- Jimmy Jean, Vice-President, Chief Economist and Strategist

Mirza Shaheryar Baig, Foreign Exchange Strategist

FX Analysis

There’s Life After 40

October 22, 2025

Highlights

- USDCAD is back above 1.40. Our year-end USDCAD forecast of 1.35 now looks out of reach. It’s time to reassess.

- Pension fund hedging flows have abated and Canada’s growth continues to lag the US. USDCAD is realigning with rate differentials, which may move against the loonie.

- We’ve revised our outlook: We expect the Canadian dollar to stay soft over the next two quarters, followed by a gradual recovery later next year.

Overview

The Canadian dollar has depreciated to 1.40 against the US dollar. Our year-end forecast of 1.35 now appears unlikely. Pension fund hedging flows have abated, and the exchange rate has re-established its link with rate differentials, which may drift against the loonie. We have changed our forecasts and now expect the loonie to remain soft in the next two quarters before gradually strengthening towards the end of next year.

Comments

After briefly firming to 1.35 against the US dollar in June, USDCAD reversed course and traded back above 1.40 this month.

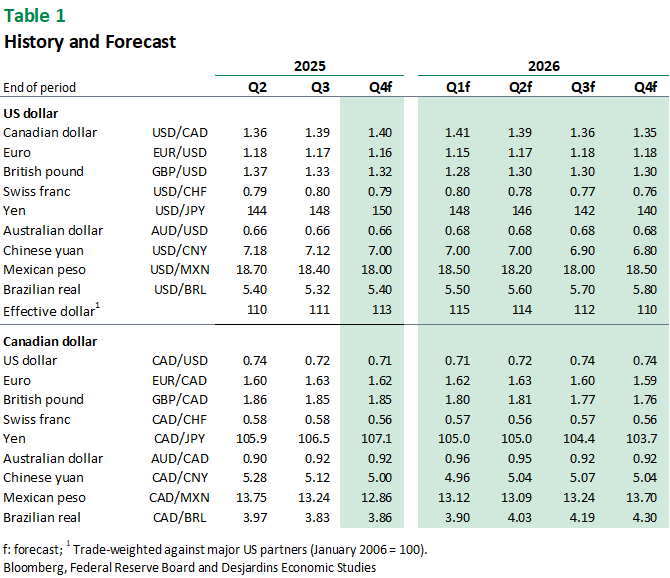

This wasn’t just a US dollar story. Since June, the loonie has lost ground against the currencies of most of Canada’s major trading partners—it’s down 6% against the Mexican peso, 5% against the euro and 3% relative to the renminbi. The Bank of Canada’s CEER Index, a trade-weighted proxy for the Canadian dollar, is now near a nine-year low (graph 1).

Why did the loonie turn weaker? We suspect two key drivers: Pension fund hedging flows have faded, and Canada’s economic momentum has slowed.

What does this mean for our outlook? Our year-end USDCAD forecast of 1.35 now appears a longshot. We have changed our forecasts and now expect the loonie to remain soft in the next two quarters before gradually strengthening towards the end of next year.

Canada’s Underperformance May Persist

Canada’s economy continues to face a familiar set of headwinds. The rapid deceleration in population growth has left pockets of excess capacity. Household budgets are under pressure from ongoing mortgage resets, and business sentiment remains cautious amid uncertainty over US tariffs.

Despite quarterly volatility, Canada’s economy didn’t grow in the first half of 2025, and our tracking suggests Q3 growth is on pace for an advance of less than 1.0%. Rising unemployment among core-aged workers (25–54) underscores the need for more policy support. While fiscal stimulus is expected, its impact won’t be felt until well into 2026. Thus, monetary policy will have to carry the load for now. We expect the Bank of Canada to cut rates to 2.00% faster than the market currently anticipates.

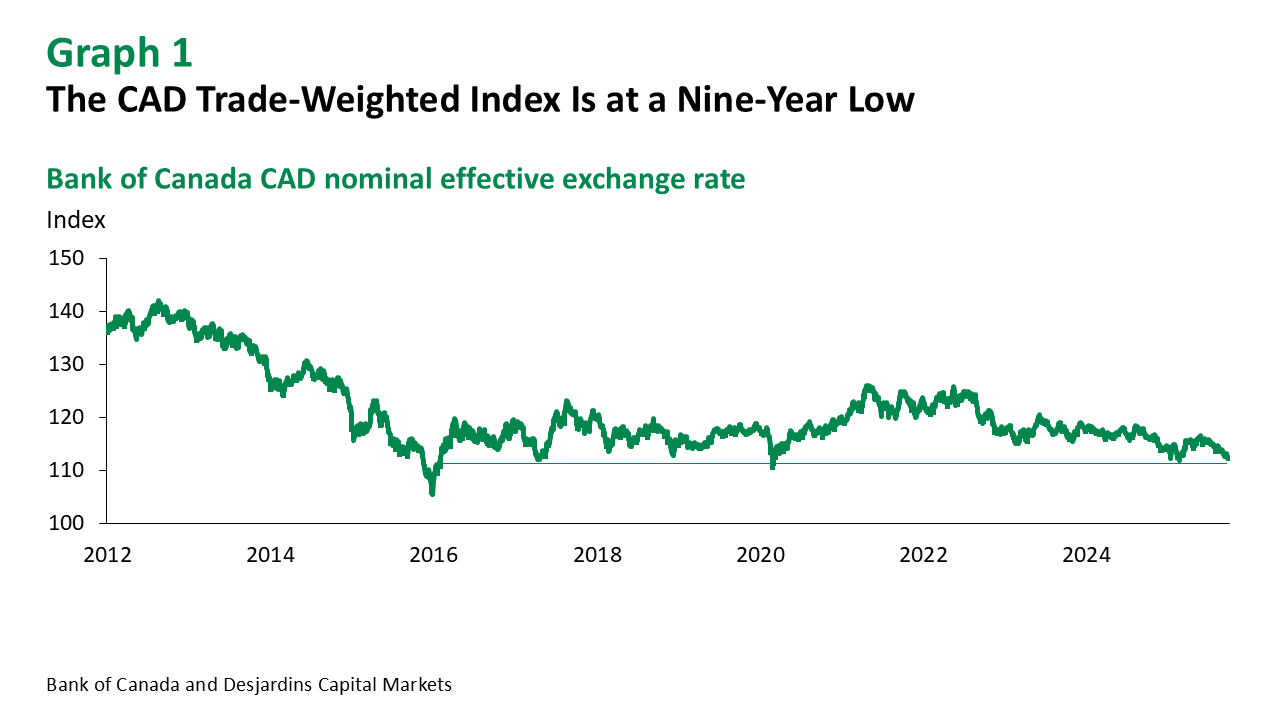

In contrast, US growth continued in the first half of 2025, supported by resilient consumer demand and strong business investment—especially in high-tech sectors. Since mid-year, economists have significantly upgraded their US growth forecasts (graph 2). The Atlanta Fed’s nowcast model for Q3 GDP growth is running at 3.9%.

That said, there are some key risks which could trigger a sharp slowdown in the US economy. These include escalating trade tensions with China over access to rare earth minerals, a prolonged federal government shutdown and a significant correction in the highly valued US tech sector.

The US dollar has stabilized for now but remains vulnerable should any of these risks materialize. This underscores the asymmetric nature of probability distribution in the forex market: while the baseline scenario points to a slightly higher USDCAD, the distribution of risks is skewed towards a weaker US dollar.

Pension Fund Hedging – Reversing or Merely out of Steam?

Our review External link. of mid-year results from Canadian pension funds showed that some fund managers significantly raised their forex hedge ratios in Q2.

Some observers argue that fund managers may be unwinding earlier hedges, adding extra fuel to recent CAD weakness. We’re skeptical. Large shifts in portfolio strategy typically require strong conviction. In our view, pension funds made a large adjustment in Q2 and are now simply on the sidelines. With the hedging wave behind us, rate differentials have reasserted their influence on USDCAD.

Converging with Rate Differentials

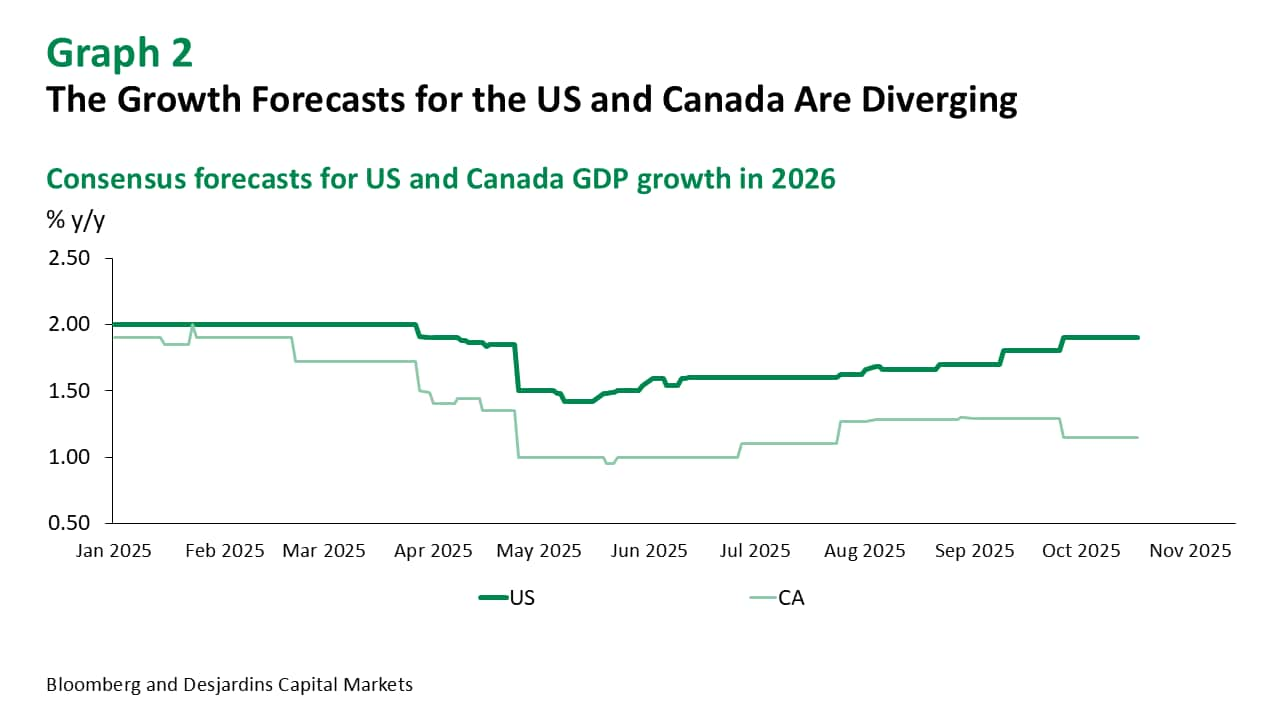

According to our factor decomposition model for USDCAD, front-end rate differentials have had the highest explanatory power since 2021. The relationship broke down between April and July amidst declining confidence in the US dollar and the actions of some Canadian pension funds to hedge their USD risk.

The historical relationship between the level of rate differentials and USDCAD appears to be reasserting itself, with full convergence indicated between 1.40 and 1.42 (graph 3).

Could the spread widen further? We expect the Federal Reserve to cut rates to 3.125% in our baseline scenario, but the market has US central bankers getting there much quicker than we do. Conversely, while the market is almost pricing in our 2.00% terminal rate forecast for the Bank of Canada, we expect monetary policymakers to get there quicker than market participants currently anticipate.

Updating Our Forecasts

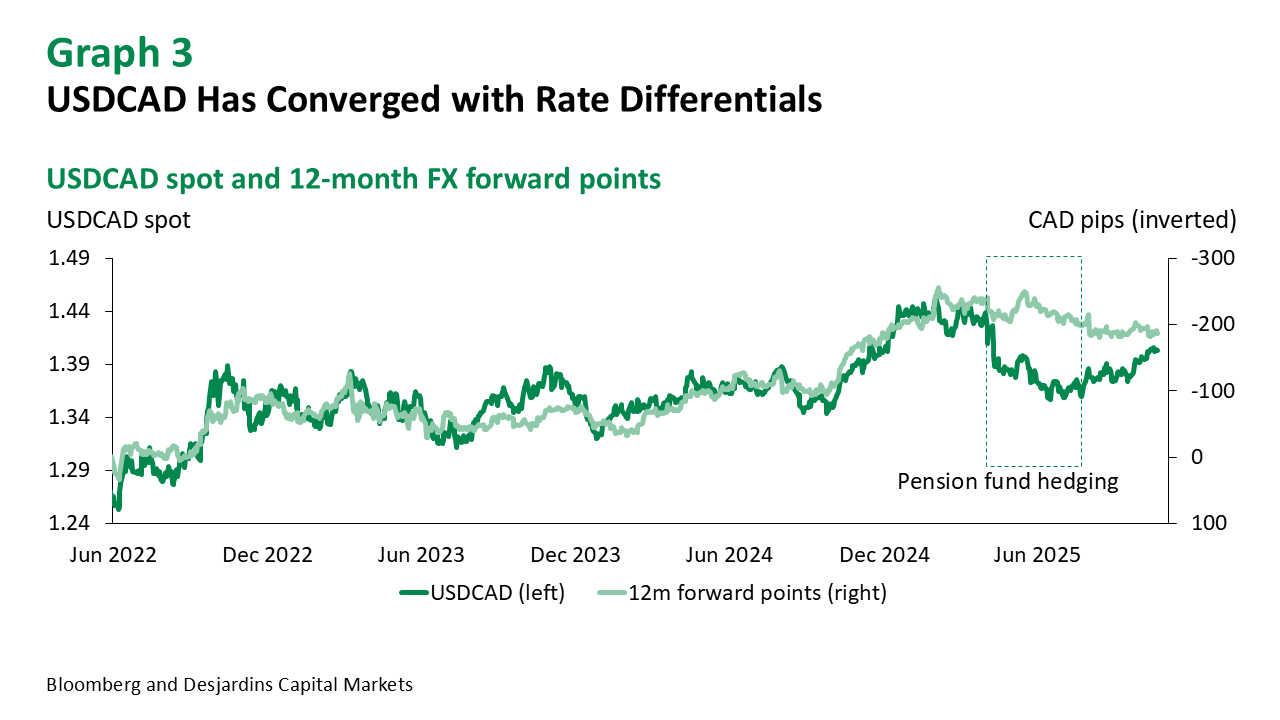

We've made substantial revisions to our USDCAD forecasts. We now expect the loonie to consolidate above 1.40 over the next two quarters. This reflects a modest widening in the US–Canada rate spread, persistent uncertainty around the CUSMA revision soap opera and continued resilience in the US economy. Further out, we see the loonie strengthening against the greenback and ending 2026 around 1.35 (table 1).