- LJ Valencia, Economist

Economic News

Productivity in Q3 Rebounded Amidst Tariffs and Uncertainty

December 3, 2025

Highlights

- Business sector labour productivity bounced back sharply in Q3 2025, up 0.9% q/q (non-annualized) following a 1.0% decline in the prior quarter.

- Real GDP for the business sector increased by 0.9% in the third quarter, after falling by 0.8% in the second quarter, driven primarily by output growth in goods-producing sectors (1.0%).

- Hours worked in the business sector fell slightly (-0.1%) in Q3, after growing for two consecutive quarters. This is only the second time hours worked fell within the last 5 years.

- Unit labour cost (ULC)—the cost of labour per unit of output—of Canadian businesses posted a 0.9% gain in the quarter, a slower pace than in Q2 but in line with the average of the past two years.

Comments

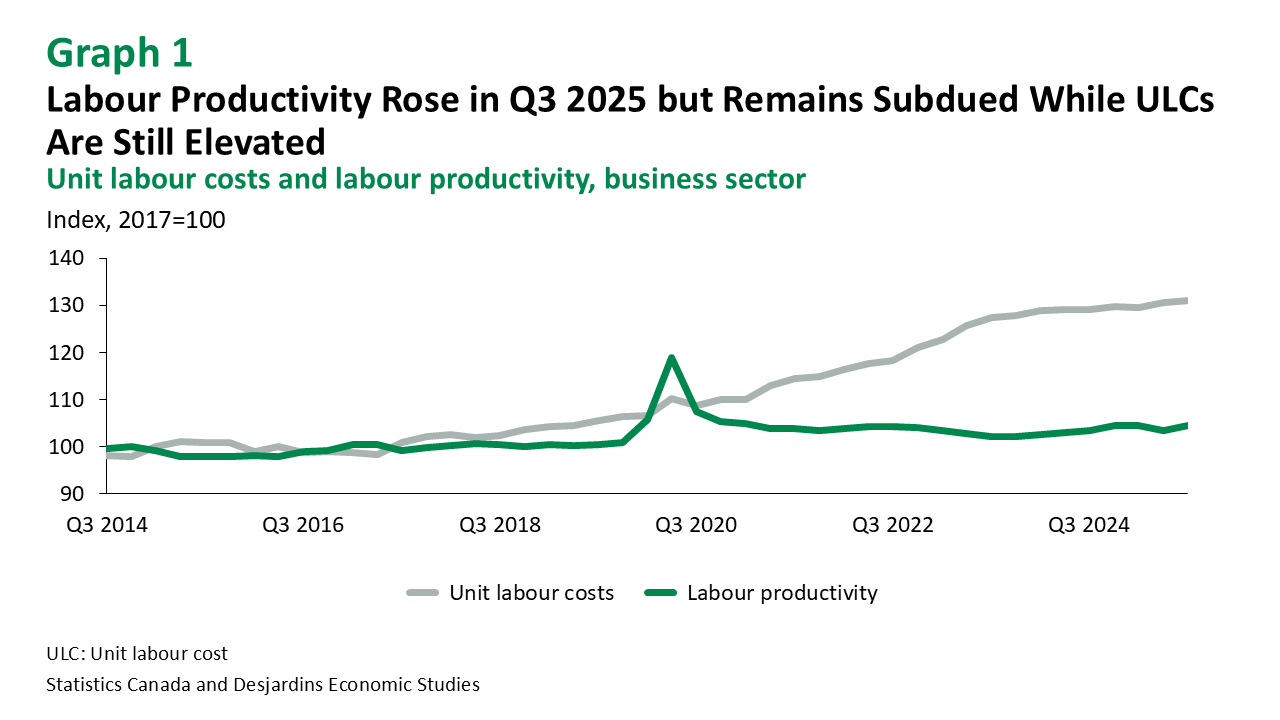

Labour productivity rebounded following a significant decline in Q2, largely trigged by the trade war. Still, this rebound follows a long period of poor productivity (graph 1). While the slowdown in ULC growth is a positive sign, high ULCs continue to eat away Canada’s competitiveness relative to the US.

Monthly data for hours worked show early signs of deceleration in Q4. However, assuming real GDP growth is in line with Statistics Canada’s flash estimate, this could imply declining productivity in Q4 2025. Wage growth also continues to rise, albeit more slowly, suggesting that unit labour costs remain high for businesses (graph 1).

Implications

Today’s productivity numbers come with a lot of caveats. The bulk of productivity gains came from goods-producing sectors, partly motivated by falling hours in trade-impacted industries. In addition, business sector labour productivity slightly fell since the beginning of the year (-0.1%). And this comes against a backdrop of US tariffs hitting economic activity and business investment.

Looking ahead, the federal government’s new immigration policies External link. should slow population growth further, providing some room for productivity to rise in the future. Still, uncertainty due to the trade war should define the near-term trajectory of Canadian business investment and productivity, with the outcome of next year’s CUSMA review being a potentially critical turning point. Despite this, we expect productivity growth to accelerate over the medium term.