- Jimmy Jean • Randall Bartlett • Benoit P. Durocher • Royce Mendes • Mirza Shaheryar Baig • Marc-Antoine Dumont

Tiago Figueiredo • Francis Généreux • Sonny Scarfone • Oskar Stone • Hendrix Vachon • LJ Valencia

Economic and Financial Outlook

Tariff De-Escalation Leads to a Slight Improvement in the Economic Outlook

May 22, 2025

Highlights

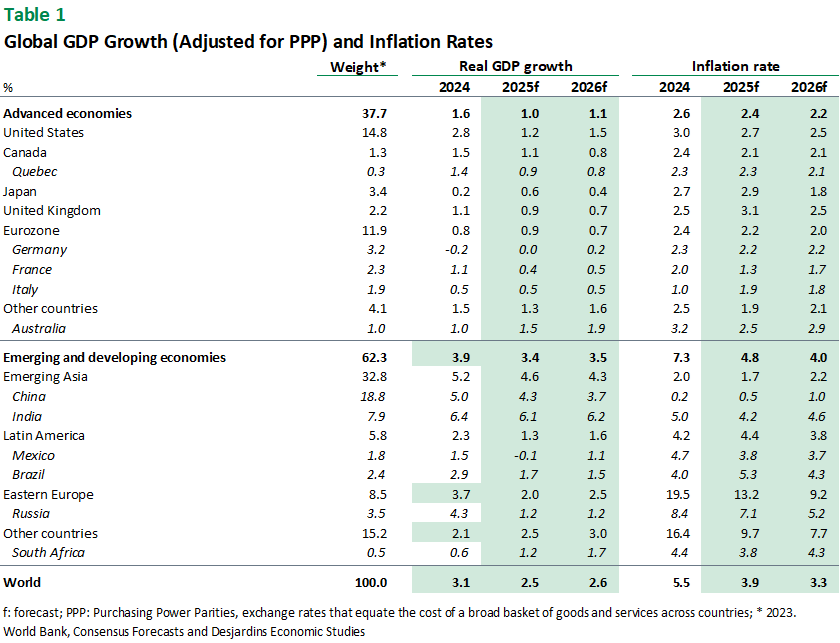

- US trade policy shifts are, once again, behind the biggest changes to our economic scenarios. This time, it’s because the United States and China have reached a deal to roll back the steepest of their previously announced tariffs. This climbdown in the trade war should help the world’s two largest economies avoid a worst-case scenario and will benefit the global economy as well. We assume that US tariffs on Chinese goods will stay at 30% when the 90‑day pause is up, and that tariffs on Mexican and Canadian goods will remain at 25% until the end of the year, with the current exemptions maintained. We also assume that the variable reciprocal tariffs for the rest of the world will be abandoned indefinitely, although the current 10% rate should stay in place. That being said, the situation is still fluid, and our economic and financial scenarios will be updated as the trade war evolves.

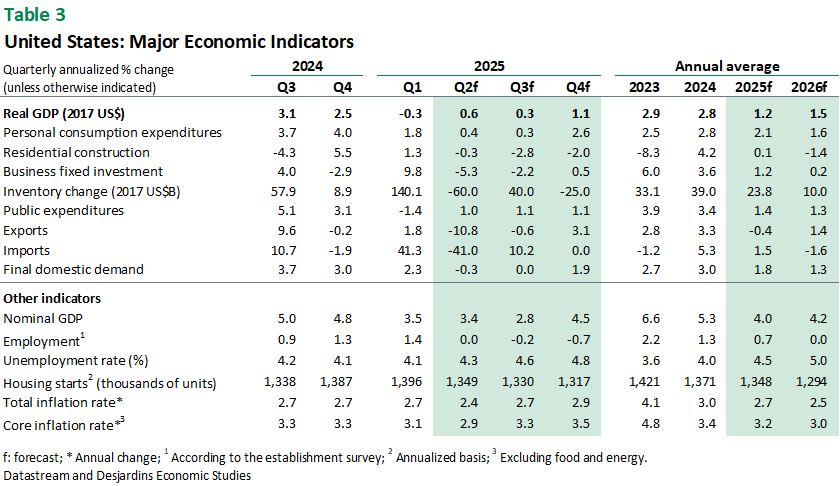

- This temporary truce with China is obviously good news for the United States. While US real GDP slipped an annualized 0.3% in the first quarter, there’s now a real chance that the country will manage to stay out of recession. The situation remains fragile, though, and some of the damage has clearly already been done. We expect May’s indicators to reflect the drop in trade and economic growth should remain weak, given the slide in consumer confidence, lower business activity indicators and spiking uncertainty. For now, the labour market remains resilient, but we expect it to weaken in the months ahead. The tariff-driven surge in inflation we expect should materialize sooner or later, but it will be somewhat mitigated by the recent US–China trade deal.

- We’ve raised our forecasts for China, since our previous projections assumed higher US tariffs. But “lower trade tensions” aren’t the same as “zero trade tensions.” And US tariffs on China and the rest of the world remain much, much higher than they were at the start of the year, which will continue to affect global economic growth. The major European economies performed slightly better than expected in the first quarter of 2025, but lower growth is expected from now on.

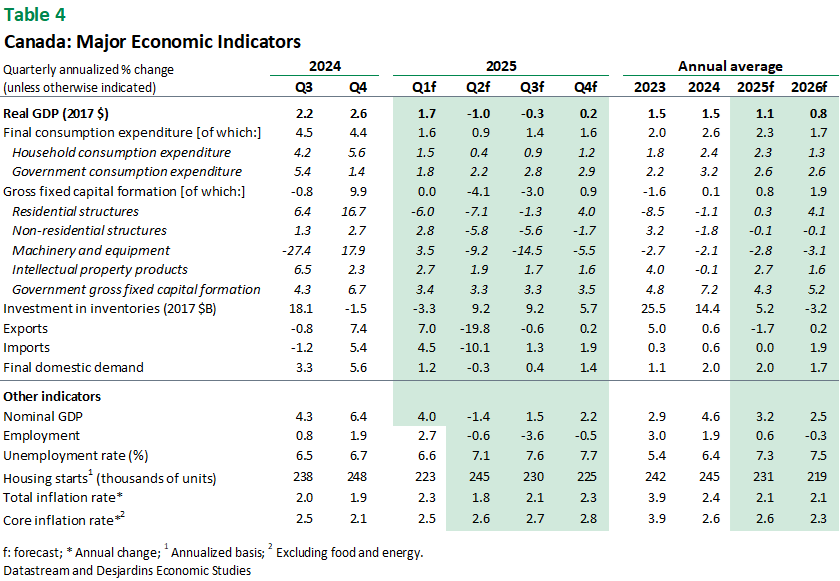

- As they apply to Canada, US tariffs have remained unchanged since “Liberation Day.” We continue to expect rapid progress towards full CUSMA compliance in the near-term. Modestly higher US growth than previously expected should provide added demand for Canadian exports. As a result, we’ve reduced our expectations for the drag on the Canadian economy relative to our April forecast, albeit with still-slow growth for most of 2025. Domestically, we expect expansionary fiscal policy to provide added support to the Canadian economy moving forward. Lower oil prices persist as a drag on growth. However, the elimination of the federal price of pollution, in tandem with falling energy prices and slower growth, will help keep a lid on inflation. This is especially notable given the upward pressure on prices coming from Canadian counter-tariffs. Indeed, our estimates suggest that inflation over the next year could average slightly below the Bank of Canada’s 2% target—something almost unimaginable until just recently.

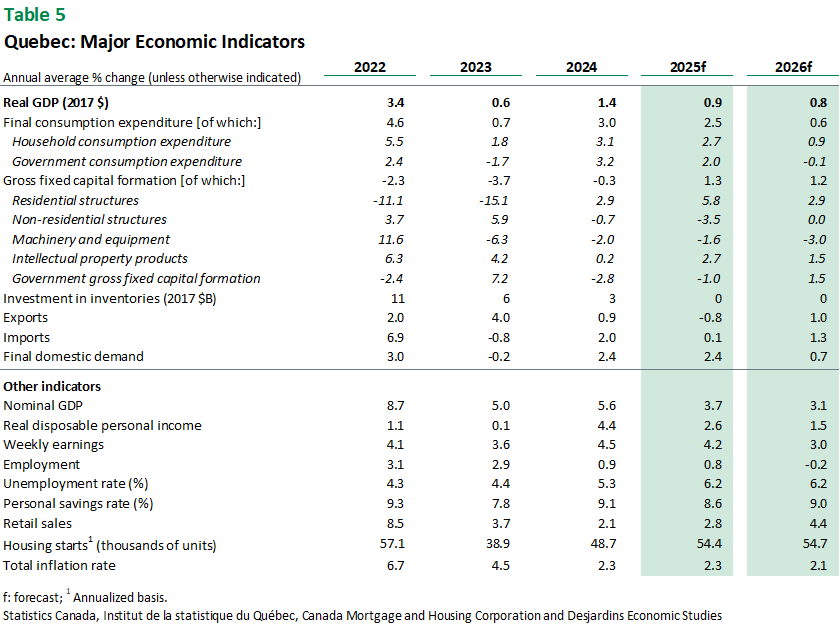

- Quebec’s economic outlooks are slightly better, as tensions have eased somewhat with the United States and other trade partners. As with Canada, our short-term forecasts have been revised upward. All the same, unless the United States and Canada reach an agreement in the coming weeks, our scenario calls for slight real GDP contraction during the second and third quarters of 2025. The labour market still appears to be stalling, with hours worked trending lower and wage growth continuing to slow. The bump in April’s net employment is largely due to the workers temporarily hired for the federal election held April 28. The general slowdown in employment is weighing on consumer confidence. Business optimism also remains fragile, and investment projects may stay on hold given the high levels of uncertainty.

Risks Inherent in Our Scenarios

The first few months of Donald Trump’s second term have triggered a massive spike in uncertainty all over the world. That uncertainty has been amplified by the tariffs that have been announced (and in some cases, rolled back), additional threats from the US, and the scope of the retaliatory measures imposed by other countries. Furthermore, the other policies implemented by the US administration, especially regarding immigration and the federal government apparatus, could send the economy into a tailspin. Adding to the instability is the fact that the US reinstated the federal debt ceiling in January. While the Treasury Department has taken “extraordinary measures” to maintain government funding, options are limited. If Congress fails to raise or suspend the debt limit, the government could run out of cash in the next few months, which would increase the risk of payment delinquency—or even default. Assuming the debt ceiling situation is resolved favourably, we’ll still need to watch how the bond markets respond to the increased US Treasuries supply, especially if the deficit grows in response to economic contraction or new spending and tax cuts. US bonds may also be shunned, as disruptive policies may lead global investors to reduce their portfolio exposure to the US. Even though we’ve already revised our forecasts, further adjustments will be needed as the situation evolves. There’s a lot of uncertainty over how much room central banks have to cut interest rates if their economies are hit by stagflation. We’ll also need to keep an eye on whether the Federal Reserve manages to maintain its independence, and if the US markets are still deemed a safe haven. Governments around the world have been hit by political crises, which could further undermine their ability to respond to economic downturns while keeping public finances on solid footing. Add to this the risks of financial instability, including those that can arise when regulatory environments are laxer. Stock markets, bond markets and commodity prices could become more volatile, further slowing the global economy. This is particularly true of currency markets, which have been one of the main outlets for post-tariff volatility.

Financial Forecast

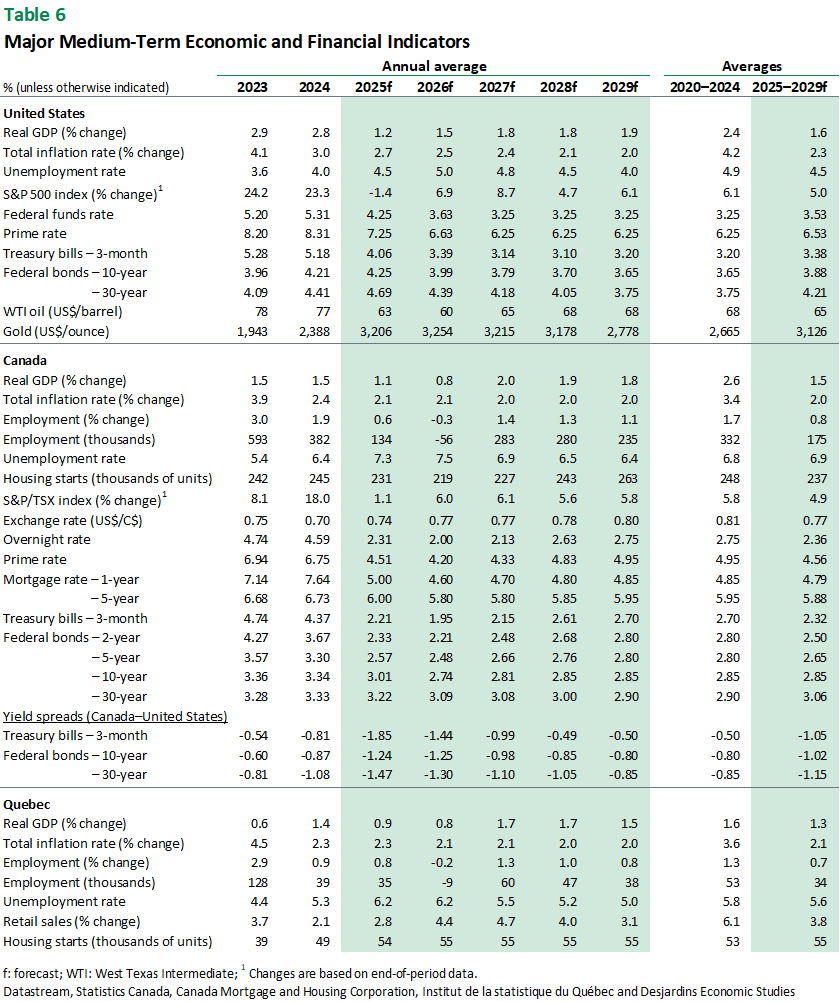

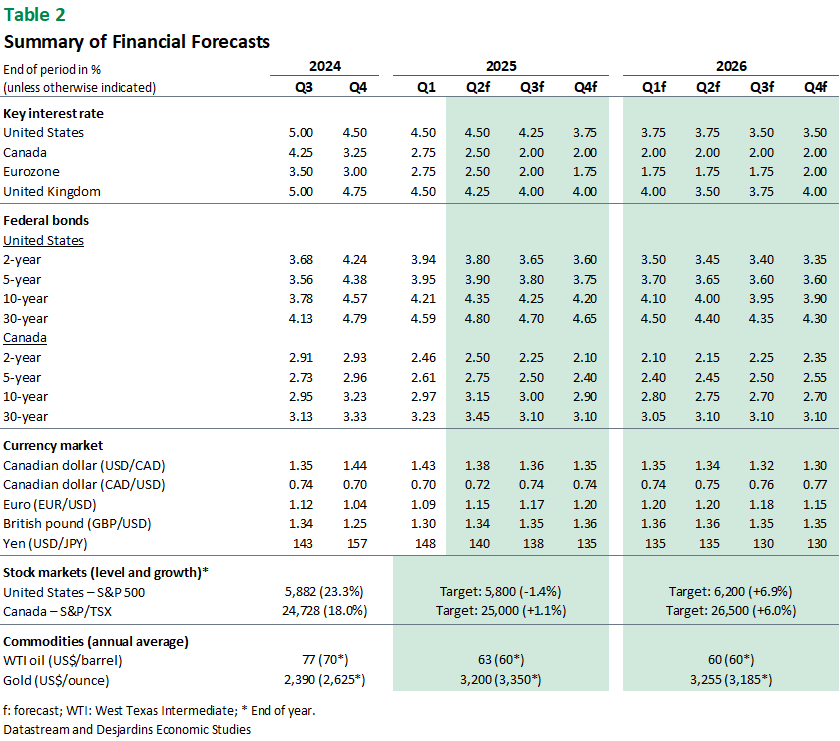

A softening of trade tensions between the US and Canada has reduced extreme downside risks to economic growth. While downside risks are less pronounced relative to our last update, the Bank of Canada will likely need to continue easing to properly manage incoming headwinds. Our forecasts now see the central bank to cut to a terminal rate of 2.00% by the end of this year.

While the Bank of Canada is likely to cut at its upcoming meeting, US policymakers were happy to keep policy rates where they are. Progress on inflation has been slow and the labour market has remained robust so far. As such, policymakers have the luxury of being able to wait for more clarity before recommencing their easing cycle. However, neither the economy nor inflation has fully felt the drag from the barrage of tariffs announced in recent months. Economic activity should slow because of those policies, and we continue to see Fed officials lower their policy rate down to 3.625% by the end of the year. Of course, risks around this forecast are skewed towards a slower pace of easing, given uncertainty over the magnitude of the tariff tailwind to inflation.

US risk assets have retraced most of their 2025 losses following the incremental pullback on tariffs. While we still expect rest-of-world equities to outperform this year, near-term risks are skewed towards US outperformance. Since our previous forecasts, both the USD and CAD have strengthened. We now anticipate USDCAD will remain near current levels towards the end of the quarter, with further strength in the Canadian dollar persisting throughout the second half of the year. A portion of this strength will come from a slower US economy, which may encourage Canadian investors to either repatriate or hedge the currency risk of their investments in US assets. The recent Moody’s downgrade of US sovereign debt reinforces concerns surrounding US debt sustainability. US yields have risen following the news, with the 30‑year eclipsing 5%.

Forecast Tables