- Jimmy Jean, Vice-President, Chief Economist and Strategist

Mirza Shaheryar Baig, Foreign Exchange Strategist

FX Analysis

Waiting on Washington

June 12, 2025

Highlights

- We remain bearish on the US dollar in the medium term but expect consolidation to continue next month.

- Carry trades are back in vogue amid falling rates in developed markets, and still-high rates in some emerging markets.

- The ECB has signalled pausing at 2%. Rates are still above neutral in Canada, Australia and the UK, and we expect gradual easing to continue.

- The US labour market is not loosening fast enough to allow the Fed to cut rates this month.

- Section 899 of the US budget bill has spooked global investors and reduced appetite for the greenback. But there’s still a chance it will be watered down in the final reckoning. Watch this space!

Comments

USD to Stay Rangebound

In our last update External link., we noted that the shift in market positioning and mixed US data pointed to a period of consolidation in forex markets. This view remains intact, and we continue to expect broad trading ranges and relatively low volatility to persist in June.

The US dollar index has been roughly flat over the last six weeks. Except for USDCAD, which made a marginal new low, the US dollar has traded in a range versus other developed market currencies.

Looking forward, we expect the Federal Reserve to remain on hold at its June 18 meeting, citing mixed data. The Bank of Japan is likely to stay on hold on June 17, while the Bank of England is set to keep rates steady and keep the door open for cuts on June 19. We will also be watching progress on US trade deals, especially with the eurozone and China. If those deals achieve a meaningful reduction in tariff and non-tariff trade barriers, as we expect, risk sentiment could remain well supported through the summer.

Carry Trades on a Tear

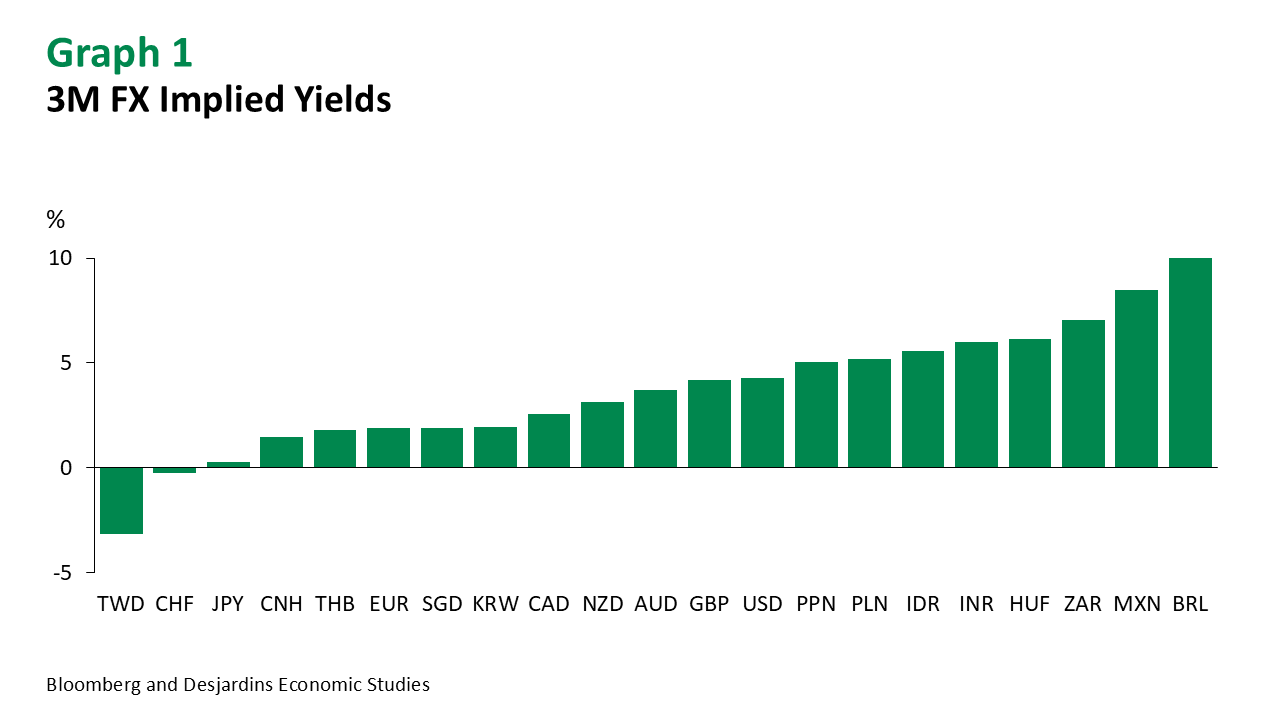

Foreign exchange carry trades have performed well of late, as declining volatility in risky assets and a wider rate differential between currencies have encouraged investors to seek yield. This strategy has been further supported by expectations that central banks in developed markets, including the Bank of Canada and the Federal Reserve will, maintain or cut rates, while some emerging markets continue to offer attractive yields. Graph 1 shows the 3‑month FX implied yields on G7 and liquid EM currencies, ordered from lowest to highest.

We think the Brazilian Real (BRL) screens as the most attractive carry long given the outright carry level, its relative undervaluation and very high real interest rates. The Brazil Central Bank has hiked rates aggressively over the last year and finally seems to be winning the battle against inflation. The Mexican peso (MXN) and the Indian rupee (INR) also offer attractive carry relative to their volatility, though the central banks here are more dovish.

On the funding side, FX implied yields on the Taiwanese dollar (TWD) are negative 3%, as panic-hedging by local life insurance companies created a large dislocation in the non-deliverable forwards (NDF) market. However, Taiwan’s financial regulator has recently eased rules on marking-to-market forex exposures, which we expect will reduce the hedging flow. We would avoid funding out of JPY and CHF due to their high safe haven beta, but CNH and THB could be more appropriate.

Is the US Dollar Carry Trade Back?

Carry trades can also affect the relative demand/supply of the greenback against the loonie. US-dollar-denominated money market funds and deposits are popular with Canadian investors looking for a pick-up yield on cash. The spread between US and Canadian interest rates is relatively wide by historical standards, at around 175bps. This could widen to 200bps if the Bank of Canada cuts rates in July as we expect (the market is pricing in a small chance of a cut).

However, investors have grown wary of piling into the US dollar carry trade for two reasons. First, US inflation expectations have increased, which has lowered the expected real return of holding the greenback. For instance, 1Y inflation expectations in the United States have increased from 2.5% in December to 3.2%, according to the inflation swap market. Second, investors are concerned that the Trump administration could raise taxes on US incomes earned by foreigners, if the “One Big Beautiful Tax Bill” going through Congress is passed in its current form. We turn to this issue next.

Section 899: Another Tariff in Disguise?

A provision in the House-passed fiscal package (H.R. 1) would create a new “Section 899” of the tax code. Dubbed by the media as the “revenge tax,” it would allow the US president to raise income and withholding taxes on foreign investors whose home countries have tax laws that the United States deems discriminatory. In particular, the bill takes aim at the Digital Services Tax (DST) applied by Canada, the UK and the EU, and the global minimum tax adopted by most OECD countries, including Canada. Remittances sent by foreign workers in the United States could be taxed as well.

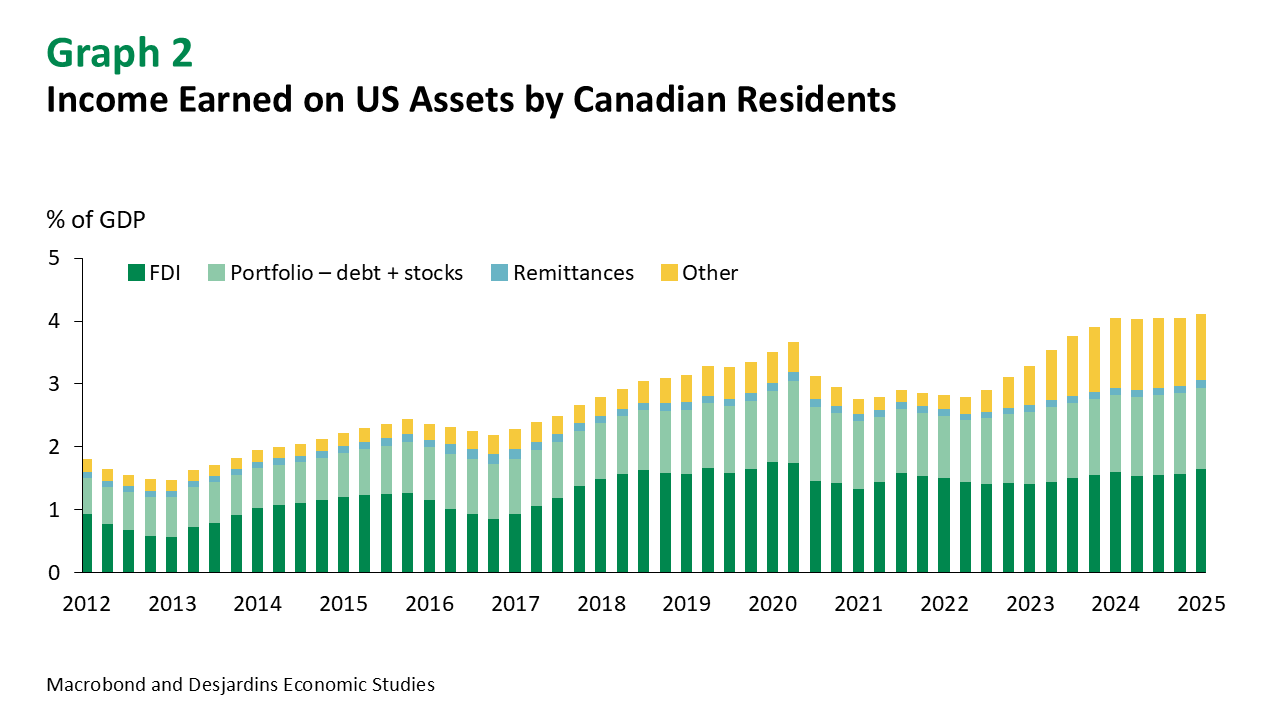

Canadian investors, including corporates, pension funds and households, own about USD4.3 trillion assets in the United States, accounting for 7% of total foreign claims on the United States. Canada is the largest investor in US stocks and 4th largest in US Treasuries. The income earned by Canadians on these assets is substantial: CAD130 billion, or 4% of GDP in 2024. Not surprisingly, the prospect of a tax hike on this income—especially one that is wielded by President Trump—has raised the perceived risks of holding US securities.

More broadly, imposing a punitive tax on your largest creditors may cause them to reconsider future investments. This would harm appetite for US assets and the dollar’s position as the world’s reserve currency. Some fear it could trigger another tit-for-tat response from foreign governments, much like the recent experience with tariffs.

However, there are mitigating factors. First, the bill needs to clear the Senate and may be watered down. Second, interest income is likely to be excluded, thanks to Sections 871 and 897 of the US income tax code. Third, Canada could simply repeal the DST to avoid being labelled a discriminating country. This tax is not a significant source of revenue for the Federal government, as it is projected to earn about CAD1.4 billion per annum, or just 0.2% of federal revenues. Fourth, sophisticated institutional investors could simply restructure their US investments through vehicles that convert dividends into more tax efficient capital gains.

Net-net, we would wait for greater clarity on this issue before factoring it into our foreign exchange forecasts.

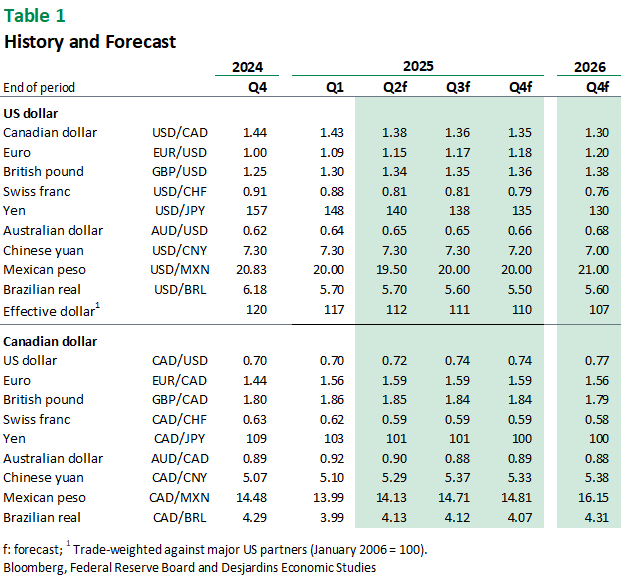

Forecast Table