- Jimmy Jean, Vice-President, Chief Economist and Strategist

Marc-Antoine Dumont, Senior Economist • Florence Jean-Jacobs, Principal Economist

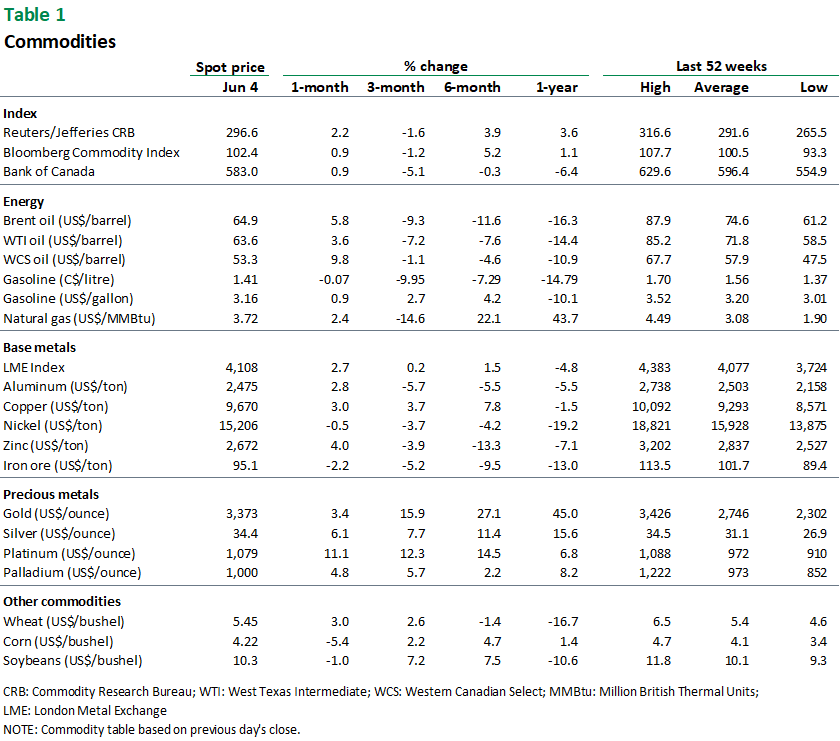

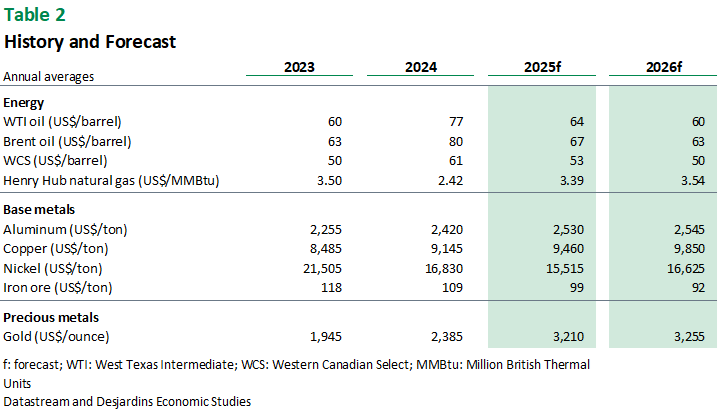

Commodity Trends

Is the Worst Finally Over for Commodities?

June 5, 2025

Summary

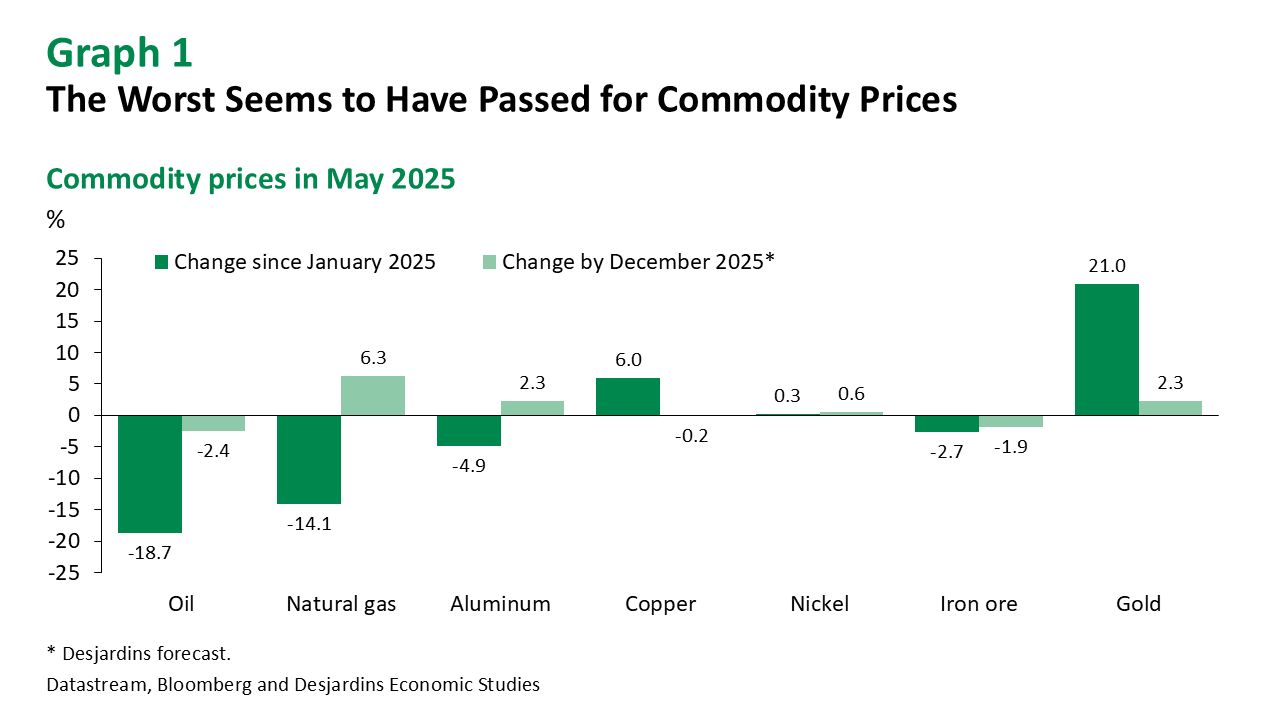

The United States has de-escalated its trade war with China, which could help it narrowly avoid a recession. The situation remains fragile, though, and some of the damage has clearly already been done. Earlier this spring, businesses rushed to stockpile industrial metals and other commodities before tariffs took effect. This sent prices soaring in March—but now that trade tensions have eased, prices are retreating just as swiftly. And while trade tensions may be lower, they’re hardly non-existent. US tariffs on China and the rest of the world remain much, much higher than they were at the start of the year, which will continue to depress global economic growth. That being said, commodity prices aren’t expected to drop significantly. We expect most base metals, excluding iron ore, to see modest price gains by the end of the year. Gold prices, meanwhile, should continue to climb steadily, propelled by ongoing uncertainty, inflation jitters and signs of growing financial stress (graph 1). Oil prices should be kept in check by the abundant supply. Softwood lumber demand has been faltering—and the economic slowdown in the United States may delay and moderate price growth. Prices for most agricultural commodities should stay low: Global supply appears sufficient to meet demand, which has cooled from last year’s levels.

Energy

CUSMA-Compliance Is Helping Canadian Producers Side-Step Tariffs

Forecasts

We still expect a surplus of 0.7 MMb/d (million of barrels per day) on the global oil market in 2025, which should keep West Texas Intermediate (WTI) prices around US$60 per barrel. While it’s true that global economic headwinds may lead to muted demand over the next few months, the main culprit for this glut in supply will be increased production. OPEC+ is also continuing to accelerate the pace of its production increases, in line with our expectations, with the goal of reclaiming the market share lost since the pandemic. On top of that, there is a growing lack of compliance among cartel members. Kazakhstan, for example, exceeded its agreed limit by 28% in April. We also expect the United States, Canada and Norway to accelerate production substantially, but that growth could be undermined by falling oil prices.

Oil

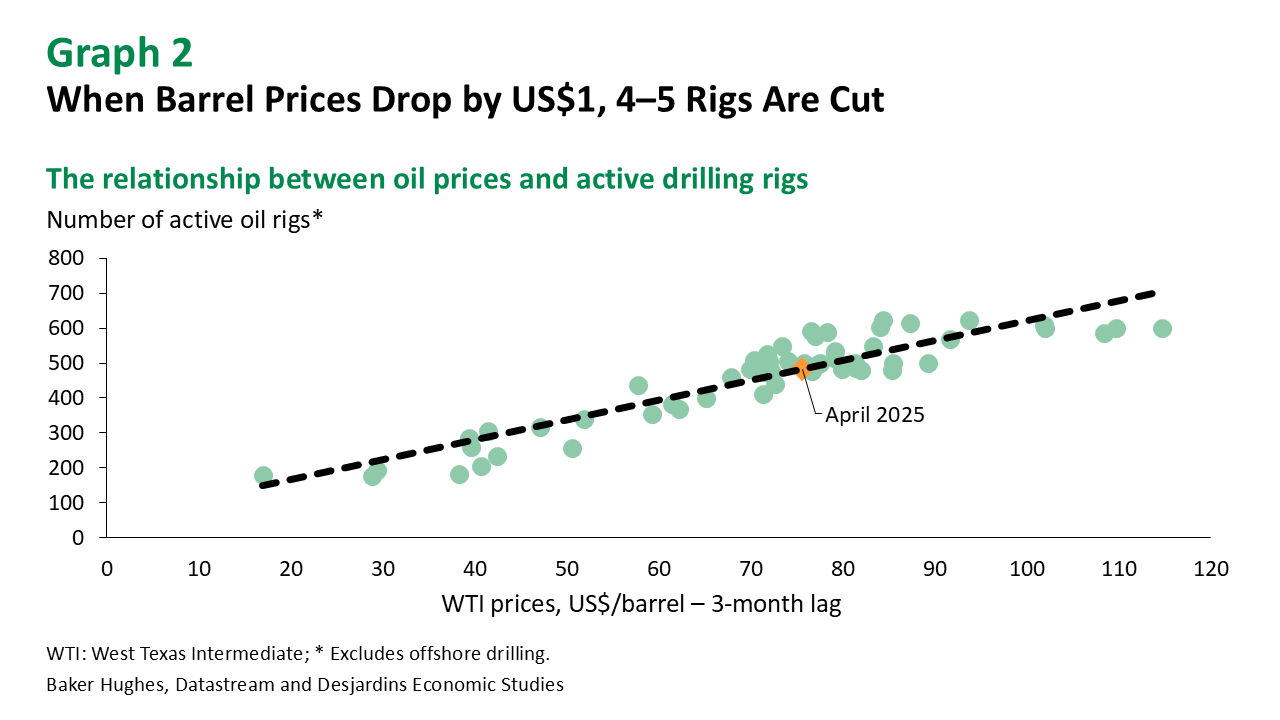

While the United States is on track to increase its crude oil production by 0.3 MMb/d in 2025, current oil prices have led many companies to question—and even scale back—their growth plans for the year. The active rig count, which acts as a leading indicator for US output, dropped from 598 in December 2024 to 574 in April 2025. We estimate that whenever barrel prices drop by US$1, approximately 4–5 US rigs are shut down three months later (graph 2). Prices should continue to drop, and we expect WTI prices to end the year close to US$60 per barrel. If oil prices slide any further, potential growth in US supply could be revised downwards. What’s more, the trade war continues to cast a shadow on US producers. Domestic demand remains stable for now, but could flag this summer, amid deteriorating economic conditions and a decline in international tourism.

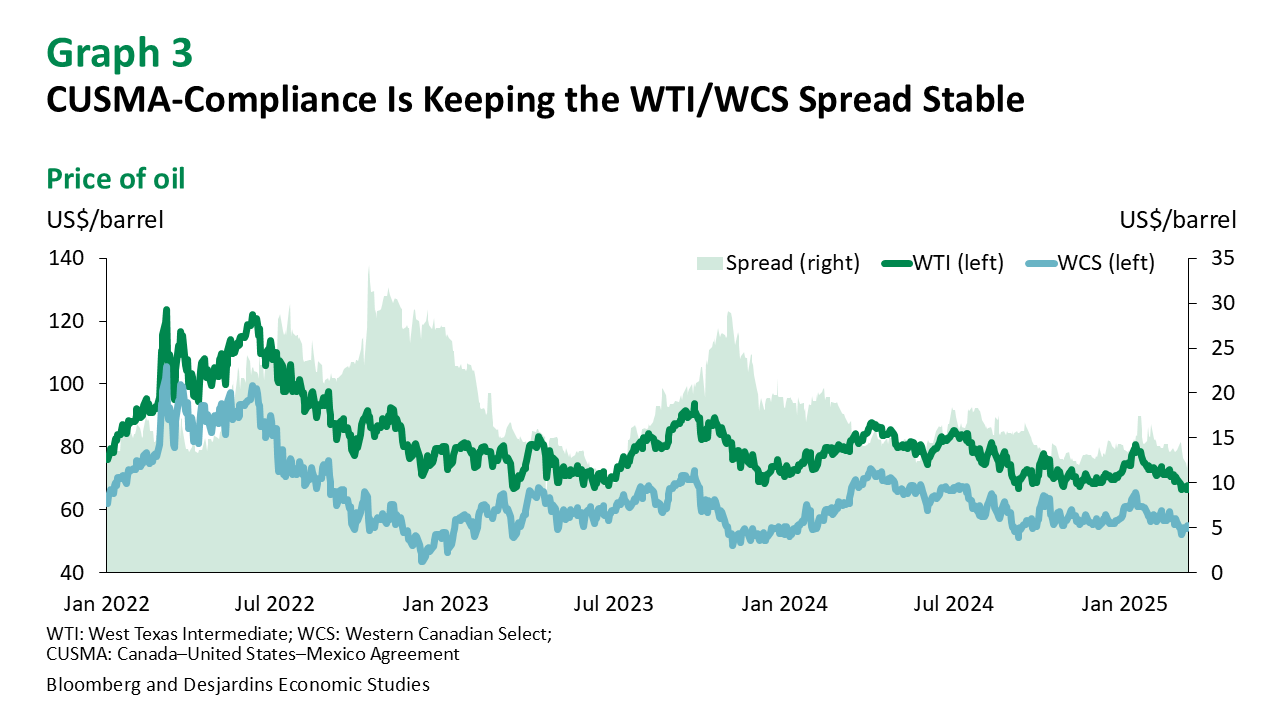

Canadian oil producers are, by and large, avoiding the 10% US import tariff, with the share of CUSMA-compliant1 barrels jumping from 20% in January to 75% in March. This is keeping the WTI/WCS (Western Canadian Select) spread close to US$11 per barrel (graph 3). Our year-end target for the gap between Canadian and US barrel prices is around US$10. Canadian oil exports to the United States did drop 9.6% in March, but one month does not make a trend: We’ll need to see what happens when the annual maintenance season comes to an end, typically in June. Another factor keeping the WTI/WCS spread historically narrow is market diversification. Over the last year, Canadian oil exporters have quadrupled their export volume to the rest of the world, with China emerging as a major buyer. This is primarily due to the opening of the Trans Mountain Expansion pipeline. Since there is still unused transportation capacity, Canadian oil production is projected to grow in 2025 and 2026. However, the wildfires in Alberta will be something to keep an eye on in the very short term.

1 Canadian oil exports that comply with the CUSMA free trade agreement are exempt from US import tariffs.

Gasoline

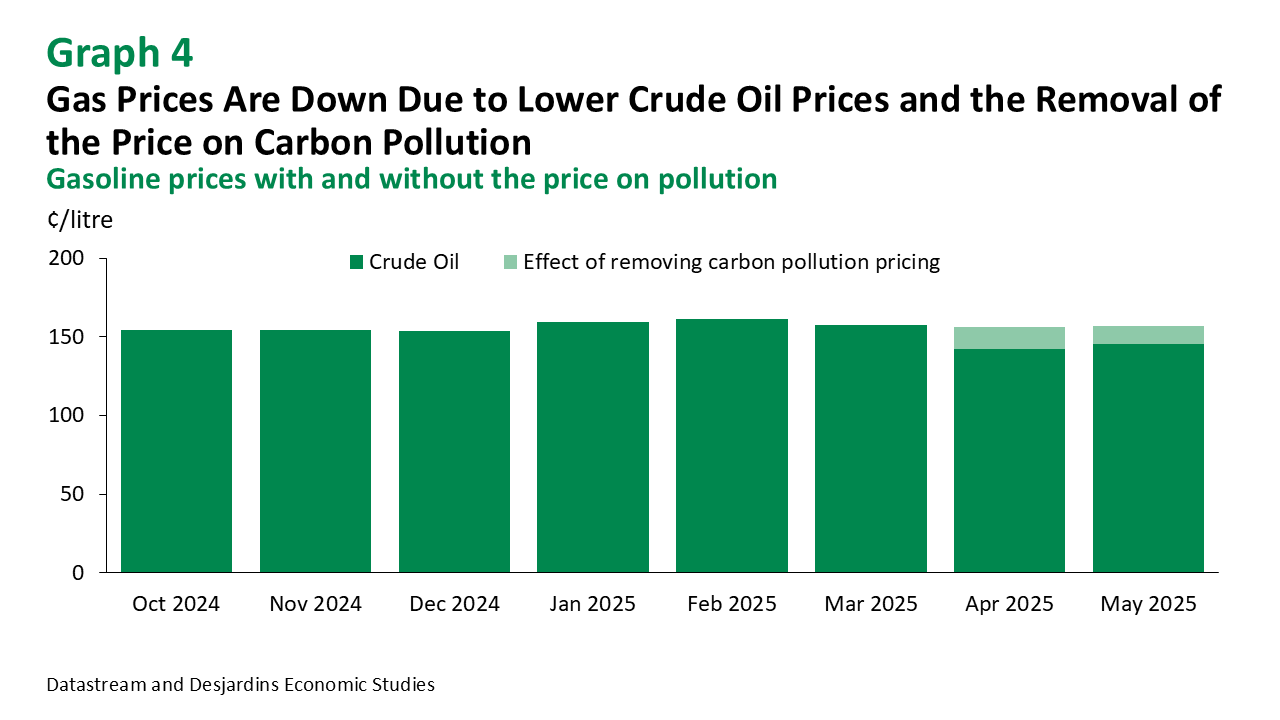

Average gasoline prices in Canada slid 10% from March to April (graph 4), due to lower crude oil prices and the federal government’s decision to cancel the consumer-facing price on carbon pollution. We estimate that nearly 75% of the price decrease is related to the removal of this surcharge. Over the next few months, we expect average gas prices in Canada to rise slightly, as demand typically perks up in spring and summer. But the average price will still remain below its 2024 highs due to lower oil prices. In the United States, gas prices advanced 2% in April. Again, this was a normal seasonal increase that was partially offset by lower oil prices. US refiners also seem to be passing some of the tariff costs on to consumers, instead of absorbing the charges on crude imports. However, we expect this effect to wane in the next few weeks, given the high share of Canadian oil exports that are now CUSMA compliant.

Natural Gas

Henry Hub natural gas prices have shed close to 15% since their April peak, settling at US$3.33 per MMBtu at time of writing. Energy demand tends to be lower in the summer than in winter, which should keep natural gas prices relatively stable over the coming weeks. On top of that, US output hit a record 105.8 billion cubic feet per day in April, which will further moderate price growth. Nonetheless, prices should return to growth by late summer, as the natural gas industry begins preparing for winter’s higher needs. Our year-end price target is therefore US$3.40 per MMBtu. However, the trade war is far from over and could drive prices higher—or push them lower. The US produces more natural gas than it consumes. If international markets like China, Mexico and the European Union are put off by high prices, the domestic market may find itself with a considerable surplus, which would cause Henry Hub prices to plummet.

Base Metals

Modest Price Gains Are Expected

Forecasts

Aluminum, copper and nickel prices are expected to post modest gains at best by the end of the year, as demand for industrial metals began moderating in April. China’s manufacturing PMI also fell below 50 points, signalling a contraction in the sector. The trade war is behind much of the sector’s malaise. Even if tariffs remain stable, the uncertainty surrounding US trade policy should cause investment to decline and manufacturing activity to slow in most countries. All the same, we don’t expect prices to drop any further. Industrial metal prices are rooted in long-term outlooks, and demand is expected to significantly increase because of the energy transition.

Aluminum

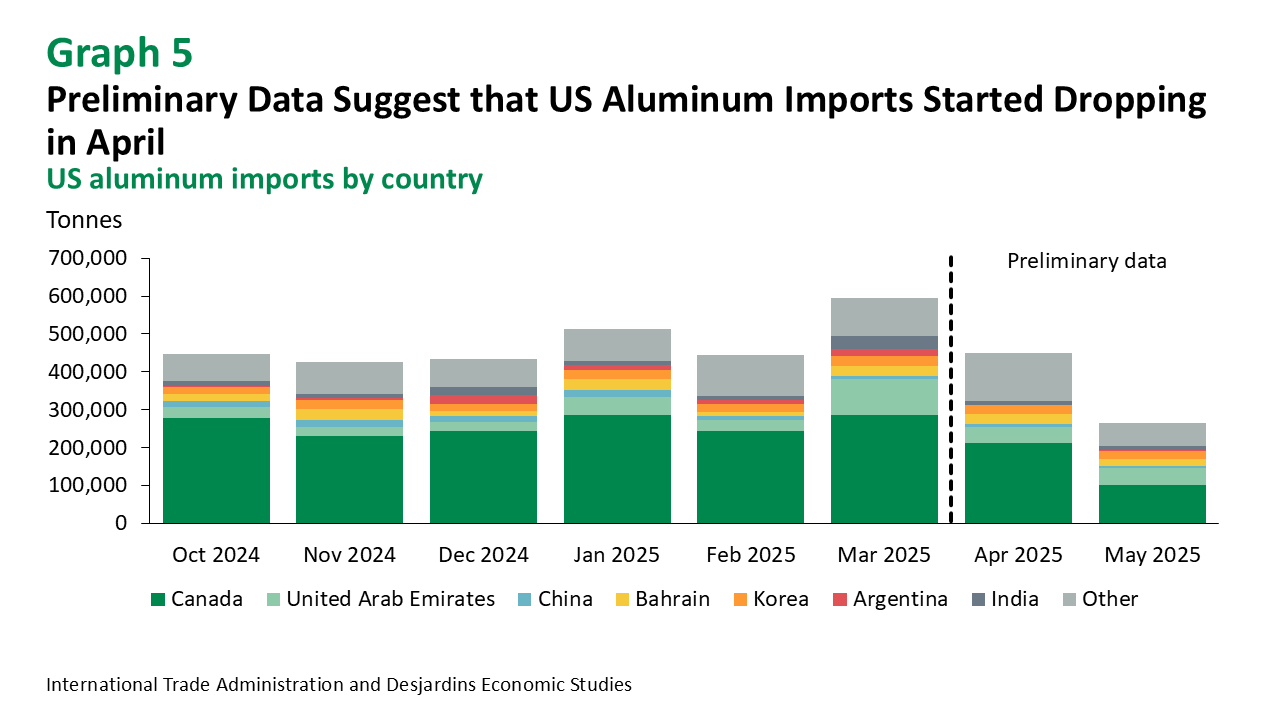

Since peaking in March, benchmark aluminum prices have declined by roughly 9%. This drop can largely be attributed to the 25% blanket tariff imposed on all US aluminum imports and weaker demand. April’s preliminary numbers also suggest that US aluminum imports have shrunk, largely due to lower export volumes from Canada (graph 5). That said, it’s important to exercise caution when interpreting these data, as they’re often revised substantially. This contraction might simply be a reversal of the surge witnessed in March, when US companies accelerated their imports to get ahead of the tariffs. While the US tariffs were ostensibly meant to support domestic manufacturing, all they’ve managed to do so far is drive up the price of aluminum for Americans. Even though the benchmark price is down, tariffs helped push the North American price per tonne from US$3,031 in January to US$3,315 in May. As of this writing, prices have not yet reacted to the recent increase in US import tariffs, which are now 50%. If this tariff remains in place, global aluminum demand is expected to decline, and the North American premium should increase further. It should also be noted that US supply changed very little over that same period. If the country wants to see real production gains, it will need to find more affordable energy sources and solve the skilled labour shortage in aluminum smelters (for more details, see our Economic Viewpoint External link. on the barriers to US reindustrialization).

Copper

While tariff front-running led to substantial gains in March, that momentum is long gone, and the price of copper has fallen 4% (graph 6). Like the other industrial metals, copper is feeling the effects of softer global demand, prolonged uncertainty and decelerating economic growth. Its price could even tick down further in the very short term. That being said, we expect things to turn around quickly. The International Energy Agency still expects copper needs to jump nearly 40% by 2040 as the energy transition continued. There’s a pronounced lack of investment in new mines, and since it often takes around 15 years to go from discovery to production, the copper market may be facing a sizable deficit by the end of this decade. Demand from AI data centres is also booming. While estimates vary, this sector may need an additional 150 to 300 kilotonnes by 2030. We therefore expect copper prices to rally in 2026, ending the year at nearly US$10,000 per tonne.

Nickel

Indonesian nickel refineries appear to be a victim of their own success. After a production boom, which caused profit margins to evaporate, several smelters are now slowing production or shutting down completely. The massive surge in Indonesia’s output caused monthly average nickel prices to sink from US$37,652 per tonne in March 2022 to US$15,146 per tonne in April 2025. The nickel market should end the year with a smaller surplus, which could help prices inch up. As with aluminum and copper, the energy transition will boost nickel’s long-term outlooks. However, protectionist US trade policy and its economic implications are expected to rein in any price growth.

Iron Ore

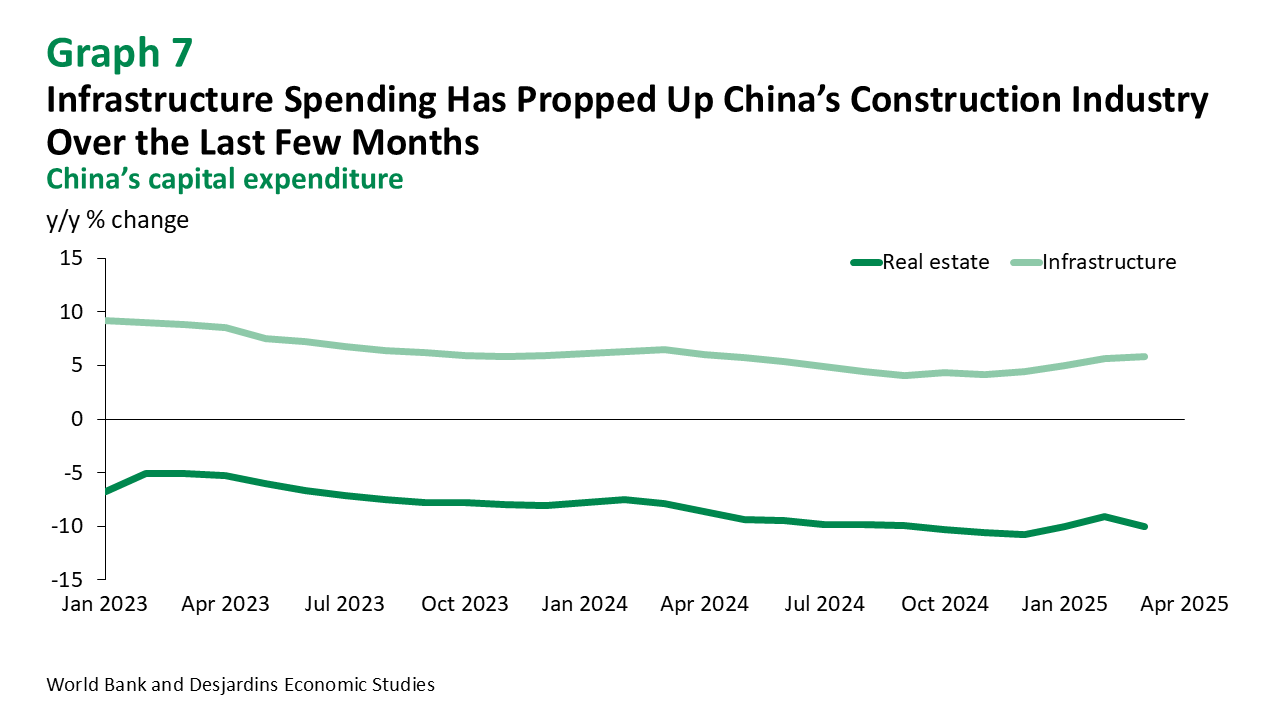

At time of writing, iron ore prices have settled at US$97 per tonne, in response to cooling demand and an ample supply. The recent increase in tariffs on all US steel imports—from 25% to 50%—is likely to dampen demand. While US steel prices are expected to rise due to a supply squeeze, regional prices outside the United States may decline, as the market would be oversupplied. Additionally, the ongoing slump in China’s property market is likely to exert further downward pressure on iron ore and steel prices. While average home prices in China have stabilized, investment in the residential sector has shown no signs of recovery (graph 7). Over the last few months, government infrastructure spending has been the only thing keeping the construction industry afloat. Prices may dip even further than anticipated if the United States and its major trade partners continue to push tariffs higher. We’re calling for a year-end price target of close to US$95 per tonne.

Precious Metals

The Gold Rally Isn’t Over—It’s Just Taking a Break

Forecasts

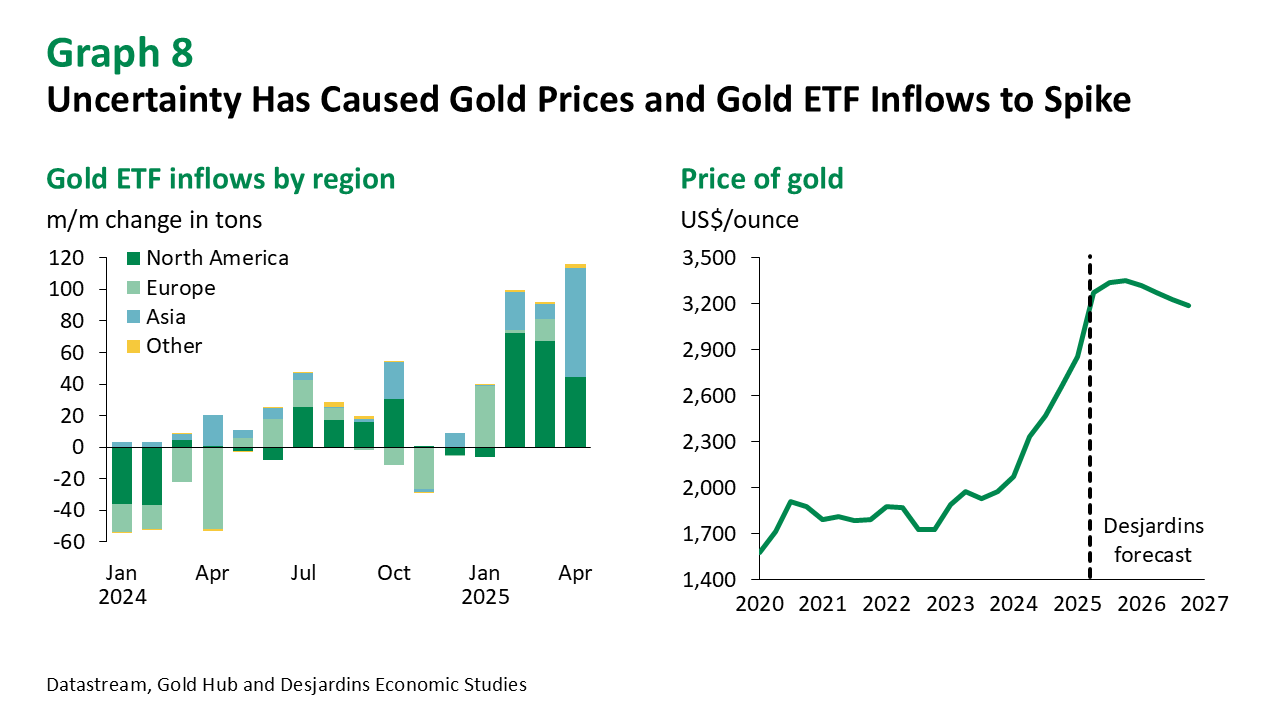

As has been the case for several months now, US domestic and trade policy decisions have been the most important—and volatile—factors influencing our gold price forecast for 2025. While the White House may have reached a truce with China, the European Union is now in the hot seat, facing potential import tariffs of 50%. What’s more, the administration’s plan to slash corporate and individual income taxes has reignited concerns that the US government will be unable to finance its debt in the long term, sending investors running for a safe haven. Little has changed, and given this prolonged uncertainty, we expect gold prices to resume their upward trend in the next few weeks, ending the year at approximately US$3,400 per ounce.

Gold and Silver

While North America accounted for the majority of gold-backed ETF inflows in recent months, Asia emerged as the leading contributor beginning in April (graph 8). White House policies are driving down the value of the greenback and raising concerns over its status as a safe haven currency. In response, investors are increasingly turning to the precious metal. Tighter financial conditions, as illustrated by the rise in 10‑year and 30‑year bond yields around the world, also helped drive gold prices up in the first half of April. However, we expect prices to lose steam in 2026, mainly in the second half of the year. By that point, investors should be accustomed to the new political landscape and the global economy External link. should have improved. We also expect gold mining production to increase. The price of silver has also benefitted from the push for safe-haven assets, and at time of writing is US$33 per ounce. We expect the silver shortage to persist as well, meaning prices should shoot up further in the coming months.

Platinum and Palladium

The April decision to relax tariffs on imported auto parts gave both platinum and palladium prices a boost, since these metals are both used in catalytic converter manufacturing. Prices for these precious metals were also subject to upside pressures from ongoing global uncertainty, the weaker US dollar and tighter financial conditions. Platinum and palladium have posted respective price gains of 11.5% and 6.3% since the end of April. That said, platinum is in short supply, which should help its price grow more quickly. Palladium prices, on the other hand, should flag. Mining output is abundant, and economic headwinds will lead to weaker industrial demand.

Other Commodities

Agricultural Prices Should Stay Fairly Low in 2025, and Lumber Demand Appears Lukewarm This Spring

Forest Products

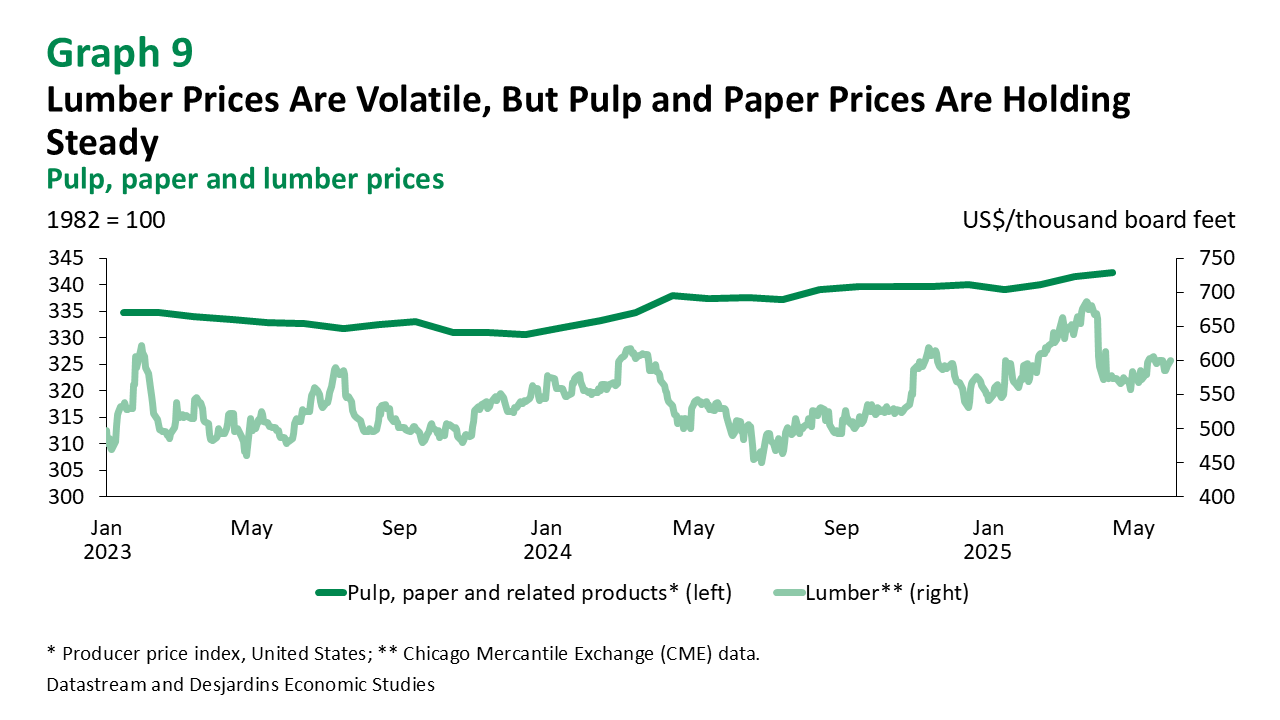

While pulp and paper prices remain stable, lumber prices have fluctuated considerably since the beginning of the year, due to tariff uncertainty (graph 9). After plummeting in April, prices in US dollars edged up slightly mid-May. However, it’s not clear if this recovery is due to the recent thaw in trade tensions (however fragile that may be), nor are we certain it will continue.

According to the Conseil de l’industrie forestière du Québec (CIFQ), Canadian softwood lumber mills were able to quickly comply with CUSMA rules, and their sales shouldn’t be overly affected by the US tariffs announced in 2025. However, Canadian lumber exports are still subject to anti-dumping and countervailing duties—and according to the U.S. Department of Commerce, these penalties will rise from 14.40% to 34.45% starting in late summer.

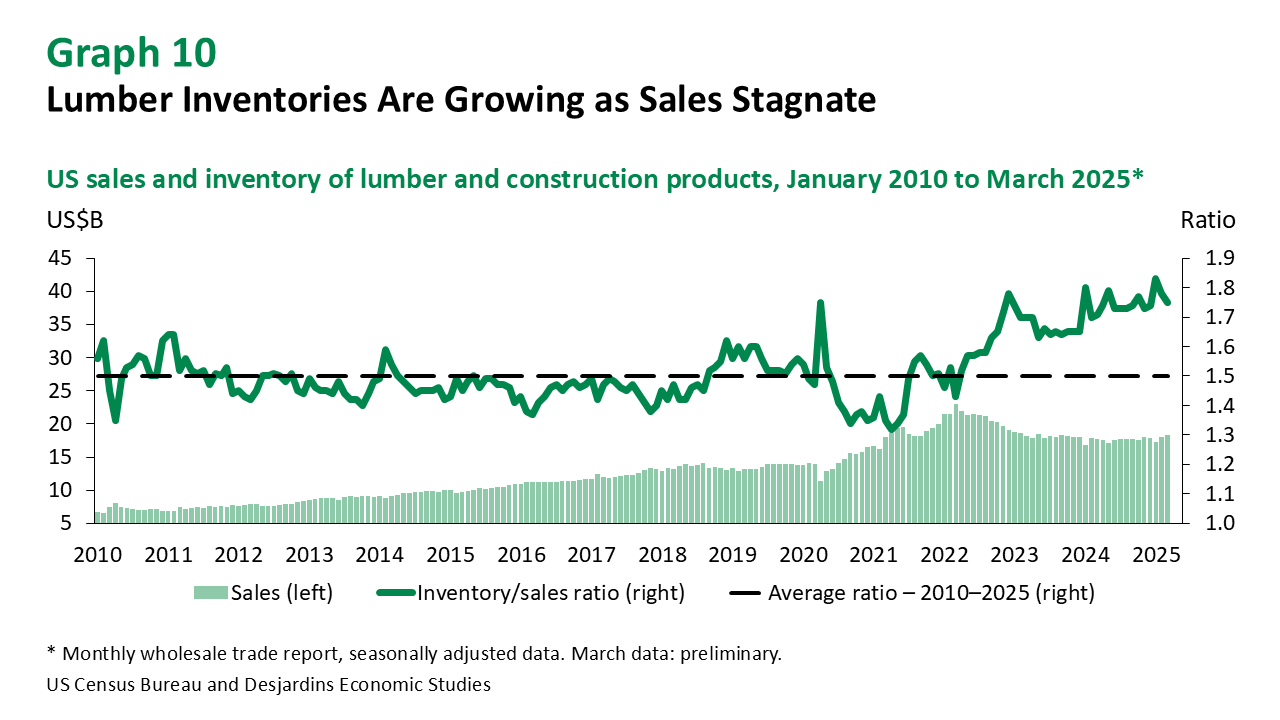

Future lumber price developments will largely depend on the US economic trajectory over the next few months. Our most recent Economic and Financial Outlook External link. calls for weak economic growth in 2025 and a drop in housing starts over the course of the year. Sales of lumber and other building products are sluggish, and inventories are growing (graph 10). Spring is here, but demand has yet to ramp up and US builder confidence was still shaky as of mid-May (NAHB External link.).

Over a longer horizon, though, two factors should support lumber prices. First, even if the current economic conditions temper demand in the short term, the fundamental need for lumber isn’t changing. It’s essential for building and repairing homes in North America. Second, the Federal Reserve is expected to cut rates in the second half of the year, which should help revive construction and, consequently, lumber demand. However, this recovery could be limited by the US government’s immigration (and deportation) policies, which will affect the pool of labourers available to keep up with construction demand. More than one third of construction workers were born outside the United States (U.S. Bureau of Labor Statistics External link.).

Agricultural Commodities

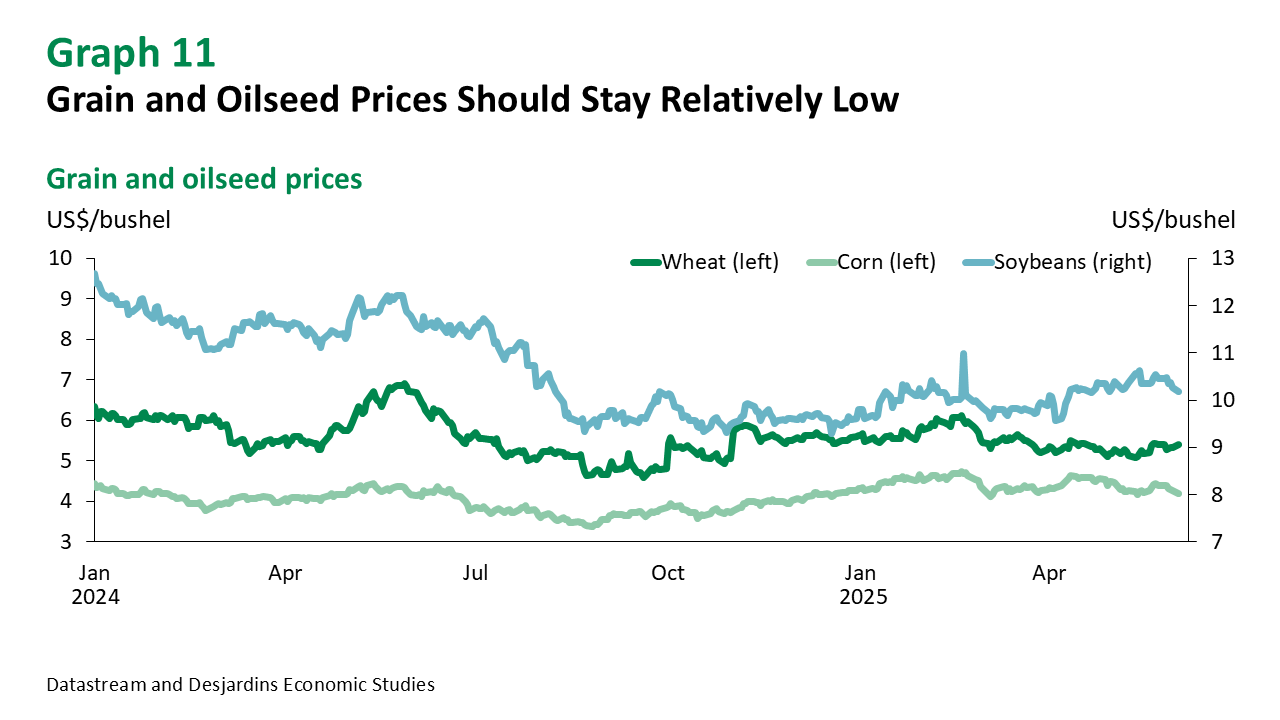

Agricultural commodity prices are facing headwinds in the medium term (graph 11). Trade tensions and the related global economic slowdown are the biggest factor driving down corn, wheat and soybean prices this year. But while prices should remain low, we don’t expect a sharp decline either. The depreciation of the US dollar should support global grains demand, as most trades are done in US dollars.

Corn prices were higher at the start of the year and producers upped their corn plantings accordingly. Supply should therefore be abundant in 2025–2026. Crude oil prices have gone down, making corn-based ethanol less attractive in comparison, so demand on that front has slipped as well. All of this will weigh on corn prices—though since corn is used in animal feed, the lower prices could be appreciated by livestock producers. Wheat production is expected to be abundant and sufficient to meet growing wheat consumption. Prices for soybeans are also expected to drop over 2025, according to the World Bank External link., as strong harvests worldwide in 2024–2025 raised beginning stocks. Global supply should also expand in 2025–2026. While China is expected to slash its imports of US soybeans, that reduction will likely be offset by increased imports from Brazil. Typically, China purchases more than half of all US soybean exports. But according to the U.S. Department of Agriculture (USDA External link.), the lower export volume will be more than offset by an increase in soybean crush (the process of transforming soybeans into meal, oil and flour), supporting domestic prices in the United States.

Commodity Prices