- Jimmy Jean, Vice-President, Chief Economist and Strategist • Hendrix Vachon, Principal Economist

FX Analysis

After Rising Quickly, the US Dollar Could Lose Some of Its Strength in the Coming Months

November 21, 2024

Highlights

- The US dollar has skyrocketed since early October, posting gains against all major currencies from advanced and emerging countries. With several indicators continuing to underscore the US economy’s strength, there are increased doubts about whether the Federal Reserve (Fed) will be able to proceed with multiple interest rate cuts over the coming quarters. Already, widening yield spreads between US Treasuries and many other sovereign bonds have given the greenback an edge.

- Donald Trump’s election win has also fueled the US dollar’s advances. Many of his proposed policies could drive up inflation pressures, which would further hinder the Fed’s ability to trim interest rates.

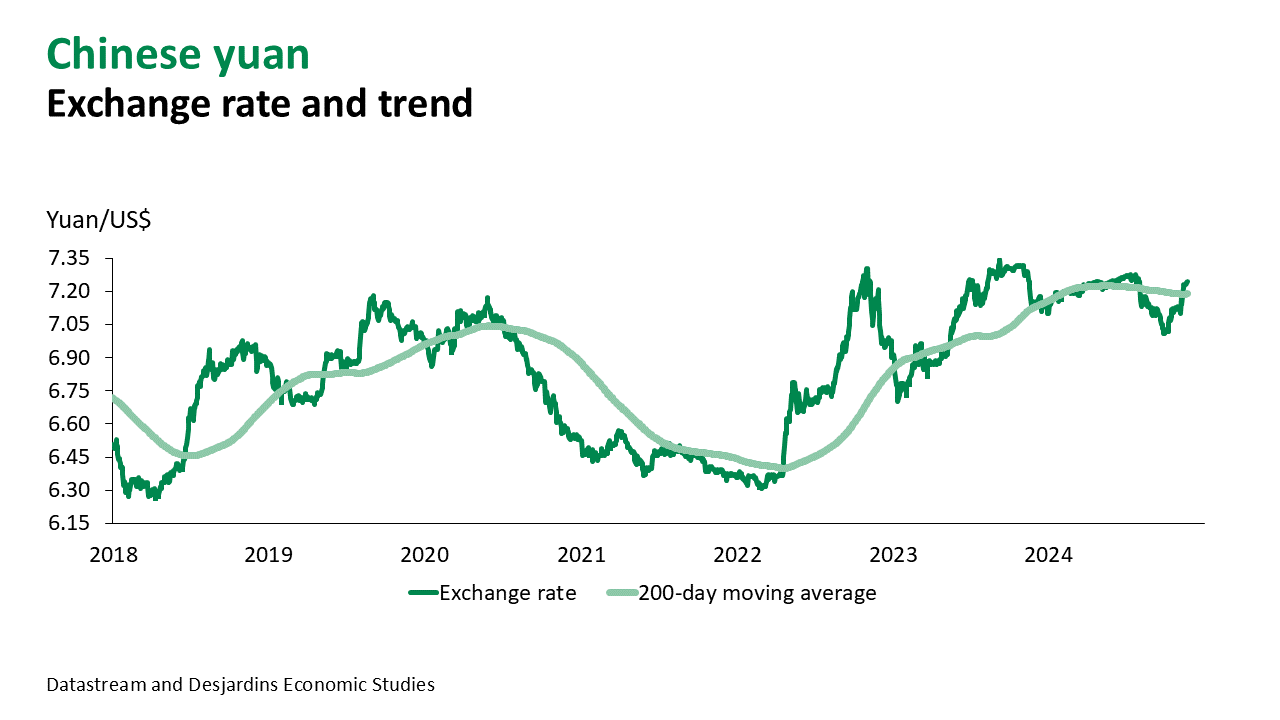

- In addition, Trump’s return to the White House is exacerbating global uncertainty on both the geopolitical and economic fronts. One of the biggest threats to many economies is the introduction of tariffs. Increased US protectionism would stifle economic growth around the world, with China being particularly at risk. On the campaign trail, Trump threatened to slap a 60% levy on Chinese imports. This would complicate what is already a difficult economic situation in China External link. and hurt the yuan, which is currently trading at around 7.25 yuan/US$.

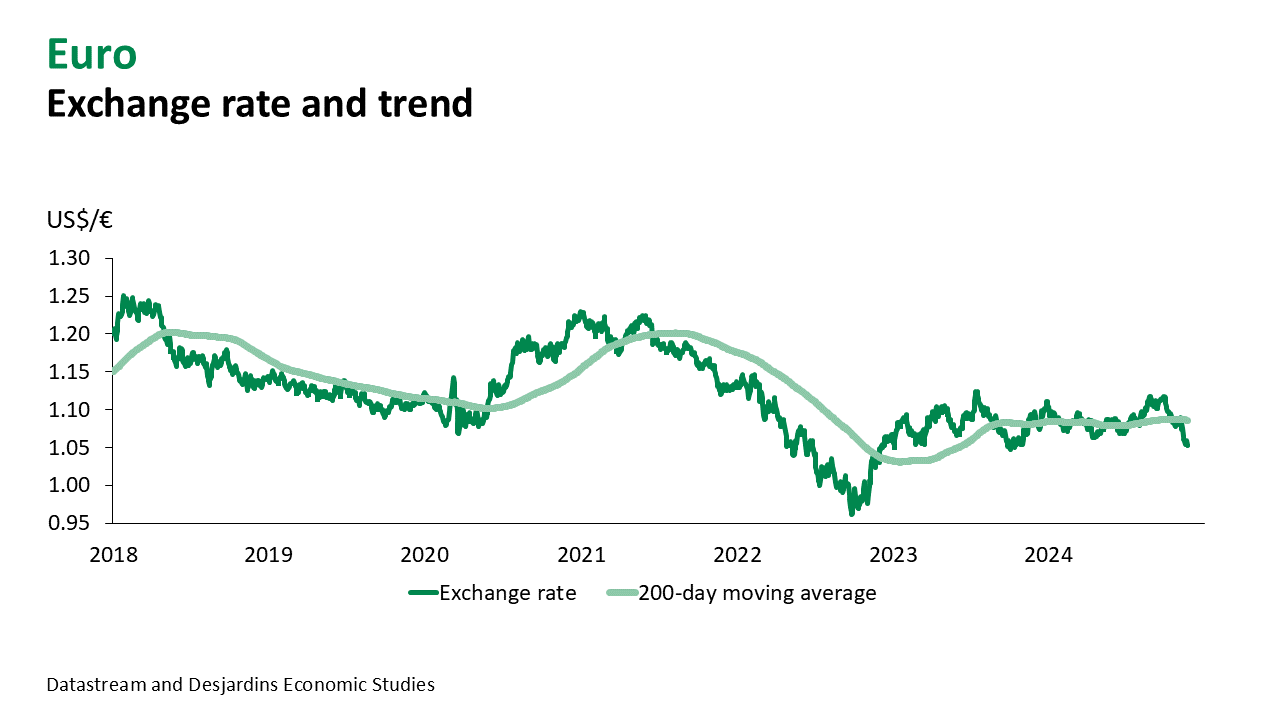

- Many other countries are also grappling with fragile economies, including many European nations. But the upside is that inflation has been coming down. The European Central Bank is now expected to make several interest rate cuts over the coming quarters. These expectations are weakening the euro, which recently approached US$1.05.

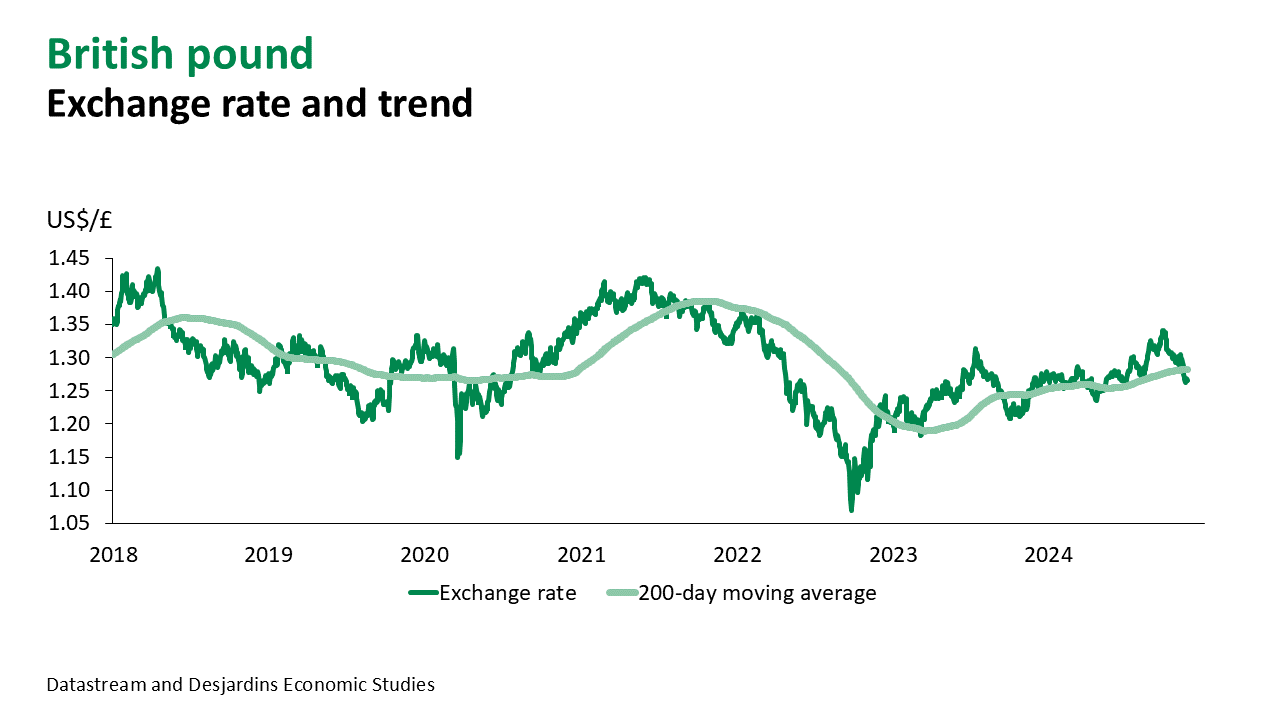

- Progress on inflation was a long time coming in the United Kingdom, but figures in recent months have been encouraging. While the progress is still largely being driven by falling energy prices, price growth is also slowing in other components. The Bank of England maintained its cautious stance in October, once again refusing to set the stage for successive rate cuts. However, this could change soon. The pound, which surpassed US$1.34 in September, has now dipped below US$1.27.

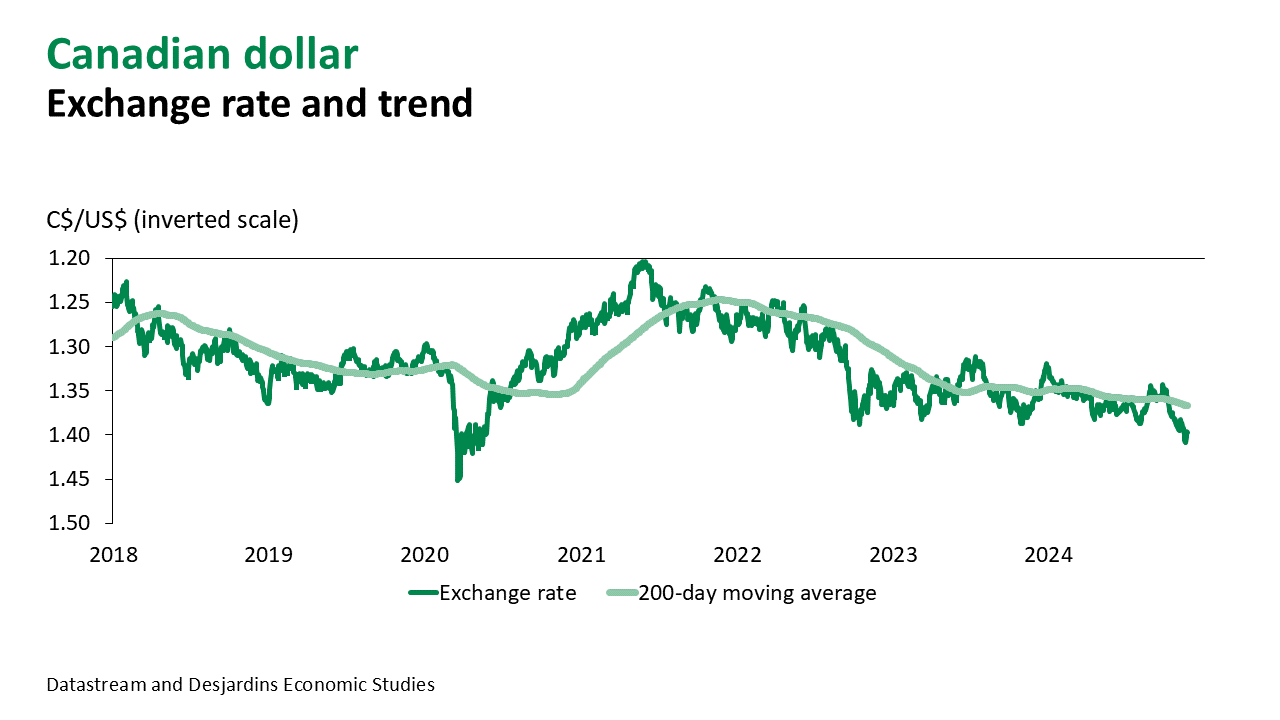

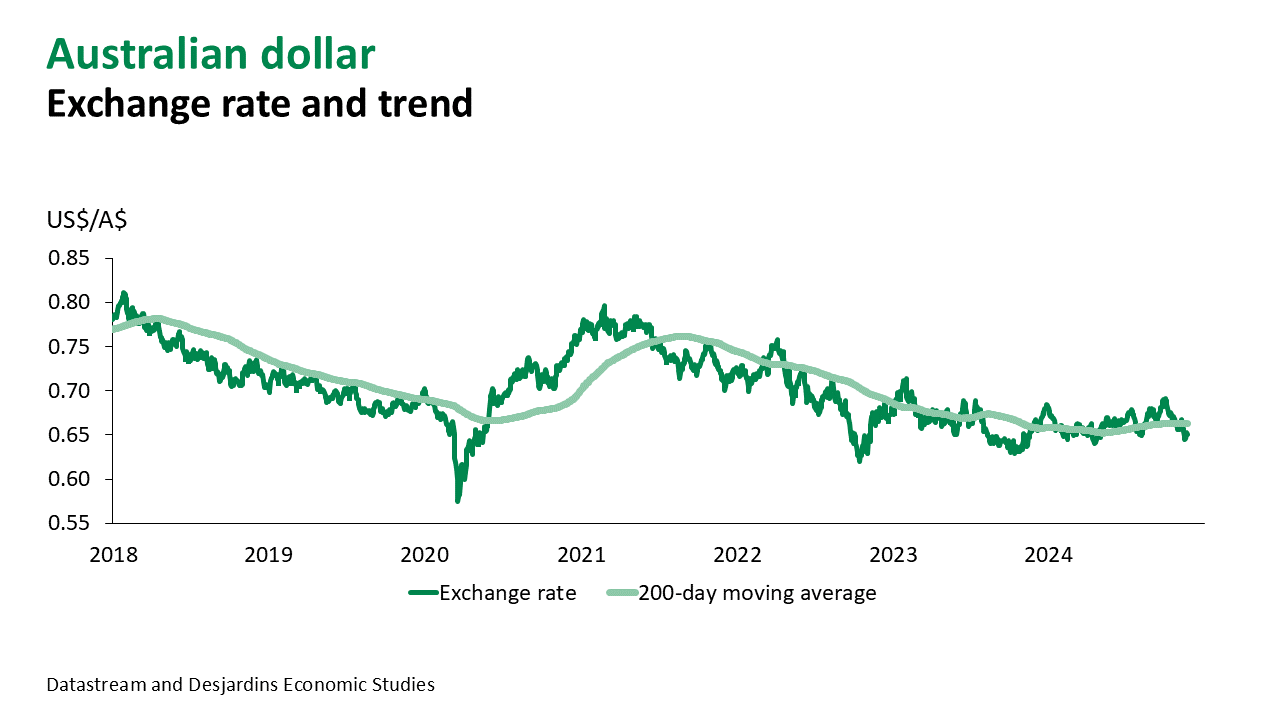

- Times are also tough for commodity-linked currencies. Heightened economic risks for the coming years are weighing on commodity prices. Plus, US oil, natural gas and coal production could rise under Trump’s policies, further limiting price increases for these products. The Canadian dollar has plummeted nearly 4.0% since the beginning of October. The Australian dollar lost slightly more, even though the Reserve Bank of Australia has yet to kick off its rate-cutting cycle. Concerns about the Chinese economy are proving to be particularly damaging to Australia’s currency.

- While the Canadian dollar has fared somewhat better than other commodity-linked currencies, its value is still a meagre US$1.40/C$ (just over US$0.71). The loonie has sunk below the nadirs of recent years and hit the levels recorded in the spring of 2020, when the first wave of the COVID-19 pandemic was in full swing. Given how heavily Canada depends on the US market, it could be one of the main victims of American protectionism. Canada faces other economic headwinds, like the mortgage renewal wall and a potentially dramatic decline in demographic growth if the federal government manages to curb immigration as planned. On the brighter side, inflation now seems to be under better control, which means we can expect several more key interest rate cuts. Of course, widening Canada–US interest rate spreads are bad news for the loonie.

Main Factors to Watch

- The foreign exchange market responded quickly to the new political landscape in the United States. The US dollar is way up, but it remains to be seen if the gains will be sustainable. Our forecasts have been updated to reflect a better part of Donald Trump’s policy proposals, including new tax cuts, deregulation (especially where it concerns energy), increased tariffs and reduced immigration. However, there’s still a lot of uncertainty about how and when these measures will be applied.

- If tariffs don’t take effect until late 2025 or even early 2026, the global economy could enjoy a temporary reprieve. And if US companies decide to get ahead of tariffs by making foreign purchases before the levies are applied, several countries could end up reaping the economic benefits. This could give many currencies a momentary boost against the US dollar. But the skies over many currencies would cloud over once again before the end of 2025 in anticipation of more challenging times in 2026.

- Changing monetary policies could also trigger high exchange rate volatility. We believe the US economy will have a hard time maintaining its current pace of growth. The recent rise in bond yields will likely weigh on the economy, and especially on the housing market. And with the labour market coming into better balance, wage growth and consumer spending will probably slow. We expect the Fed to announce several more interest rate cuts before opting for a more cautious approach once the Trump administration officially introduces measures deemed likely to drive up inflation.

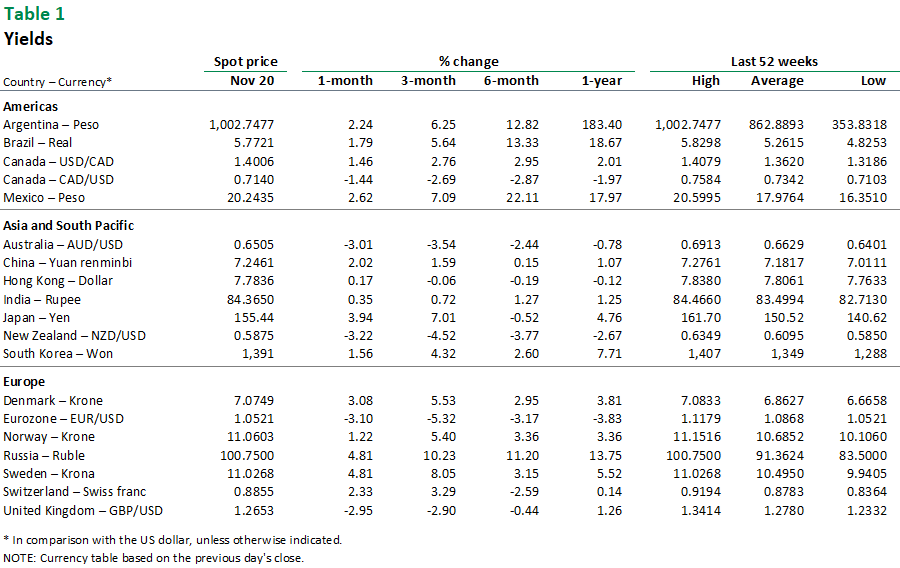

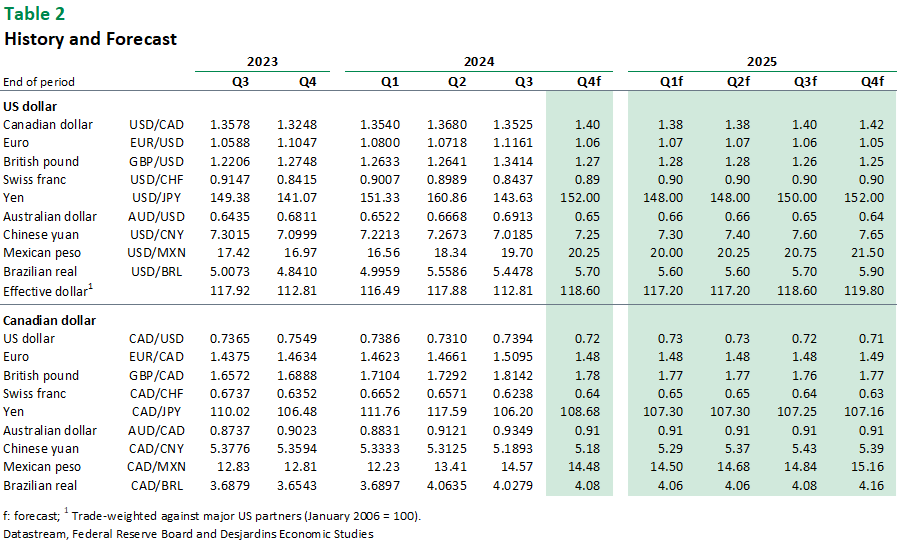

Main Exchange Rates

Currency Market