- Jimmy Jean, Vice-President, Chief Economist and Strategist

Tiago Figueiredo, Macro Strategist • Oskar Stone, Analyst

Investment Strategy and Interest Rate Analysis

Expect a Choppy End to the Summer

August 8, 2025

Economic Trends and Interest Rates

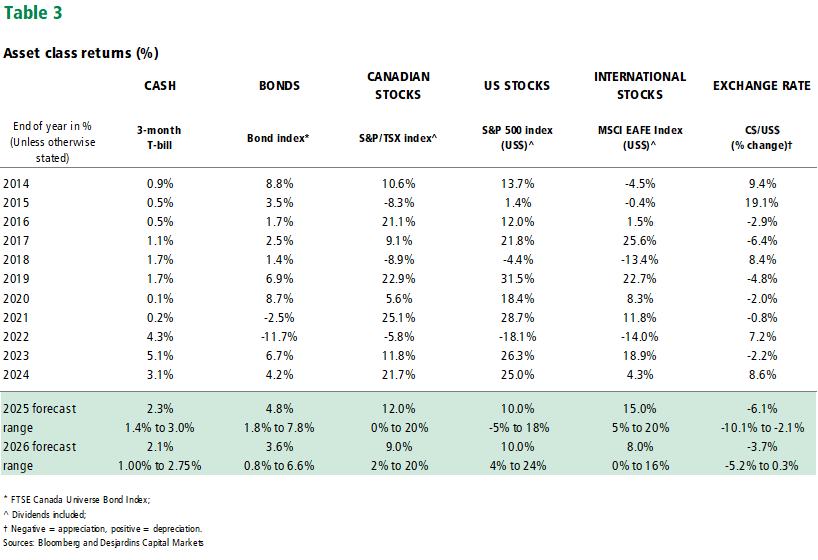

Incoming trade deals continue to moderate downside risks to growth and upside risks to inflation.

Trade agreements with Japan, Vietnam, South Korea and the European Union have reduced the risks of a material increase in tariff rates going forward. While the effective levy on US imports for most countries is around 15%, that’s well below the almost 30% seen post Liberation Day. Outside of North America, the US has secured deals with almost all its major trading partners, covering roughly half of its global imports (Graph 1). Recent inflation readings in the US have shown signs of tariff pass‑through, but those concerns have been largely offset by weakness in employment growth. Overall, the direction of travel for short‑end rates is skewed lower in developed markets excluding Japan.

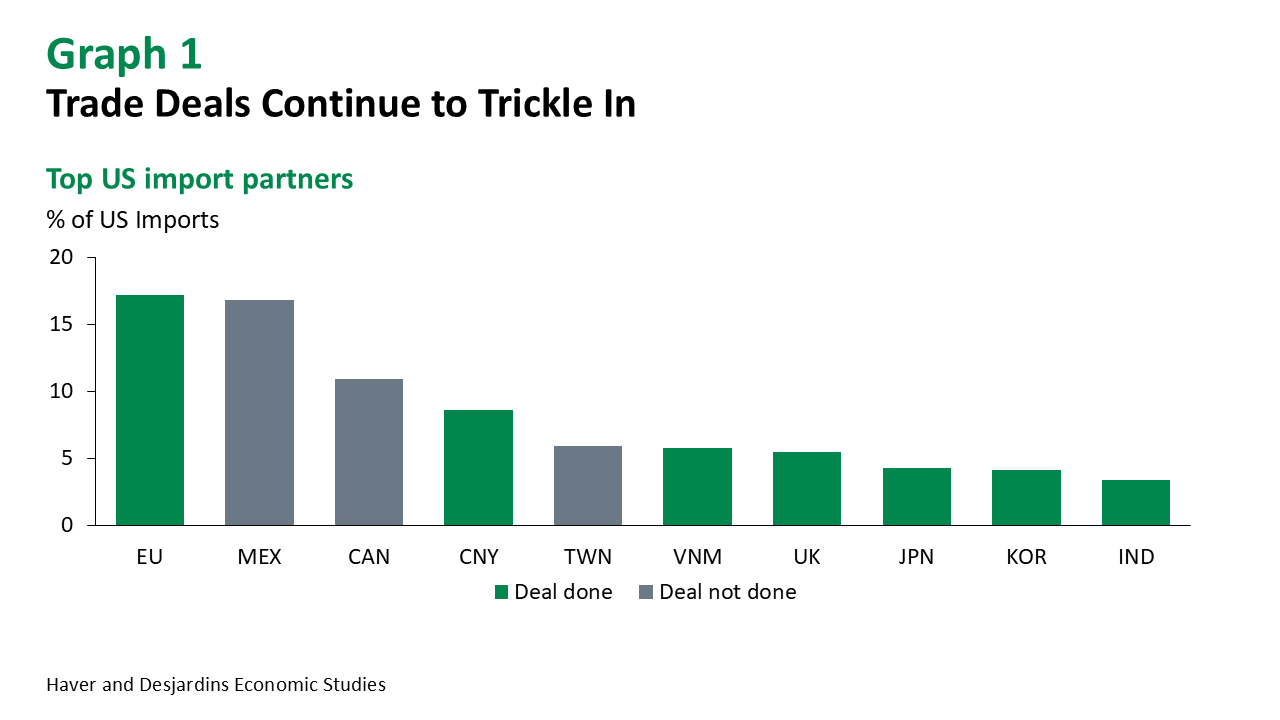

Longer-term interest rates continue to diverge from the short end.

The average 30‑year yield on major market sovereign bonds has been moving higher, while the average overnight rate across jurisdictions has fallen (Graph 2). A myriad of factors continue to put upward pressure on long‑term bond yields, not least of which are looming concerns around the fiscal outlooks for many countries. While we still believe that 10- and 30-year yields are likely to be lower one year from now, curves should continue to steepen as a higher term premium dampens the effect of falling short rates on the long end. Sharpe ratios (i.e. the expected returns relative to the expected volatility of these returns) on long‑term debt are likely to be lower than during previous cutting cycles due to these dynamics, making it riskier to hold duration.

Markets are pricing in too high of a probability that the Bank of Canada is done cutting interest rates.

Much of this is rooted in the belief that the central bank has clearly outpaced its developed market peers and monetary stimulus needs time to work. While true, the Bank of Canada policy rate is sitting at a neutral setting, and we believe that domestic economic challenges will still push central bankers to deliver more easing than what the market is currently pricing. We continue to expect that Canadian central bankers will move off the sidelines in September, delivering three rate cuts over the remainder of this year. That said, risks around that rate path are skewed towards a slower pace of easing.

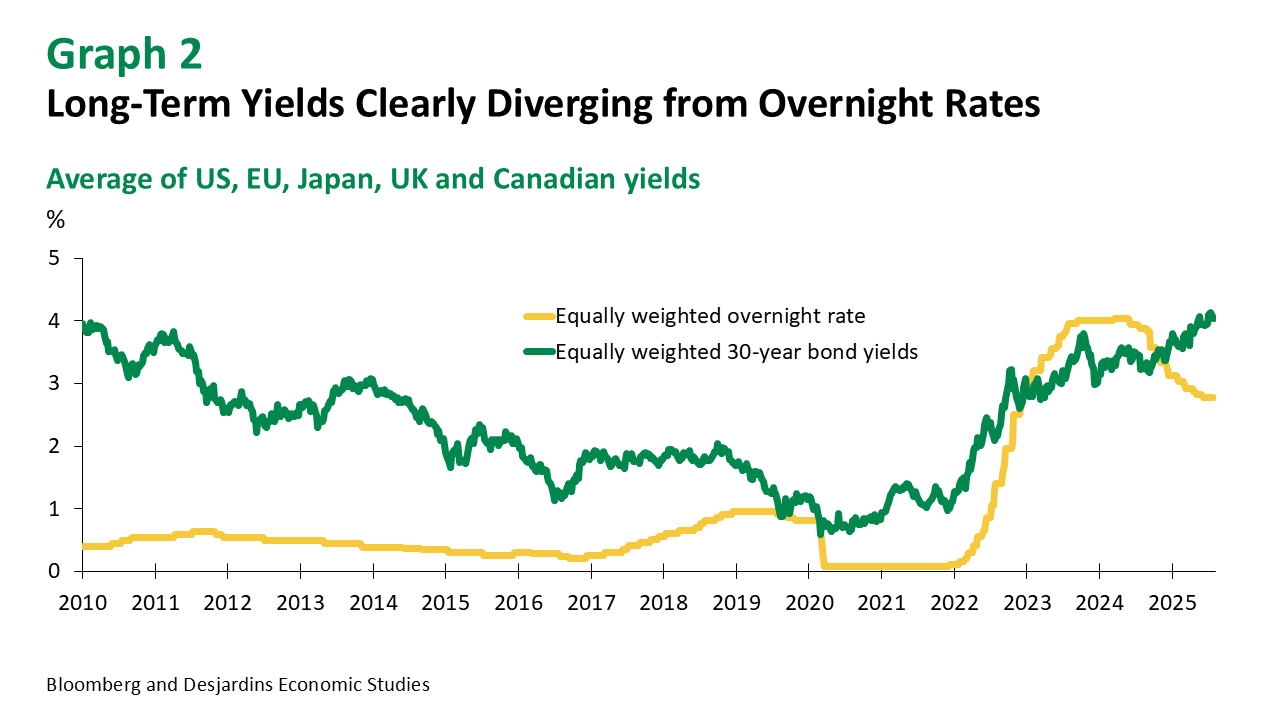

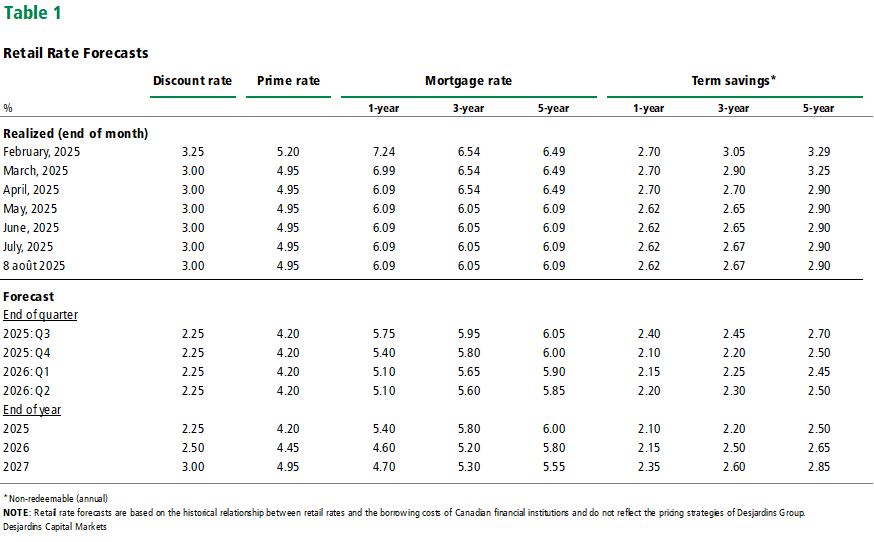

With the Bank of Canada on pause for now and yields broadly rangebound, our mortgage rate forecasts remain relatively unchanged.

There is still scope for mortgage rates to fall across the curve in the second half of the year, but we’re penciling in less of a decline in 5‑year posted mortgage rates relative to 1‑ and 3‑year tenors. Part of this reflects ongoing pressures on longer‑term yields which, have resulted in rising term premiums. This trend is evident in the 5‑year sector where a sizeable share of mortgages are issued (Graph 3).

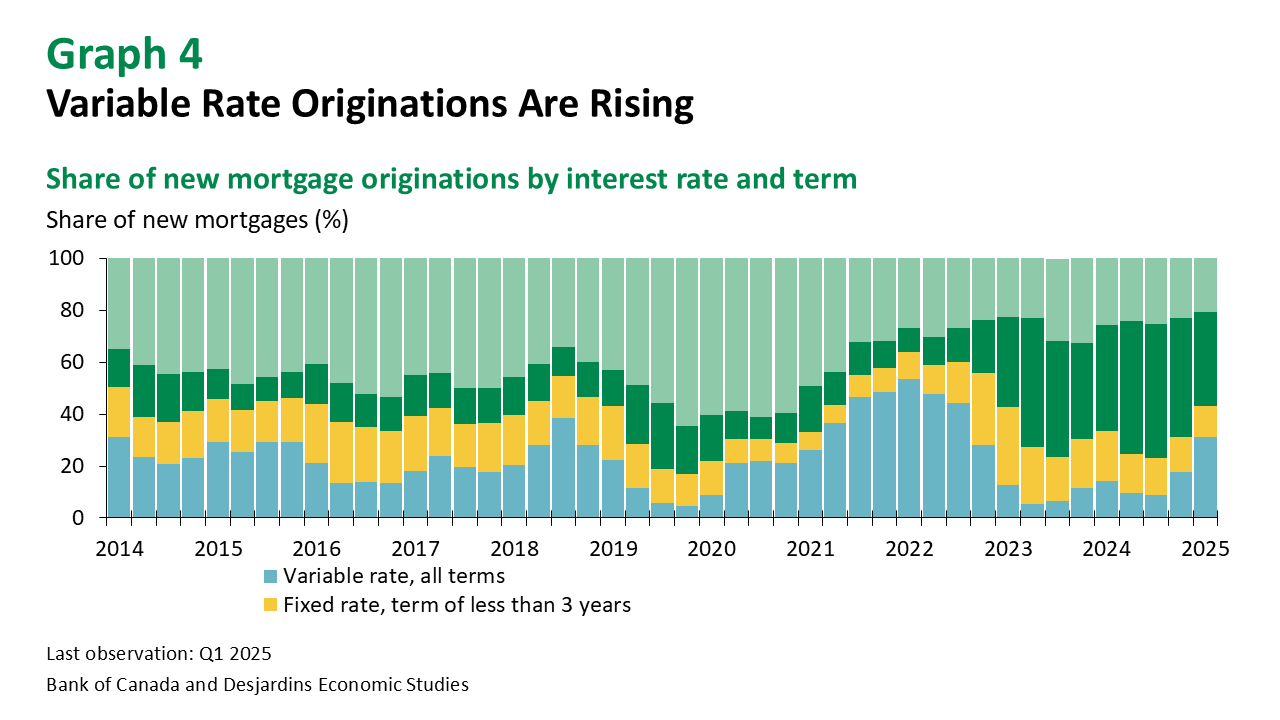

While 1‑year and 3‑year mortgage rates may see more relief, they tend to be higher than for the 5‑year sector, limiting their appeal. By contrast, variable mortgage rates have turned more competitive, and originations have increased in that sector as a result (Graph 4). Variable rates should continue to move lower, in tandem with the policy rate, likely eliciting some take-up in a context of still‑stretched affordability.

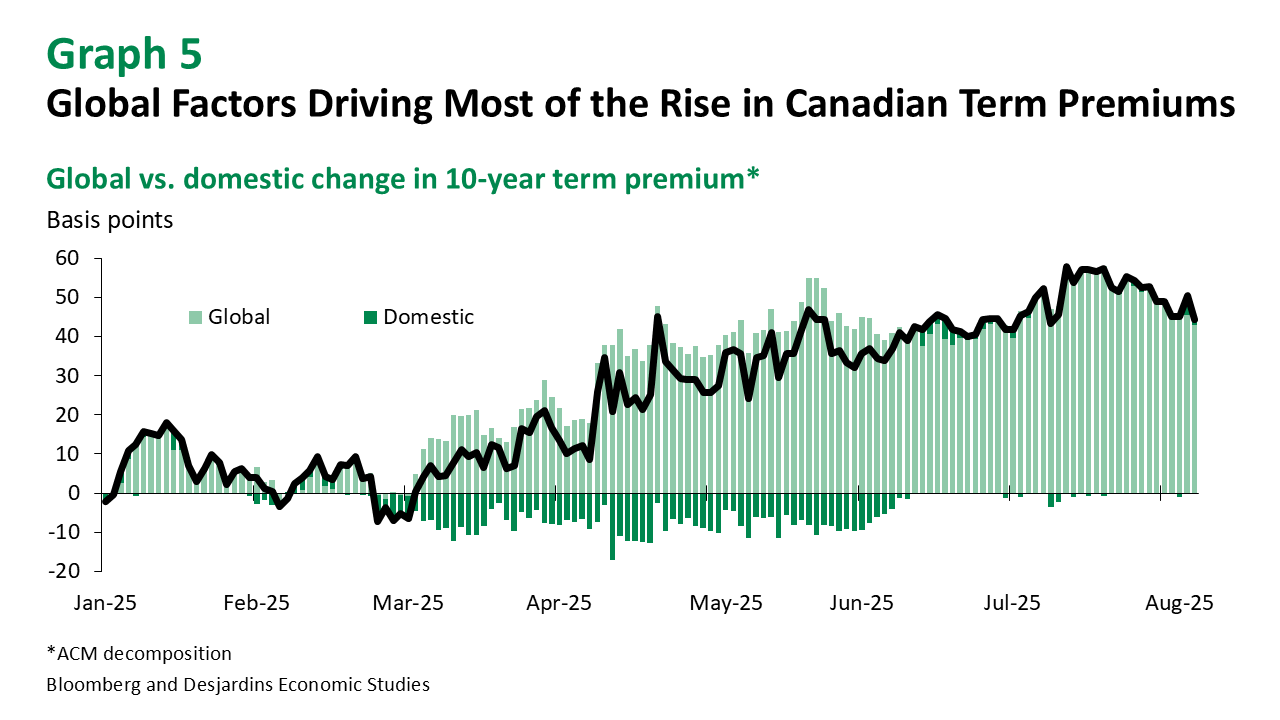

Canada could be less impacted by many of the factors that are pushing term premiums higher.

Most of the increase in Canadian term premiums reflects global trends (Graph 5). That’s unsurprising, given that Canada is a small open economy which tends to import term premiums, particularly from the US. That said, the spectre of increasing global bond supply should help GoC bonds at the margin. The latest debt management strategy from the Federal government didn’t raise any eyebrows, and if the new government delivers a sound budget in the fall, Canadian fixed income could benefit via increased capital inflows. The government is starting from an enviable position relative to other jurisdictions, with general government deficits as a share of GDP the lowest across the G7. Even with the increased spending being proposed, our research External link. suggests that Canada’s AAA sovereign rating is not in jeopardy in the near term. Outside of issuance, ongoing uncertainty around the stability and credibility of US institutions could continue to fuel a gradual rotation away from US assets.

Policymakers in the US should be ready to recommence their easing cycle in September.

Outside of the recent month, progress on inflation has been better than many had expected. Any tariff-related pass-through to inflation has been offset by normalizing services prices. Final domestic demand and employment growth are both slowing stateside, suggesting that the need for lower rates might be more urgent than originally thought. US central bankers will be closely watching incoming data for signs of further weakness in other sectors, notably on the consumer side.

US T-Bill issuance should rise notably between now and the end of summer.

The passing of the One Big Beautiful Bill Act has lifted the debt ceiling to US$5T and the Treasury is beginning to rebuild its cash balance. The Q3 refunding announcement didn’t offer any surprises, with projections suggesting a quarter‑end government cash balance target of US$850B, an increase of US$500B from current levels. T‑bill auctions have held up well and there have been no signs of stress within repo markets. That said, we’re just getting started with the incoming supply, even though money market mutual funds, the big players in US T‑bills, remain well positioned to absorb this issuance. Still, this issuance should reduce liquidity at the margin going into a period where trading volumes tend to wane due to summer vacations. With the US fiscal position continuing to deteriorate, it’s likely that the Treasury will need to increase bond supply over the coming years. That should continue to put upward pressure on US term premiums.

Cross-border flows for May remain in line with the view that any rotation away from US assets will be gradual.

Canadian international transaction data showed that US investors were net buyers of Canadian equities in May, although the trend continues to point to a broader selling of Canadian equities over a longer horizon. Meanwhile, US TIC data showed plenty of volatility in Canadian holdings of US Treasuries. Year‑to‑date, Canadian investors have been net sellers of US assets, but most of that has come from selling in agency bonds. The May release also showed that official accounts were net buyers of US assets, offering more evidence that concerns about de‑dollarization following Liberation Day, particularly among FX reserve managers, were overblown. While the data in hand does suggest limited selling of USD denominated assets, there is some evidence that participants were hedging their US dollar exposure.

Exchange Rates

Surging volumes in cross-currency swaps suggest that investors were hedging their US dollar risk in April.

The latest data from the Bank of Canada’s semi‑annual FX trading volume survey confirms our earlier thesis that investors were looking to adjust their long‑term exposure to the US dollar. That said, this hedging flow does appear to have slowed recently, perhaps because currency hedge ratios have now been raised. Overall, the risks around the US dollar appear more balanced.

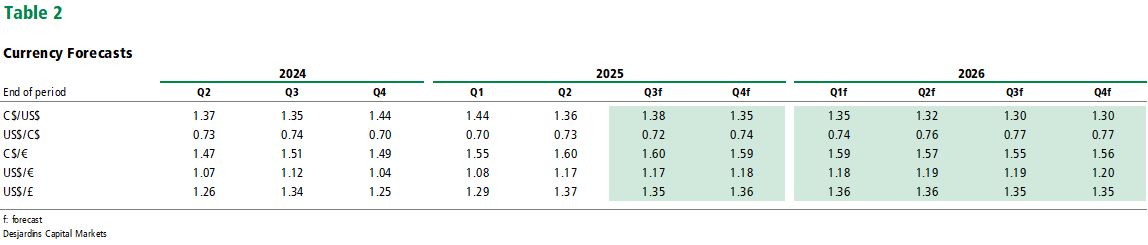

We expect the US dollar to strengthen over the summer but end the year weaker.

While tariff uncertainty is not quite finished, we expect some sort of a trade deal could be worked out soon. The focus should shift towards economic fundamentals and relative interest rate differentials. Economic weakness stateside could put more upward pressure on the US dollar in Q4.

Equities and Credit

Equity markets got a boost from the passage of the One Big Beautiful Bill Act, incoming trade deals and fading geopolitical risks, making new all-time highs.

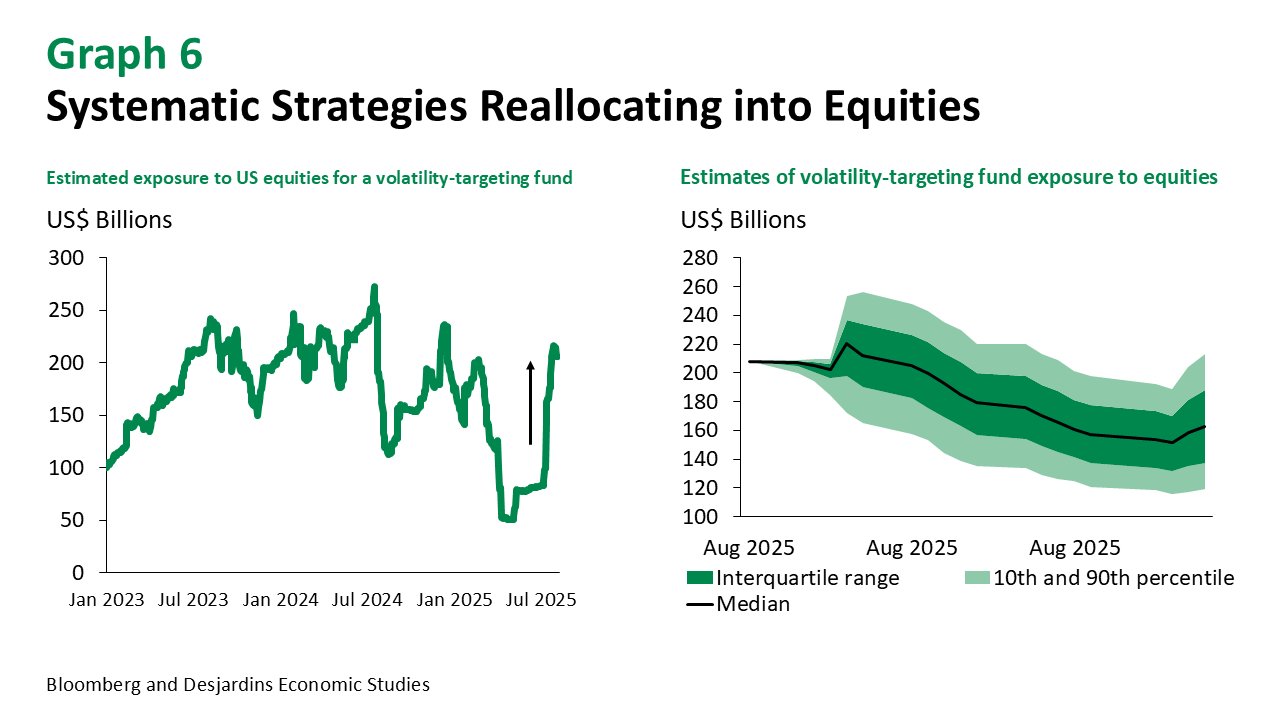

Risk assets looked through any adverse headlines relating to US central bank independence and have remained stable. The S&P 500 posted 23 consecutive days without a 1% move, the largest run since last September. That’s helped improve liquidity with market depth, as measured by order book depth on S&P 500 futures, suggesting some of the best conditions seen this year. That said, part of this stability has also been technical. Volatility‑targeting funds, most popular among variable annuity product portfolio managers, have been strong buyers of equities throughout July (Graph 6). Trend‑following Commodity Trading Advisors (CTAs) have also been reallocating back into equities, supporting the price action.

Buybacks have been, and will likely continue to be, a source of support for equities.

By the end of the first week of August, nearly all the S&P 500 will have exited their blackout windows, with many expected to have capacity to increase share repurchase activity.

That said, we are entering pool party season and it’s likely that these favourable conditions deteriorate.

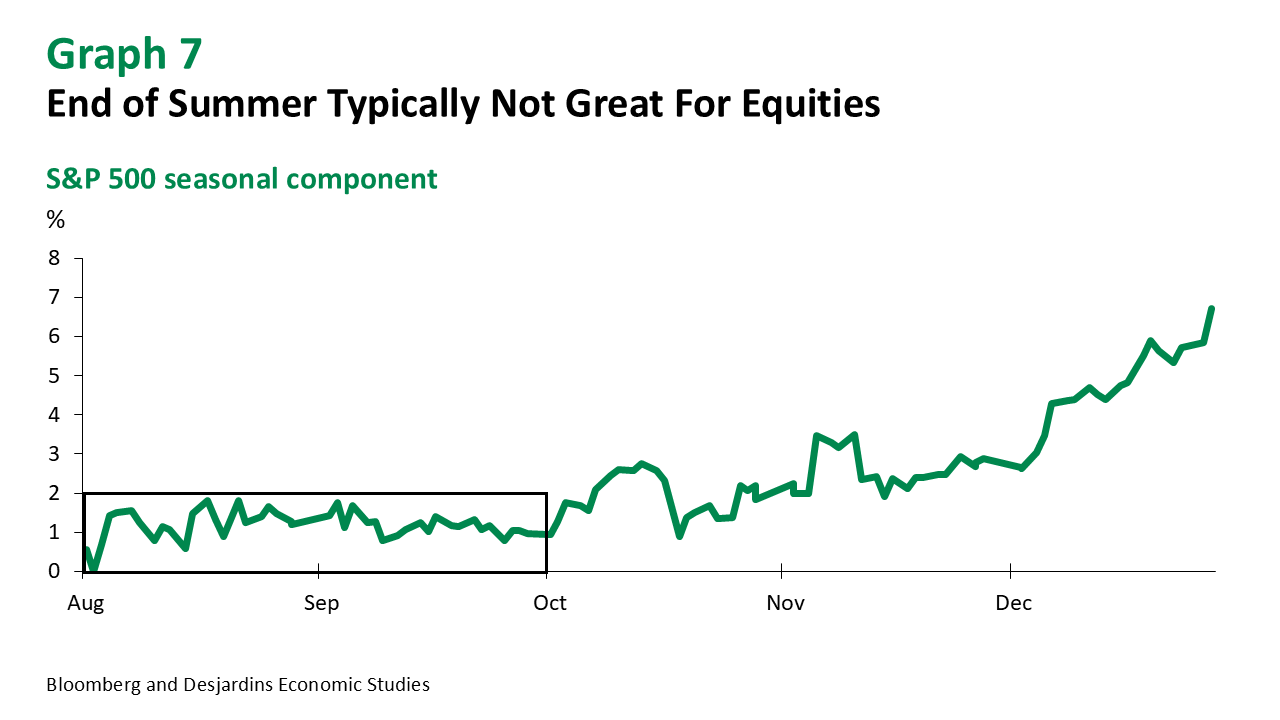

Seasonally, August through to September tend to be uninspiring months for equities (Graph 7). Mutual funds tend to see large redemptions throughout August as well. This soft patch is coming at a time when economic data is starting to show more signs of weakness following the tariff barrage earlier in the year.

Barring a material deterioration in the economic backdrop, corrections are likely to remain shallow.

During the Liberation Day selloff, money market mutual funds saw redemptions of over US$150B, which were seemingly used to buy the dip. That suggests some willingness by investors to deploy cash into risk assets during drawdowns. That said, household cash allocations as a share of total assets remain relatively stable around pre-pandemic levels and we don’t believe there is a material amount of excess cash waiting to be deployed into risk assets. This story is similar in Canada.

The resilience in equity markets has pushed us to revise our year-end equity forecasts slightly higher.

We still see scope for a pullback before the end of September but see equities moving higher into year‑end as North American central banks resume their easing cycles.

Corporate spreads have continued to compress but term premiums have kept all-in borrowing costs relatively unchanged.

With spreads narrow, it’s difficult to see further tightening but all‑in borrowing costs should gradually move lower over the coming year. Coupon reinvestment flows continue to put downward pressure on spreads.