- Jimmy Jean • Randall Bartlett • Benoit P. Durocher • Royce Mendes • Mirza Shaheryar Baig • Marc-Antoine Dumont

Tiago Figueiredo • Francis Généreux • Sonny Scarfone • Oskar Stone • Hendrix Vachon • LJ Valencia

Economic and Financial Outlook

The Federal Reserve and the Bank of Canada Could Soon Start Lowering Their Policy Rates Again

August 21, 2025

Highlights

- US trade policy has returned to the spotlight over the last few weeks. President Trump officially announced a series of new tariffs and modified reciprocal tariffs, coming into effect in early August. For now, though, effective tariff rates are below the levels called for in his executive orders, thanks to numerous exemptions, implementation delays and other mitigating factors. This is particularly true for the tariffs targeting Canada and Mexico. We expect that the rates currently in place or already announced will remain in place until at least the end of the year. But the situation is still fluid, and our economic and financial scenarios will be updated as the trade war evolves.

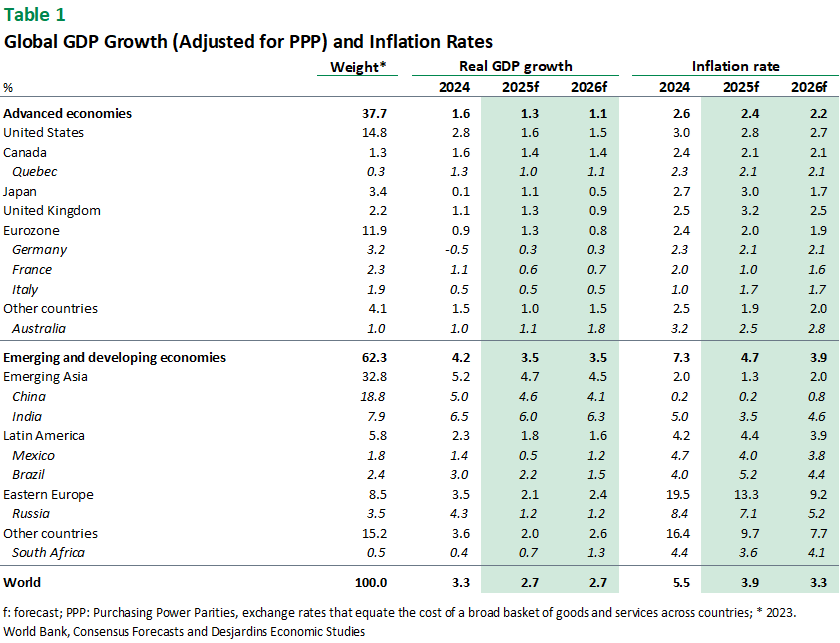

- In the United States, real GDP growth slid in the first quarter before rallying in the second with an annualized gain of 3.0%. That said, this uptick is chiefly the result of significant shifts in both imports and business inventories—final sales to domestic purchasers slowed overall, with an annualized increase of just 1.1%, the weakest since summer 2022. We expect real GDP growth to soften in the quarters ahead, albeit without any sharp declines. The labour market has already shown some signs of cooling and may stall in the months ahead. And while inflation has not yet surged in response to tariffs, producer prices have begun climbing and the most recent announcements from the White House could change the situation.

- The ongoing truce between the United States and China is encouraging. All the same, China’s real GDP growth slowed in the second quarter, and both industrial production and retail sales disappointed in July. And while France, the United Kingdom and Japan all posted relatively solid results for the second quarter, real GDP declined in Germany and Italy. US trade policy should continue to weigh on global economic growth, and countries like Brazil and India could be severely affected, given the especially high tariffs they now face.

- Additionally, recent shifts in US trade policy have led to a further increase in tariffs on Canadian exports. But we expect this to have only a limited overall impact on trade, given the ongoing progress toward CUSMA compliance. That said, slower US growth in the near term should provide a headwind to demand for Canadian exports. As a result, we continue to expect choppy growth for the second and third quarters. Beyond this year, the federal government’s infrastructure External link. and defence External link. initiatives are expected to offer some support to the Canadian economy. Meanwhile, the removal of the federal price on pollution External link., combined with lower energy costs and slower economic momentum, should help contain inflationary pressures. This is especially notable considering the inflationary pressures coming from Canadian counter-tariffs External link.. Indeed, our estimates suggest that inflation over the next year could average close to the Bank of Canada’s 2% target.

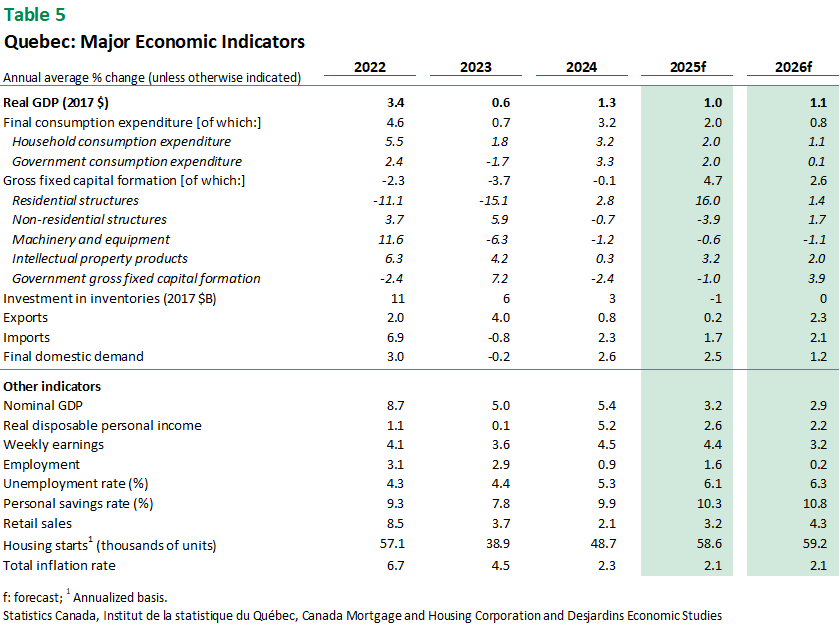

- In Quebec, real GDP is expected to fall into negative territory in the second quarter, with exports suffering a significant decline after many US importers moved their purchases forward in the first quarter. What comes next is less certain for Quebec’s economy. While some sectors will be particularly affected by the trade war, most of the province’s exports should still benefit from the CUSMA exemptions. Under these conditions, real GDP could see virtually zero growth in the second half of 2025.

Risks Inherent in Our Scenarios

Global uncertainty should remain high, given the country-specific tariff hikes already announced, other sector-specific measures and the threat of additional tariffs. Economic growth could also be affected by other policies implemented in the United States, particularly those on immigration and the federal government apparatus. And we’ll need to watch how the bond markets respond to the increased US Treasury supply, now that the One Big Beautiful Bill Act has been signed into law. If global investors find recent policies disruptive, they may scale back their exposure to the United States, giving the cold shoulder to US bonds and other assets. It’s also not clear whether central banks will be able to cut rates if tariffs and supply chain disruptions cause inflation to climb and growth to slow. Geopolitical tensions could further contribute to inflation by pushing the price of some commodities up, including oil. We’ll also need to keep an eye on whether the Federal Reserve manages to remain independent, and if US economic data maintains its integrity. In the longer term, geopolitical fragmentation and budget pressures could make it harder for governments to respond effectively to economic slowdowns without straining their public finances or seeing their credit rating lowered. And there are risks of financial instability, especially if regulatory frameworks become more relaxed. Stock, bond, currency and commodity prices could become more volatile, further slowing the global economy.

Financial Forecast

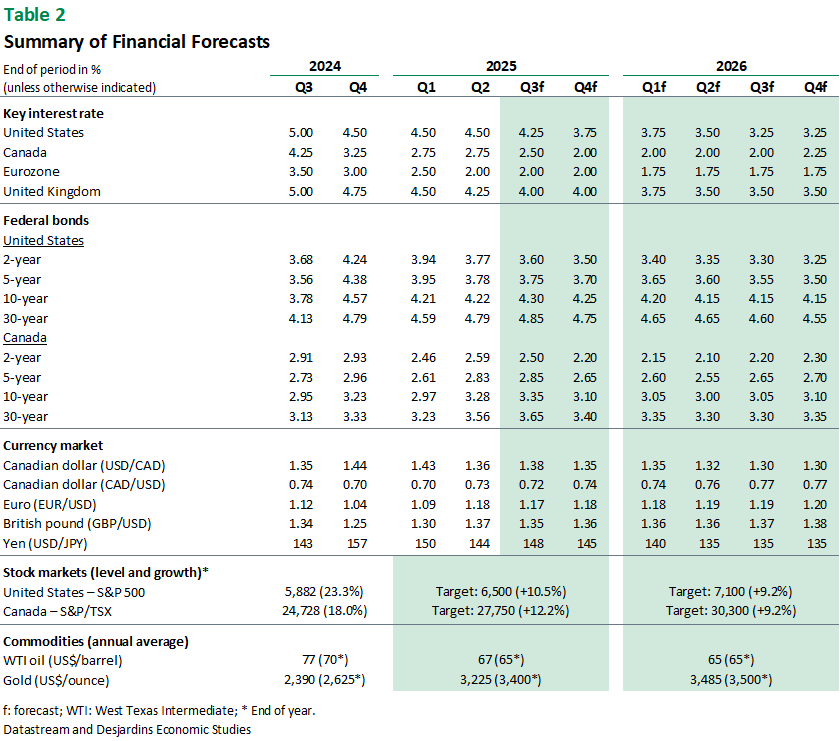

We continue to believe that Canada does not have an inflation problem. Tariffs have not resulted in persistent inflationary pressures thus far, and barring any escalation in retaliatory tariffs, we continue to expect the Bank of Canada will cut rates three times this year. Risks around this forecast are skewed to a slower pace of easing and will depend on incoming inflation and labour market data. The Canadian yield curve should continue to steepen, led by falling front-end rates but also stickier long-term borrowing costs. We still expect yields to fall across the curve, just to a lesser extent on 10‑year and 30‑year bonds.

The story is similar in the United States. While recent inflation readings suggest the inflationary picture is mixed, we still believe that inflationary pressures should subside over the coming year. A weaker labour market coupled with normalizing inflation will likely result in the FOMC resuming its easing cycle in September. While we expect yields to fall stateside, we do not expect to see as large of a drop in 10‑year and 30‑year bonds relative to Canada. Rising deficits and US policy uncertainty should continue to push investors away from US assets over time.

We continue to see equities rising throughout the year, although we expect a period of volatility over the coming months. Incoming rate cuts, corporate buybacks, and more clarity around trade policy should provide a floor for equities into year-end. While we expect foreign exchange markets to be more rangebound over the coming months, the Canadian dollar should appreciate by the end of the year as the economy stabilizes.

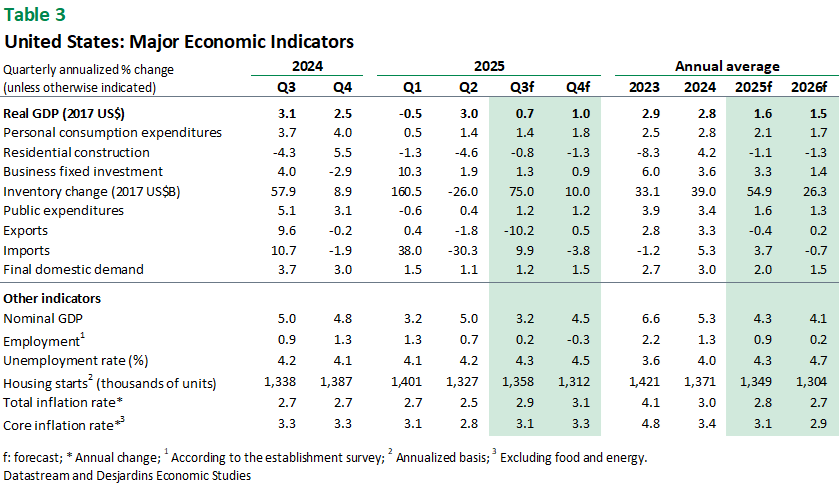

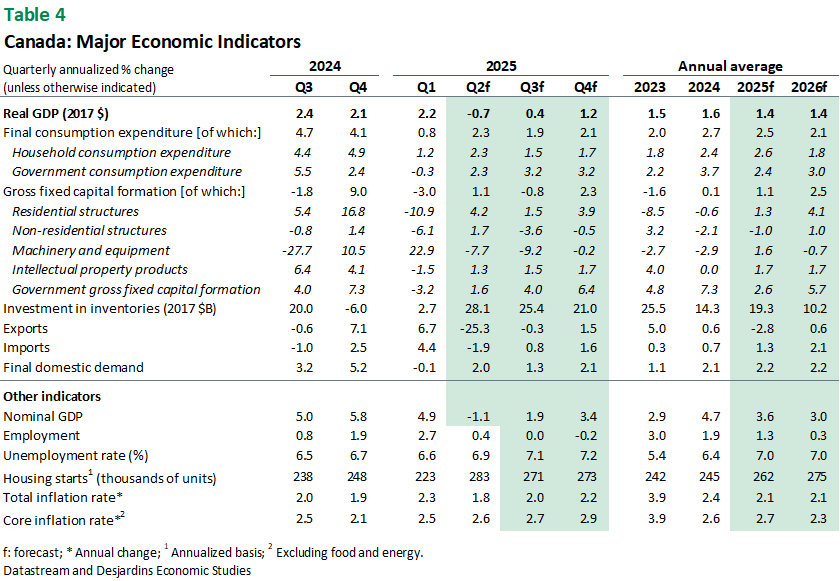

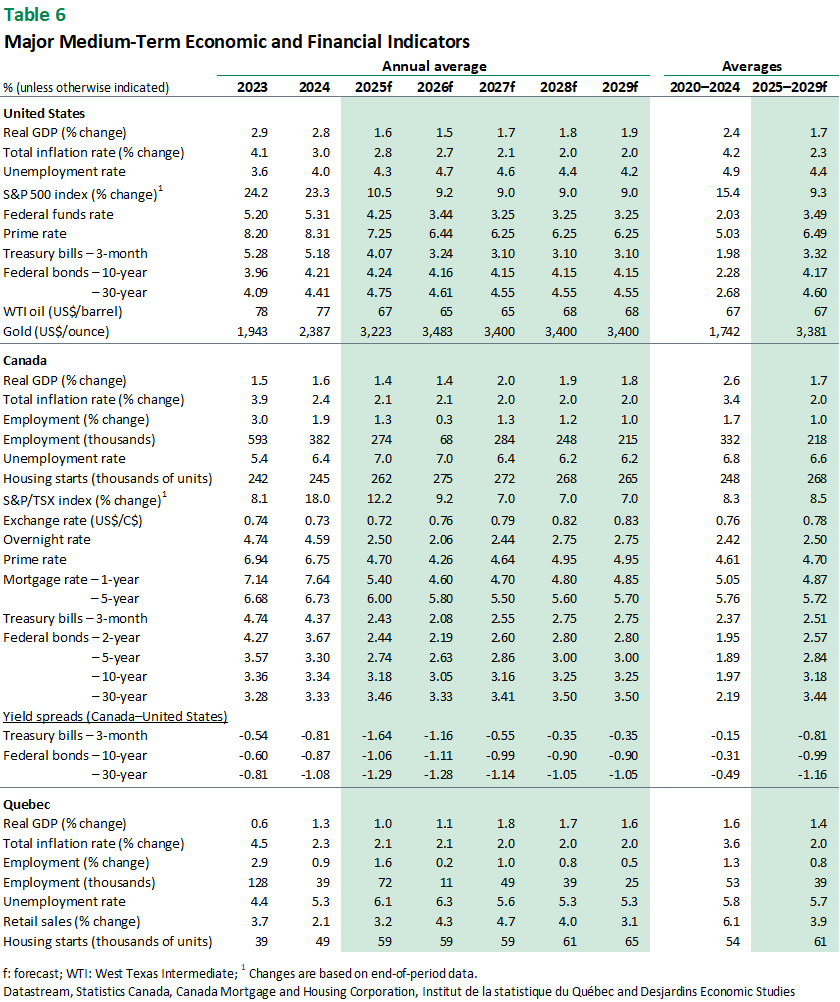

Forecast Tables