- LJ Valencia, Economist

Economic News

Canada: Real GDP Fell in April and Another Drop in May Is Likely

June 27, 2025

Highlights

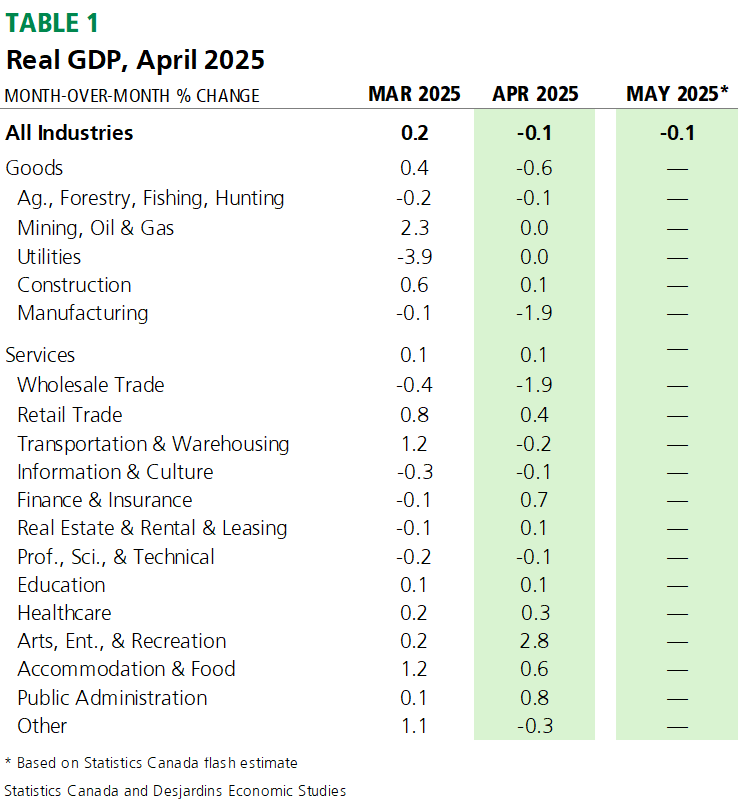

- Canadian real GDP fell by 0.1% in April 2025, following 0.2% growth in the prior month. This was one tick below the consensus of economic forecasters and two ticks below Statistics Canada’s flash estimate. Ten of 20 subsectors posted declines. See Table 1 for further details.

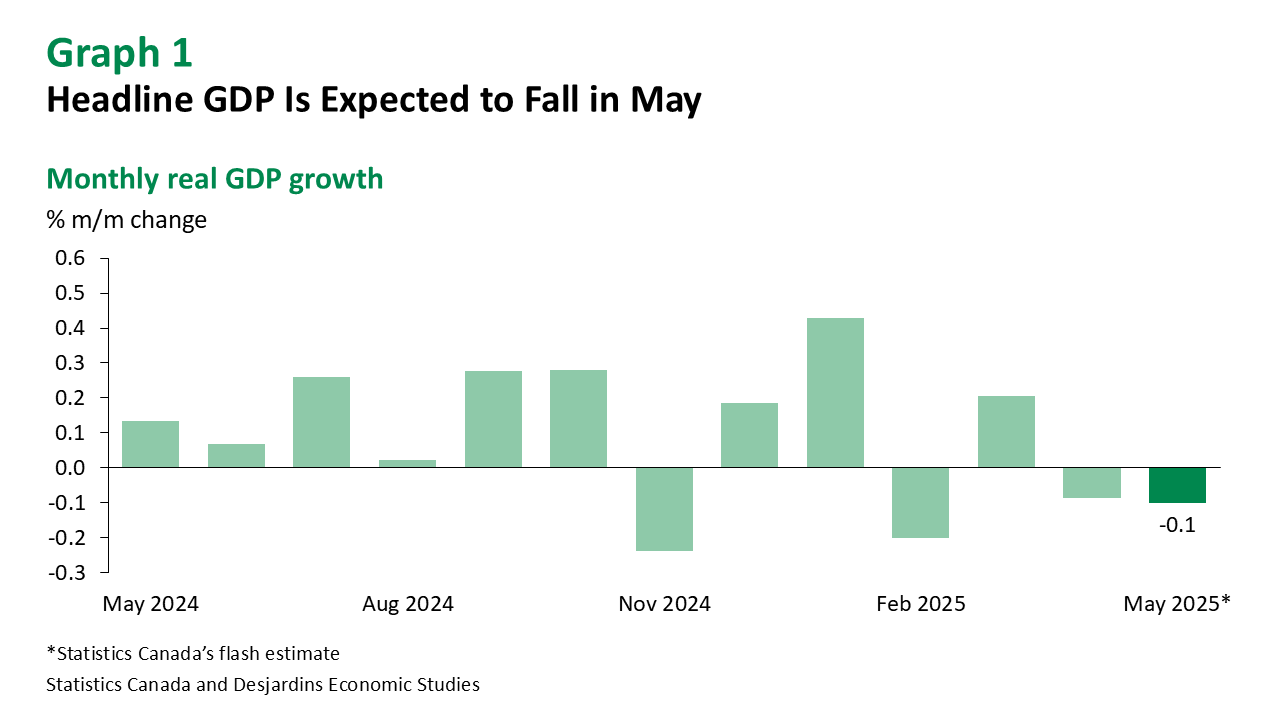

- Statistics Canada’s flash estimate points to another decline in real GDP of 0.1% in May (graph 1). This would imply a -0.3% annualized loss in real GDP by industry in the second quarter of 2025, assuming no change in June. This is in line with the forecast published in our June 2025 Economic and Financial Outlook External link..

Implications

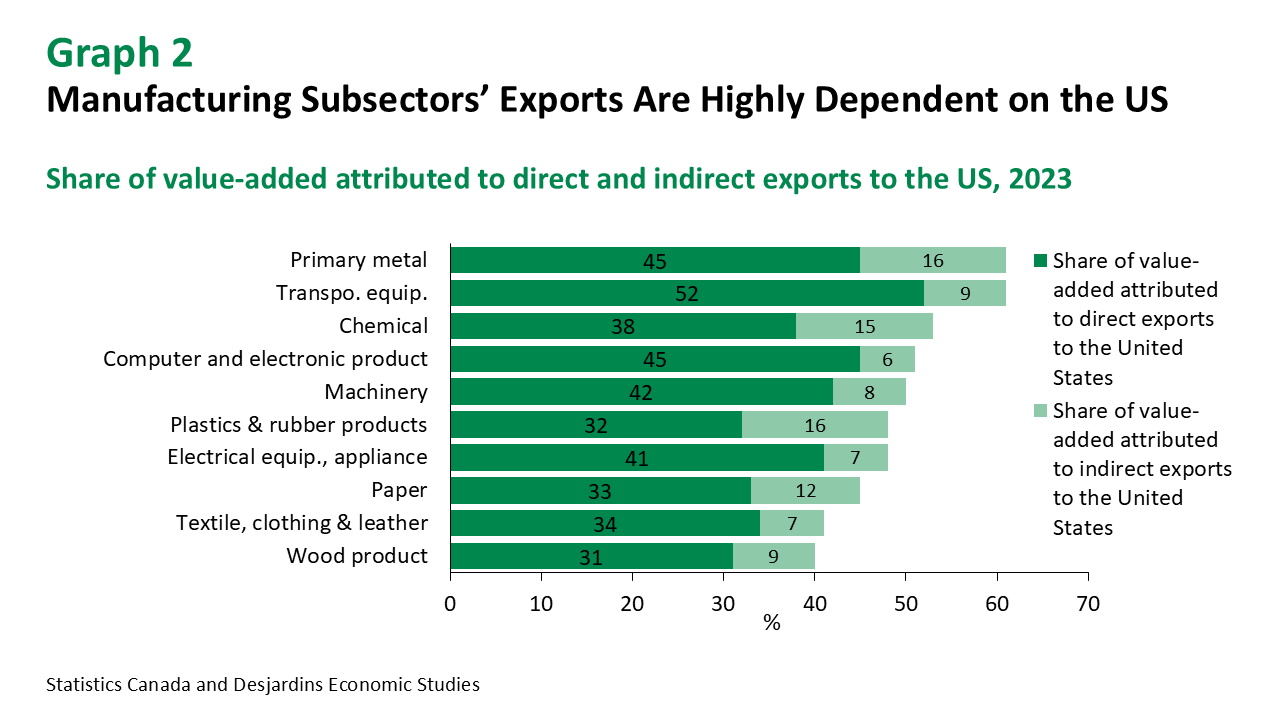

April 2025’s decline in real GDP by industry was largely attributed to significant weakness in goods-producing sectors. The manufacturing sector saw a broad and significant contraction—the deepest since April 2021. Declines in manufacturing output were particularly pronounced in transportation equipment and non-durable goods. Reduced exports of motor vehicles amid ongoing trade tensions with the US led some auto manufacturers to cut back on output. The manufacturing sector is especially sensitive to shifts in cross-border demand—Statistics Canada notes that over 40% of manufacturing output and employment are tied to the US market, with primary metal and transportation equipment manufacturing among the most exposed in terms of exports to the US (graph 2). Meanwhile, resource extraction was unchanged in April, as declines in oil, gas, and mineral extraction were balanced by gains in support activities.

While services experienced a modest bump in April, wholesale trade saw its steepest drop since June 2023. This was primarily due to reduced activity among motor vehicle and related goods distributors, reflecting diminished cross-border trade. In contrast, finance and insurance witnessed its sharpest increase since August 2024, in large part to trade tensions driving equity flows to Canada in the month. Lastly, the public sector posted a modest expansion, driven mainly by the federal election.

Looking ahead, Statistics Canada’s flash estimate for real GDP growth suggests weak manufacturing, wholesale and retail trade activity in May. That said, the recent Labour Force Survey External link. showed a relatively unchanged labour market in the month despite the trade war.

Signs indicate that the economy is weakening due to escalating trade tensions with the US. In addition, slower population growth and the mortgage renewal wall hitting Canadians this year are extra sources of economic headwinds, albeit somewhat offset by planned federal infrastructure External link. and defence External link. spending. Our recent analysis External link. on economic growth and projections also suggest a relatively subdued outlook for Canada’s economy in the coming quarters. The recent inflation data External link. point to modest price growth ahead as well. As such, we are of the view that the Bank of Canada will resume its rate cutting cycle in July.