- Jimmy Jean • Randall Bartlett • Benoit P. Durocher • Royce Mendes • Mirza Shaheryar Baig • Marc-Antoine Dumont

Tiago Figueiredo • Francis Généreux • Sonny Scarfone • Oskar Stone • Hendrix Vachon • LJ Valencia

Economic and Financial Outlook

The US government shutdown adds to the many sources of concern

October 23, 2025

Highlights

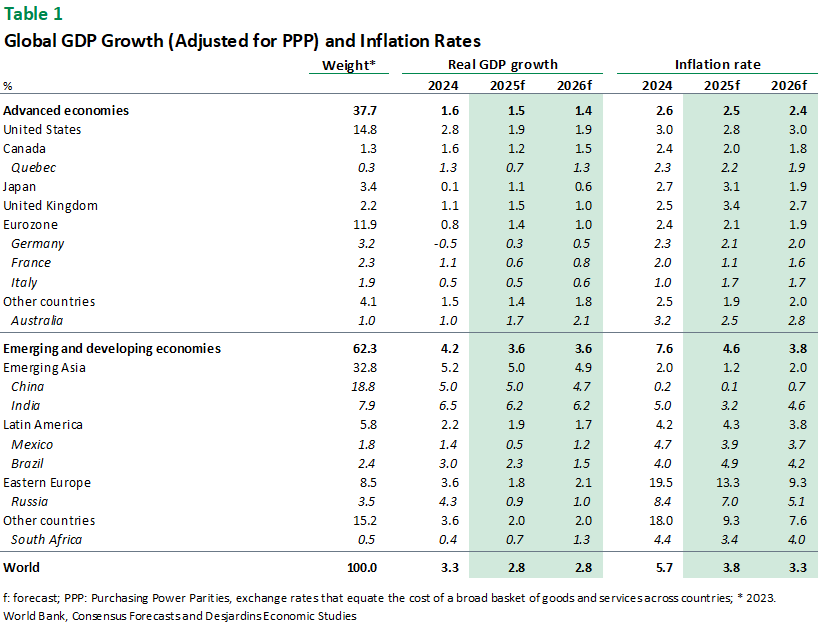

- The global economy is still showing resilience, but that resilience is being put to the test. The United States has threatened further protectionist measures, primarily against China, and new tariffs on US heavy‑duty vehicle imports are expected to take effect on November 1. That said, economic growth seems to be holding steady in Europe, and PMI indexes have been fairly solid lately. China’s exports contributed to growth in the third quarter, but this was offset by a renewed slowdown in domestic demand. All things considered, we expect global real GDP to rise by 2.8% in 2025 and in 2026.

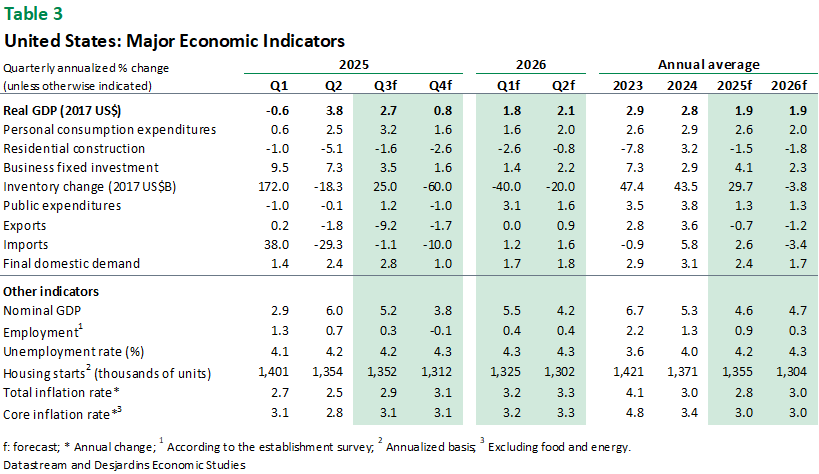

- The US government shutdown that began on October 1 has delayed the release of key economic indicators. Without these numbers, it’s hard to get a clear picture of the labour market, household consumption, business investment and international trade. The most recent data did suggest, however, that real GDP made solid annualized gains of nearly 3% in the third quarter. The economic impact of the government shutdown will largely be determined by how long it lasts, but there’s still a chance that the economy could recover much of the ground lost by the end of the year. That said, real GDP growth is expected to be weaker in the fourth quarter.

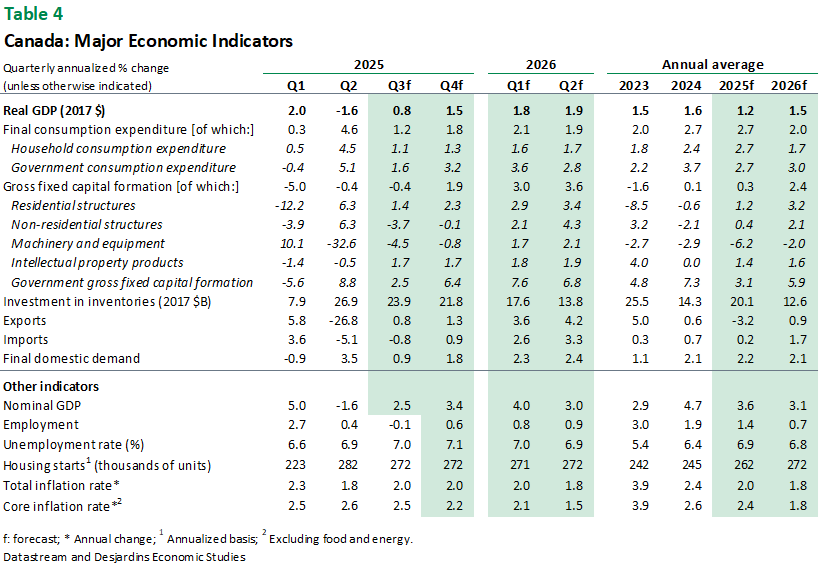

- For Canada, our baseline outlook for real GDP has been revised up again, as recent data point to stronger near‑term growth. We expect domestic demand to remain firm with robust consumer spending, partly thanks to the labour market holding up better than expected. Government spending should provide an added boost in quarters ahead, with the federal government announcing ambitious defense and infrastructure spending plans, likely more than offsetting anticipated cuts to the operating expenses. Trade activity will likely remain soft despite rapid CUSMA compliance and the removal of some retaliatory tariffs by the Government of Canada. The latter should however help inflation to trend below the Bank of Canada’s 2% target, creating room for further rate cuts. Slowly recovering trade next year should also help business investment recuperate modestly, although the outcome of the CUSMA review is an important wildcard.

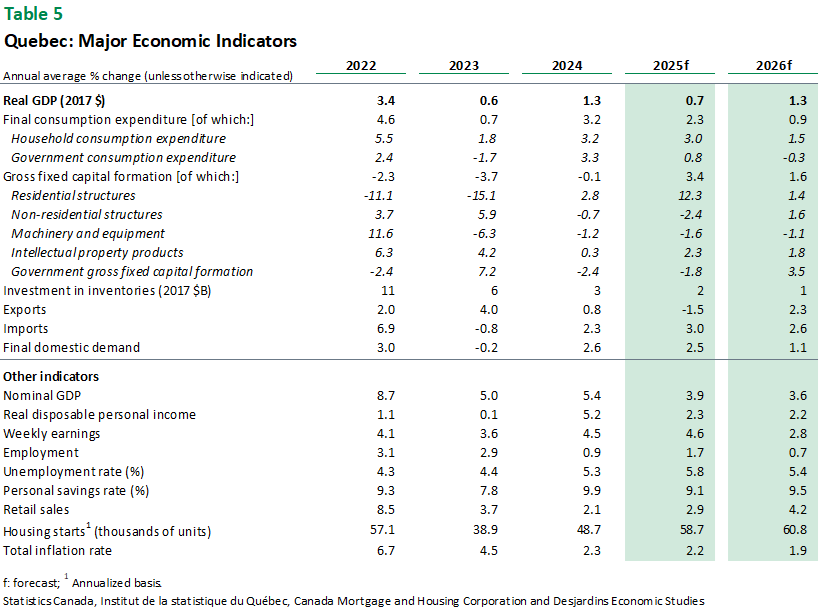

- For Quebec, resilient domestic demand in Q2 could give way to more limited gains over the rest of the year—high‑frequency data suggest that household contributions may have hit a ceiling, albeit a relatively high one. The overall outlook remains largely unchanged from last month, as the most recent data confirms that the housing market, government spending and non-residential investment have all evolved as expected. Exports, however, may not have performed quite as well as anticipated. While the data we have is partial, given the ongoing US government shutdown, it does appear that Quebec’s exports south of the border have recovered more slowly than initially hoped. As a result, our forecasts for international export growth have been slightly downgraded for the rest of 2025. This revision is further justified by the recent sector-specific tariffs on furniture manufacturers, trucks, buses and lumber. We now expect real GDP growth of 0.7% for 2025, down from 0.8%. Our forecast for 2026 remains unchanged at 1.3%. External link.as the most recent data confirms that the housing market, government spending and non‑residential investment have all evolved as expected. Exports, however, may not have performed quite as well as anticipated. While the data we have is partial, given the ongoing US government shutdown, it does appear that Quebec’s exports south of the border have recovered more slowly than initially hoped. As a result, our forecasts for international export growth have been slightly downgraded for the rest of 2025. This revision is further justified by the recent sector‑specific tariffs on furniture manufacturers, trucks, buses and lumber. We now expect real GDP growth of 0.7% for 2025, down from 0.8%. Our forecast for 2026 remains unchanged at 1.3%.

Risks Inherent in Our Scenarios

Global uncertainty should remain high, given the existing tariffs and the threat of other sector‑specific measures. Economic growth could also be affected by other policies implemented in the United States, particularly those on immigration and the federal government apparatus. It’s also not clear the extent to which central banks will be willing to cut rates if tariffs and supply chain disruptions cause inflation to climb and growth to slow. Geopolitical tensions could further contribute to inflation by pushing the price of some commodities up, including oil. We’ll also need to keep a close eye on the threats to the independence and neutrality of key economic institutions in the United States. The longer the political deadlock continues, as Congress and the White House argue over federal funding, the greater its consequences may be for economic activity. The state of US public finances may prompt some global investors to further reduce their exposure to the United States. But the rest of the world, including Europe, is facing its own political and budgetary challenges. In the longer term, geopolitical fragmentation and budget pressures could make it harder for governments to respond effectively to economic slowdowns without straining their public finances or seeing their credit rating lowered. And there are risks of financial instability, especially if regulatory frameworks become more relaxed. Bankruptcies in the automotive sector have weakened some US regional banks and revived concerns about private credit quality and the risk of contagion. Further volatility in stock, bond, currency and commodity prices could damage confidence and weaken the outlook for the global economy.

Financial Forecast

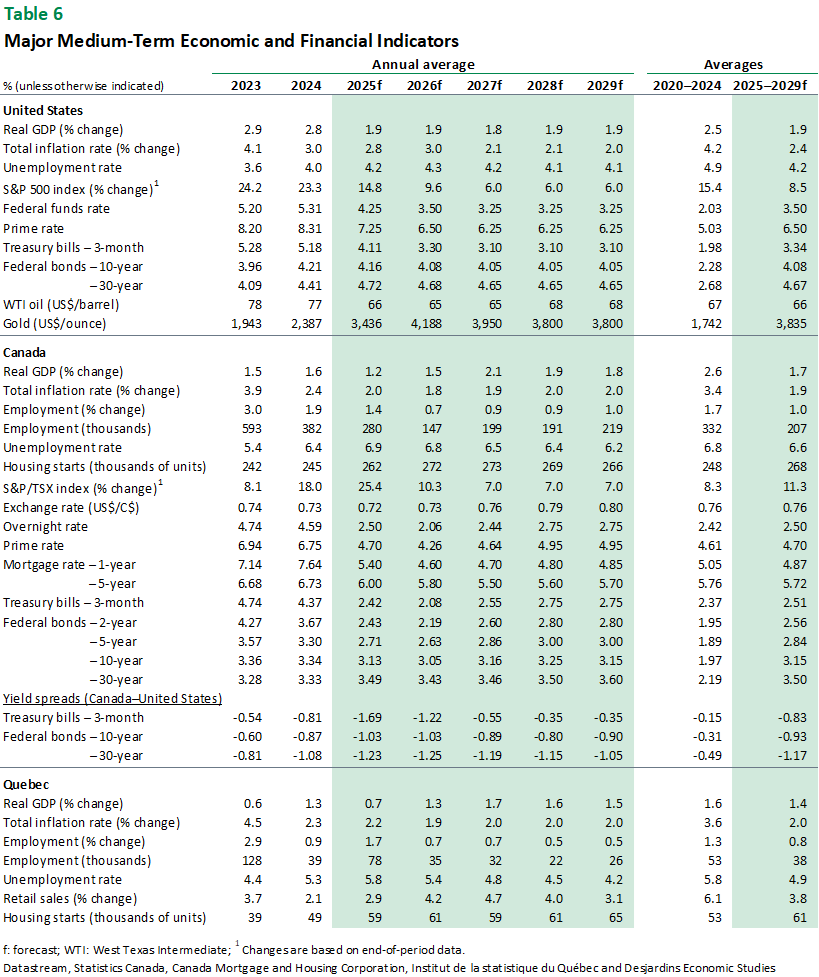

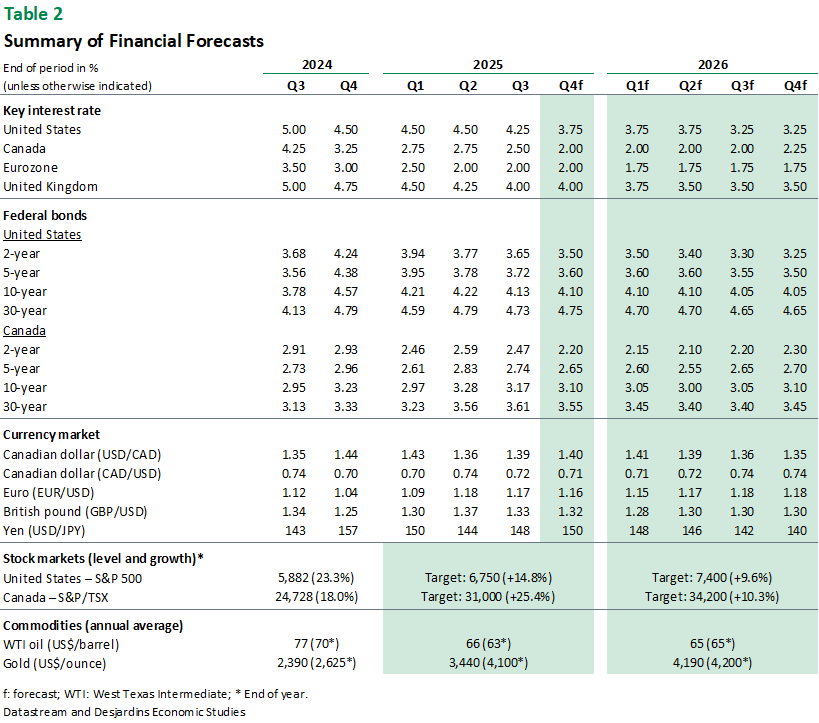

North American central banks have resumed their easing cycles in response to ongoing economic weakness and the limited inflationary impact of tariffs thus far. In Canada, policymakers are expected to continue easing through year‑end, with rates likely bottoming at 2.00%. In the U.S., the outlook is less certain. While we still anticipate two more 25‑basis‑point rate cuts this year, inflation concerns may prompt a pause in the first half of next year. Yields are expected to decline further, with yield curves steepening into year‑end—particularly in Canada.

Equity market volatility has increased following a period of unusual calm. Investor sentiment is being weighed down by rising US‑China tensions, questions around the Fed’s independence, fiscal sustainability, and US capital expenditure trends. While equities may continue to drift higher, we’ve revised our year‑end target for the S&P 500 to reflect these headwinds and account for the growing downside risks. In Canada, equity performance is also expected to cool off, as we anticipate some consolidation in gold prices heading into year‑end.

The Canadian dollar has depreciated to 1.40 against the US dollar. Our previous year‑end forecast of 1.35 now appears increasingly unlikely. Pension fund hedging flows have abated and the exchange rate has re‑established its link with rate differentials, which may continue to drift against the loonie. We have changed our forecasts and now expect the loonie to remain soft in the next two quarters and then gradually strengthen towards the end of next year.

Forecast Tables