- Jimmy Jean, Vice-President, Chief Economist and Strategist

Marc-Antoine Dumont, Senior Economist • Florence Jean-Jacobs, Principal Economist

Commodity Trends

Western Canadian Select Is Faring Better than Expected

May 1, 2025

Highlights

- The WTI-WCS spread remained close to US$10 per barrel, as US refiners appear to have absorbed almost the entire 10% US tariff on non-USMCA-compliant Canadian energy exports. We had previously expected Canadian producers to absorb the US tariff, which would have widened the price gap. In addition, according to preliminary data, China bought more Canadian oil to replace imports from the US, which also helped keep the WTI-WCS spread historically narrow. Henry Hub natural gas hasn’t been so lucky, with prices in the United States falling from over US$4.50 per MMBtu at the start of the year to below US$3.00 per MMBtu currently. China has also imposed tariffs of over 100% on US exports. The lack of affordable access to the Chinese market pushed the US natural gas market into overproduction, causing prices to plummet.

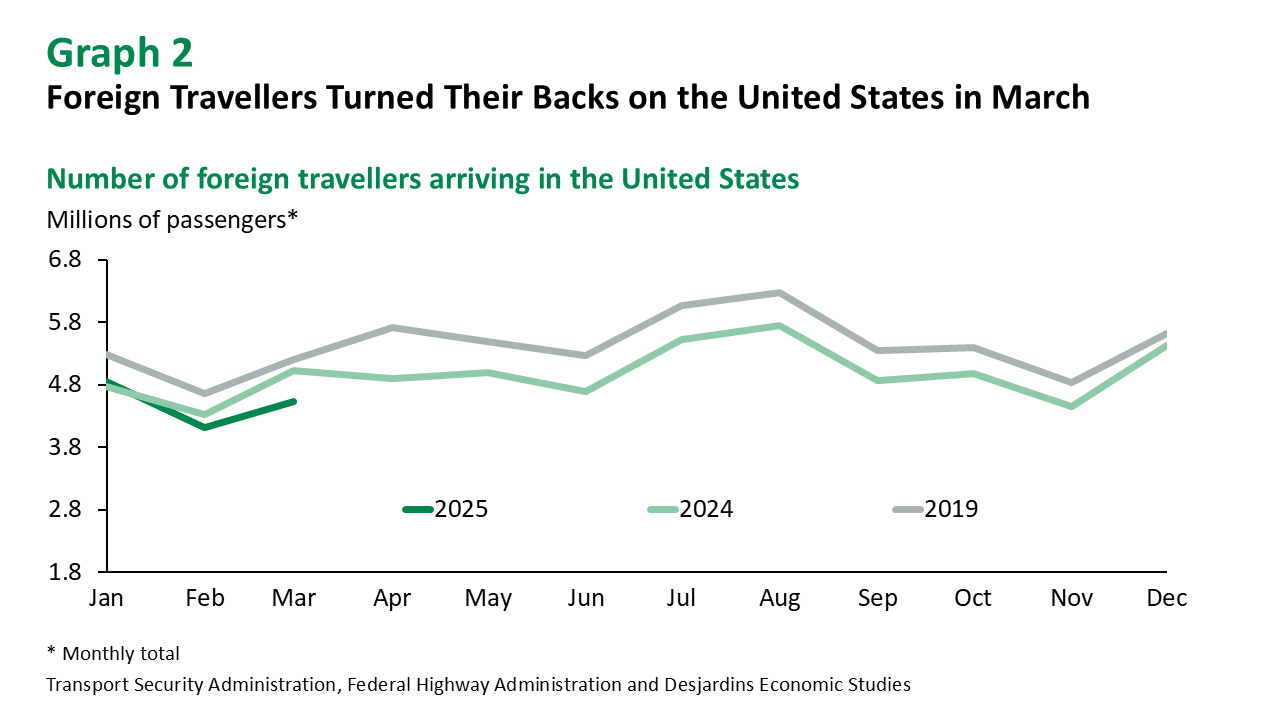

- We’ve revised our year-end target for West Texas Intermediate (WTI) to US$60 per barrel as we anticipate a recession in Canada and the United States and a global economic slowdown, unless the tariff war comes to a swift and permanent end. OPEC+ also unexpectedly decided to increase its May output by 0.4 million barrels per day—three times more than the group originally planned—which could cause a supply glut. The cartel’s output has now exceeded its target for 14 consecutive months, and Kazakhstan has said it would prioritize national interests over those of OPEC+ when deciding on output levels. We’ll be watching closely for signs of any cracks in the group, which controls 35% of global oil output. Meanwhile demand is surrounded by uncertainty, particularly with respect to air travel. The number of foreign travellers arriving in the United States fell 10% between March 2024 and March 2025. The US tourism industry is also concerned that the situation will get worse due to the trade war and changes in immigration policy.

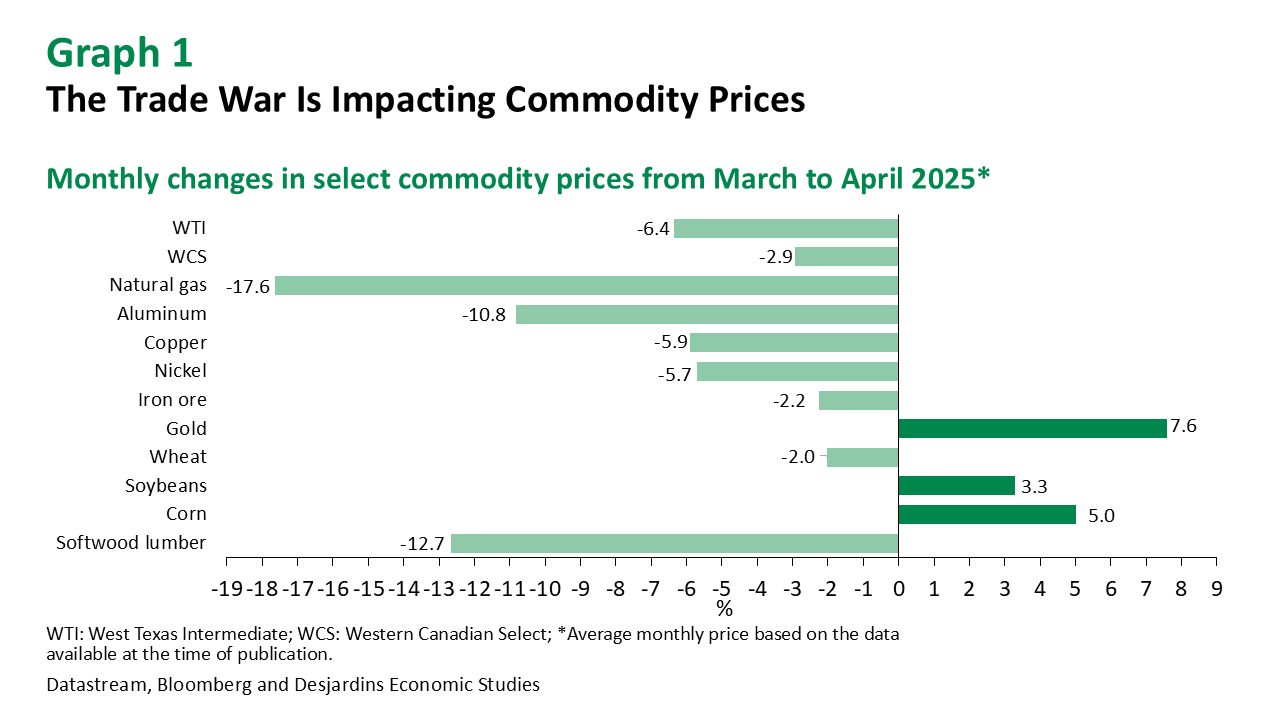

- As expected, base metal prices have fallen since March as the effects of the economic frontloading have dissipated. We expect prices to edge down in the coming months due to deteriorating economic conditions, although steeper declines are possible. Meanwhile, the price of gold has been moving in the opposite direction, with the trade war and financial instability driving a 7.6% jump since March. Amid the economic turmoil and weakening US dollar, we expect gold to end the year at around US$3,350 per ounce.

- North American softwood lumber prices have fallen from early March’s sudden tariff-induced high and are back at their early-February level. A recent announcement by the U.S. Department of Commerce suggested a major increase in countervailing and anti-dumping duties on Canadian lumber this September. The rate paid by exporters could rise from about 15% to over 30% as a result, further reducing the competitive advantage of Canadian sawmills. We also expect economic activity in the United States to contract in the second and third quarters, slowing the pace of housing starts, dampening lumber demand and putting downward pressure on prices. We cannot rule out further softwood lumber tariff announcements from the US administration in the near future—President Trump alluded to them on April 2—which could trigger renewed price volatility.

- Agricultural commodity prices, which typically depend mainly on seeding intentions and the impact of weather on crops, are also likely to be influenced by geopolitical factors over the coming year. The grain and oilseed price scenario is fairly balanced, and the weather in the US Midwest will be a determining factor in the coming months. China will look increasingly to Brazil for its soybean imports given the prohibitive 125% tariff in place on US soybeans. A recent report from the U.S. Department of Agriculture indicated lower demand for wheat, particularly from China. More limited global supply and geopolitical uncertainty could help keep urea prices high, but that will also depend on China’s exports of this nitrogen fertilizer, which have declined in recent months.

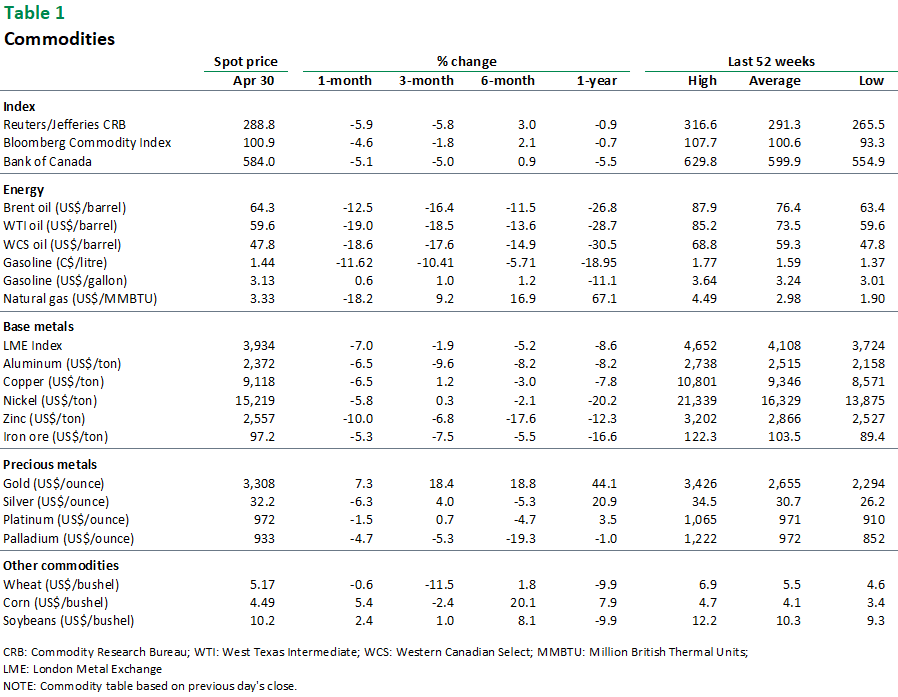

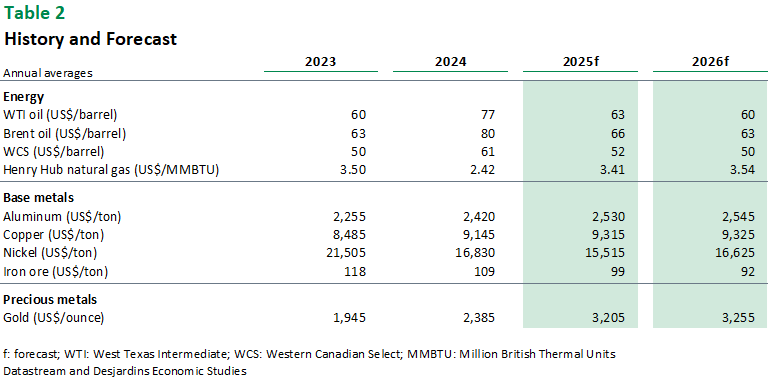

Main Commodities

Commodity Prices