- Jimmy Jean, Vice-President, Chief Economist and Strategist

Mirza Shaheryar Baig, Foreign Exchange Strategist

FX Analysis

Rate Cuts and Curveballs

September 4, 2025

Highlights

- Global appetite for US assets has recovered. US monetary policy and data surprises will dominate FX dynamics through year‑end.

- We’ve become less optimistic on the Canadian dollar, as fading pension fund hedging and deeper rate cuts limit upside. The correlation of USDCAD to rate differentials is set to strengthen.

- Political and fiscal fragility in Europe and the UK are capping euro and pound gains despite earlier investor optimism; the euro’s strength is vulnerable to setbacks, and the pound may act as a pressure valve during gilt market stress.

- Asian currencies may catch up with the dollar’s decline. The yen could surge if risk sentiment sours, while the renminbi may appreciate gradually as China continues to gain global market share.

Overview

The most significant driver of US dollar weakness following “Liberation Day” was a shift in global asset allocation away from the US, coupled with increased hedging of US exposures by foreign asset managers.

In our view, those pressures have largely faded. Investors may be worried about the eroding credibility of US institutions, but they’re willing to look past it—at least for now. Foreign buying of US equities has resumed, signalling a renewed appetite for American assets.

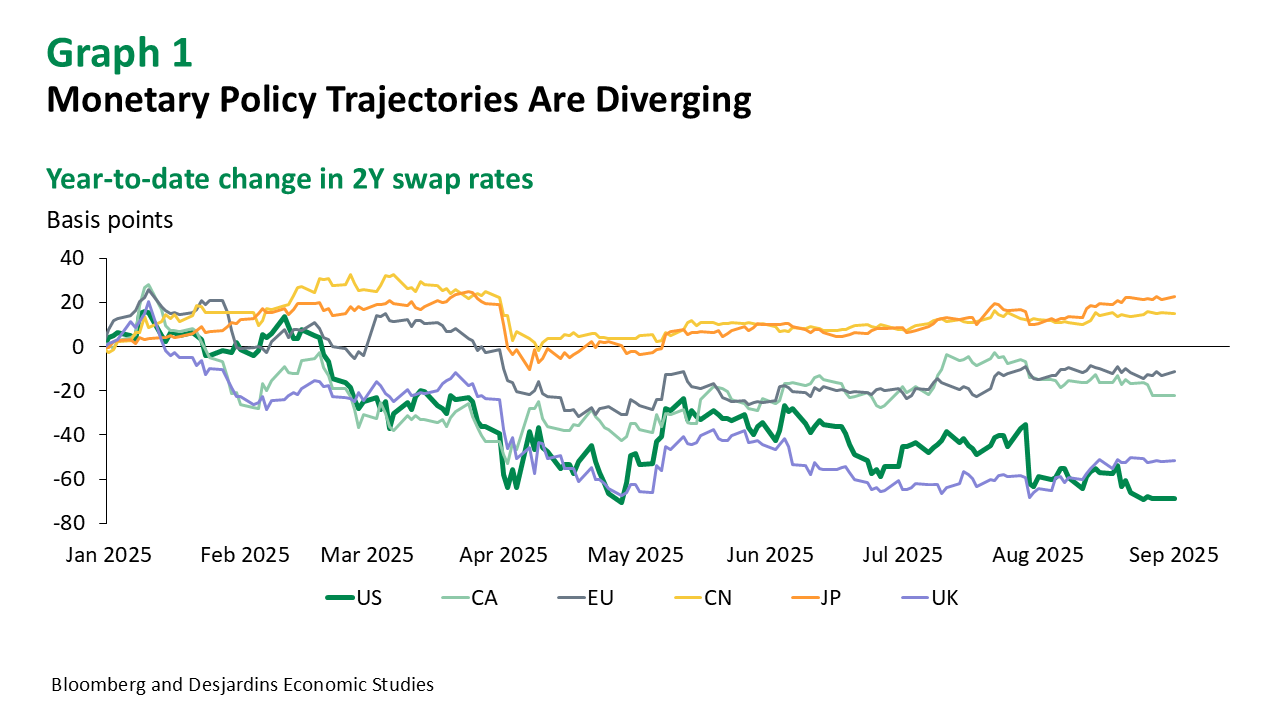

Looking ahead, we expect monetary policy to reassert itself as the primary driver of foreign exchange markets. The Federal Reserve and the Bank of Canada are both poised to resume rate cuts in September, while the Bank of Japan is preparing for a potential hike in October. Meanwhile the European Central Bank has signalled a pause, though weaker growth could compel it to ease again.

Across all major central banks, confidence in the path of policy remains low and the potential for surprises remains high.

Comments

Will Lower Rates Hurt the US Dollar?

The market has already priced in a terminal fed funds rate of 3.00%. However, there’s a risk that a politically influenced Federal Reserve could ease more aggressively, which would put the US dollar under renewed pressure in the near term.

The outlook for next year is clouded, with most jurisdictions around the world facing challenges. Growth in major economies outside the US remains sluggish, with Europe still grappling with elevated energy costs. Strained public finances, especially in the UK and France, may force governments to cut welfare spending, heightening the risk of social unrest. China is merely muddling through, leaning heavily on exports as domestic demand picks up only gradually.

In short, it may not be that difficult for the US to outperform the rest of the world. Even with lower interest rates, the dollar may benefit from relative economic strength next year.

We expect the US dollar to trade sideways or drift lower through the end of this year. While our forecasts imply a weaker US dollar next year as well, we have limited conviction in that call.

CAD

Rate Cuts to Weigh on the Loonie

Statistics Canada reported that GDP declined 1.6% SAAR in the second quarter, significantly worse than the consensus estimates. On the inflation front, Prime Minister Carney’s decision to remove most retaliatory tariffs should bring inflation closer to the Bank of Canada’s de‑escalation scenario from the July Monetary Policy Report, which sees inflation remaining below the central bank’s target for an extended period.

We expect the Bank of Canada to restart its rate‑cutting cycle at the September 17 decision date, ultimately pushing the policy rate below market expectations for a terminal rate of 2.50%.

With the Fed also poised to cut rates, the key question for USDCAD is who will surprise more—the Fed or the Bank of Canada? There are risks on both sides. We expect markets to focus more on relative data surprises and policy actions. As such, the correlation between USDCAD and rate differentials—which has been muted since April—is likely to strengthen.

We now see less upside in the Canadian dollar over the next year. We’re maintaining our 2025 year‑end forecast of 1.35, but changing our 2026 year‑end forecast from 1.30 to 1.33.

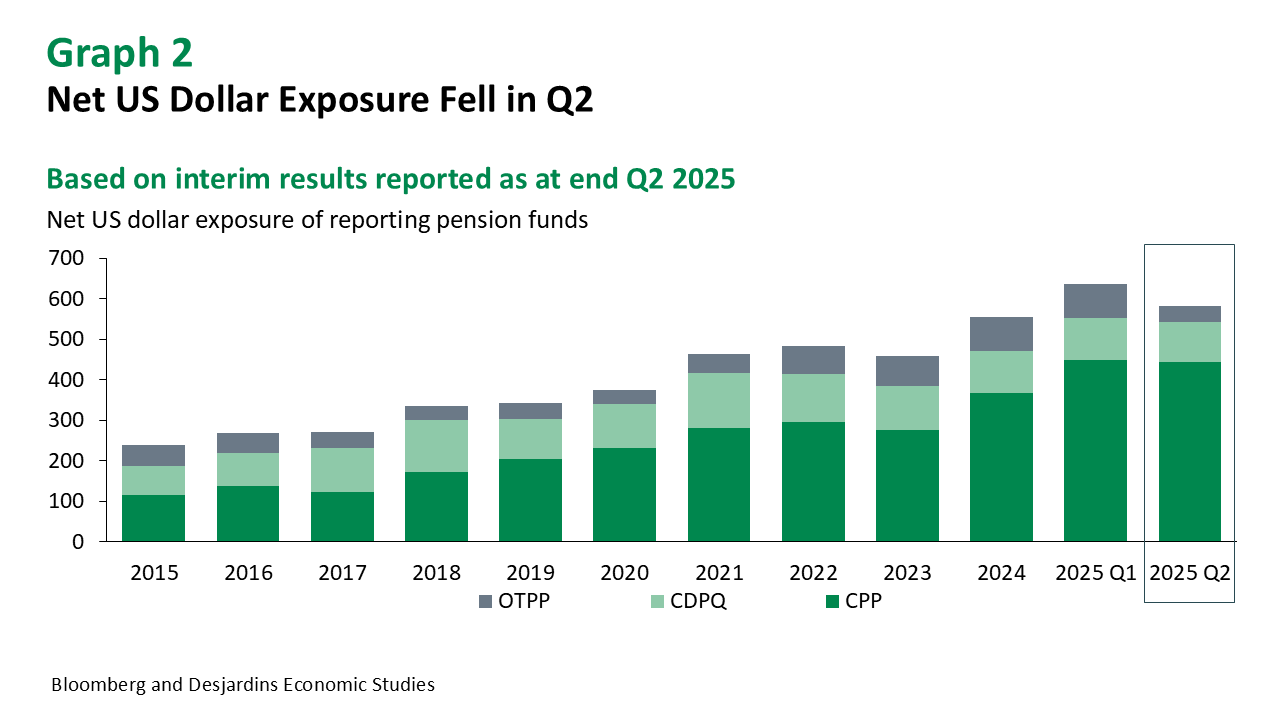

Pension Fund Hedging Is Largely Behind Us

Six of the “Maple 8” pension funds publish their currency exposures. Of these, four (CPP, CDPQ, OTPP and OMERS) have reported mid‑year updates covering data up to the end of June.

The two large public pension funds (CPP and CDPQ) did not report a material increase in forex hedges, while OTPP reported a substantial increase in hedges. OMERS’s interim results excluded a numeric breakdown of currency exposure, but the fund noted that currency hedging boosted their returns.

This data is consistent with our view that the bulk of the FX hedging flow from pension funds is behind us. Since the most active fund has already raised its hedge ratio, there is little scope left for a further increase, at least by that fund.

Future hedging will hinge on the usual cost–benefit trade‑off between the USD correlation with equities and, more importantly, the rate differentials embedded in FX forwards.

EUR

Inner Weakness

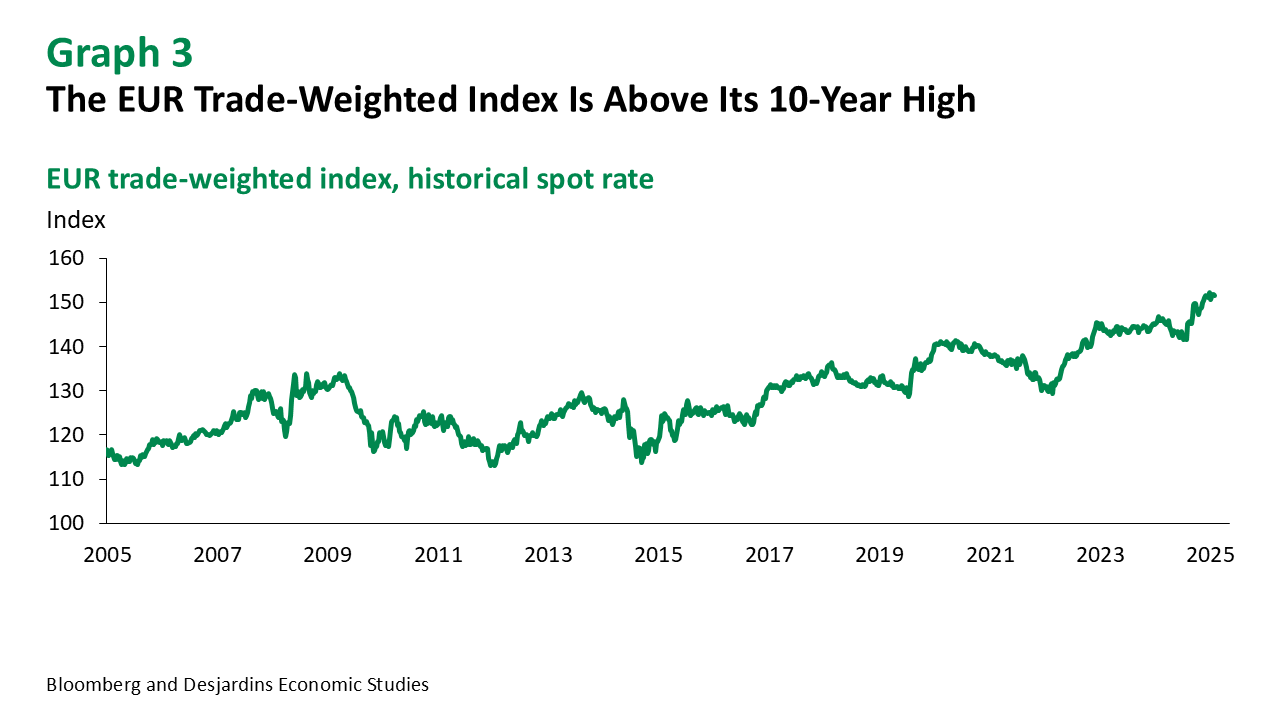

Earlier this year, the US dollar had to fall, and the path of least resistance was the flexible euro. Japan and China actively resisted currency appreciation, leaving the euro to bear the brunt of the falling greenback.

Investor inflows into European assets accelerated—not only to diversify away from the US, but also in response to Germany’s pivot towards a more expansionary fiscal policy, which many hoped would spark an investment boom across the continent.

Now, Europe’s internal fault lines are beginning to re‑emerge. A no‑confidence vote in the French government looms on September 8 over the austerity budget, with mass “Shutdown France” protests planned for September 10. Meanwhile German Chancellor Merz warned that higher defence spending will require cutbacks in welfare, which could cause his ruling coalition to splinter.

Even as President Trump continues to signal a weaker dollar by pushing the Fed toward rate cuts, the euro is already at its strongest level since 2010 in trade‑weighted terms. In our view, the scope for further gains is limited.

We maintain our 2025 year‑end forecast of 1.18 and 2026 year‑end forecast of 1.20. However, we don’t expect this to be a linear trend. Political instability and underwhelming growth could trigger periodic setbacks for the euro.

GBP

No Headroom, No Jobs

The UK fiscal outlook is deteriorating rapidly. Chancellor Reeves’ U‑turn on fuel subsidies and welfare cuts has left the government little choice but to hike taxes in the autumn budget on October 30. While higher taxes may plug the deficit, they will weigh on an already fragile growth outlook.

Most economists are skeptical that the UK can easily escape the vicious cycle of deteriorating fiscal conditions and sluggish growth. Although the gilts market has remained relatively stable for now, we believe time is running out.

We expect the pound to underperform both the euro and the US dollar, as investors will require a higher risk premium for holding UK assets. While our forecasts point to a gradual depreciation, the reality is likely to be more volatile. The pound will probably act as a pressure valve during periods of stress in the gilts market.

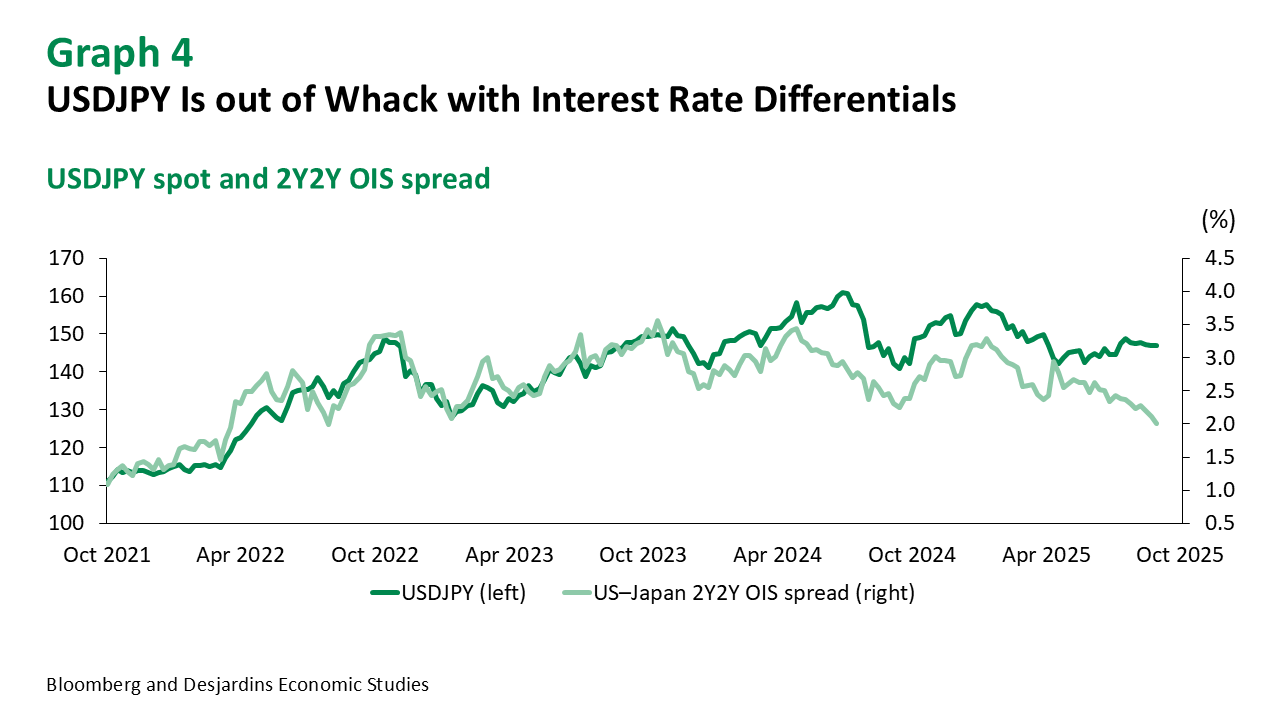

JPY

The Yen Could Surge on US Economic Concerns

The Federal Reserve and the Bank of Japan are poised to diverge in the coming months. At the Jackson Hole symposium, Fed Chair Powell opened the door to rate cuts, while Governor Ueda signalled a hawkish stance, noting that a tight labour market in Japan was pushing up wages.

Rates markets have responded accordingly, with US–Japan yield differentials narrowing to their tightest levels in four years. Yet USDJPY has remained surprisingly resilient, hovering around 147.

We believe the yen’s lack of appreciation is driven by two technical—not fundamental—factors: (1) strong risk sentiment has encouraged CTAs to use the yen as a funding currency, and (2) traders have grown tired of trading BoJ signals, as the central bank has repeatedly walked back its own hawkish signals this year.

We see potential for USDJPY to drop sharply if risk sentiment turns worse and leveraged investors begin to unwind their JPY shorts. Our forecast for year‑end 2025 remains at 145, but we see risks skewed lower.

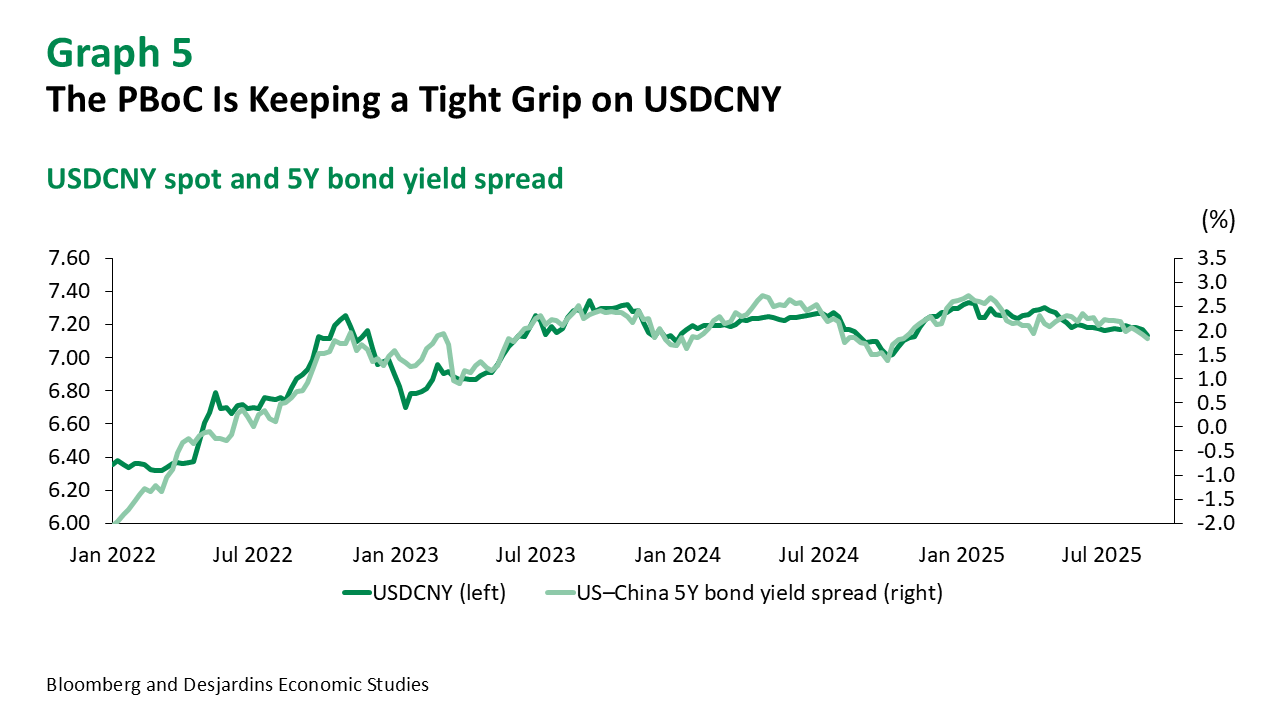

CNY

Stay Bullish

We think there is scope for a stronger renminbi in the coming months.

Based on the central bank’s preferred trade‑weighted index, the renminbi has depreciated by 6% this year. The PBoC has kept the USDCNY fixing rate virtually unchanged, causing the CNY to fall against most of its trade partners like the euro and the yen.

Chinese exporters have leveraged the weaker yuan to cut prices and become more competitive in non‑US markets. But this is alienating these other trade partners, especially the EU, which stands to lose the most from China’s export dominance.

We continue to anticipate a gradual appreciation of the CNY and expect USDCNY to fall to 7.00 by the end of 2025 and 6.80 by the end of 2026.

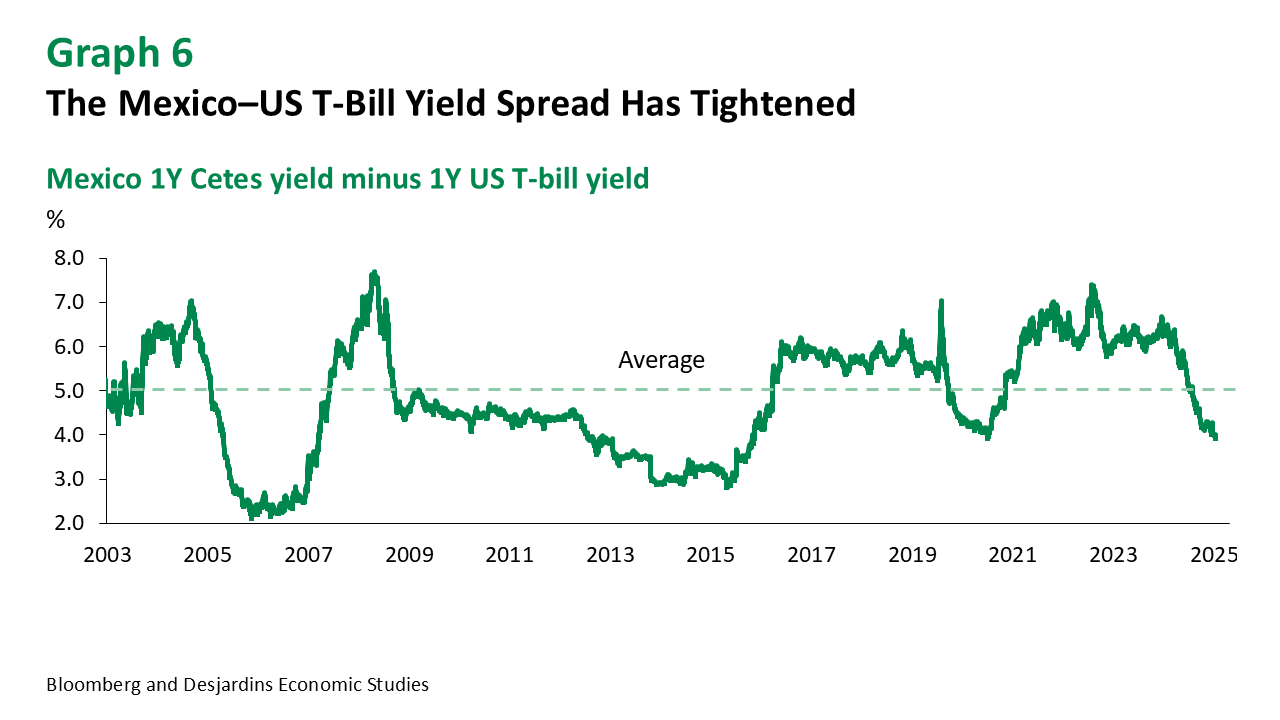

MXN

Where’s My Carry, Dude?

The Bank of Mexico cut the benchmark rate by 25bps to 7.75% in early August and left the door open to further rate cuts.

We expect the central bank to cut rates by 25bps at its next two meetings, on September 25 and November 6, after which the decisions are likely to be more dependent on the Fed.

The yield differential between US and Mexico T‑bills has declined to about 4%, the lowest in 10 years. While the Mexican peso has remained stable so far, we think the central bank will be mindful that a further narrowing of the spread could put pressure on the peso.

We expect the MXN to remain stable around recent ranges, barring a sharp increase in global risk aversion.

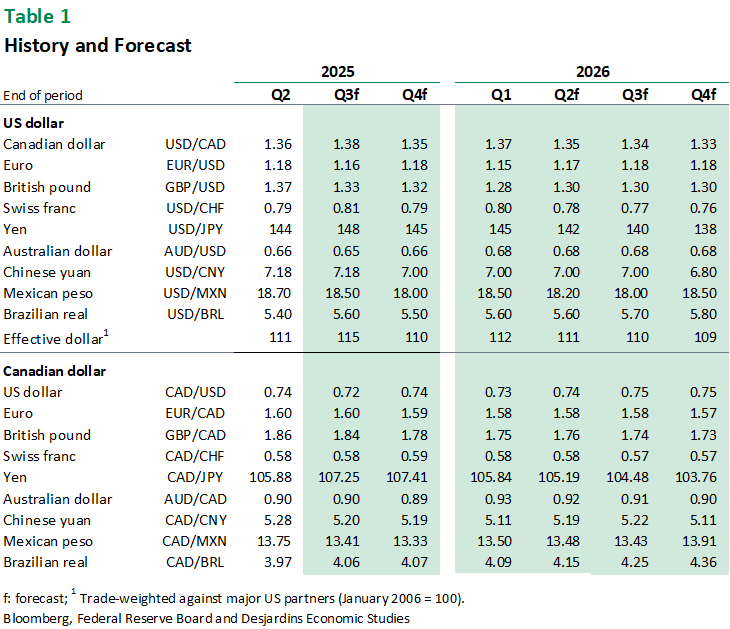

Forecast Table