- LJ Valencia, Economist

Economic News

Canada: The Trade Deficit Narrowed in May but the Road Ahead Should Still Be Rough

July 3, 2025

Highlights

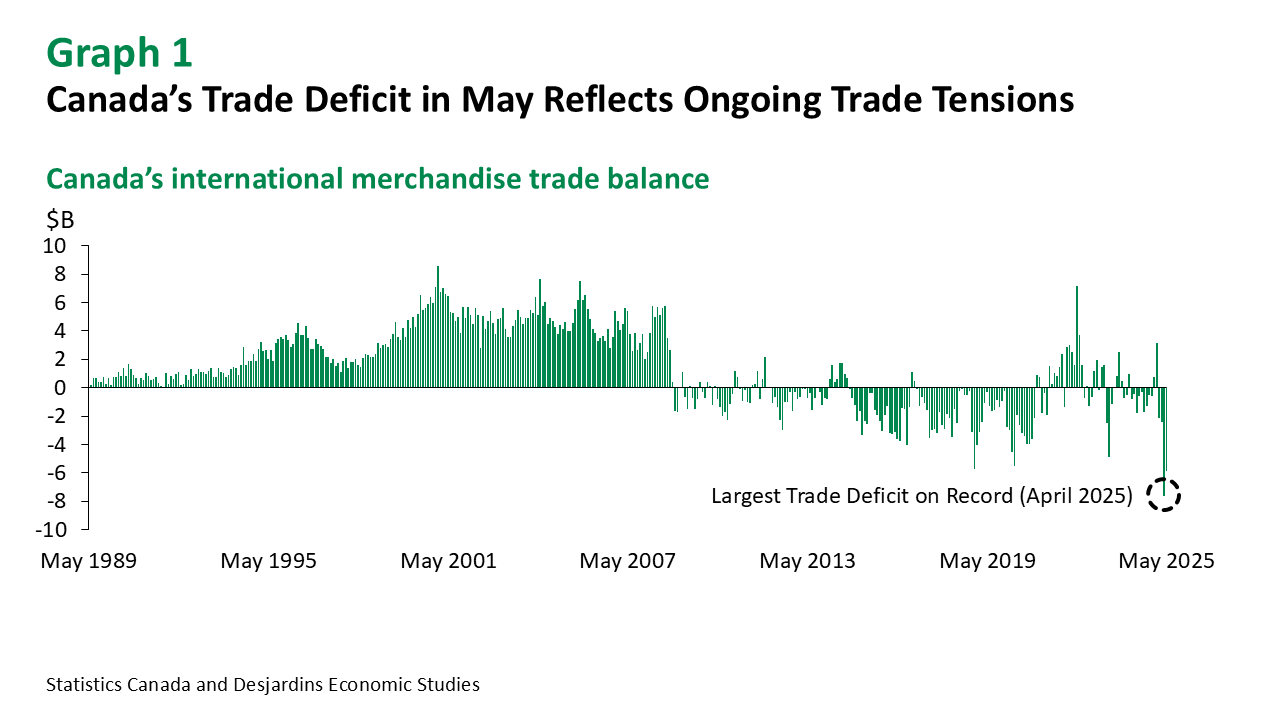

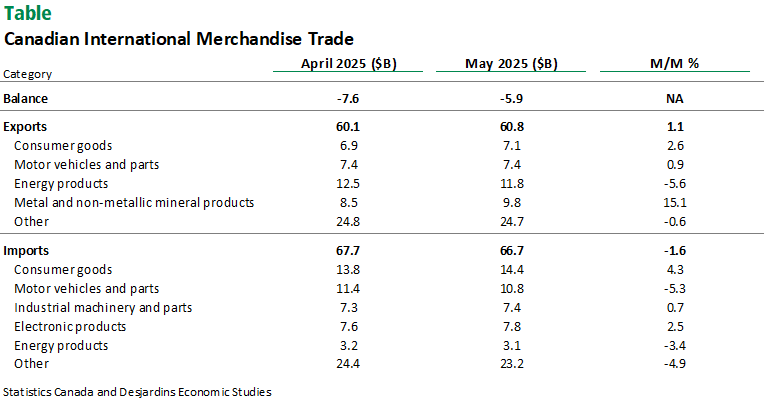

- Canada’s international merchandise trade deficit narrowed to $5.9B in May, after reaching a record low of -$7.6B in April (graph 1). This was slightly better than the consensus expectation of economic forecasters (-$6.0B). See table for more details.

- Goods exports rose by 1.1% m/m in May—a partial reversal of the 11.0% drop the prior month. Imports fell by 1.6%—a third consecutive monthly decline. In real terms, exports were up 1.6% while imports decreased by 1.3%.

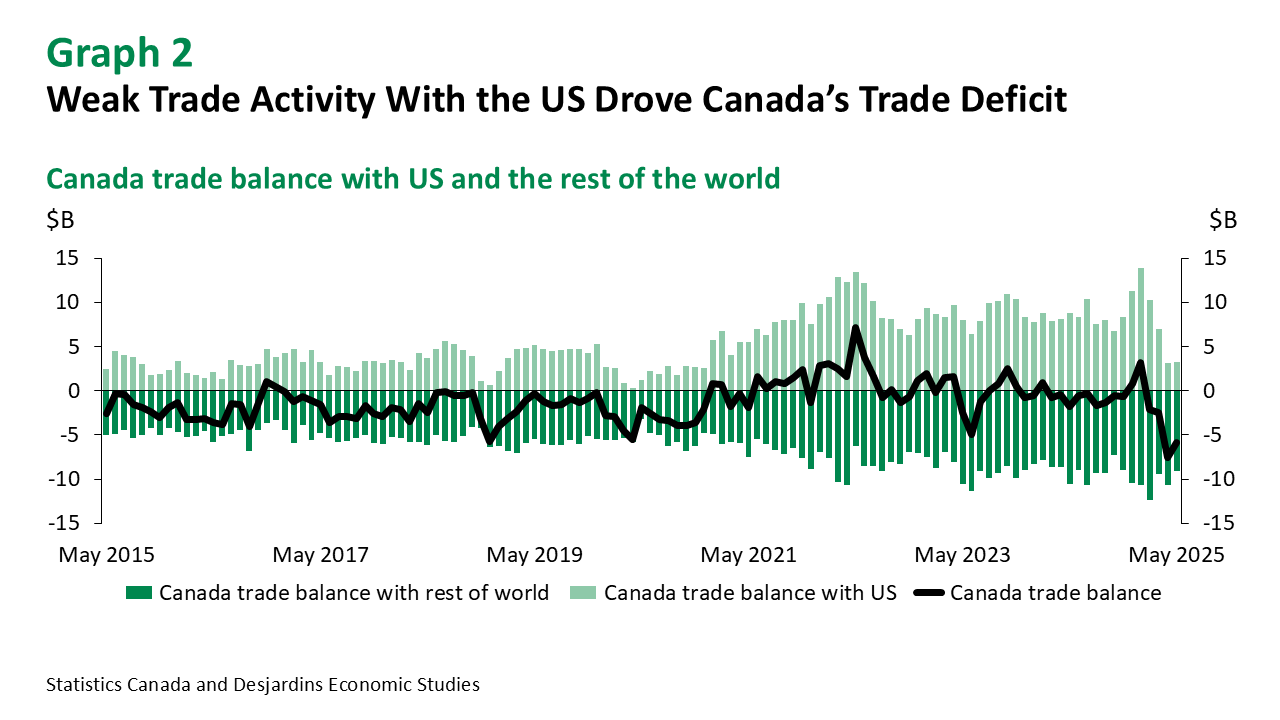

- Canada’s trade surplus with the US rose slightly from $3.1B to $3.2B in May (graph 2). However, Canada’s exports to the US dropped by 0.9% m/m, marking a fourth consecutive monthly decline. In addition, Canada’s share of exports to the US fell from a monthly average of 75.9% in 2024 to 68.3%—one of the lowest shares ever recorded. Meanwhile, Canada’s trade deficit with countries other than the United States narrowed from $10.7B to $9.1B in the month.

- Services trade fell further into deficit in May, to -$760M. Service exports dropped by a modest 0.2% while service imports increased by 1.8%.

Comments

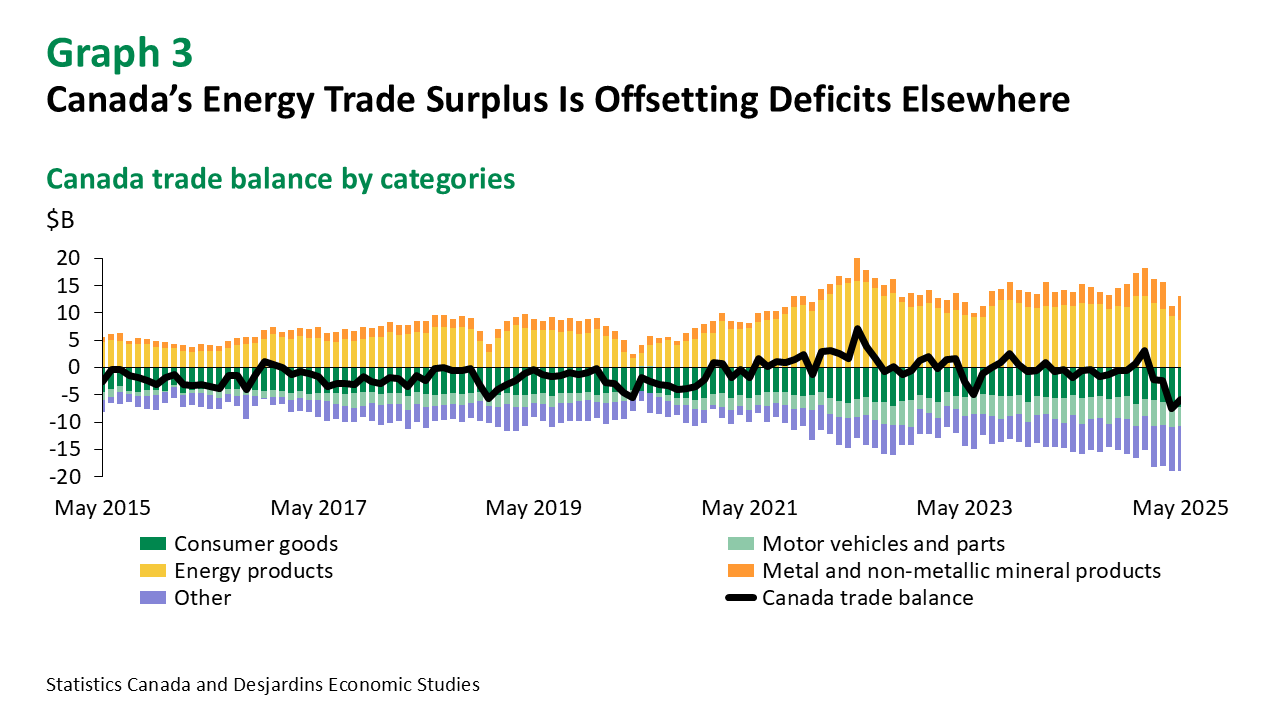

Seven out of 11 export categories experienced an increase in May, despite persistent trade tensions with Canada’s southern neighbour. Metal and non-metallic minerals posted the largest gains (15.1%), on the back of record high gold exports. Exports of consumer goods rose as well (2.6%), in part due to higher shipments of meat as well as prepared and packaged seafood products, much of it destined for Japan. In contrast, the fall in energy exports (-5.6%) can be primarily attributed to lower global oil prices, although Canada continues to have a substantial trade surplus in energy (graph 3).

On the import side, declines were observed in five out of 11 categories. The largest moves were seen in the imports of metal and non-metallic products (-16.8%) and motor vehicles and parts (-5.3%). These sharp decreases followed the introduction of counter-tariffs by Canada in response to US trade measures. Statistics Canada again noted that the CBSA's Assessment and Revenue Management (CARM) initiative may significantly revise import values from November 2024 to May 2025, so import data should be viewed cautiously.

Implications

Despite an improvement in Canada’s trade balance in May, the data point to a further deterioration in trade activity with our southern neighbour. As a result, net exports are expected to drag down Q1 growth by about 5.7%, leading our real GDP growth tracking to fall in the range of -0.5% to 0.0%. This is within the band of the Bank of Canada's April Monetary Policy Report forecasts.

Looking ahead, current trade tensions and volatility should heavily influence growth. Our recent analysis External link. on economic growth and latest projections External link. suggest a more subdued outlook for Canada’s economy in the coming quarters. Consequently, we’re of the view that Canadian central bankers will continue to gradually ease monetary policy through the end of the year.