- Laura Gu

Senior Economist

Economic Viewpoint

Provinces Stand on Uneven Ground amid Shifting Trade Winds

June 3, 2025

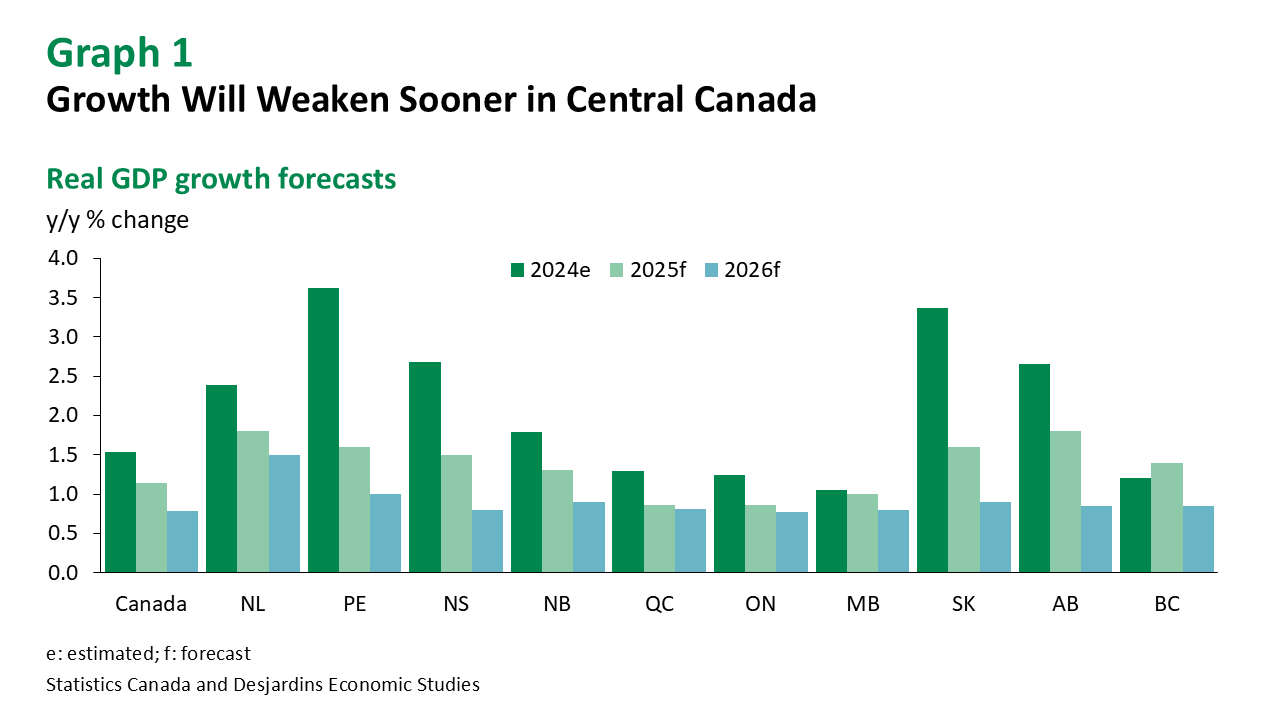

Canada’s economic outlook has improved modestly since “Liberation Day” as global trade tensions have de‑escalated. However, the benefits are not evenly distributed across industries and regions. The manufacturing, agriculture and transportation sectors remain under pressure, weighing on central Canadian provinces (graph 1). In contrast, the resource sector—particularly energy—continues to buoy growth in western provinces, as well as Newfoundland and Labrador.

Housing market dynamics are contributing to regional imbalances. Ontario and British Columbia are grappling with significant oversupply, driven by slowing population growth and weaker sentiment. Meanwhile, housing markets in other provinces remain more balanced, though broader economic uncertainty is expected to keep activity subdued nationwide.

Provincial governments are leaning on expansionary fiscal policy to support growth. Budgets remain in deficit as spending on healthcare, infrastructure and targeted tax relief—particularly Alberta’s income tax reform—continues. These measures should help offset some of the private sector weakness and support household demand.