- Florence Jean-Jacobs

Principal Economist

Economic News

Canada: Retail Sales Remained Rangebound to End the Summer

October 23, 2025

Highlights

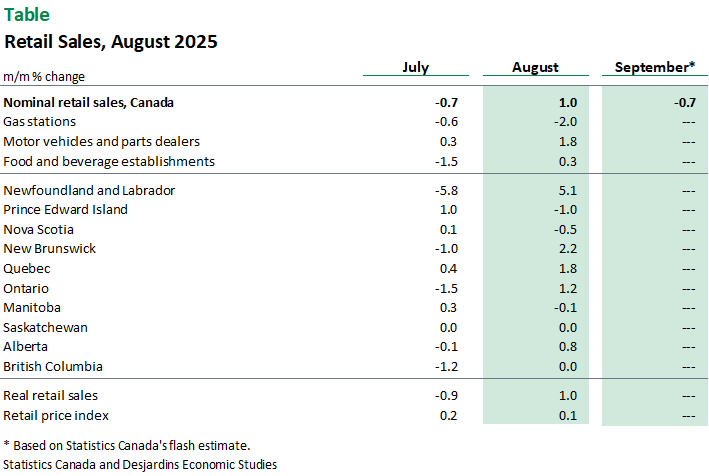

- Retail sales rose by 1.0% m/m in August, in line with the consensus of economists and Statistics Canada’s flash estimate (see table for details).

- Contrary to expectations, sales at motor vehicle and parts dealers increased (1.8%), with both new car dealers and used car ones contributing to the advance.

- Gasoline sales were down 2.0% due to lower volumes.

- Core retail sales, which exclude autos and gasoline, rebounded by 1.1% in August, following a roughly equivalent drop in July.

- Growth was evenly distributed, with 6 out of 9 categories and half of provinces posting gains. Quebec posted its strongest monthly advance this year and a third consecutive gain. Nova Scotia saw a 0.5% contraction, in a month marked by wildfire activity in the province.

- Real retail sales advanced 1.0% in August, erasing the prior month’s contraction.

- Statistics Canada’s preliminary estimate points to a decrease of 0.7% in September retail sales. If that proves correct, volumes likely dropped by 1.4%, given goods prices rose 0.7% over the month.

Implications

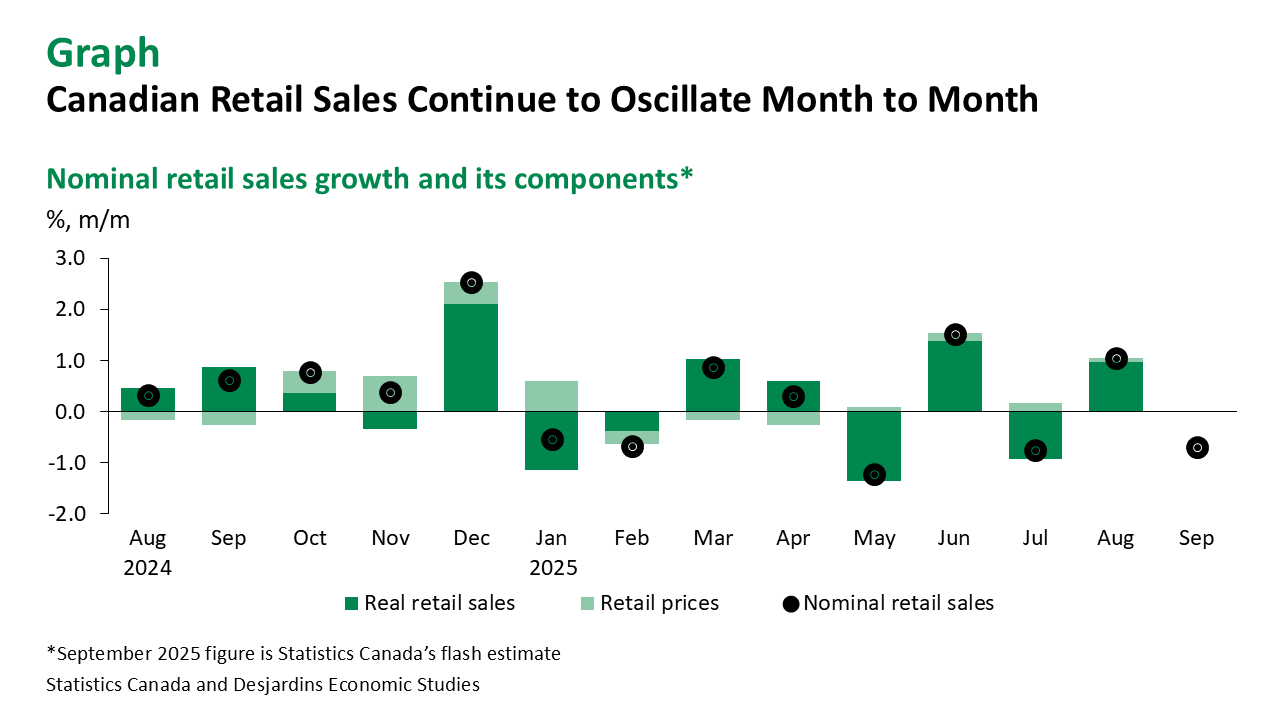

Since the beginning of the year, monthly variations in retail sales have been choppy and left receipts fairly rangebound (graph). It remains difficult to see a clear trend, except one of relative resiliency, in an environment otherwise marked by economic uncertainty and trade turmoil. That said, retail sales have done little to fill the gap left from weaker activity in trade-exposed sectors.

Although consumer spending is clearly not falling off a cliff, it has weakened in Q3. If September’s flash proves correct, nominal retail sales advanced by 1.2% q/q (seasonally adjusted and annualized) in Q3, a touch weaker than the 1.4% q/q in Q2 and significantly lower than 4.5% in Q1. But in real terms, Q3 growth was likely negative (-1.2%, based on the flash estimate).

As confirmed in the Bank of Canada’s Q3 consumer survey External link., uncertainty, elevated prices (due to past inflation) and the high cost of housing continue to weigh on consumer spending. We expect this to persist for the rest of the year.

The accompanying business survey External link. suggested some positives for retailers: after weakness in early 2025, sales outperformed retailers’ worst-case expectations, which respondents attributed to factors such as lower interest rates and gas prices, more domestic tourism (Canadian-resident return trips from the United States were down 29.7 % y/y in August), and consumers adapting to higher uncertainty. More businesses reported that their customers’ “Buy Canadian” spending behaviour boosted their sales.

After today’s release, our tracking for real GDP in Q3 is just a touch lower than the Bank of Canada’s 1.0% SAAR forecast. We still expect the Bank to proceed with a 25 basis point cut next week, despite the recent uptick in headline inflation External link..