- Jimmy Jean, Vice-President, Chief Economist and Strategist

Mirza Shaheryar Baig, Foreign Exchange Strategist

FX Analysis

Pausing for Breath

May 1, 2025

Highlights

- The decade-long bull market for the US dollar has come to an end, as the notion of “American exceptionalism” that supported it is no longer assured.

- But after a 10% decline and substantial unwinds of overweight positions in US assets, the US dollar may be set for a near-term reprieve. We would sell USD on rallies.

- Recent USDCAD declines have been driven by USD weakness rather than CAD strength. Delivering on credible fiscal stimulus and investment reforms could extend CAD gains.

- Can the euro be an alternative to the dollar? Investors and reserve managers have shunned the euro for years, so there is scope for a shift on the margin.

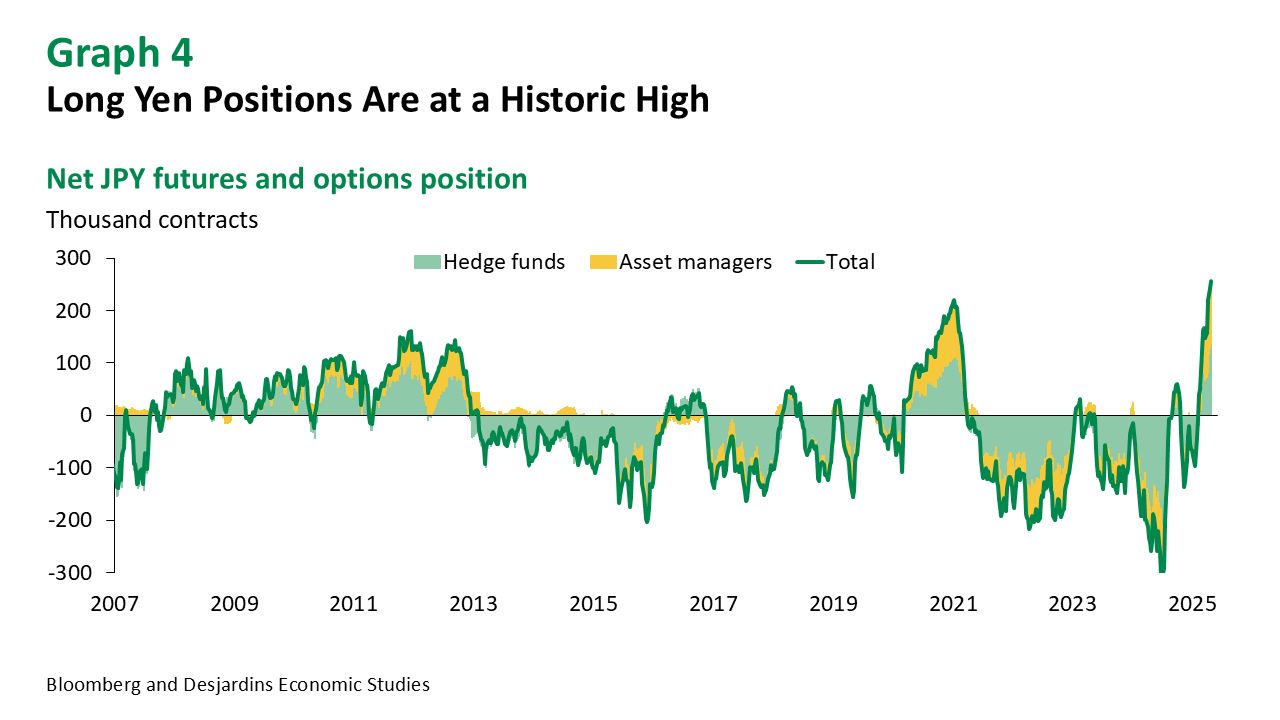

- The yen lived up to its appeal as a safe haven. But foreign asset managers are now record long, so it could stall for a while.

- China now has spare capacity and a cheaper currency. Brace for import-driven deflation in other countries!

Overview

Position Unwinds Done, but Dollar Downtrend Not Over

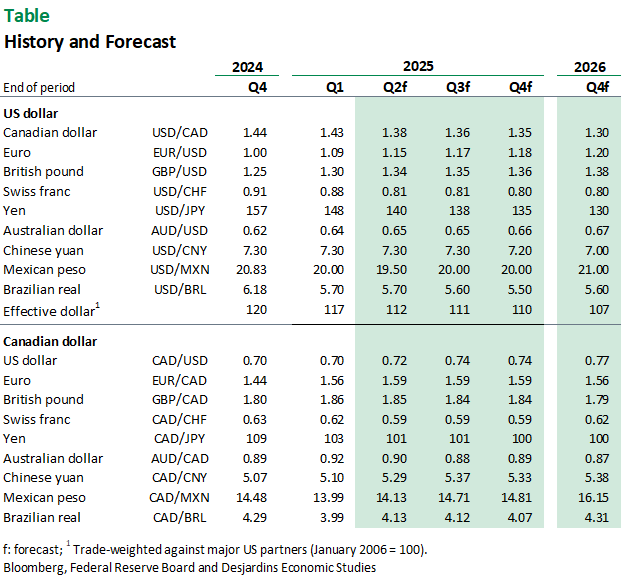

The broad US dollar index is now down 10% from its peak in January. Several technical indicators, including our short-term fair value model for USDCAD, suggest the dollar may be oversold versus developed market currencies. CTA positioning, which is a good proxy for speculative sentiment, has shifted from record long dollar positions to sizable shorts, particularly versus the yen. The implied volatility skew of EUR calls over USD puts is now at a historically extreme level. Furthermore, President Trump appears to have dialled back some of the more egregious threats like firing Federal Reserve Chairman Powell. All this suggests that the dollar may be due for a short-term reprieve. Currencies don’t move in straight lines, and we wouldn’t be surprised if there was some mean reversion in the coming weeks.

However, we believe the decade-long bull market for the US dollar has come to an end, as the notion of “American exceptionalism” that supported it is no longer assured. Stronger US growth versus the rest of the world and superior market returns were responsible for the dollar’s strong valuations. But the chaos following “Liberation Day” has raised concerns over corporate profit margins and real incomes in the US, while Europe and China have been forced to double down on fiscal and structural policy to boost their own growth prospects. Investors have voted with their feet and reduced allocation to US assets in favour of global—especially European—assets.

There may be a policy put in bonds, and perhaps even in stocks. But it’s clear that there is no such support for the US dollar. At last week’s IIF summit, US Treasury Secretary Scott Bessent mentioned that the strong dollar policy meant “having the policies in place to deserve capital flows, but it doesn’t mean the price of the dollar that you see on the Bloomberg screen.” In fact, the Trump administration is likely to welcome a weak dollar as it makes US exports more competitive.

In short, the USD may rebound after its sharp sell-off, but we would look to sell rallies.

CAD

Fiscal Factor

We remain optimistic on CAD and expect it to extend gains versus USD. We have brought forward our forecast of CAD appreciating to 1.35 versus USD from 2026 to this year. We see scope for further gains to 1.30 next year.

The move down in USDCAD since “Liberation Day” is largely a US dollar move. The Canadian dollar has underperformed compared to its trade partner currencies, hitting post-Covid lows against the euro and staying in a range against the Mexican peso. Year to date, the loonie is one of the weakest performers among the major currencies.

Monetary policy is unlikely to provide much support for the loonie in the near term. The Bank of Canada (BoC) paused in April, citing the need for more clarity on the tariff impact on inflation. We expect them to resume cuts starting at the June meeting, which isn’t fully priced by the market.

The BoC has put the onus of countering the drag from the trade war on fiscal policy, and it’s likely that the new government in Ottawa will scale up fiscal support. However, just printing wider deficits is not a remedy for Canada’s struggling economy. The currency market will focus on whether new policies will boost labour productivity and improve the investment climate in Canada. Canada needs investment in infrastructure like roads, rail, ports and airports. Some of these investments could be structured as project financing deals, which would suit the investment objectives of long-term investors, particularly Canadian pension funds.

EUR

No More TINA

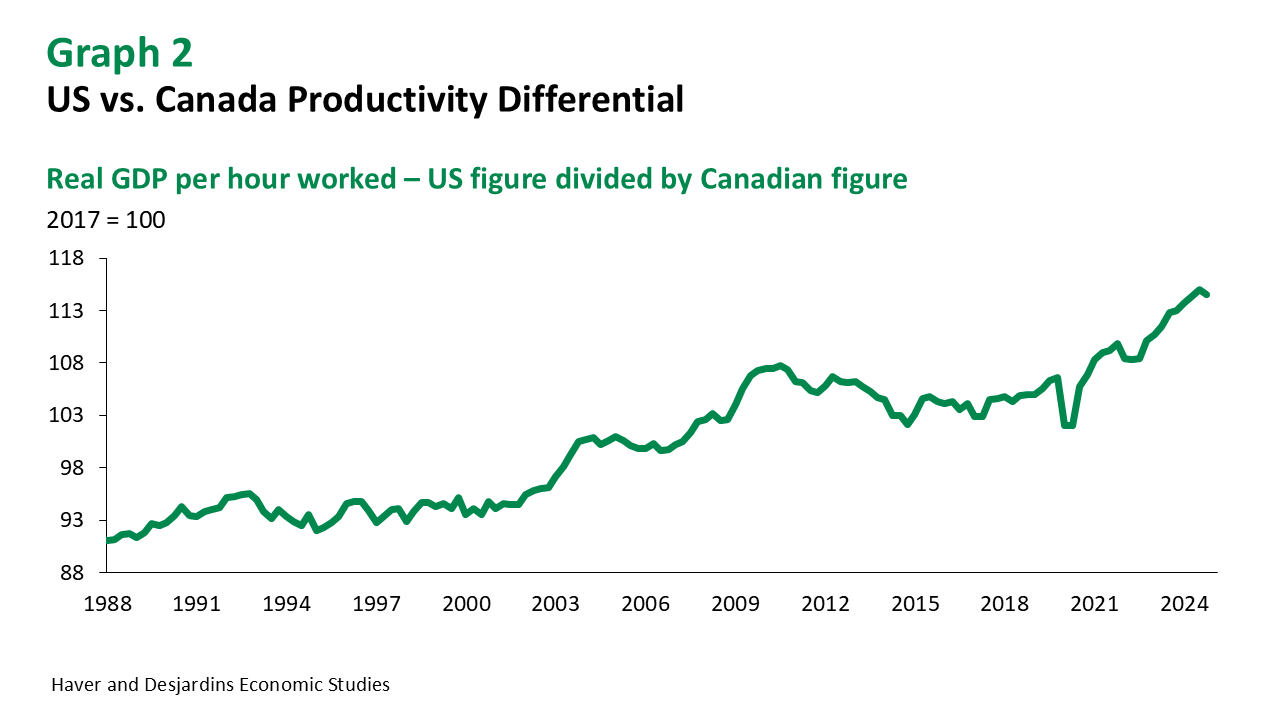

Market participants often refer to the US dollar’s dominance using the acronym TINA, “There Is No Alternative.” The term implies that even though the US runs huge deficits, one is better off holding dollars because the euro area could break up, Japan has deep structural problems and China has capital controls.

But financial flows now suggest the euro is in the limelight as a potential dollar alternative. ETF flows suggest equity investors have turned away from America’s tech-heavy stock market towards Europe’s more industrials-heavy indices. Official reserve flows are hard to track in real time, but the significant divergence between bunds and Treasuries in April suggests reserve managers may be moving from US dollars to the euro. The euro’s share in global reserves has been languishing around 20% for the last 10 years, but it used to be above 25% before the Lehman crisis when the US was running twin deficits comparable to today’s. We reckon this rotation from dollars to euros might play out over several months or even years.

There are geopolitical factors to consider as well. Will Europe join the US in shutting out China from its markets? Or will it play a more even hand and manage to partner both sides? Will Germany’s fiscal stimulus be as transformative as investors hope? And while internal euro area imbalances are smaller than they were at their peak levels, have the concerns about a break-up of the currency union truly gone away? These are unanswered questions, though the market is now viewing them through rose-tinted glasses.

Finally, there is the question of safety over yield. The ECB sees a strong euro as a tightening of financial conditions. ECB President Lagarde described the euro’s strength as “counterintuitive” at the IIF summit last week. Indeed, we think the strong currency was one factor behind her dovish tilt at the April ECB meeting. The market is now pricing the ECB to cut its policy rate down to 1.50% by the end of this year compared to 3.50% for the Fed. Investors may ignore the negative carry for a while, but if the US economy manages to avoid a recession this year, some of the recent flows into the euro might reverse.

JPY

JPY Strength May Be Overdone

The yen has lived up to its traditional safe-haven status amidst recent turmoil. We expect risk aversion in equity markets will continue to support the yen. This is despite the Bank of Japan now signalling a pause at the June policy meeting, which was fully priced for a 25bps hike before “Liberation Day.” Some market participants are also wondering if the yen will feature in the trade deal that US and Japan are currently negotiating. We reiterate our year-end forecast of 135.

However, we do not expect a sizable appreciation in the near term. The 140 level is a key support area. Foreign asset managers now have record long yen positions. This is a testament to the yen’s status as a safe haven, but also suggests positions are quite extreme. Finally, the trade agreement may simply reiterate Japan’s commitment to the G7 statement, which promises not to devalue currencies for competitive gain. In recent years Japanese authorities have intervened to strengthen the yen, so this wouldn’t have any marginal effect.

Net-net, while we expect the yen to appreciate over time, it may consolidate in the near term.

CNY

Here’s My Number, So Call Me Maybe

The tariff war between the US and China has escalated dramatically, with both countries imposing significant tariffs on each other’s goods. More recently, both sides have exempted specific product categories, and US media has circulated sourced articles saying that President Trump will lower the 125% reciprocal tariff to a more “reasonable” 50%–60% soon.

It’s crucial for President Xi to maintain a strong stance in negotiations. Moreover, his more statesman-like approach is in total contrast to the style of the US president. China has appointed Li Chenggang as a new trade tsar and asked the US to name one of its own so that negotiations can be conducted. President Trump says he expects President Xi to give him a personal call.

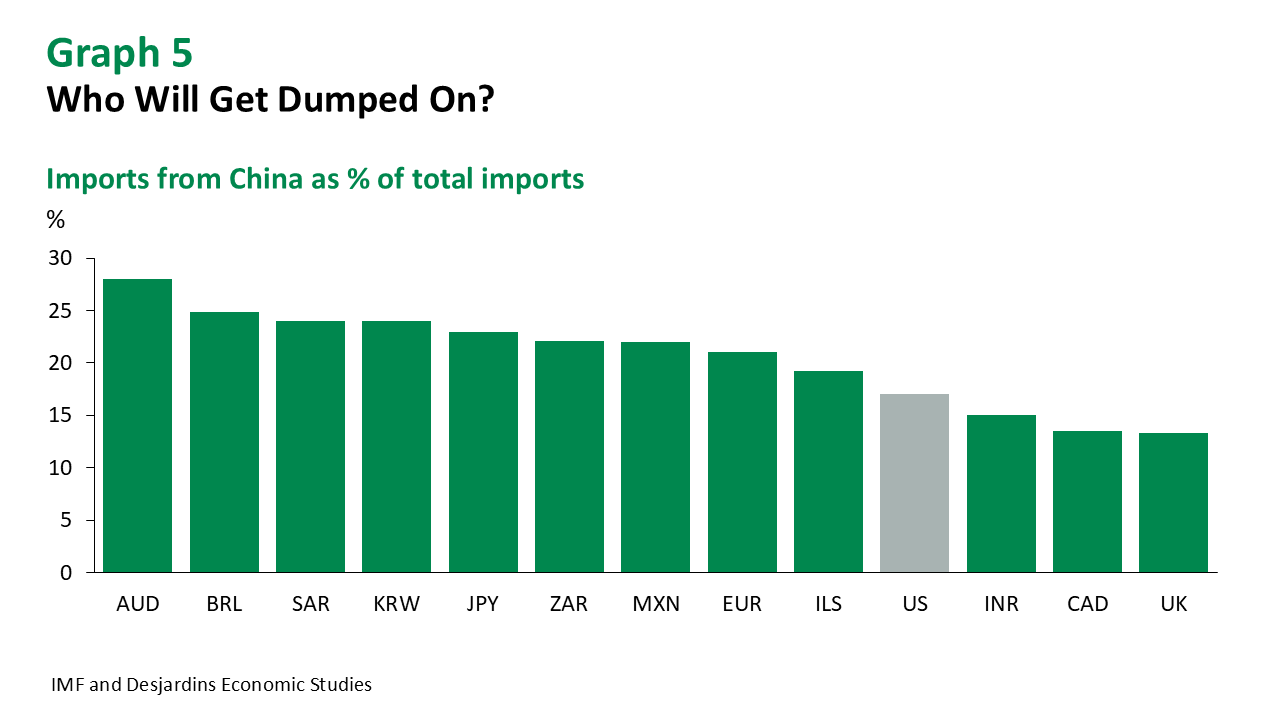

The PBoC has kept the renminbi stable versus the US dollar, and as a result, the RMB has depreciated versus most other currencies. In trade-weighted terms, the RMB has cheapened almost 6% this year. This will help Chinese exporters cut prices and divert what they used to sell in the US to other markets. Investors should watch this trend carefully as it may widen inflation divergence between the US and other major economies.

While the tariff war is in the spotlight, the US and China are also waging an “influence war” to win over other countries. China offers both carrot and stick—President Xi says he supports preserving the rules-based global trading system, while his Ministry of Commerce has threatened countermeasures against any nation that strikes trade deals with the US at Beijing’s expense. The Trump administration says it is negotiating bilateral trade deals with several countries, but it’s not clear whether they are pushing to undercut China.

We expect the US and China will eventually come to some sort of détente. But the economic consequences of a prolonged standoff are global. Early estimates put the potential hit to global output in the US$1.5–2.0T range. Commodities are already reflecting the stress, with familiar bellwethers like oil and copper under pressure this month.

Forecast Table