- LJ Valencia

Economic Analyst

Economic News

Canada: Solid Q1 Advance in GDP But There Are Turbulent Times Ahead

May 30, 2025

Highlights

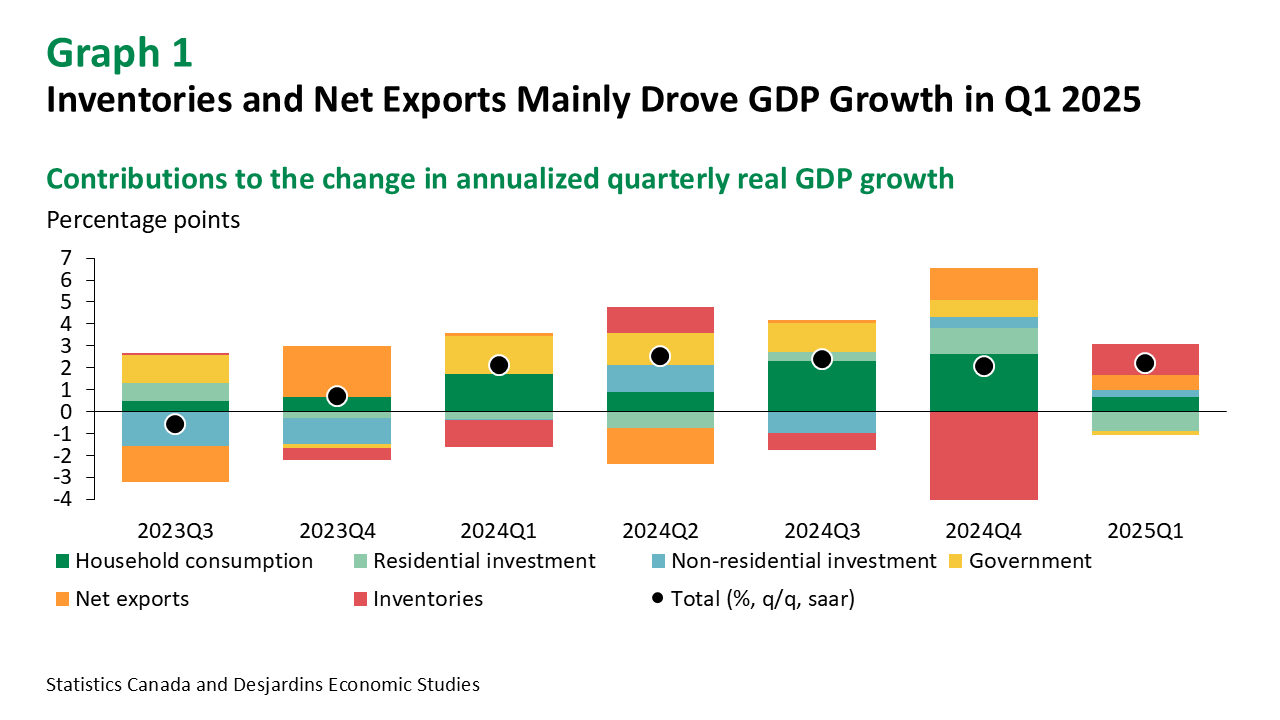

- Real GDP growth advanced at an annualized pace of 2.2% in Q1 2025. This was above the consensus of economic forecasters (1.7%) and the Bank of Canada’s (BoC’s) outlook (1.8%). Table 1 provides more details on the release.

- Monthly real GDP bounced back in March (0.1% m/m), in line with Statistics Canada’s flash estimate and consensus. Statistics Canada expects that real GDP by industry grew by 0.1% in April 2025. Early data and tracking indicate growth in between 0.5% and 1.0% in Q2 2025.

- Real GDP growth in Q4 2024 was revised down substantially to 2.1% annualized, from 2.6% previously, while monthly GDP growth had modest upward revisions in January and February of this year.

Implications

The new year began with solid Canadian real GDP growth for Q1. Under the hood, net exports added a modest lift with rising exports and imports coinciding with US tariff uncertainty (graph 1). Increased imports of aircraft and other transportation equipment and parts also led the gains in business investment in machinery and equipment. Despite growing trade activity during the quarter, there was a significant accumulation of business non-farm inventories after large withdrawals in the previous quarter. This was driven largely by increased wholesale trade inventories and, to a lesser extent, retail trade inventories.

Household spending slowed last quarter, as government supports such as the GST and HST tax holiday ended mid-February, and the job market showed signs of weakening. Residential investment was a meaningful headwind to growth last quarter as ownership transfer costs experienced the largest decline since Q1 2022. Business investment in non-residential structures fell with slumping investment from the oil and gas sector. The advance in compensation of employees slowed down ever so slightly this quarter from 3.4% to 3.2% annualized. As a result, the savings rate edged down to 5.7% from 6.0% in Q4 2024.

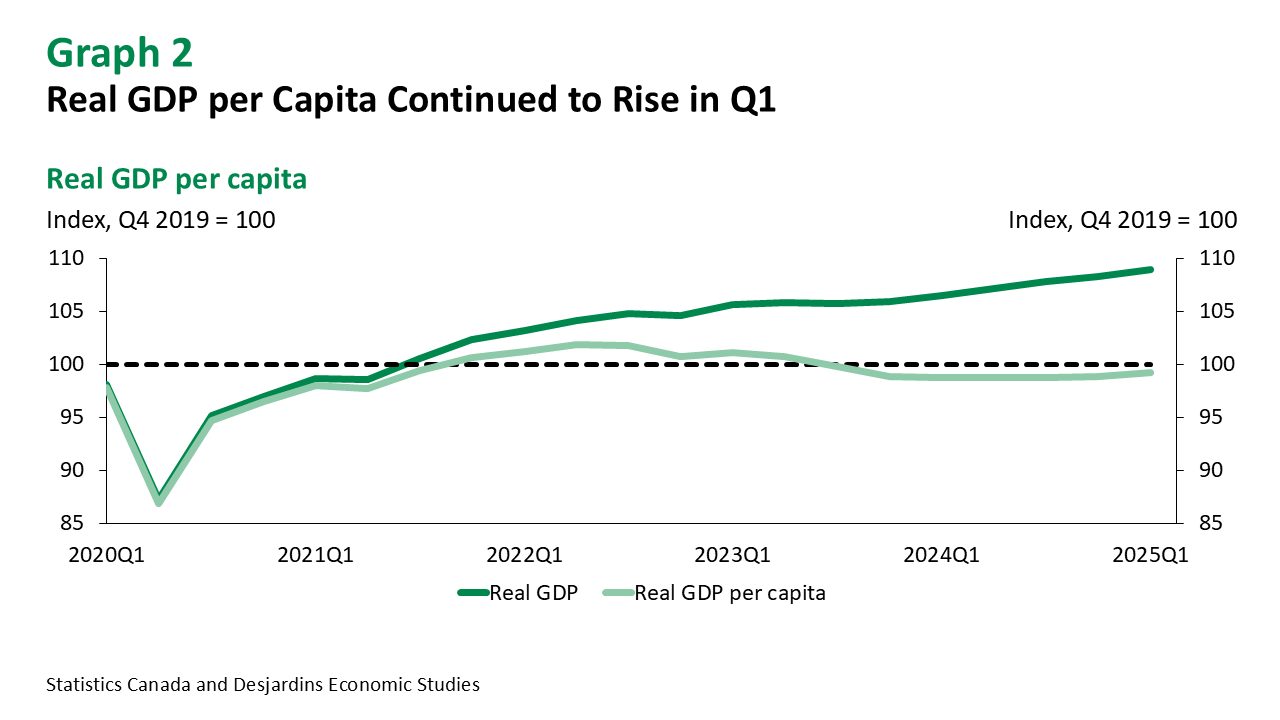

Thanks to strong GDP to start the year and the rapidly slowing pace of population growth, real GDP per capita rose again in Q1, reversing declines in previous quarters (graph 2). Overall, the economy started the year in relatively good terms, but that was largely due to the volatility tied to tariffs. Lastly, final domestic demand looked particularly weak.

The path appears turbulent coming into Q2. The economy faces significant headwinds from US tariffs, in addition to slower population growth, deteriorating labour market activity and the mortgage renewal wall. Despite a recent de-escalation of tariffs, the damage done may be too late to reverse. We anticipate economic growth to be subject more heavily to downside risk External link.. As such, we expect the Bank of Canada to cut rates by another 25 basis points next week.