- Jimmy Jean, Vice-President, Chief Economist and Strategist

Marc-Antoine Dumont, Senior Economist • Florence Jean-Jacobs, Principal Economist

Commodity Trends

Gold Continues to Shine

August 28, 2025

Highlights

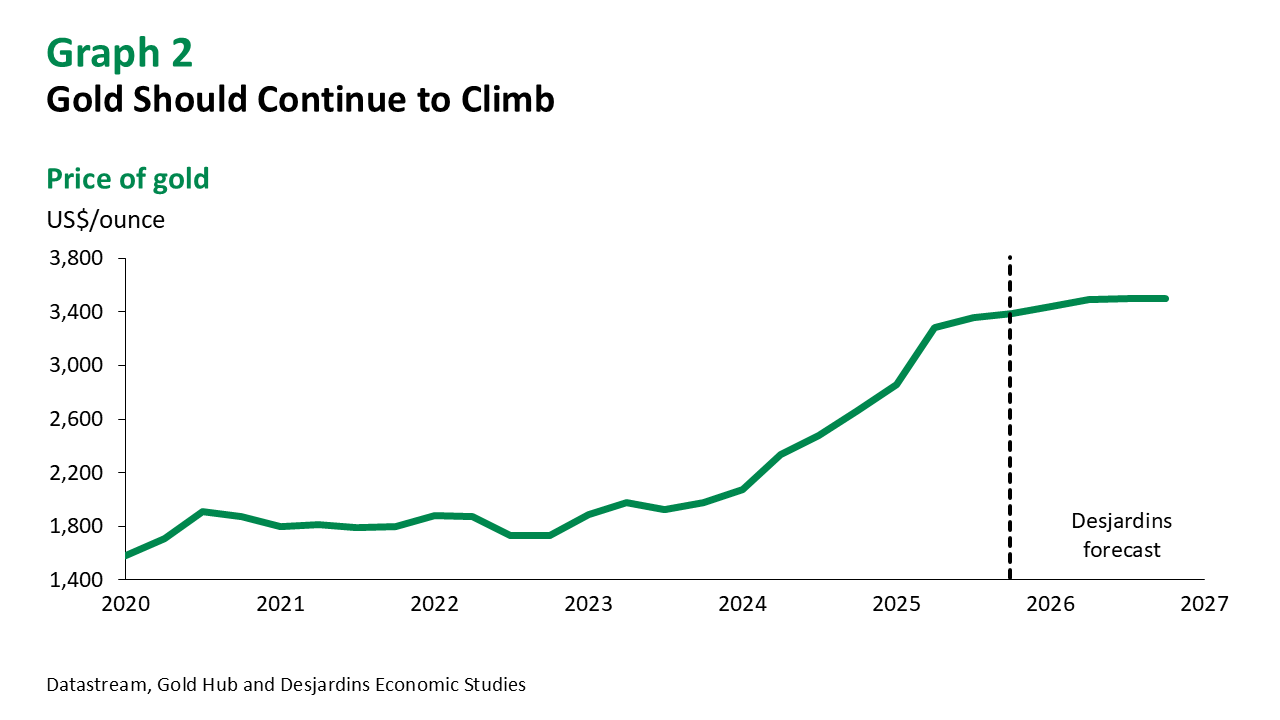

- Ongoing economic and geopolitical uncertainty should help gold end the year around US$3,400 per ounce. With interest rate cuts set to resume this fall and inflation expected to remain above the 2% target in the United States, gold should hover near the US$3,500 mark in 2026. Prices are also being supported by growing central bank gold reserves—part of a global move away from the dollar that shows no signs of letting up.

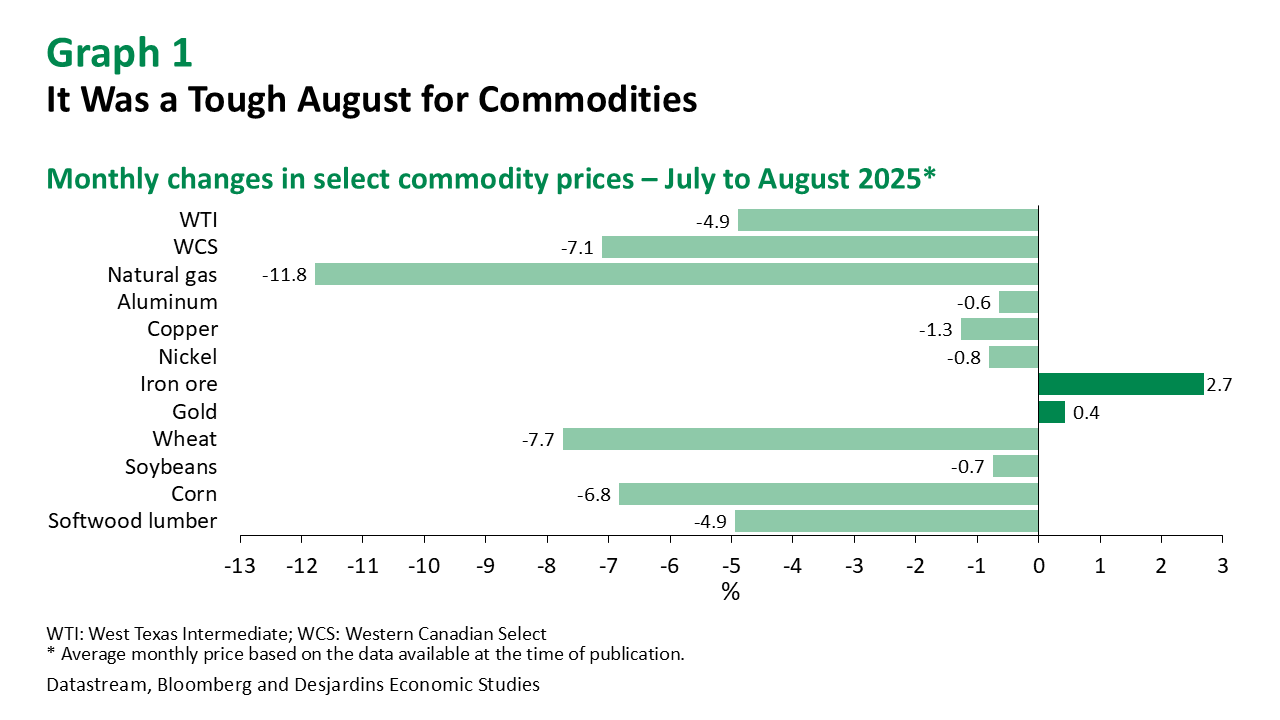

- Abundant supply continues to weigh on oil prices, with the price of WTI (West Texas Intermediate) stabilizing at around US$64 per barrel following a period of heightened volatility. Prices are being propped up by strong refinery demand, especially in Asia, but this could change as OPEC+ boosts production over the coming months. If OPEC+ does ramp up production as planned, supply could outstrip demand by nearly 4 million barrels per day in Q1 2026, possibly triggering a sharp price correction. While OPEC+ is unlikely to meet its production target, this highlights the downside bias in today’s oil market.

- The 50% US tariff on copper imports wasn’t as bad as the market was expecting in July. It ended up applying to a limited number of semi-finished copper products, not raw or refined ore. (For more information, see Trump Turns His Attention to Copper External link.). Following this announcement, the North American premium on copper ore collapsed after surpassing US$2,300 per ton earlier in July. But it’s still about US$100, roughly double its historical average, reflecting ongoing market uncertainty. Aluminum and steel also took another hit after more than 400 products including aerosol cans and door frames were added to the list of goods subject to 50% tariffs. While these tariffs apply only to the metal components of these products, they’re expected to put downward pressure on demand. Despite these developments, we're maintaining our year-end price targets for industrial metals, as the global economy has proven more resilient to the trade war than initially anticipated.

- Canadian softwood lumber exporters saw the combined rate of US countervailing and anti-dumping duties double to a record 35% in early August. (Unlike import tariffs, these duties are paid by Canadian exporters, not US importers.) This caused serious headaches for Canadian sawmills and fuelled price volatility. While US lumber futures fell on the Chicago Mercantile Exchange, Canadian price indexes took distinctly different paths, with the price of lumber destined for the United States rising as sawmills passed on some of the higher duties to customers, while the price of lumber destined for Canada remained relatively unchanged. US housing market conditions will play a key role in lumber prices going forward, but for now, it looks like they’ll continue to be contained by low builder confidence. We expect the Federal Reserve to resume rate cuts in September. If this results in lower long-term mortgage rates, it could give the housing market a boost.

- Wheat and corn prices continue to fall. Good weather in the United States is translating into high corn yields, meaning we could see lower prices over the coming months. Global wheat production has been abundant this year as well. Soybean prices rebounded in the second half of August, and according to the latest USDA External link. report, prices should continue to rise as low seeded acreage results in lower supply this year. Meanwhile Canadian oilseed exporters are facing a new obstacle. After imposing a 100% tariff on canola oil and canola meal in March of this year, China slapped a 75.8% tariff on Canadian canola seed exports in mid-August. At the same time, global fertilizer prices continue to rise, with the World Bank index External link. jumping 8% between June and July on higher urea prices.

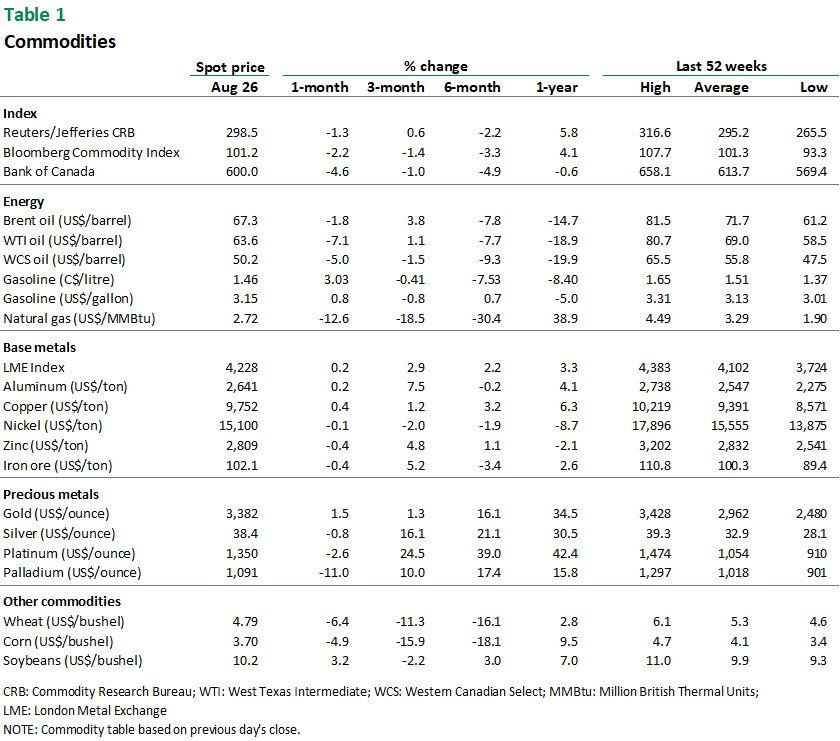

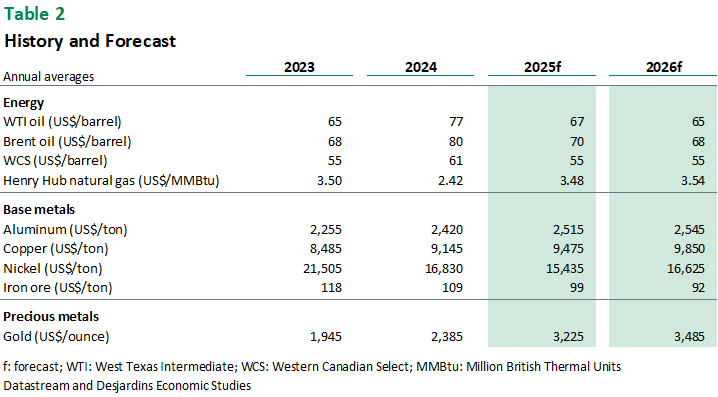

Commodity Prices