- Jimmy Jean, Vice-President, Chief Economist and Strategist

Mirza Shaheryar Baig, Foreign Exchange Strategist

FX Analysis

FX Analysis: The Worst Is Over for the Loonie

March 27, 2025

Summary

- The Bank of Canada has turned cautious on the pace of rate cuts, while the Fed waits for hard data. Yield spreads may narrow, especially if the US labour market cracks.

- We now see USDCAD holding in a 1.41–1.45 range over the next three months and expect CAD to appreciate over the medium term, especially if economic reforms post elections improve the growth outlook and convince domestic asset managers to “buy Canadian.”

- With the EU fiscal pivot now largely priced into markets, further upside for European currencies may be limited.

- Japanese wage and inflation data have exceeded expectations. Japanese interest rates and the yen are set to rise further, albeit gradually.

- China’s central bank continues to prop up the RMB while authorities woo foreign capital for local companies.

Swapping Places: The Fed Out-Doves the BoC

US trade policy continues to weigh on the economic outlook for North America. Our economics team now expects a shallow recession on both sides of the border starting in Q2.

Inflation is likely to rise, but there are different views on how central banks should deal with it. If tariffs result in a one-time price increase, they can look through it. But if higher prices lead to rising inflation expectations, they may need to tighten monetary policy or, at the very least, slow the pace of easing.

The Bank of Canada and the Federal Reserve see things differently.

The Bank has become concerned about rising inflation expectations, signaling a pause in its rate cut cycle. The statement noted that monetary policy must “ensure that higher prices do not lead to ongoing inflation.” Governor Macklem’s prepared remarks at the press conference included two references to the weak Canadian dollar contributing to inflation, compared to zero mentions of the currency at the January meeting. In follow-up remarks the next day, the Governor noted “there can be no doubt about the central bank’s commitment to low inflation.”

In contrast, the Fed opted for a wait-and-see approach. But reading between the lines, there were some dovish messages. Officials cut their growth forecast for 2025 to 1.7% from 2.1% and marked down their 2026 and 2027 forecasts by 0.2% and 0.1% respectively. On the other hand, they increased their core inflation forecast only for 2025, leaving the 2026 and 2027 forecasts unchanged. This suggests the Fed is more concerned about the persistence of a growth shock than inflation. In fact, with no sense of irony, Chair Powell mentioned in the press conference that in his base case, the impact of tariffs on inflation will be “transitory.”

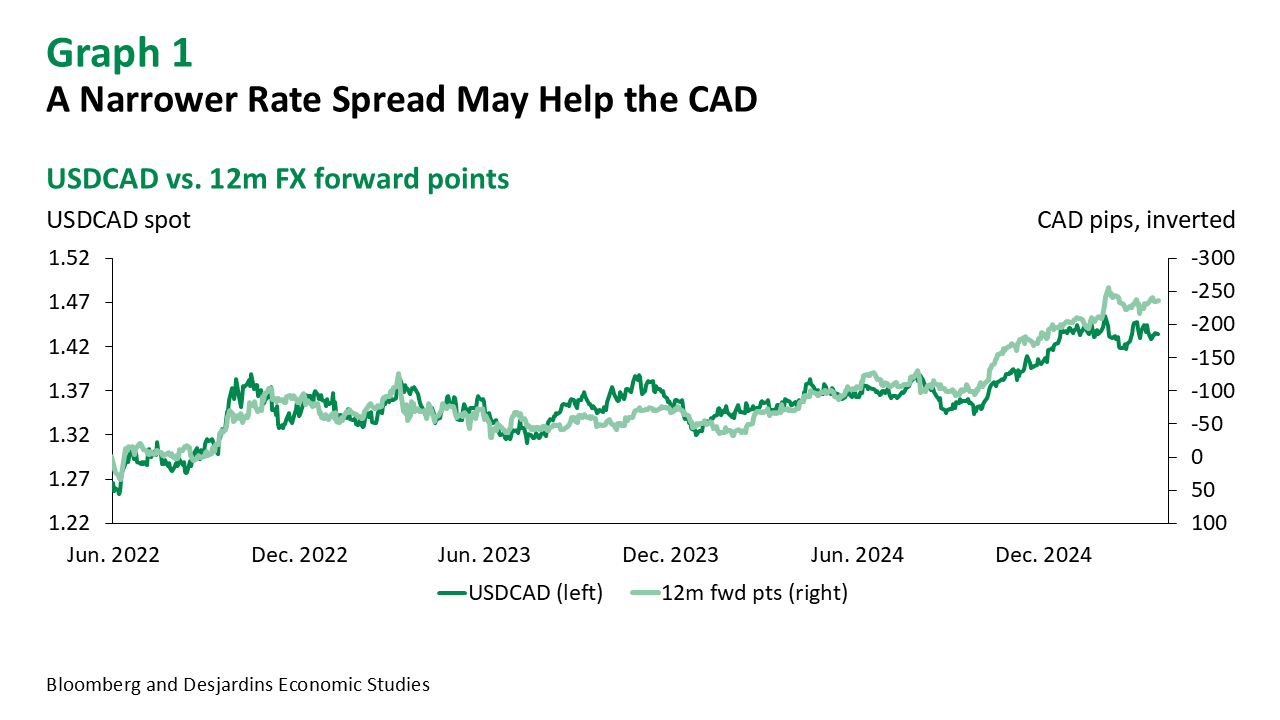

We think there is scope for convergence in US–Canada rate spreads over the next few weeks, which could be due to the differences in the central banks’ mandates. The Bank of Canada is officially only focused on inflation, whereas the Fed has a dual mandate. Of course, the Bank of Canada has also delivered far more monetary easing to date, so the different tactics may well just reflect starting points.

Upgrading Our Forecast for CAD

We are no longer forecasting USDCAD to rise to 1.48 this year. There are three reasons for the change:

- The risk of a US recession has increased. While we forecast a recession in Canada as well, the Bank of Canada frontloaded its cutting cycle and is likely to proceed more cautiously from here. If the US labour market weakens materially, there is scope for the Fed to cut faster than the BoC. But that’s not our base case forecast.

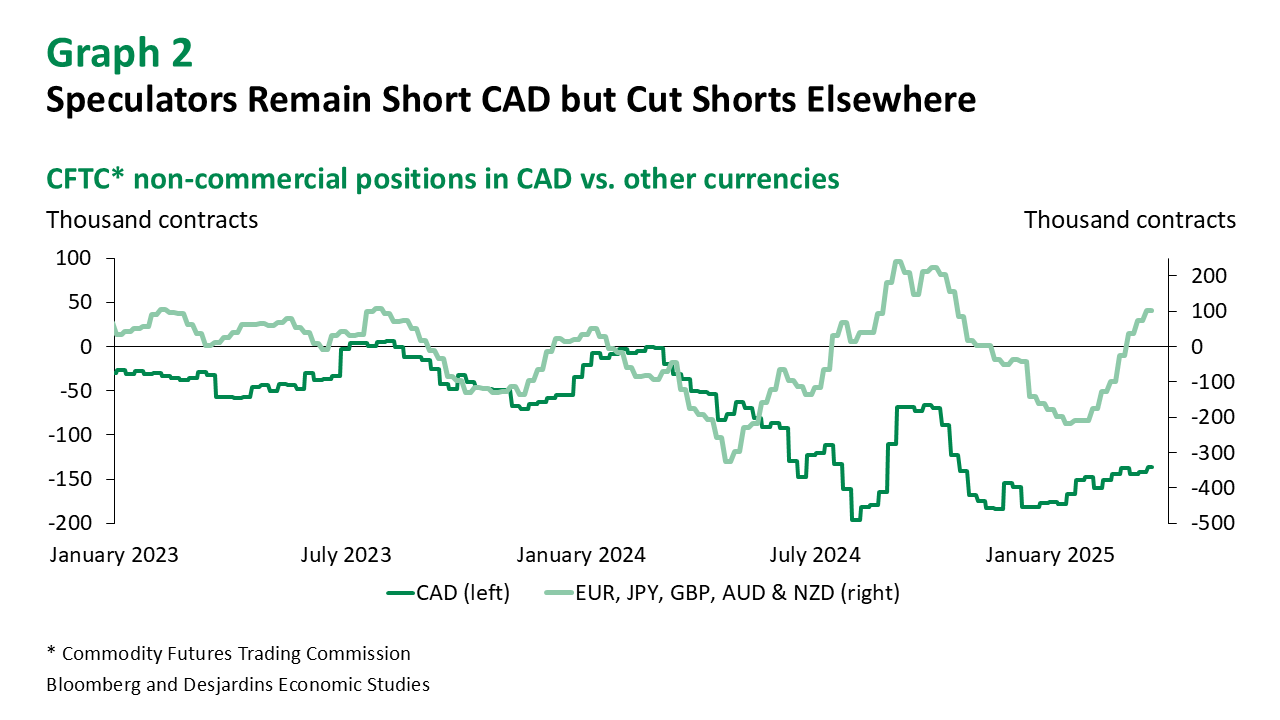

- The CAD has depreciated significantly in trade-weighted terms this year, even though it has been in a range vs. USD. The Bank of Canada’s nominal effective exchange rate has depreciated 5.5% in the last three months, and its real effective exchange rate is at a 10-year low. This relative cheapness of the loonie should help Canadian exporters in their effort to find new markets outside of North America.

- Policy upheaval in the US has weakened the safe haven appeal of the US dollar. The weight External link. of US equities in the MSCI ACWI, the most widely followed benchmark for global equities, was at a record high of 66% in February. Given that the US is less than a third of the global economy, investors seem overallocated to US equities.

- A common belief among asset allocators like Canadian pension funds is that holding the dollar hedges the risk of a market downturn as the dollar is a safe haven currency. However, when stocks fell in July and August last year, and in February and March of this year, the dollar fell too. Context matters. With a made-in-America recession lurking, the US dollar is unlikely to hedge risky assets as it did in the past.

There are still downside risks to the loonie:

- First, the market is factoring in only a short period of tariffs, particularly since the Trump administration has made many U-turns. If the tariff hikes prove more durable or more punitive, CAD may weaken further vs. USD. We are monitoring the reciprocal tariff announcements on April 2, as a significant tariff hike on Canada could cause currency volatility.

- Second, we could be wrong on the US recession call. The post-pandemic recovery in the US has proven incredibly resilient. Weakness in survey data has not translated to hard data yet. In short, the US economy could defy predictions of recession yet again. This prospect looks less likely in Canada given its high trade exposure and the weakening of previous tailwinds like population growth.

Elections: Policy Reset?

Prime Minister Carney has called for elections on April 28 in Canada. His Liberal Party and the Conservatives are tied in opinion polls. We think the Canadian dollar will not be significantly impacted by the election outcome.

Both candidates are aligned on key economic reforms like promoting investment in the mineral sector and reducing internal trade barriers. This is an encouraging sign. Non-residential capex and productivity have lagged in the last decade. If these proposals are implemented effectively, they could boost productivity growth and unlock long-term gains in Canadian assets. Improving investor sentiment could reverse decades of capital outflows from Canadian households and institutional investors. Bringing more of Canada’s vast resources to international markets would also increase demand for the Canadian dollar.

We will review our forecasts when there is more clarity on the next government’s economic agenda.

EUR – All in the Price

Looser EU fiscal rules and Germany’s €1 trillion package for defence and infrastructure spending mark a significant policy shift. Indeed, the speed with which EU Commissioner Ursula von der Leyen and German Chancellor-in-waiting Friedrich Merz made this happen exceeded our expectations.

Investor sentiment towards the European growth outlook has shifted, with a sizable rotation of equity flows from the US to European stocks taking place in March. While the German spending package will be implemented from H2, business sentiment surveys like the ZEW and HCOB PMIs have improved sharply, indicating the long winter in German manufacturing may finally end.

With fiscal policy becoming more expansionary, there is less pressure on the ECB to do the heavy lifting. We now expect the ECB to pause at its April meeting and deliver only two more rate cuts this cycle, down from three previously. The risk now seems to be that the ECB goes on hold after just one final cut at the June meeting.

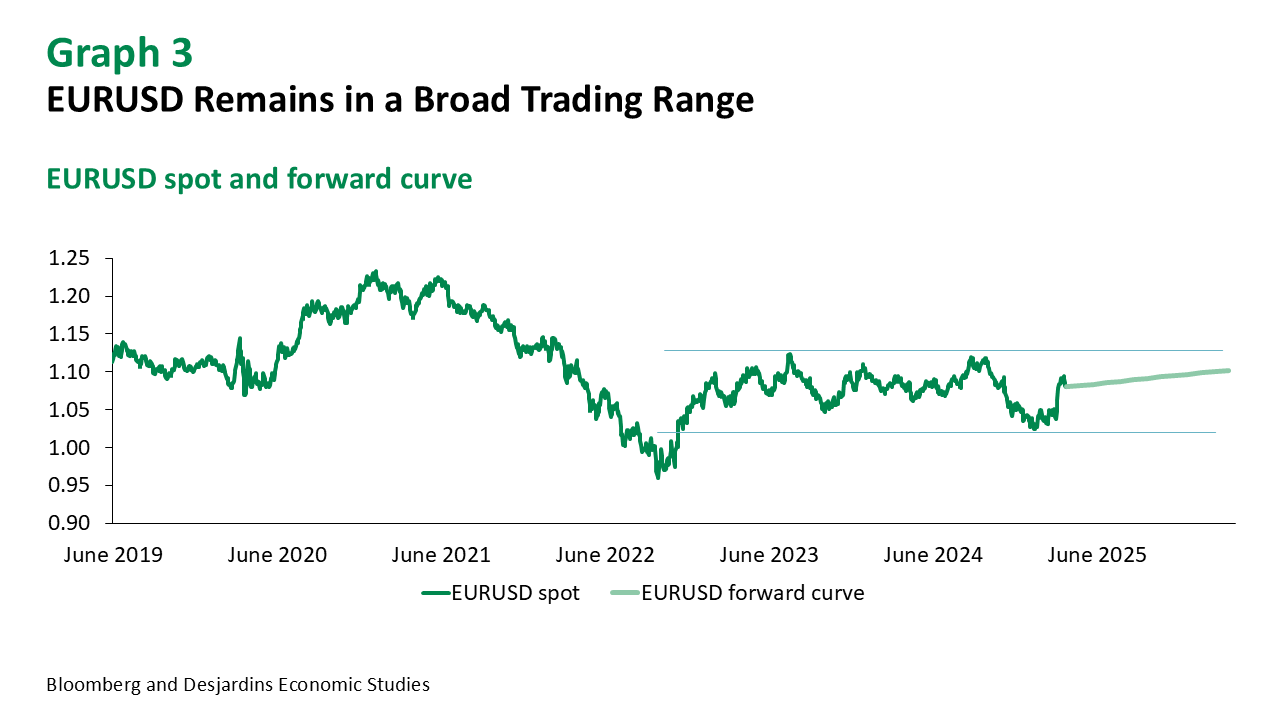

The euro has rallied about 6% over the last month due to these shifts. EURUSD is trading at the high end of the broad 1.02–1.12 trading range of the last two years. We think the fiscal story is well priced now.

The market’s attention will turn to tariff risks looming on April 2. Press leaks citing sources claim the Trump administration is mulling a reciprocal tariff rate of 15%, while others indicate each trade partner will have a different number based on the magnitude of trade grievances. If it’s the latter approach, the eurozone could be slapped with a larger tariff, as the region has a larger trade surplus with the US and more formidable non-tariff barriers. Trading these outcomes is further complicated by the fact that the initial rise in tariffs could be reduced through negotiation.

GBP – Let’s Make a Deal

The pound has largely tracked the broader rally in European currencies. The Bank of England struck a relatively hawkish note last week with an 8–1 decision in favour of holding interest rates at 4.50%.

On the domestic front, the focus will turn to the UK Spring Statement in late March. Chancellor Reeves is set to cut back welfare spending to deliver on promised fiscal consolidation. The negative feedback loop between gilts and the pound has abated recently, but if the budget is more populist than expected, there may be renewed pressure on UK assets.

On the trade front, PM Starmer’s administration decided not to follow Brussels with counter-tariffs for the 25% levy imposed by the US on steel and aluminium. The Trump administration has responded positively to PM Starmer’s proposal for a bilateral trade deal, though negotiations are at an early stage. It is too soon to tell, but if the deal results in better treatment of the UK relative to the eurozone, the GBP could outperform the EUR.

JPY – More in Store for the Yen

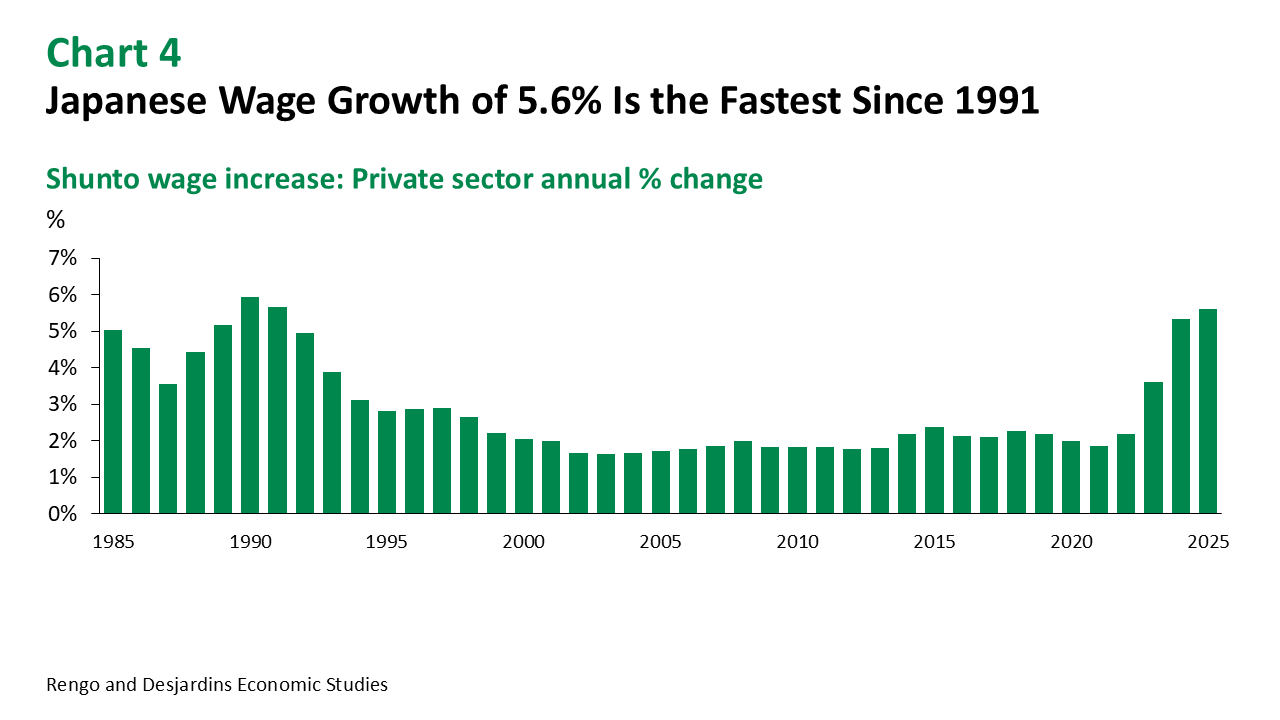

The yen has performed well, and we expect it to extend its gains. The Bank of Japan held rates as expected at its March 18 MPC meeting and signalled it will stick to a gradual pace of rate hikes. We expect it to skip the May meeting, with the next 25bp hike likely coming on June 16. The BoJ will not stop there. In fact, we think it will hike to 1.50% by the middle of next year, compared to market pricing of only 1.00%. Early results from the Shunto spring wage negotiations show an average wage increase of 5.6%, bigger than last year’s 5.3% and the largest since 1991.

On the other hand, the yen carry trade appears to have largely unwound, at least among fast-money participants. CFTC data shows net positioning in JPY futures is now the most bullish since Covid. In addition, the yen’s gains in the recent NASDAQ sell-off were surprisingly muted, which further hints at the JPY carry trade being much smaller than was the case in July and August of last year.

Net-net, while we expect the yen to appreciate over time, it is unlikely to surge in the near term.

CNY – China Keeps a Low Profile

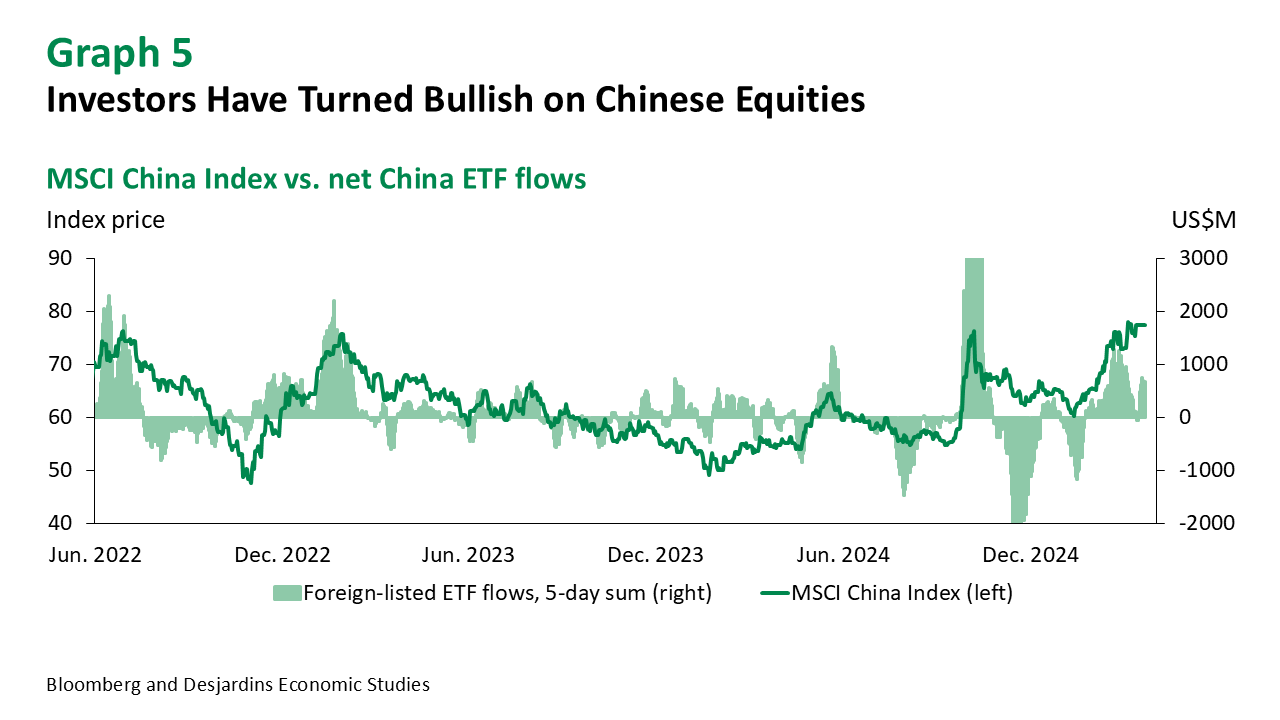

Chinese authorities have tried to fly under the Trump administration’s radar. Chinese government officials have avoided direct criticism of President Trump, and the PBoC has kept the USDCNY fixings stable. Meanwhile portfolio inflows to Chinese equities have underpinned the renminbi. Foreign investors have bought US$18 billion worth of Chinese equity ETFs year to date.

Meanwhile, President Trump implemented a 20% import tariff External link. as punishment for not curbing illegal fentanyl exports to the US and instructed government agencies to prepare to de-list Chinese companies from US exchanges under his America First Investment Policy External link.. But he has kept his powder dry on other issues such as the Phase One trade deal and the forced sale of TikTok.

Despite the relative calm, it is almost inevitable that the US–China rivalry will heat up at some point and impact financial markets. But for now, the mood is calm, investors are chasing Chinese stocks and the renminbi is stable. The ball is in Trump’s court.

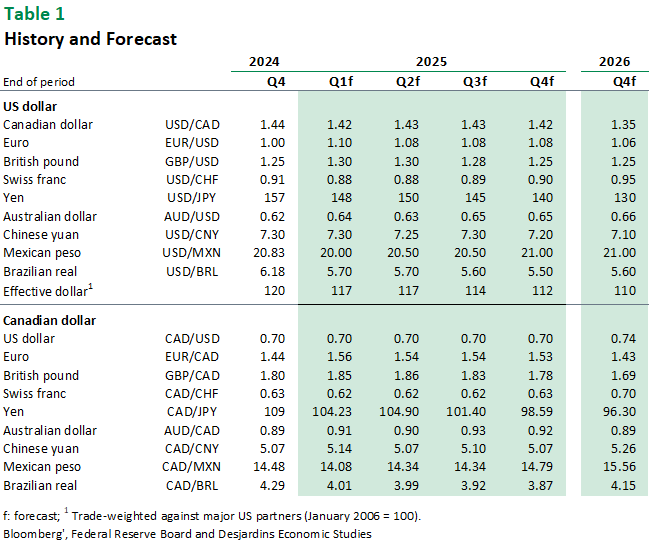

Forecast Table