- LJ Valencia

Economic Analyst

Economic News

Canada: August GDP Was All Trick but With Some Treat in September

October 31, 2025

Highlights

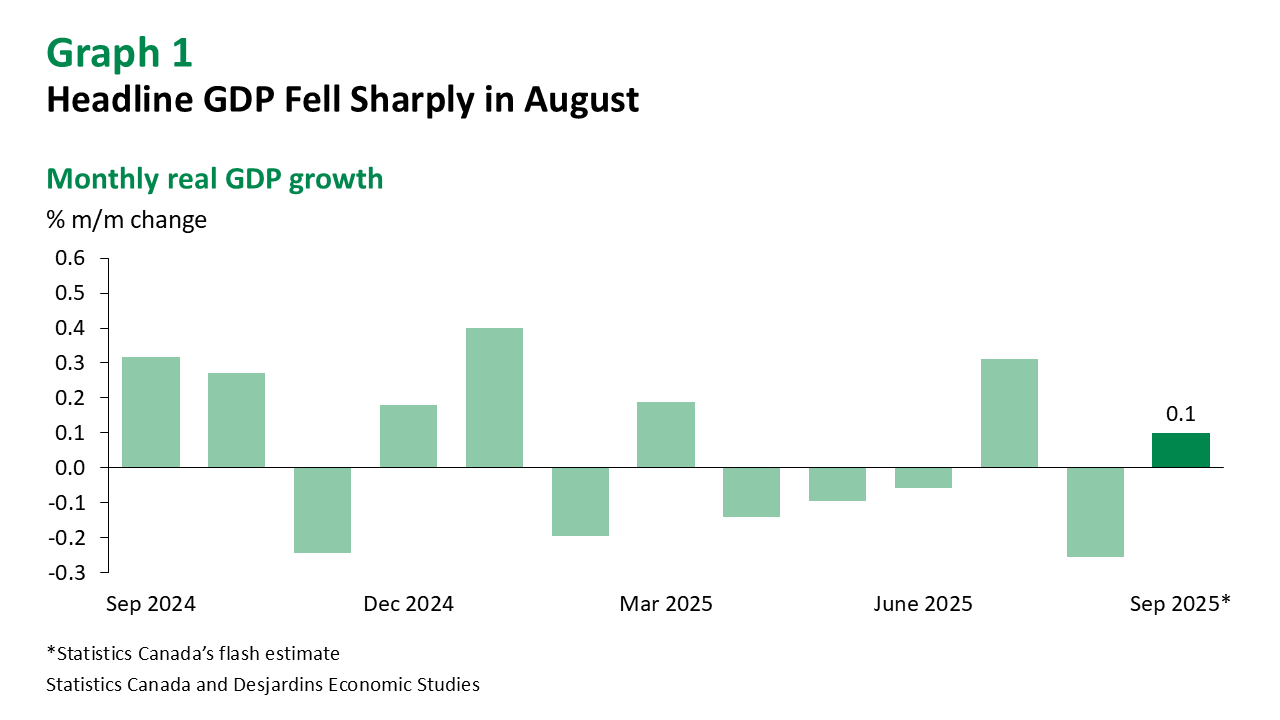

- Canadian real GDP fell by 0.3% m/m in August, offsetting most of the gains from the prior month. This was far below the consensus of economic forecasters and Statistics Canada’s flash estimate. Declines were observed in both goods-producing and services-producing industries. See Table 1 for further details.

- Statistics Canada’s flash estimate points to a 0.1% increase in real GDP for September (graph 1).

Comments

August’s sharp decline in real GDP came as a big surprise to forecasters, offsetting most of the gains made in July. The decline was driven by weakness in goods-producing industries at -0.6% m/m, marking their fifth drop since the beginning of the year. The manufacturing sector saw contractions in durable and non-durable manufacturing, though gains in primary metal manufacturing helped offset some of the losses. Utilities fell due to reduced hydroelectric output amid worsening drought conditions. Mining and quarrying also declined, led by lower metal ore and coal production. In contrast, oil and gas extraction rose for a third consecutive month, supported by increased crude oil extraction in Alberta and Newfoundland and Labrador.

The services sector posted a modest contraction, at -0.1%. While retail trade External link. recorded gains, these were mostly offset by declines in transportation services and wholesale trade, which fell for the first time in four months. Air transportation posted its steepest decline since January 2022, primarily reflecting disruptions caused by the flight attendants’ strike.

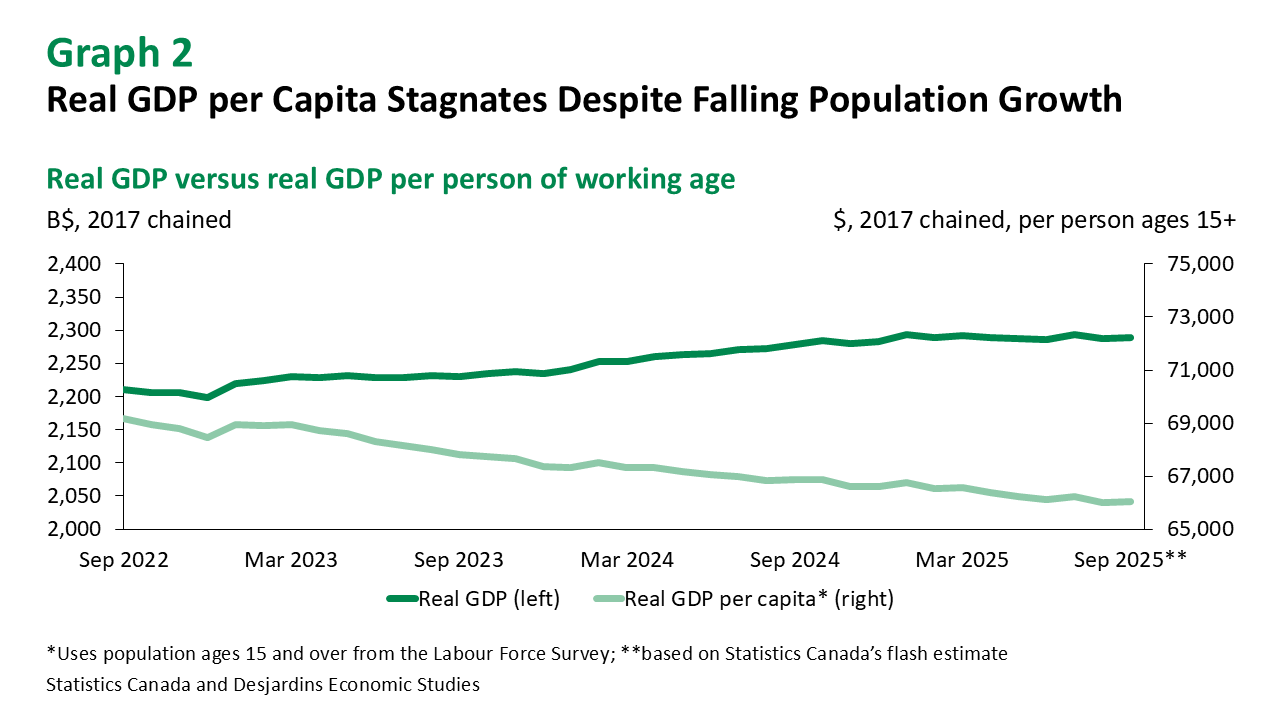

Given the economic weakness in the month, GDP per capita remains on a downward trajectory, showing no clear signs of recovery even as population growth slows (graph 2).

Implications

Statistics Canada’s flash estimate for real GDP growth in September suggests gains in finance and insurance; mining, quarrying, and oil and gas extraction; and manufacturing were partially offset by weakness in wholesale and retail trade. Given the new GDP data, our tracking framework suggests the economy would grow at an annualized pace of about 0.5% in the third quarter, in line with the Bank of Canada’s latest projection.

While this suggests Canada will avoid a second consecutive contraction, the economy remains weak as it continues to face significant headwinds from slower population growth External link. and trade tensions. The path ahead remains precarious, especially given uncertainty surrounding the upcoming CUSMA review. That said, the removal of most retaliatory tariffs External link. should offer some relief by supporting growth and lowering inflation.

The Bank of Canada lowered its policy rate External link. by 25‑basis points for the second consecutive meeting to 2.25% this week, citing a soft labour market and weak economic growth. However, the trade war’s impact on Canada’s productive capacity prompted it to refrain from signalling further cuts, barring data disappointment. There are limits to what rate cuts can accomplish in the face of a structural economic shock. Today’s GDP data is broadly in line with the Bank’s latest forecast, and therefore, does not move the monetary policy needle.