- Kari Norman

Economist

Economic News

Canada: Population Growth Continued to Slow—but Not Enough to Meet the NPR Target

September 24, 2025

Highlights

- Canada’s population grew marginally from April 1 to July 1, 2025, increasing by only 47k to nearly 41.7M.

- The 0.9% year-over-year increase was the smallest since 2016, outside of the pandemic. Table 1 summarizes key data points.

Comments

Canada’s population growth remained subdued in Q2 2025, continuing the slowdown that began late last year. The sharp decline in net non-permanent residents (NPRs) continued, at nearly 59k. NPRs now account for 7.3% of the population, down from a peak of 7.6% in Q4 2024. At the same time, immigration remained in line with the previous two quarters. Desjardins Economic Studies’ internal research corroborates Statistics Canada’s statement that “the number of immigrants welcomed in the second quarter of 2025 (103,507) is in line to meet the 2025–2027 Immigration Levels Plan of Immigration, Refugees and Citizenship Canada.” However, the number of NPRs isn’t falling fast enough to meet the federal government’s target of 5% of Canada’s population after 3 years.

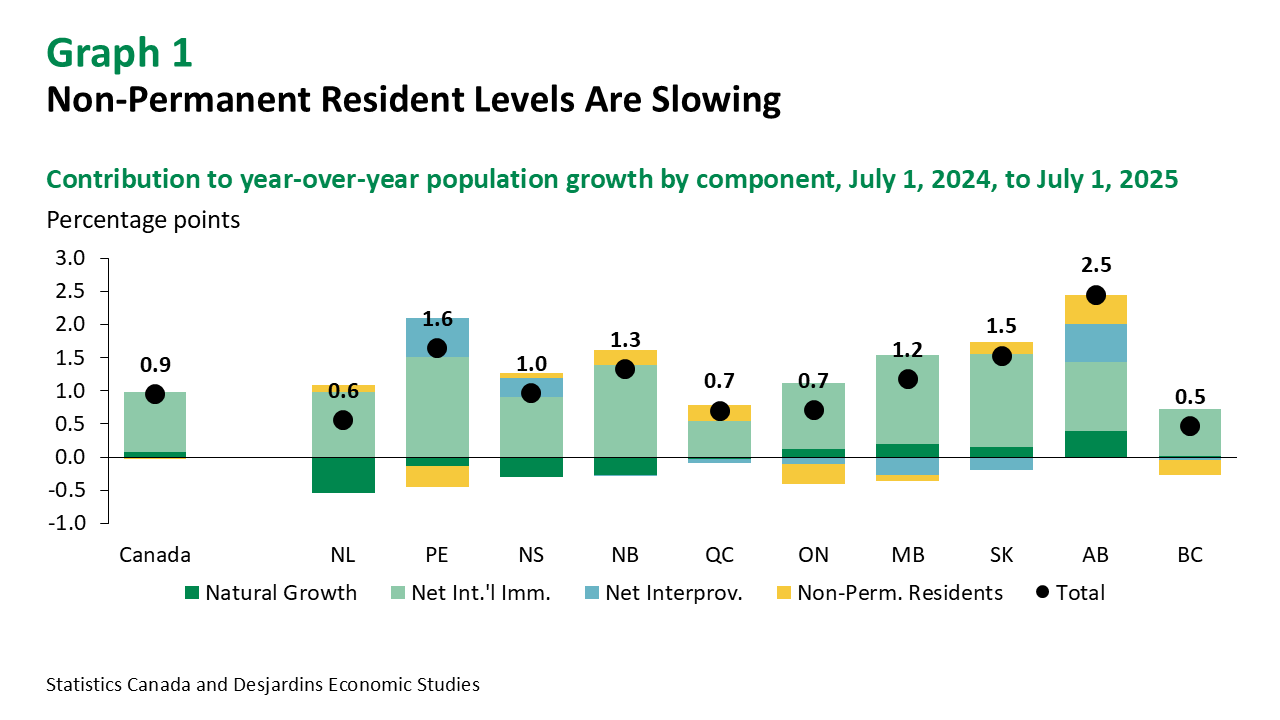

BC was the only province to see its population decline from April 1 to July 1, 2025, although it remained higher than a year ago (graph 1). The losses of NPRs was concentrated in two provinces, Ontario (-37k) and BC (-17k). This is likely to weigh heavily on their respective housing markets External link., particularly demand for rental accommodation and investor demand for condo construction. Quebec’s population increased by 17.1k in the quarter, primarily due to higher net immigration (+17.4k). Net NPRs reversed the decline of the previous two quarters, advancing by 1.5k, but the province lost 2.5k people to net interprovincial outflows.

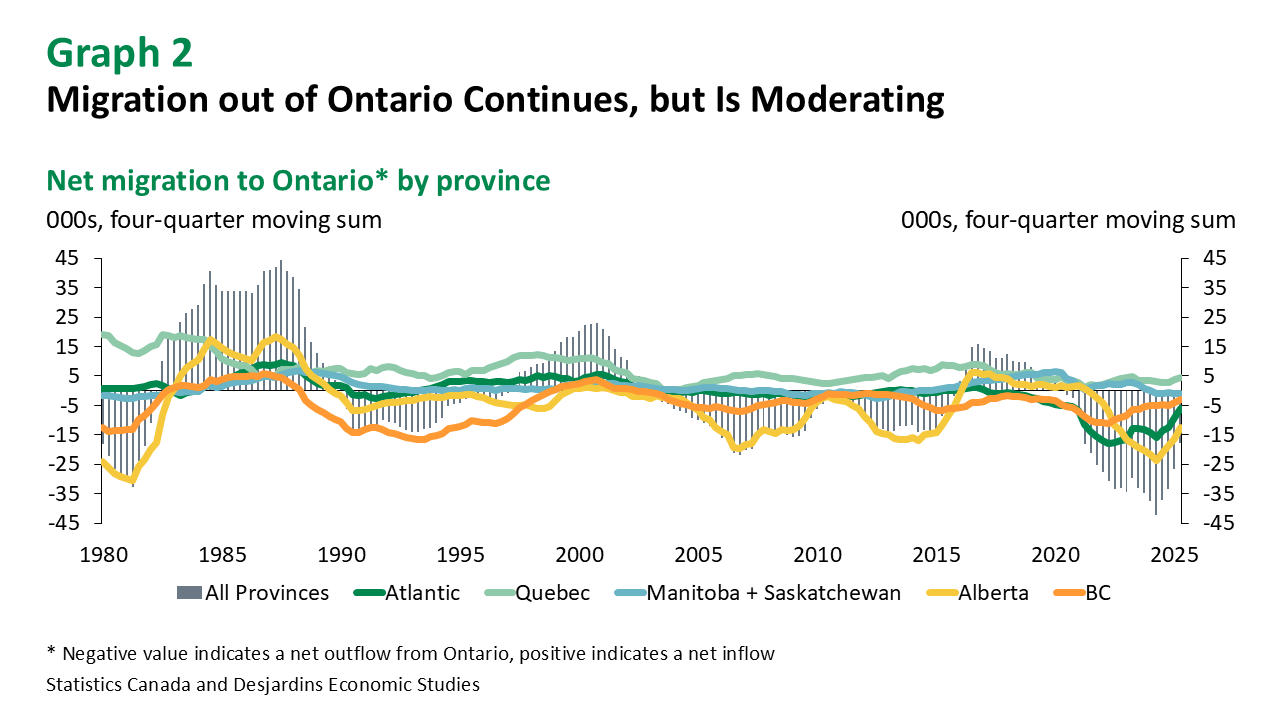

Net interprovincial migration out of Ontario continued (graph 2). Over the past year, Alberta remained the top destination, followed by Atlantic Canada. The trend has softened compared to 2022 and 2023, suggesting that some of the pandemic-era drivers of migration may be easing.

Implications

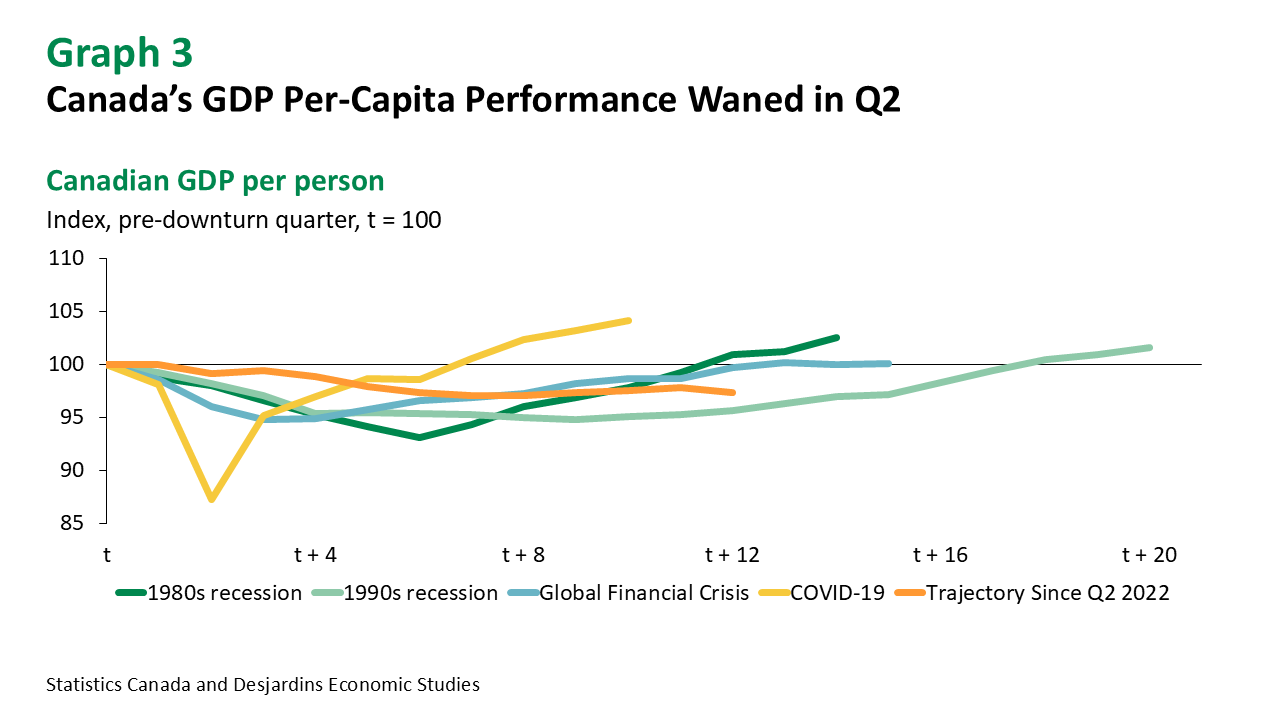

Looking ahead, slower immigration and continued declines in net NPRs should further allow Canada’s housing supply and public services to catch up. It should also ultimately help to lift Canada’s real GDP per capita, which has been trending lower over the last three years. However, the trade-war-induced slowdown in GDP growth in the second quarter resulted in a slight deterioration of this standard of living measure, suggesting a slower advance in Canada’s population is no panacea (graph 3). In fact, weaker population growth—especially if it turns negative—could weigh on broader economic momentum going forward. Policy may further evolve in that space, given the need to balance short-term constraints and long-term needs.

The Bank of Canada (BoC) resumed its rate cutting cycle in mid-September. Among the reasons offered, lower population growth was cited as a headwind to household spending—a prior tailwind that boosted growth while the Bank was hiking interest rates. We continue to expect the BoC will cut the policy rate again at its upcoming October announcement, and that the rate will need to fall to 2.00% from the current 2.50% to help stabilize the economy.