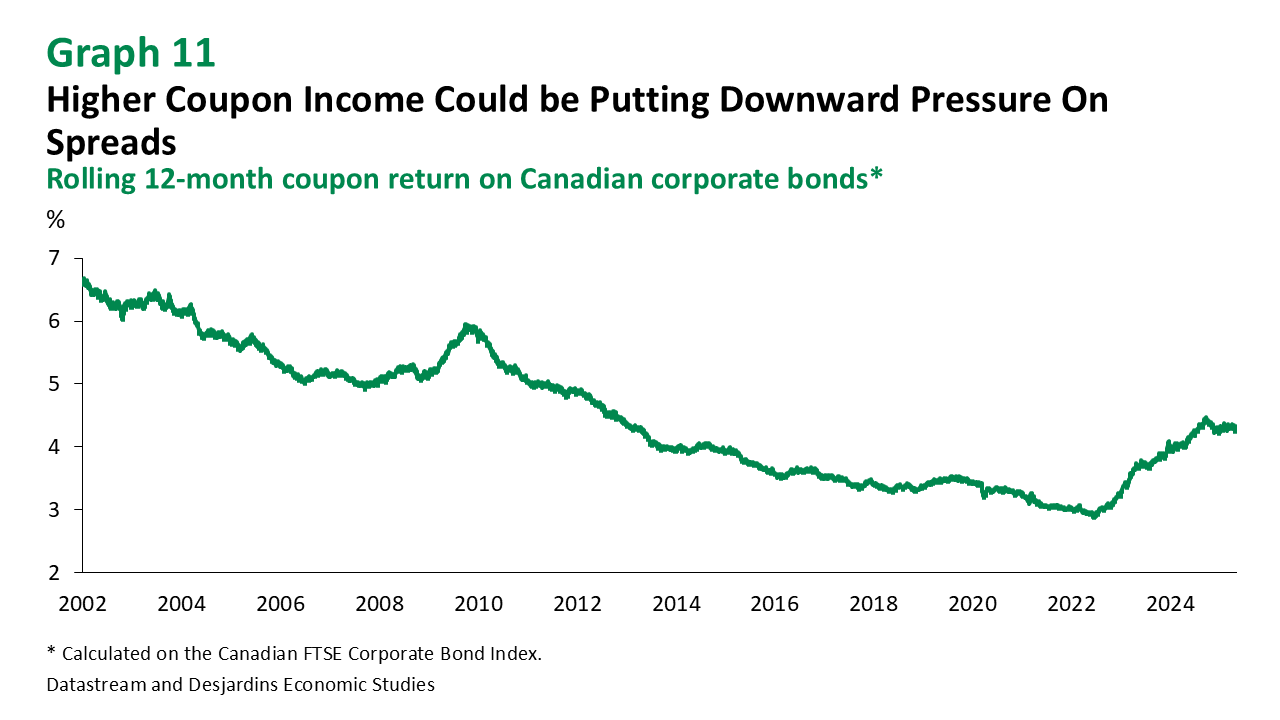

Spreads Widened Modestly in April but Remain Largely Within Historical Ranges

One contributing factor may be elevated coupon reinvestment. Looking across various bond indices, the 12‑month rolling return from coupon income has risen to the highest levels since 2013 (graph 11). The larger coupon flows being reinvested back into the market are likely contributing to downward pressure on spreads.