- LJ Valencia, Economist

Economic News

Canada: Real GDP Fell Again in May but Rebounded in June

July 31, 2025

Highlights

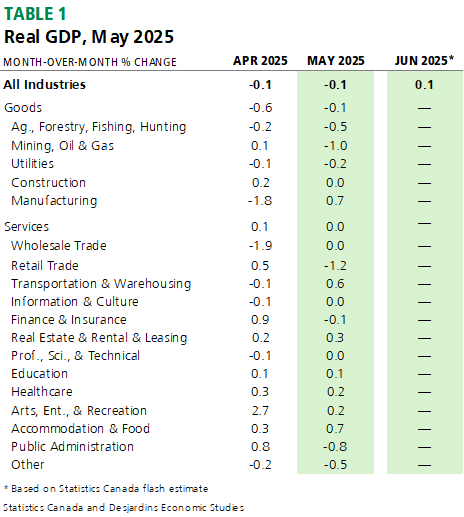

- Canadian real GDP fell by 0.1% in May 2025, following a similar decline in the prior month. This was in line with the consensus of economic forecasters and Statistics Canada’s flash estimate. Only seven of 20 subsectors posted increases during the month. See Table 1 for further details.

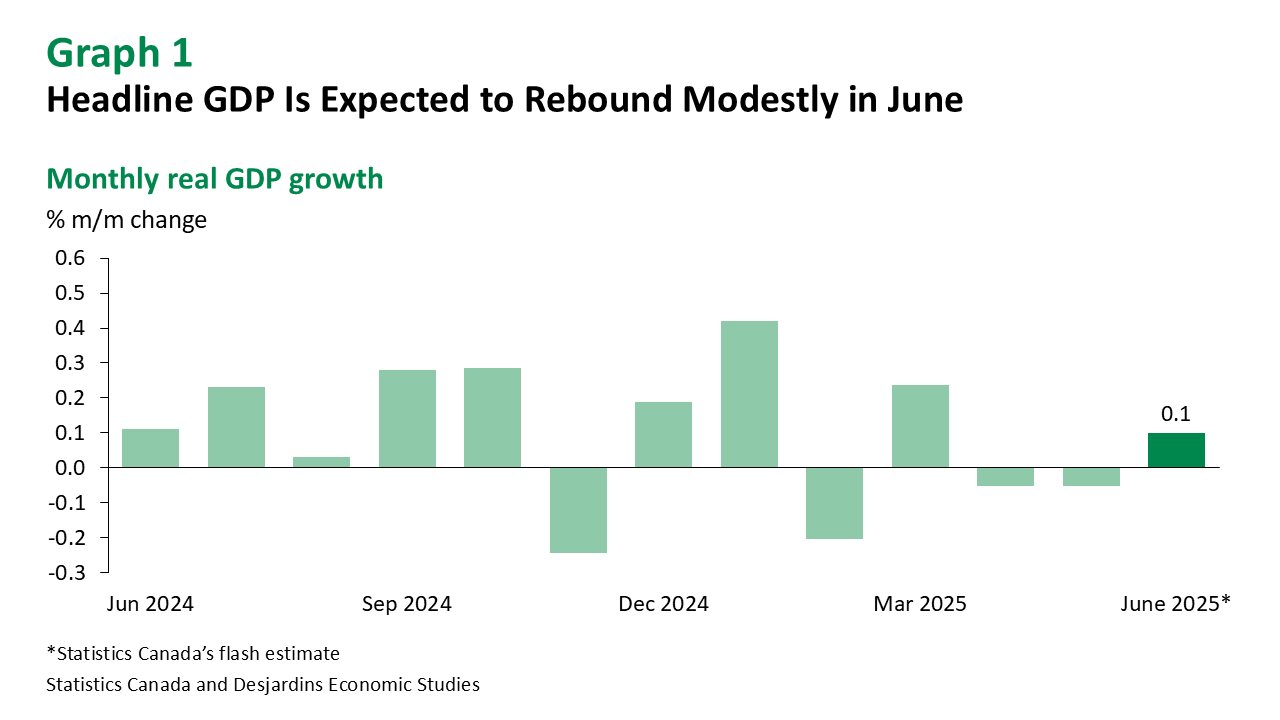

- Statistics Canada’s flash estimate points to a 0.1% rise in real GDP for June (graph 1). This would imply a 0.1% annualized growth in real GDP by industry in the second quarter of 2025.

Implications

May 2025’s decline in real GDP by industry was largely attributed to ongoing weakness in goods-producing sectors. The manufacturing sector saw a rebound, somewhat offsetting the broad contraction from the prior month. This was the third increase in five months, with gains posted in both the durable and non-durable goods manufacturing. However, these gains came on the back of significant inventory accumulation, not increased sales activity. Indeed, Statistics Canada notes that manufacturing sector activity was 1.1% below the March level when US tariffs came into effect—a worrying sign for Canadian manufacturers. Meanwhile, Resource extraction led the goods sector decline, driven by reduced mining and lower oil and gas activity due to maintenance and turnaround work.

On the other hand, the services sector saw no change in the month with varying gains and losses observed across subsectors. The transportation and warehousing sector posted gains, driven by higher activity in rail, pipeline, and other transportation services. Real estate, rental and leasing also rose supported by higher activity in the home resale market. Meanwhile, arts, entertainment, and recreation experienced a notable boost, largely due to three Canadian NHL teams advancing to the second round of the playoffs—marking the first time this has occurred since 2004. In contrast, retail trade saw a significant contraction, motivated by weaker motor vehicle sales. Lastly, the public sector fell following increased activity from the Canadian federal election in April.

Looking ahead, Statistics Canada’s flash estimate for real GDP growth suggests gains in retail and wholesale trade being partially offset by weaker manufacturing sector activity. The recent Labour Force Survey External link. signals a similar trend, with job gains in private services and softening labour demand in goods-producing sectors.

All this points to building slack in the economy as a result of trade tensions with the US. Domestic headwinds come in the form of slower population growth and the mortgage renewal hitting the Canadian economy this year. The planned federal infrastructure External link. and defence External link. spending could provide some offset. But our recent analysis External link. on economic growth and projections suggest a relatively subdued outlook for Canada’s economy in the coming quarters. The Bank of Canada held its policy rate External link. steady at 2.75% yesterday, citing persistent inflationary pressures. However, we are of the view that the Bank of Canada will resume its rate cutting cycle in September as fears about inflation subside.