- Jimmy Jean, Vice-President, Chief Economist and Strategist

Mirza Shaheryar Baig, Foreign Exchange Strategist

FX Analysis

The Greenback Is Due a Rebound

July 17, 2025

Highlights

- President Trump has upped the ante on tariffs and increased pressure on Fed Chair Powell to lower interest rates. But markets are discounting extreme developments.

- The US dollar has suffered one of its steepest declines in history this year. But now it’s testing key support levels, and most traders are short.

- Short-term correlations suggest the greenback may be recovering its safe-haven appeal.

- The loonie continues to lag other G7 currencies. We expect it to closely track rate differentials.

- ECB officials are reluctant to shoulder the bulk of the USD adjustment, particularly since the PBoC is in no mood for burden sharing.

- The BoJ remains cautious on further tightening, and political uncertainty is rising in the lead-up to next week’s elections. The yen could struggle.

- The Mexican government continues to follow a strategy of appeasement with Trump. MXN still looks attractive on carry-to-vol despite Banxico rate cuts.

Comments

Tariffs, Tactics and TACO: The State of Play

President Trump has returned to hardball negotiating tactics, threatening to impose broad-based tariffs on major economies starting August 1 unless new bilateral deals are signed. The likelihood of a coordinated response from the EU, Japan and Canada remains low. Our best guess is that tariffs on key trading partners will eventually settle in the 10%–20% range, allowing global trade to adjust without major disruption, though admittedly this is in line with the consensus view.

Central banks are in wait-and-see mode. Should tariffs exceed market expectations or uncertainty persist beyond August 1, pressure will mount on the ECB, BoE, BoC and RBA to ease policy. But the inflation–growth trade-off will be challenging for the BoJ, which has now missed its inflation target for 38 consecutive months.

As for the Fed, Chair Powell has indicated rates will remain on hold at least until the September 17 meeting, pending clarity on the inflationary impact of tariffs. However, President Trump continues to push for lower rates and has openly pressured Powell to resign, adding a layer of political risk to the Fed’s policy outlook.

The most critical point is this: US stock indices have recovered to all-time highs while bond yields have stabilized, even in the face of the deficit-expanding One Big Beautiful Bill. This raises a key question: are markets placing too much confidence in the TACO trade—the assumption that Trump will ultimately tone down the rhetoric before it inflicts real damage?

The irony is hard to ignore: stable financial markets may be encouraging Trump to up the ante. Investor complacency may have created a potentially precarious moment.

What does all this mean for forex markets? We believe the US dollar is poised to rebound over the next few months. Investor positioning has shifted so dramatically in recent months that the pain trade is a stronger greenback in the near term. However, we expect any rebound to be temporary.

US Dollar: Safety Concerns

At the time of writing, the broad trade-weighted dollar index is down about 10% year to date—its second-worst performance over a 12‑month period since 1971. Few would have expected this in January, when the dollar index hit a 40‑year high!

The shift in sentiment was triggered by concerns that the dramatic increase in tariffs on “Liberation Day” would send the US economy into a tailspin. Moreover, the US dollar stopped behaving as a safe haven, which convinced foreign asset managers to increase forex hedges External link. on US assets.

However, USD selling pressure appears to be waning. Specifically:

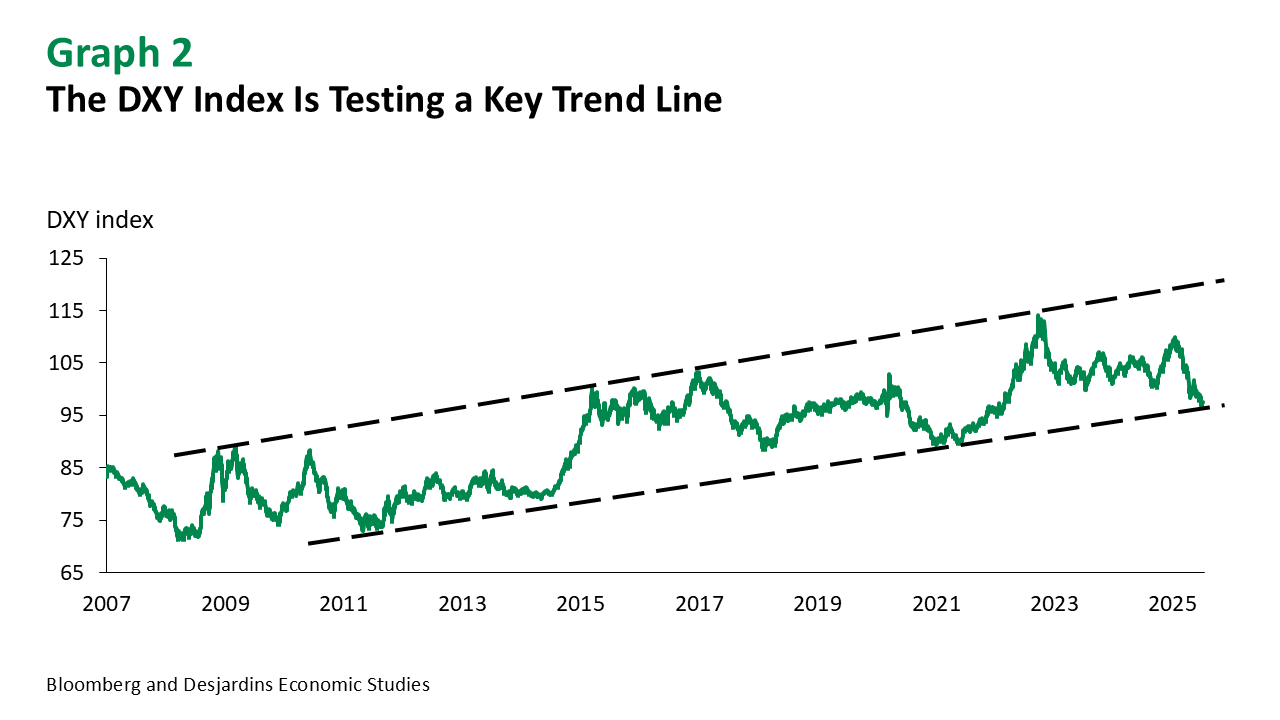

1. The trendline is holding: The US dollar has been trending higher since 2011 and is now testing some key support levels. Graph 2 shows the DXY index, a basket of USD/G7 currency pairs. There are formidable psychological levels at play, such as 1.35 for USDCAD, 1.19 for EURUSD and 140 for USDJPY.

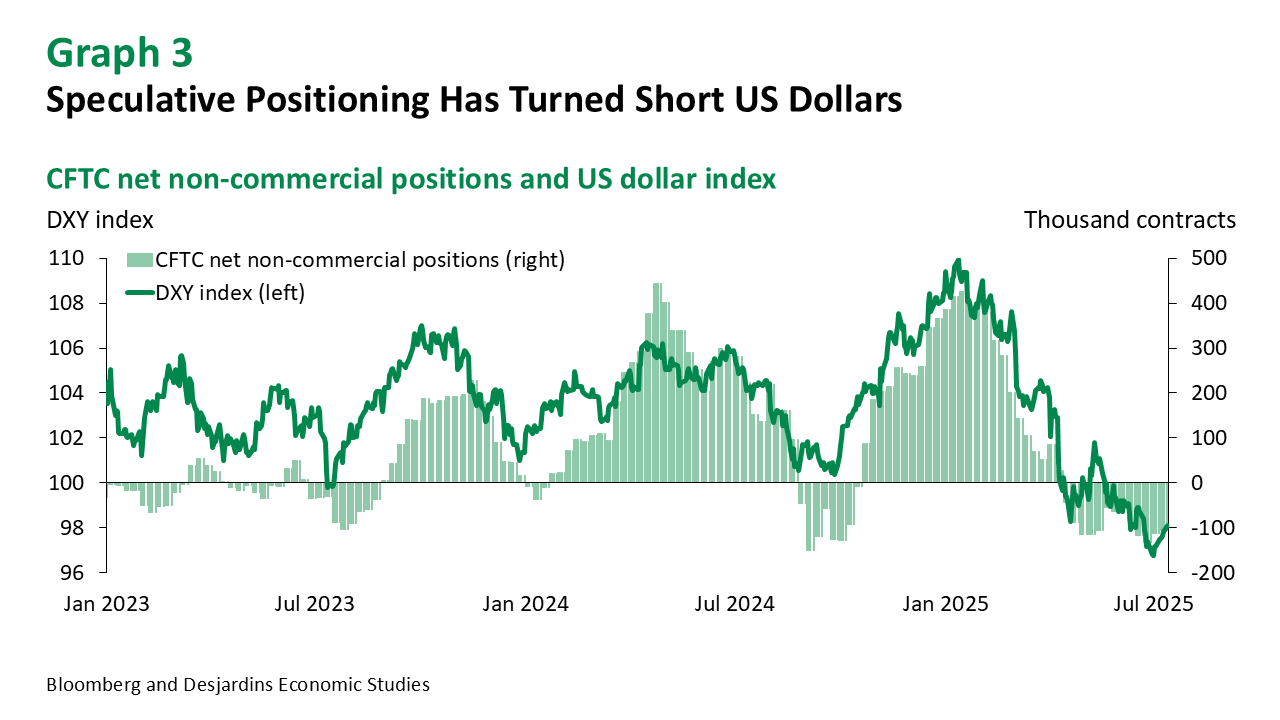

2. Positioning has turned: According to data from the Commodity Futures Trading Commission (CFTC), which tracks the futures positioning of trend-following Commodity Trading Advisors (CTAs) and other asset managers, net positioning in USD has turned short USD. While this isn’t as large as the long positioning in January, it’s still substantial, suggesting the pain trade would be a USD rally.

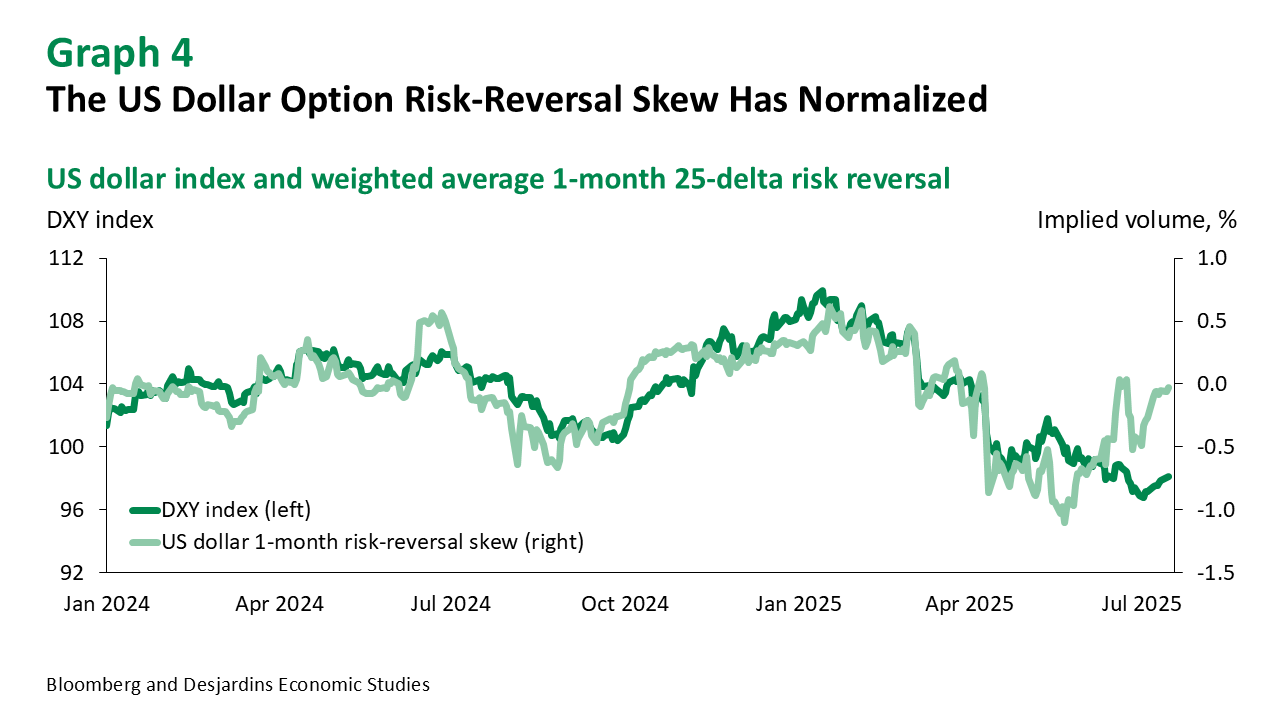

3. Hedging pressure has abated: As asset managers sold US dollars to raise hedge ratios, it caused cross-currency basis swap spreads to widen and dramatically shifted the skew in FX option volatility surfaces towards USD puts. But these distortions have now normalized in most currencies, suggesting the panic is over. Graph 4 shows the DXY index against the weighted average 1‑month 25‑delta risk reversal skew of the basket components.

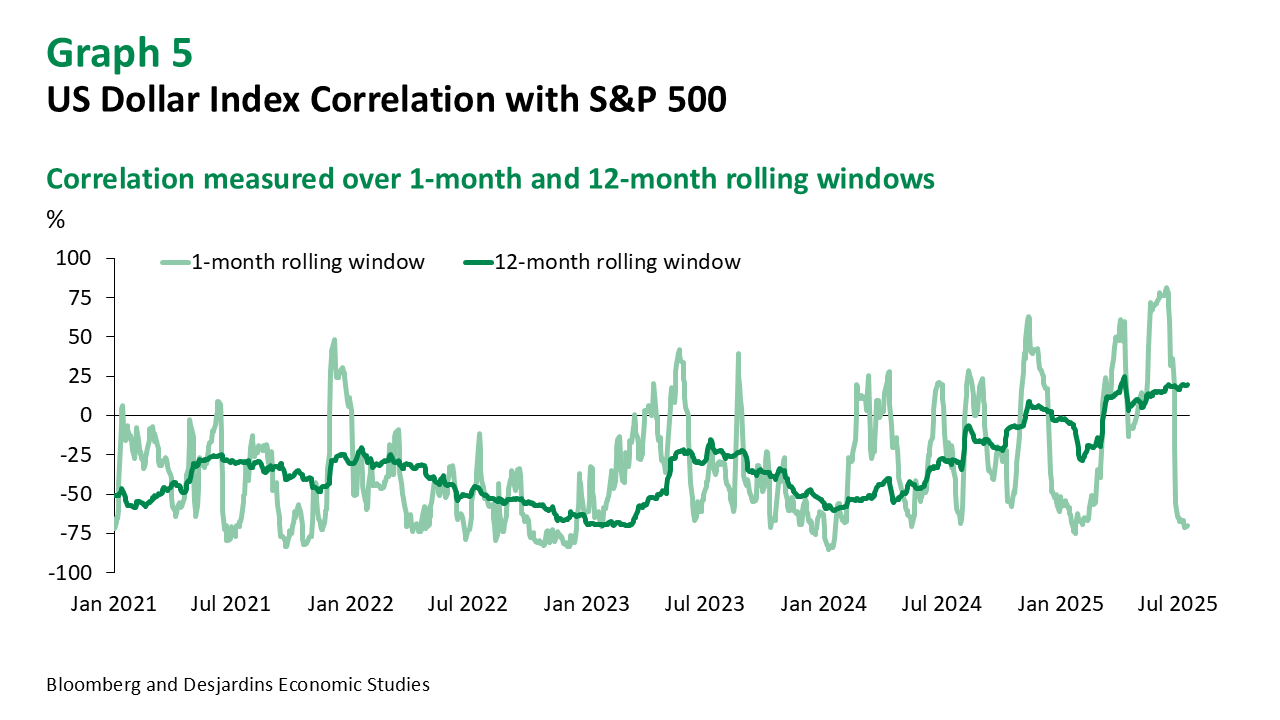

4. Safe-haven correlations are turning: As we have shown, foreign asset managers, including Canadian pension funds, have traditionally leaned on the US dollar’s safe haven status. Their risk models were wrong-footed when the greenback stopped behaving as a safe haven post “Liberation Day.” But now, short-term correlations suggest the USD may be recovering its safe-haven status (graph 5). To be sure, short-term correlations can be noisy. But if this recent shift persists, risk models and market commentators will be forced to reverse course.

CAD

Back to Differentials

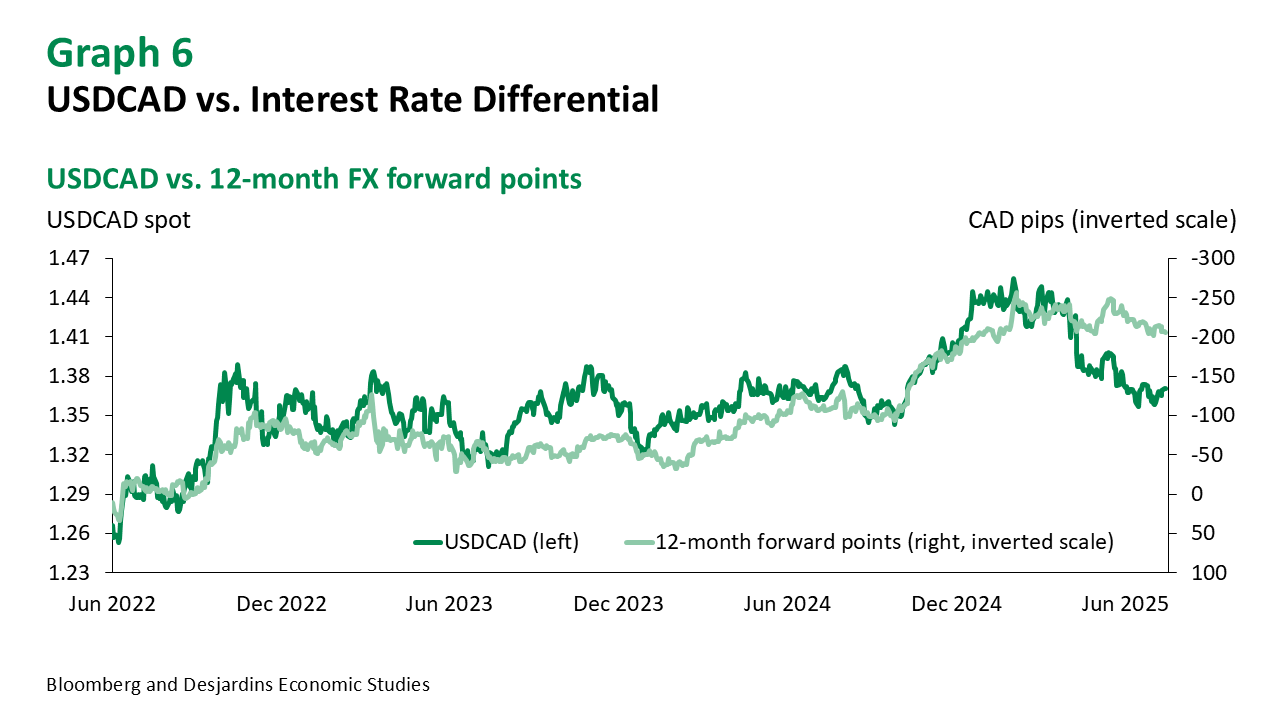

The Canadian dollar has underperformed compared to other G10 currencies, hitting post-Covid lows against the euro and Swiss franc and weakening against the Mexican peso. The year-to-date move down in USDCAD is largely a US dollar move.

As discussed above, forex hedging flow from Canadian asset managers was a key source of USDCAD selling. However, net flows and skew in the option market have become balanced of late, suggesting the hedging flow has moderated.

We expect a balanced two-way market in USDCAD over the next few months, with the focus shifting back to economic fundamentals and relative interest rates. Our rates strategists believe there is scope for the BoC to cut rates more than market expectations, which could weigh on the loonie.

We expect USDCAD to stay in a core trading range of 1.36–1.38 over the next few months, but it could bounce as high as 1.40, though we expect this would be temporary. We’re maintaining our 2025 and 2026 year-end forecasts of 1.35 and 1.30 respectively.

EUR

It’s Getting Hot in Here

The Sintra conference yielded valuable insights about how ECB officials are balancing the euro’s long-term potential with the macroeconomic risks posed by its recent rapid appreciation.

ECB President Lagarde spoke optimistically about the euro playing a larger international role, while other officials including Vice‑President de Guindos expressed concerns that the euro’s appreciation could harm exporters and depress inflation below target.

The ECB’s primary concern lies in the speed and lack of breadth of the euro’s appreciation. The euro has absorbed much of the dollar’s decline, rising 13% year to date—outpacing gains in the pound (7%), yen (7%), loonie (5%) and renminbi (under 2%). Given the sharp rise in the euro’s trade-weighted exchange rate, these concerns appear well-founded, and markets have taken notice.

From a technical perspective, we think EURUSD could pull back to test 50‑day moving average support around 1.14 and consolidate around there for a while. We expect the ECB to tolerate a gradual rise in the single currency. Thus, we’re maintaining our 2025 year-end forecast of 1.18 and 2026 year-end forecast of 1.20.

JPY

BoJ in a Quandary

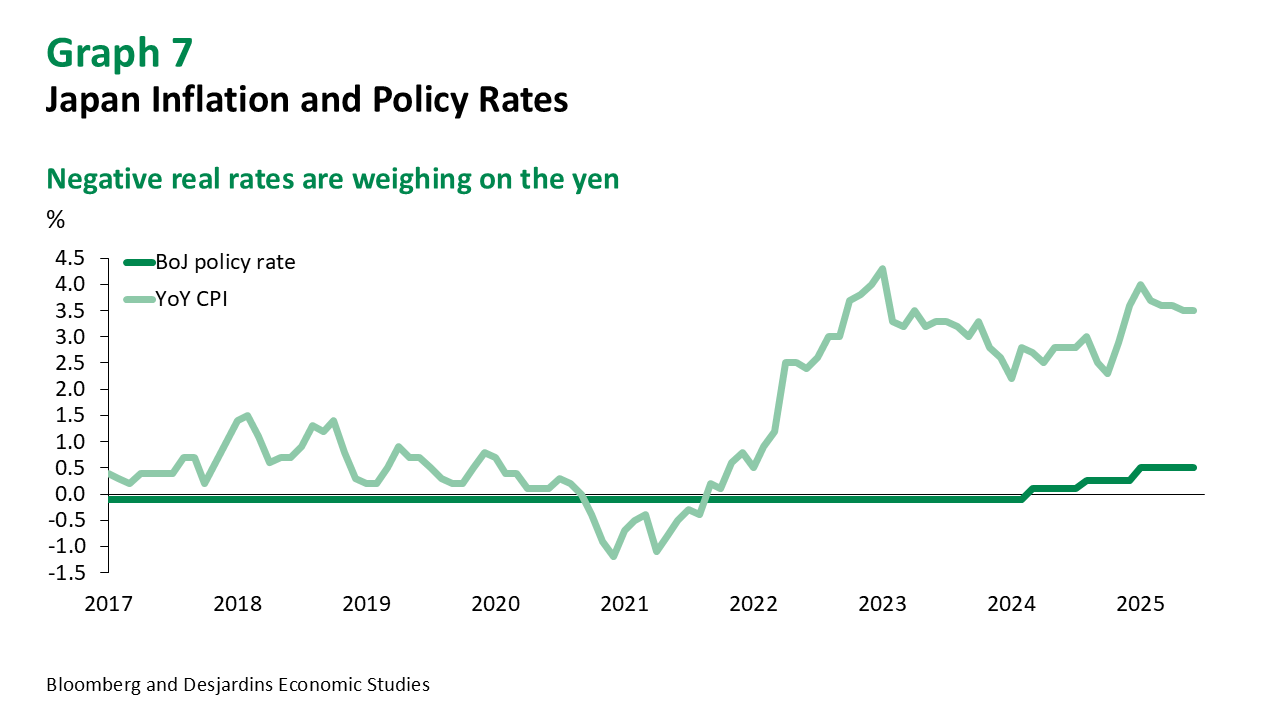

The BoJ meets on July 31. It’s widely expected to hold rates steady and reaffirm downside risks to the economy from continuing tariff-related uncertainty. While this caution is warranted, the simple fact is that the BoJ’s inflation target is 2% and CPI has been above target for 38 consecutive months.

High inflation and negative real rates have benefited Japan’s debt dynamics, but rising term premia mark the end of easy financing. Japanese government bond (JGB) yields hitting multi-decade highs signals this regime shift.

Inflation has become politically toxic in Japan, emerging as the top voter concern ahead of the July 20 upper house election. With approval ratings sliding and the Liberal Democratic Party at risk of losing its majority, Prime Minister Ishiba—already leading a minority government—could face mounting pressure to resign. Meanwhile, the threat of a 35% US import tariff looms, surpassing even the 24% imposed on “Liberation Day.”

Put simply, political and policy uncertainty is rising in Japan, making our bullish forecast for the JPY untenable. We are thus raising our USDJPY forecast for year-end 2025 from 135 to 145, and for end 2026 from 130 to 140.

CNY

Need for Speed

The People’s Bank of China’s (PBoC) daily USDCNY fixes and official statements show that the central bank prefers to manage USDCNY tightly. This is why CNY has significantly lagged G7 currencies as well as most emerging market currencies.

Chinese authorities earned praise for resisting CNY devaluation despite US tariffs reaching 145%, avoiding a potential wave of competitive devaluations across Asia. However, that same currency stability is now drawing criticism—particularly from the EU—as EURCNY hits 11‑year highs, giving Chinese exporters a perceived unfair edge.

Meanwhile, as measured by the GDP deflator, China is in deflation for the ninth consecutive quarter. From a purely monetary standpoint, a weaker currency would be preferable.

So should the PBoC allow the yuan to strengthen to deflect dumping accusations and avoid future tariffs? Or should it maintain a weaker currency to counter deflation? It’s a tough call—perhaps why China appears content to muddle through with the status quo.

We continue to anticipate a gradual appreciation of the CNY and expect USDCNY to fall to 7.10 by the end of 2025 and 7.00 by the end of 2026.

MXN

The Pivot to the US Has Lowered Risks to the Peso

President Sheinbaum’s government has broadly followed a policy of appeasing President Trump in order to preserve the country’s strong economic ties with the US. Migrant apprehensions at the US–Mexico border are down 93% year over year, and according to the Mexican government, about 83% of Mexico’s exports in May were USMCA-compliant, up from 50% in March.

Mexico’s pivot toward the US is also clear from its shift away from China. Imports from China are declining, and the government is scrutinizing high-profile Chinese investments. For instance, BYD—China’s top EV maker—recently scrapped plans for a factory in Mexico. These shifts likely strengthen Mexico’s position ahead of USMCA renegotiations expected to begin in late September.

The Bank of Mexico’s rate cuts have narrowed the Mexico–US policy rate spread to 350bps—down from 700bps last year and below the 400bps long-term average. Yet with currency volatility also declining, the MXN still offers an attractive carry-to-vol ratio.

We expect USDMXN will continue to grind lower to 18.0 by the end of 2025 and remain stable at around that level in 2026.

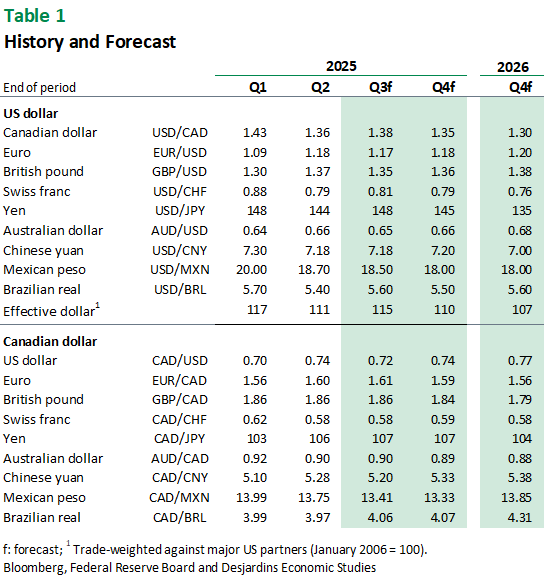

Forecast Table