- LJ Valencia

Economic Analyst

Economic News

Canada: February GDP Declines on the Back of Bad Weather and Tariff Uncertainty

April 30, 2025

Highlights

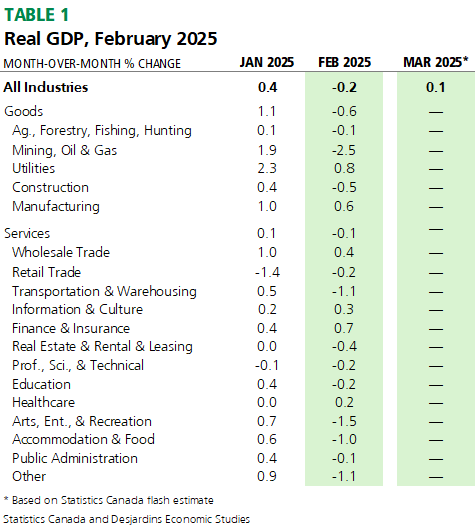

- Canadian real GDP fell by 0.2% in February 2024, following a 0.4% growth in the prior month. This was two ticks below the consensus of economic forecasters and Statistics Canada’s flash estimate. Twelve of 20 subsectors posted declines. See Table 1 for further details.

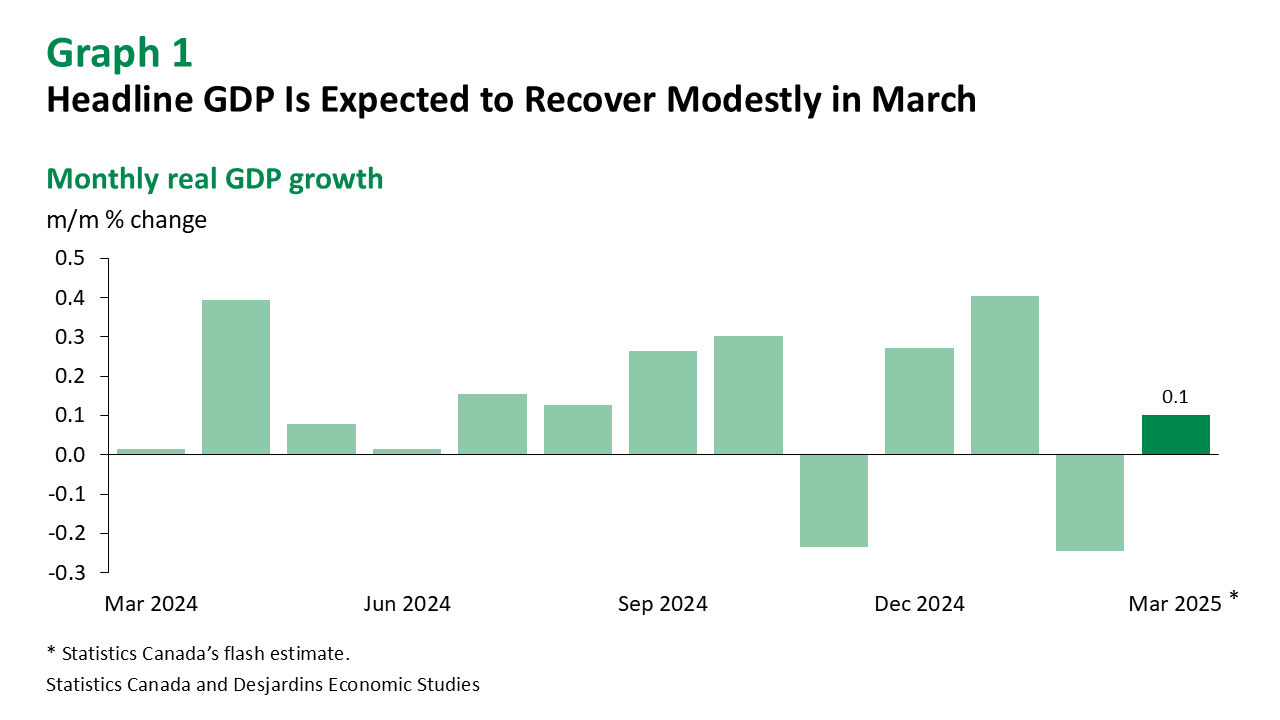

- The flash estimate points to growth of 0.1% in March (graph 1). This would imply a 1.5% annualized gain in real GDP by industry in the first quarter of 2025.

Implications

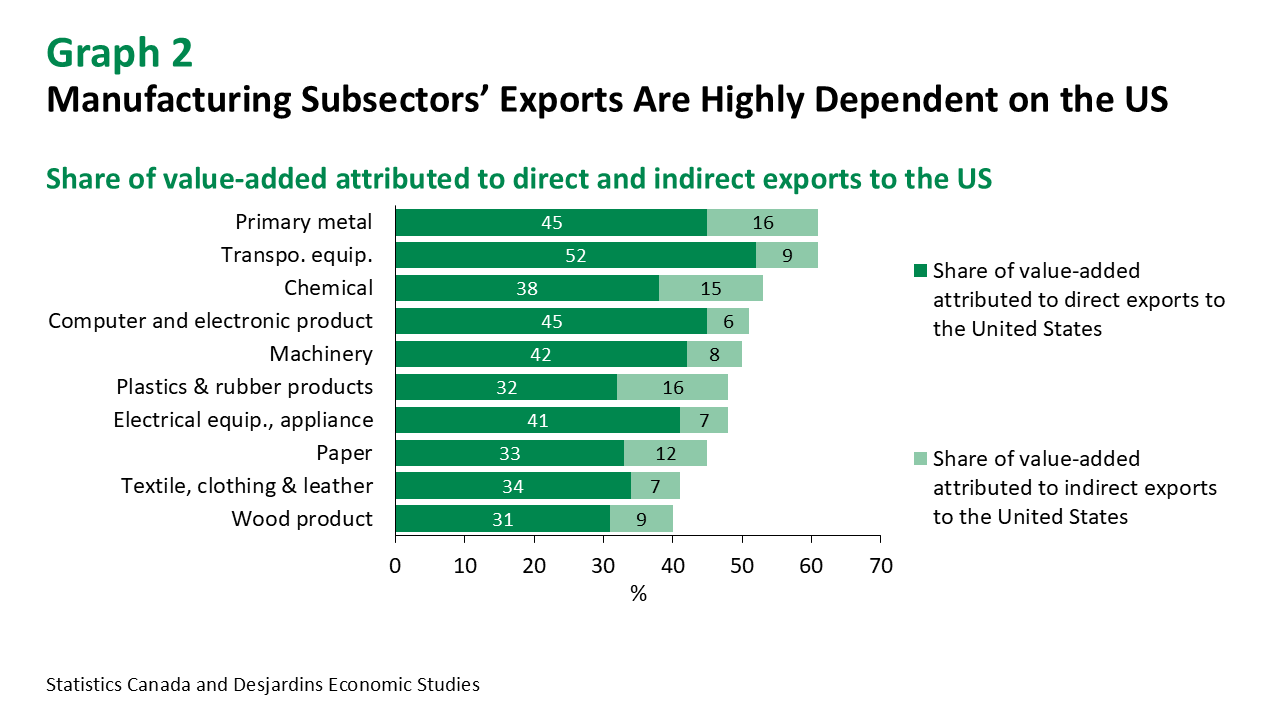

February 2025’s decline in real GDP by industry was primarily attributed to weather-induced weakness in goods-producing sectors. Resource extraction contracted due to lower activity in oil sands extraction, mining and quarrying. Construction also declined for the first time in four months driven by a broad slowdown in building activities. In contrast, the manufacturing sector rose for a second consecutive month, driven by higher production of motor vehicle parts and machinery. This may have reflected manufacturers trying to get ahead of US tariffs being imposed on Canadian exports. According to Statistics Canada, the manufacturing sector is among the most exposed industries to the US market, relying on US demand for more than 40% of its output and employment. Primary metal and transportation equipment manufacturing are particularly vulnerable (graph 2).

In the services sector, real estate posted its largest decline since April 2022, a worrying sign of slower housing market activity. Adverse weather across Canada caused transportation and warehousing services to fall after two consecutive monthly gains. While finance and insurance services rose for a third consecutive month, this rise appears to have been driven by escalating trade tensions and a significant divestment of Canadian securities from non-residents, not exactly a positive sign of things to come.

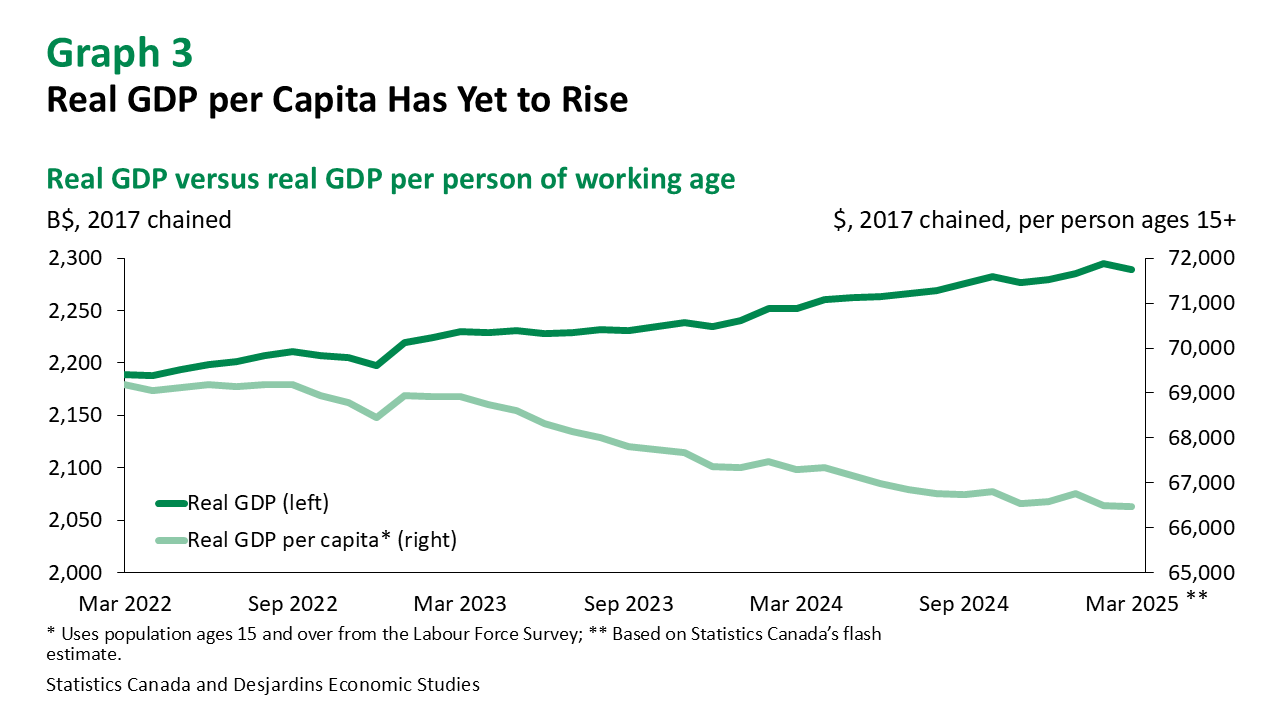

Looking ahead to March, the recent Labour Force Survey External link. showed further signs of softening in the job market. This corresponds to the weak flash estimates for real GDP, manufacturing and wholesale trade, albeit offset by a solid retail print anticipated in the month. Note that our latest outlook for real GDP by expenditure shows growth broadly in line with the Bank of Canada’s Q1 projection of 1.8% in the April Monetary Policy Report. Regardless, real GDP continued to lag population growth in the first quarter (graph 3).

While the weak February real GDP data was heavily influenced by adverse weather conditions, this shouldn’t lead to a sense of complacency. Under the hood, there are signs the economy is responding adversely to escalating trade tensions with the US. In addition, there are other downside risks posed by slower population growth and the impending wall of mortgage renewals about to hit Canadians this year. Consequently, we’re projecting External link. a mild recession in 2025, possibly starting as early as Q2. And with recent inflation data External link. pointing to slower price growth ahead, we are of the view that the Bank of Canada will resume its rate cutting cycle in June.