- Kari Norman

Economist

Economic News

Canada: The First Increase in Four Months for Real GDP

September 26, 2025

Highlights

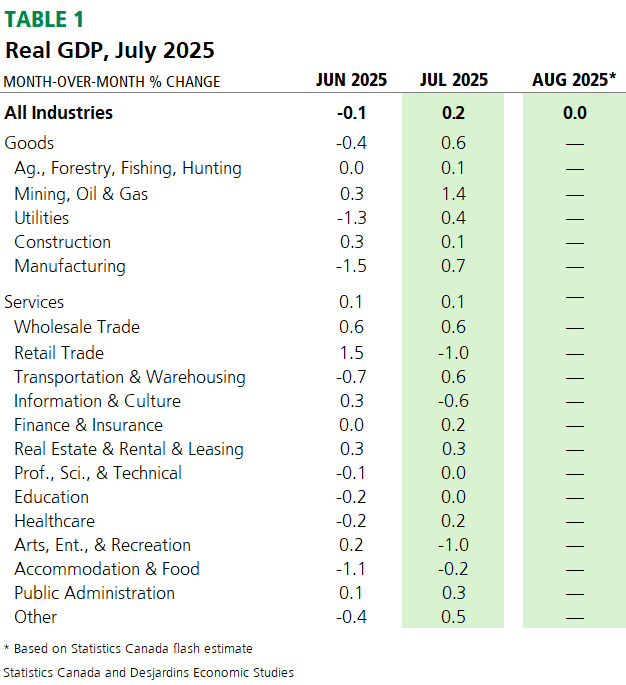

- Canadian real GDP rose by 0.2% in July 2025, after edging down the month prior. This was above the consensus of economic forecasters and Statistics Canada’s flash estimate. Eleven of 20 subsectors posted increases during the month. See Table 1 for further details.

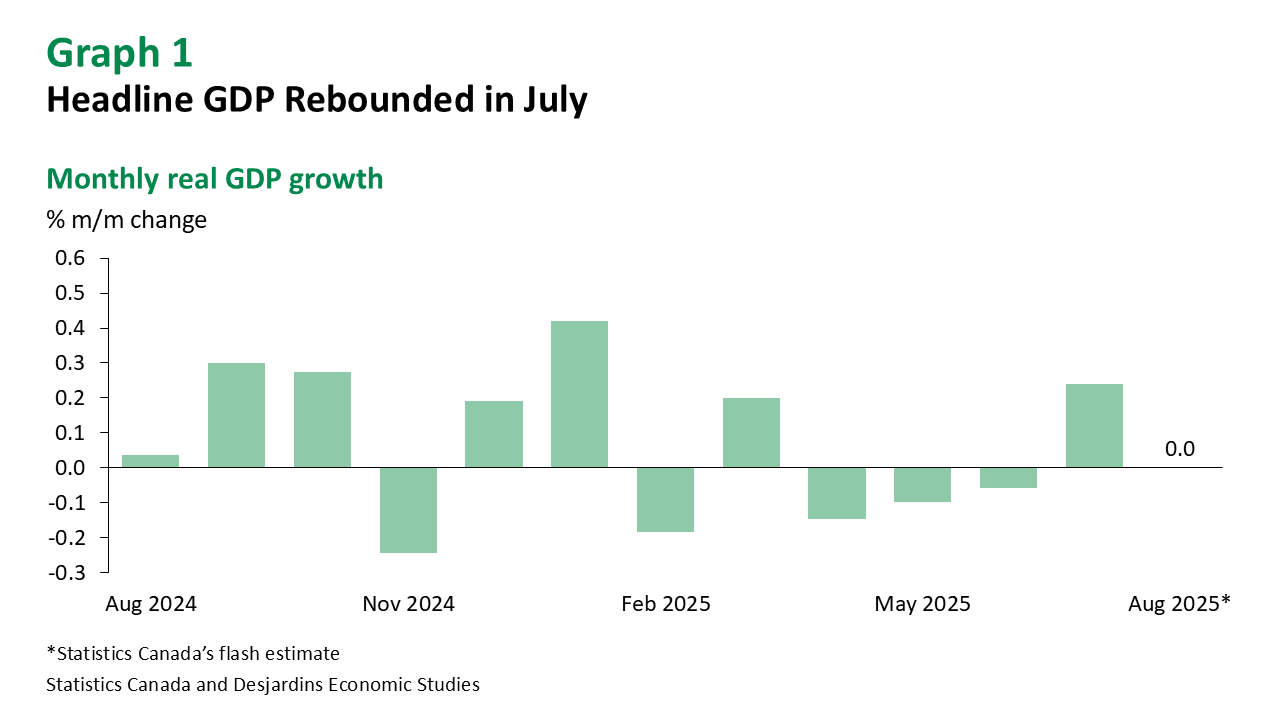

- Statistics Canada’s flash estimate points to no change in real GDP for August (graph 1).

Comments

July 2025’s rise in real GDP by industry nearly recouped all the losses in the previous three months. It was largely attributable to strength in goods-producing sectors, which rebounded with a 0.6% increase. All goods sectors grew in the month, a first since January. Strong gains in motor vehicle parts (+10.5%) and motor vehicle manufacturing (+9.1%) coincided with higher exports of motor vehicles and parts External link.. Mining and quarrying rose a strong 2.6% in the month after back-to-back declines. Oil sands extraction grew 1.2% following completion of retooling and maintenance activities in the spring.

The services sector saw a smaller advance, at 0.1%, with more mixed results among subsectors. Gains in wholesale trade, transportation and warehousing among others were mostly offset by declines in retail trade External link., arts and entertainment, information and culture, as well as accommodation and food. Hand-in-hand with increased oil and gas production in the goods sector came a solid 2.8% rise in pipeline transportation in the services sector, registering its strongest growth since September 2022.

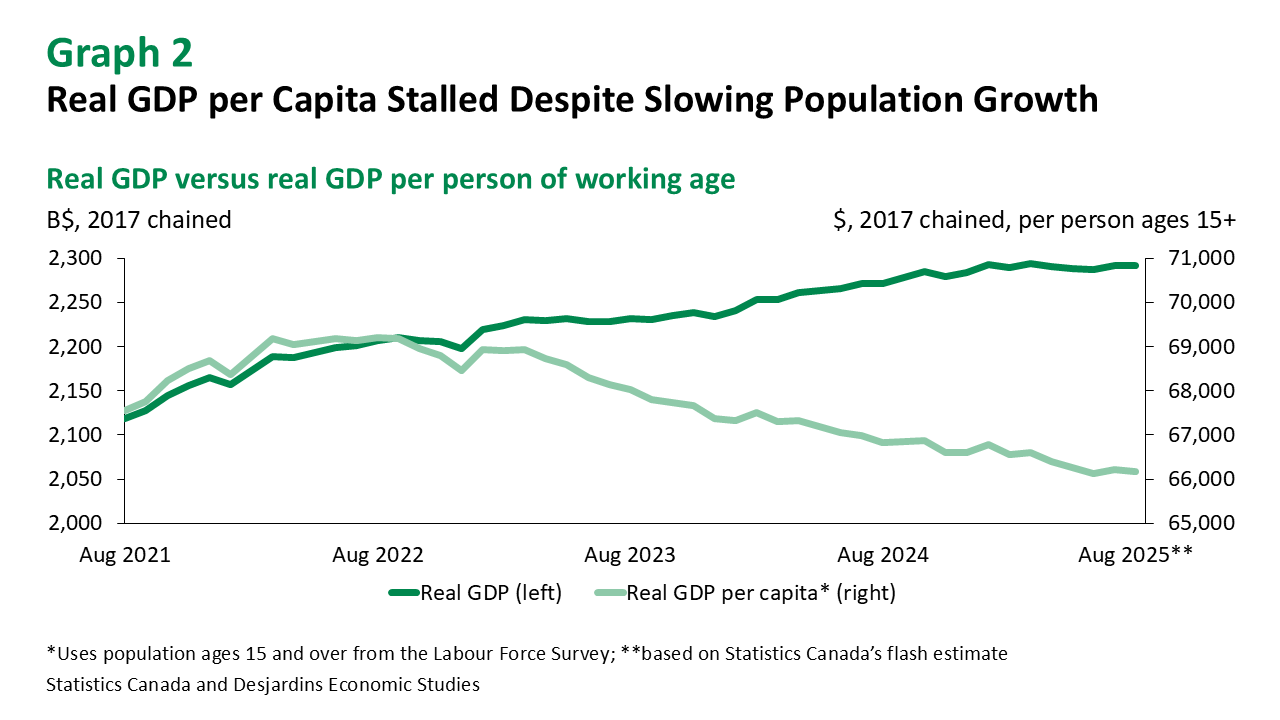

Despite strength in the month, GDP per capita has yet to show signs of returning to its pre-pandemic trajectory, even as population growth slows (graph 2). Immigration and non-permanent resident admissions have only eased for a few quarters—too brief to lift per-capita measures meaningfully—while the trade war’s drag on exports pushed GDP growth into negative territory in the second quarter.

Implications

Statistics Canada’s flash estimate for real GDP growth in August suggests gains in wholesale trade and retail trade were fully offset by weakness in mining, quarrying and oil and gas extraction; manufacturing; and transportation and warehousing. All this points to continuing slack in the economy. Domestic headwinds come in the form of slower population growth External link. and the summer’s back-to-back employment losses totalling over 100k External link.. Our recent analysis External link. on economic growth and projections suggest a relatively subdued outlook for Canada’s economy in the coming quarters. Until output consistently re-accelerates, trade headwinds fade and fiscal stimulus kicks in, GDP per capita will likely remain well below its peak.

The Bank of Canada lowered its policy rate External link. by 25-basis points to 2.50% last week, citing a softening labour market, diminished upward pressures on inflation, and the removal of most retaliatory tariffs External link.. We continue to anticipate that the Bank will cut the policy rate again at its upcoming October announcement, and that the rate will need to fall to 2.00% to support economic activity.