- Jimmy Jean, Vice-President, Chief Economist and Strategist

Marc-Antoine Dumont, Senior Economist • Florence Jean-Jacobs, Principal Economist

Commodity Trends

Fundamentals Drive Oil Prices Lower

July 24, 2025

Highlights

- With the price of WTI (West Texas Intermediate) at US$66 per barrel, market fundamentals suggest a modest pullback in the short term. Supply remains ample, while demand continues to be dampened by persistent trade tensions and geopolitical uncertainty. The International Energy Agency anticipates a production surplus of around 1 million barrels per day in the third quarter, adding further downward pressure on prices. In this context, WTI prices could gradually trend toward US$65 per barrel by the end of the year. With respect to natural gas, elevated summer temperatures are supporting demand for air conditioning, while concerns over tighter supply—particularly due to tensions in the Middle East—have pushed Henry Hub prices above US$3.50 per MMBtu (Million British Thermal Units). However, prices are expected to remain relatively stable over the coming months.

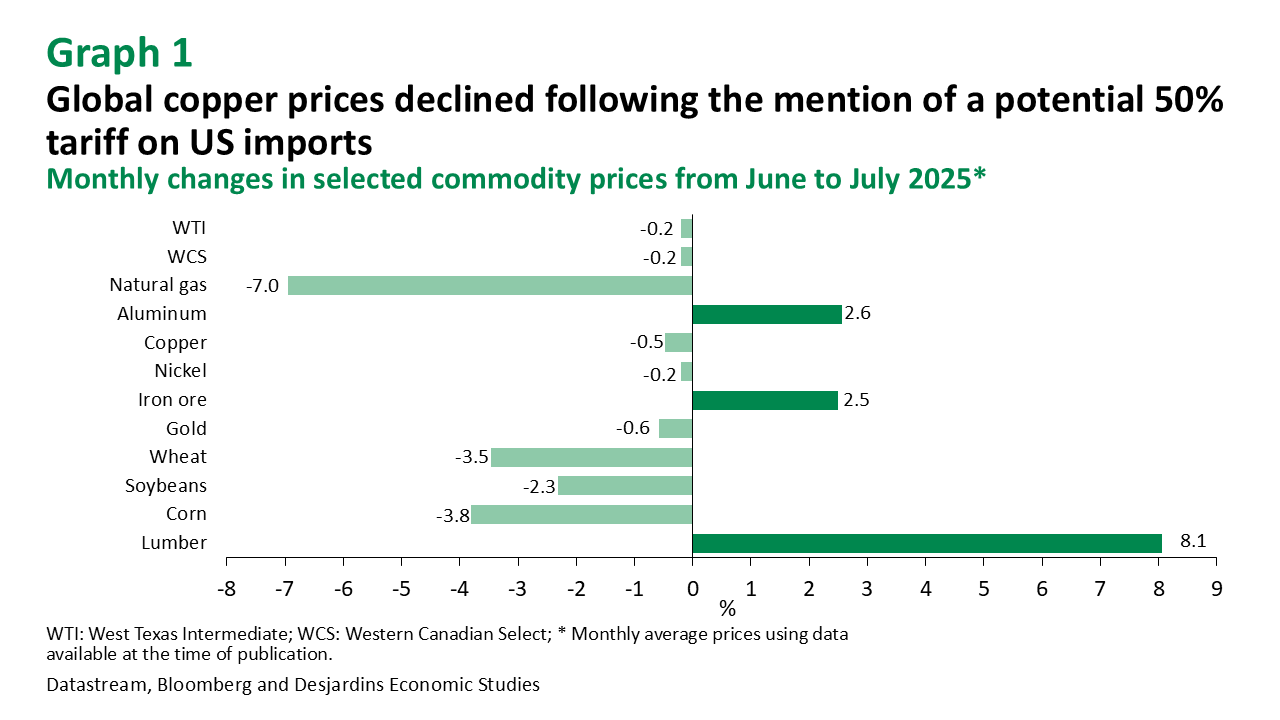

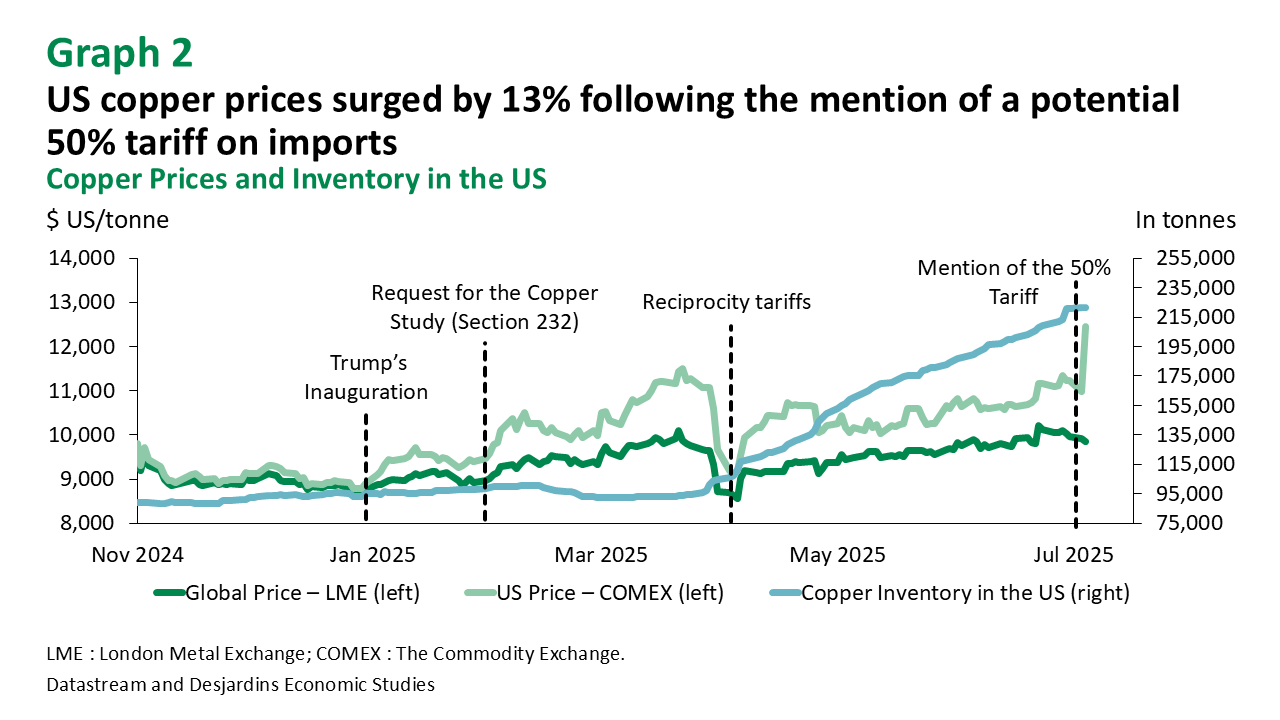

- Although Donald Trump has raised the possibility of imposing a 50% tariff on copper imports starting August 1, no official decree has been signed, leaving uncertainty around the scope of the measure, including potential inclusions and exclusions. Nonetheless, the announcement triggered a strong market reaction, with North American copper prices rising by more than 13%. Global prices, however, retreated, reflecting oversupply and the potential isolation of the US, a major consumer. It is worth noting that US companies have stockpiled the equivalent of a full year’s worth of copper consumption since the beginning of January, which could exert downward pressure on North American prices once the tariff is implemented. We are maintaining our year-end forecast for LME (London Metal Exchange) copper prices at US$9,600 per metric tonne. As for other industrial metals, the resilience of China’s economy amid trade tensions should provide slightly firmer support for prices than previously anticipated.

- Gold prices continue to benefit from a particularly favourable landscape, prompting us to revise our year-end target to US$3,400 per ounce. Persistent trade and geopolitical tensions, combined with inflationary risks, support the fundamentals of the yellow metal. Additionally, a certain degree of dedollarization is enhancing gold’s appeal as a safe haven, encouraging a growing number of investors to turn to this traditional hedge against uncertainty and inflation.

- Wheat, corn, and soybean prices all fell over the past month. Soybean supply from South America is abundant, and favourable weather in the US Midwest and Great Plains is limiting price appreciation. Upside potential also remains limited for corn and wheat. Fertilizer prices could face upward pressure due to the global geopolitical situation, since the Middle East accounts for a significant share of global nitrogen fertilizer production, such as urea. Indeed, the World Bank’s global fertilizer price index jumped 7.3% in June, reaching its highest level since 2023. (World Bank External link.)

- Canada’s lumber sector is deeply concerned about the imminent increase—scheduled for August—in anti-dumping and countervailing duties by the US Department of Commerce. The rate paid by Canadian exporters will more than double, rising from 14.40% to 34.45%, the highest level recorded since the beginning of the softwood lumber dispute. Mill closures and job losses have already been announced across the country. Despite some improvement in July, North American lumber prices are struggling to regain momentum, adding to the challenges faced by sawmills. A modest and hesitant recovery is underway, but only limited appreciation is expected in the coming months. This is due to high mortgage rates in the US, which are slowing the pace of housing starts and demand for lumber. While pent-up demand for new residential construction is significant and could materialize in the medium term, a recovery is not expected this year.

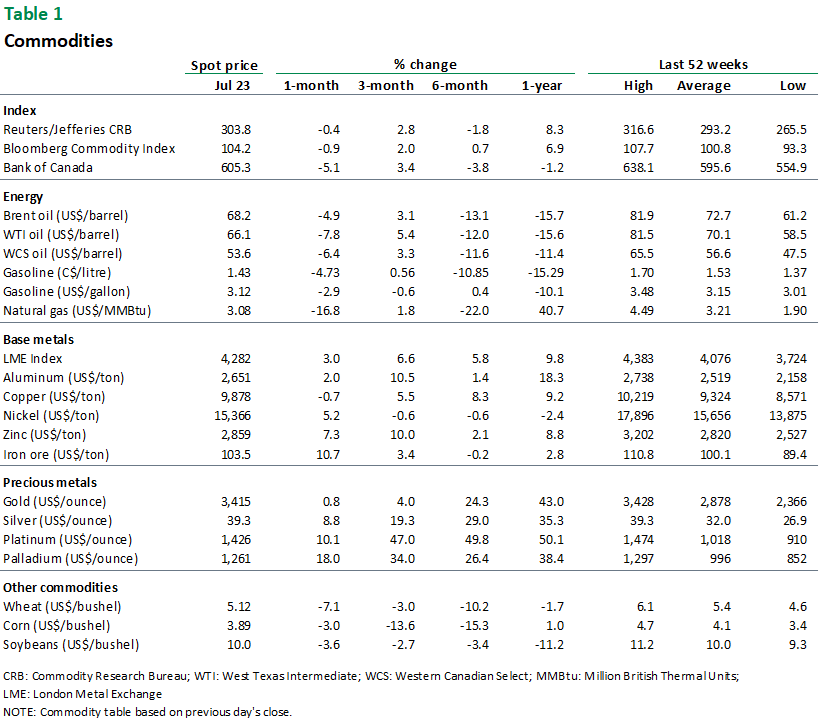

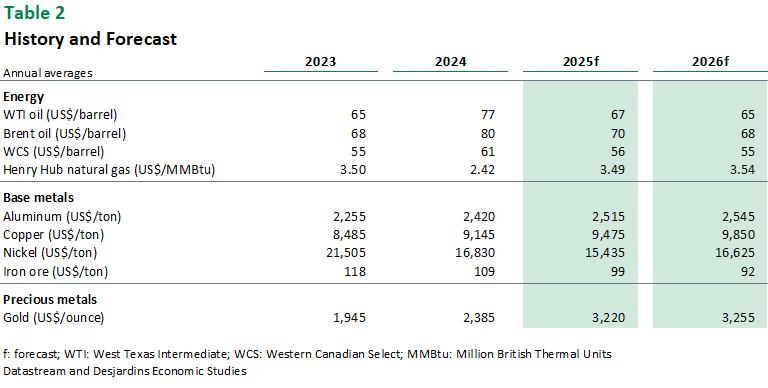

Commodity Prices