- Florence Jean-Jacobs

Principal Economist

Economic News

Canada: Retail Sales Show Surprising Resilience in March and April

May 23, 2025

Highlights

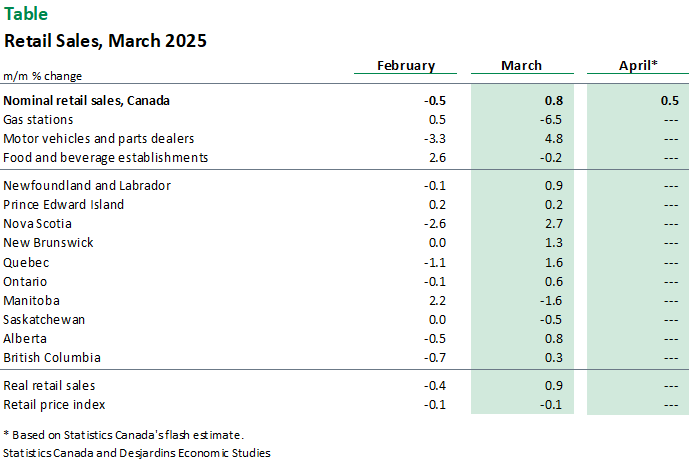

- Retail sales increased by 0.8% m/m in March, one tick above Statistics Canada’s flash estimate. The table below summarizes key data points.

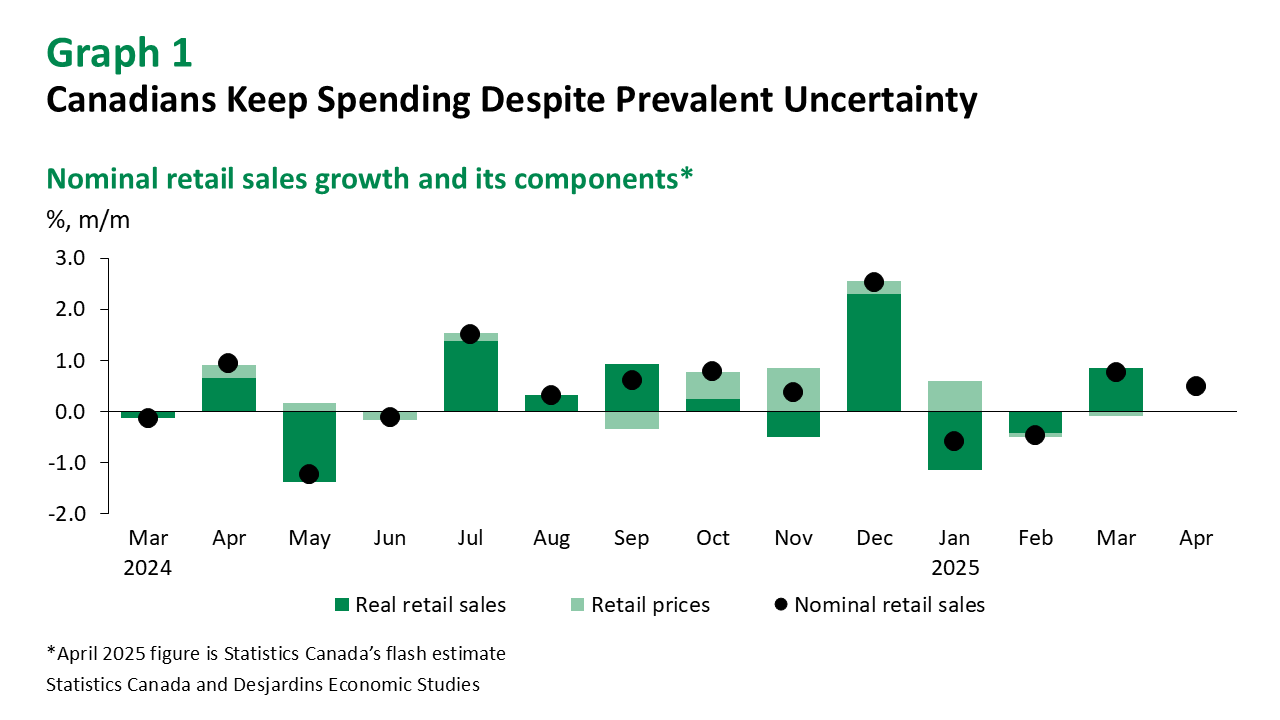

- Real retail sales were up 0.9% m/m, contrasting with declines in the first two months of the year (graph 1).

- Receipts at motor vehicle and parts dealerships, rebounding by 4.8% m/m (after two monthly declines), were the main driver behind the increase in nominal retail sales. While all subcategories advanced, the largest increase came from new vehicle dealerships (+5.2%). Excluding autos, nominal retail sales were down 0.7%.

- Sales at gasoline and fuel vendors dropped by 6.5% with both volumes and prices decreasing month-over-month.

- Core retail sales, which exclude gasoline and autos, increased for a second consecutive month, but at a moderate pace (+0.2%).

- Overall, nominal retail sales advanced 4.7% q/q annualized in the first quarter, while volumes grew by a much more sluggish 0.8%. This is much slower than Q3 and Q4 which were at roughly 6% in annualized real terms.

- Statistics Canada’s advance indicator for April points to surprising strength: +0.5% m/m. We expect this to be mainly the effect of volumes. That’s because retail sales receipts exclude taxes. Without the effect of changes in taxation (notably the carbon tax), seasonally adjusted retail goods prices were roughly flat in April.

Implications

Despite the disproportionate contribution of autos, the advance in retail sales in March was fairly broad based (6 of 9 subsectors posting gains), with gasoline a notable exception. Canadians increased spending on building material and garden equipment, clothing and accessories, furniture, furnishing, electronics and appliances. With talks of tariffs and counter-tariffs running high during March, some consumers may have purchased big-ticket items ahead of time, anticipating a future rise in prices of imported goods. The push to buy Canadian likely also boosted sales by domestic companies, as e-commerce sales by foreign-based retailers don’t play into Canada’s retail numbers. That patriotic zeal may have carried over into April as well.

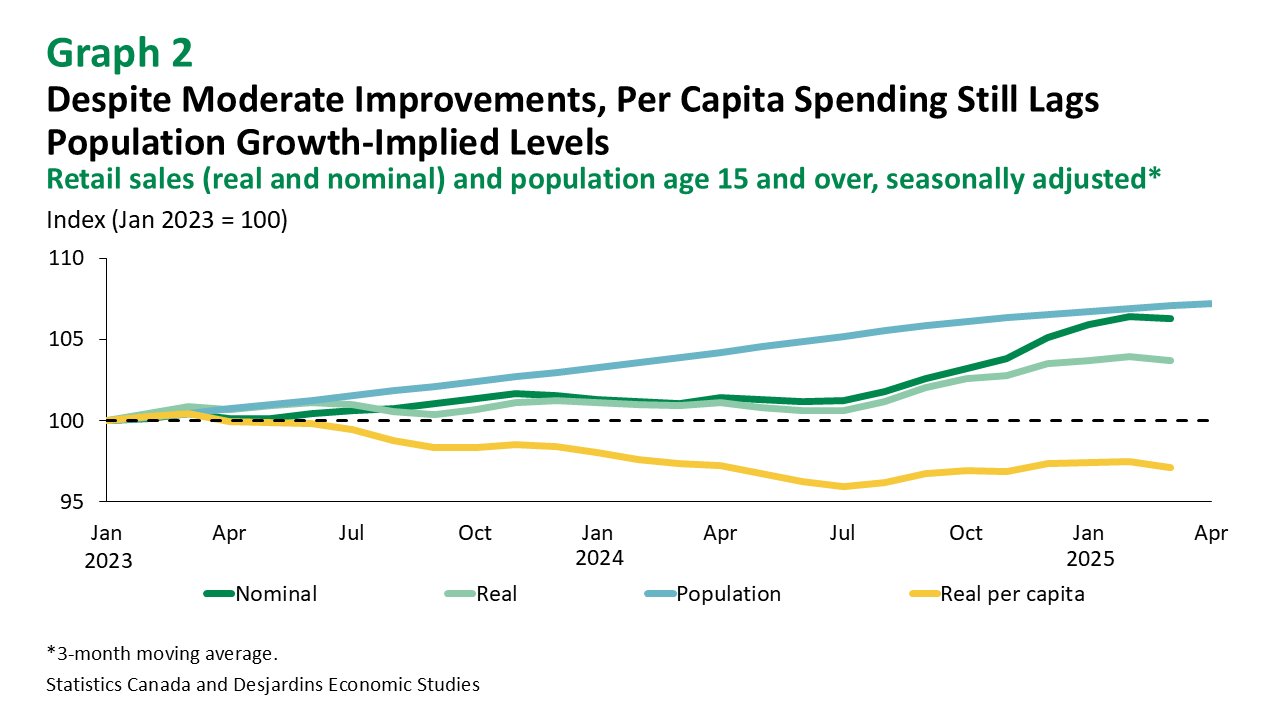

With the tentative de-escalation of trade tensions on the global stage recently, we could see moderate improvements in consumer confidence in the coming months. Still, we expect downside factors to continue to weigh on retail spending in the medium term, including an incoming wave of mortgage renewals at higher interest rates, job market weakness, and slowing population growth. Despite a gradual uptick since last summer, per capita spending is still lagging population growth-implied levels (graph 2).

After today’s release, our tracking for annualized real GDP growth in Q1 2025 is just shy of the Bank of Canada’s latest forecast of 1.8%. (See our latest Economic and Financial Outlook External link..) We expect the Bank to cut its policy rate by 25 points at its June meeting.