- Kari Norman

Economist

Economic News

Canada: Builders Stayed Busy While Buyers Stepped Back in September

October 16, 2025

Highlights

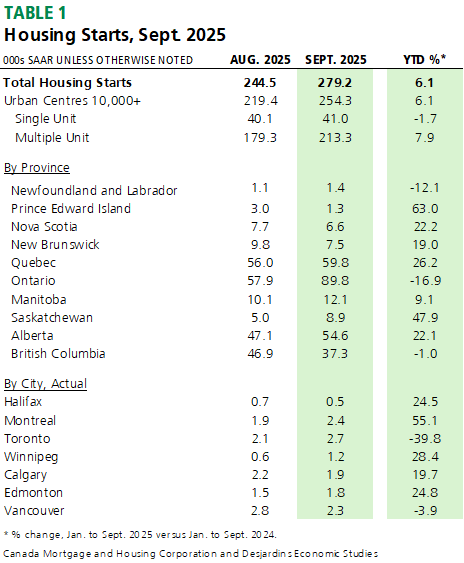

- The pace of housing starts in Canada rose in September, reaching 279k (saar). Table 1 summarizes key data points.

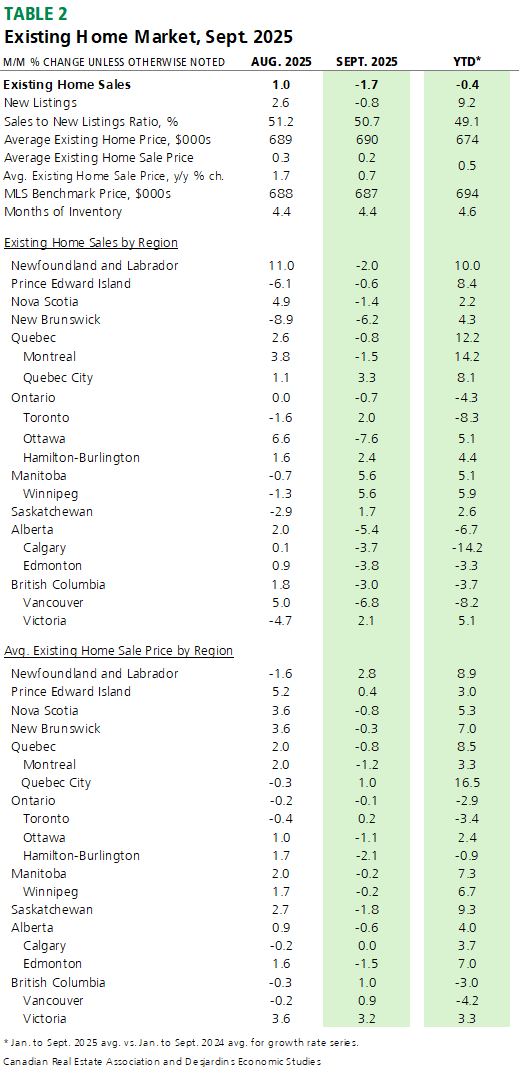

- Existing home sales in Canada declined by -1.7% m/m in September. The average national sale price rose 0.2% m/m, while the benchmark price was flat. Both remain well below their historic peaks reached in 2022. Table 2 summarizes key data points.

Comments

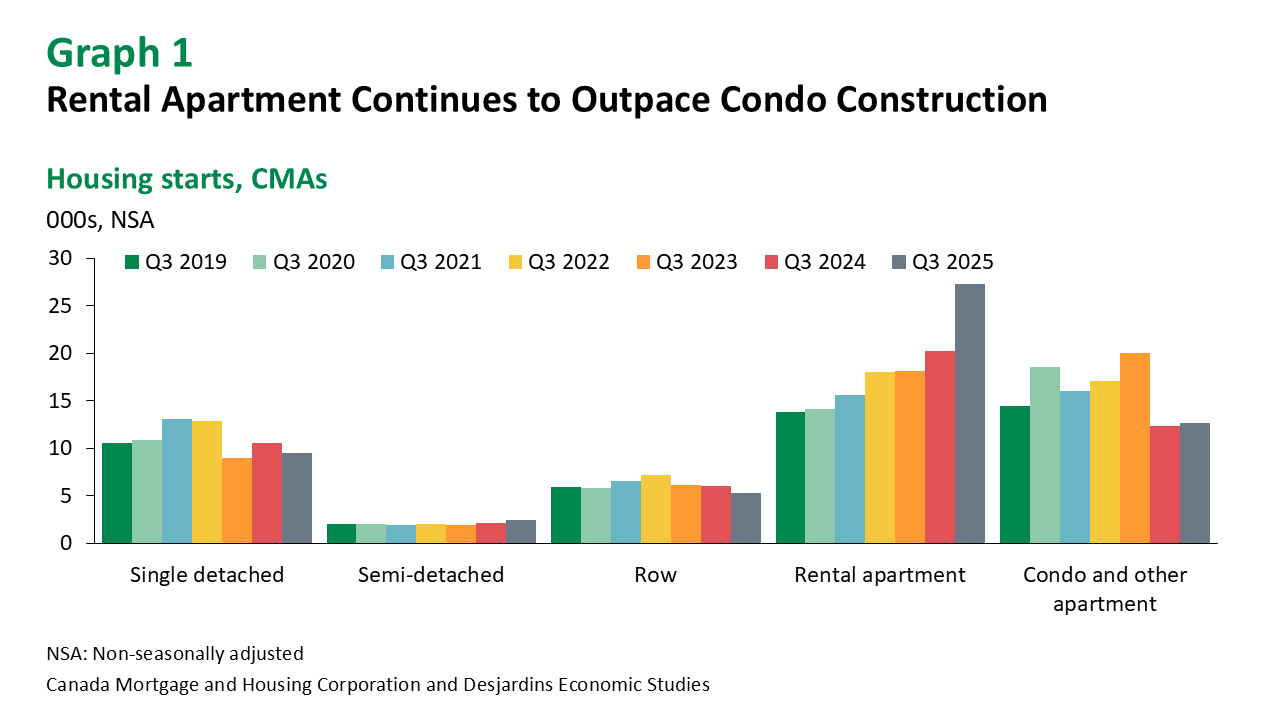

September’s seasonally adjusted housing starts reached 279k, in line with our forecast but beating the consensus of economic forecasters. The strength was led by the multi-unit sector, while single family housing starts remained flat. Looking at longer trends, growth in purpose-built rental apartment construction continues to accelerate each quarter, on a non-seasonally adjusted basis, and was more than double the pace of condo construction in Q3 (graph 1).

Homebuilding fell in BC and the Maritime provinces in September. But the big news was a rebound in housing starts in Ontario. At nearly 90k, it was the highest print since July 2024. While Quebec’s gains were more muted last month, the pace of homebuilding over the first three quarters remained well above 2024 levels.

In the resale market, September saw the first decline in seasonally adjusted home sales since March, at

-1.7% m/m. Nevertheless, the level of non-seasonally adjusted sales remained higher than the previous three Septembers.

Regionally, sales pulled back in all provinces except Manitoba and Saskatchewan. Average prices were little changed in Toronto and Calgary, dipped slightly in Montreal, rose in Vancouver and reached a new high-water mark in Quebec City.

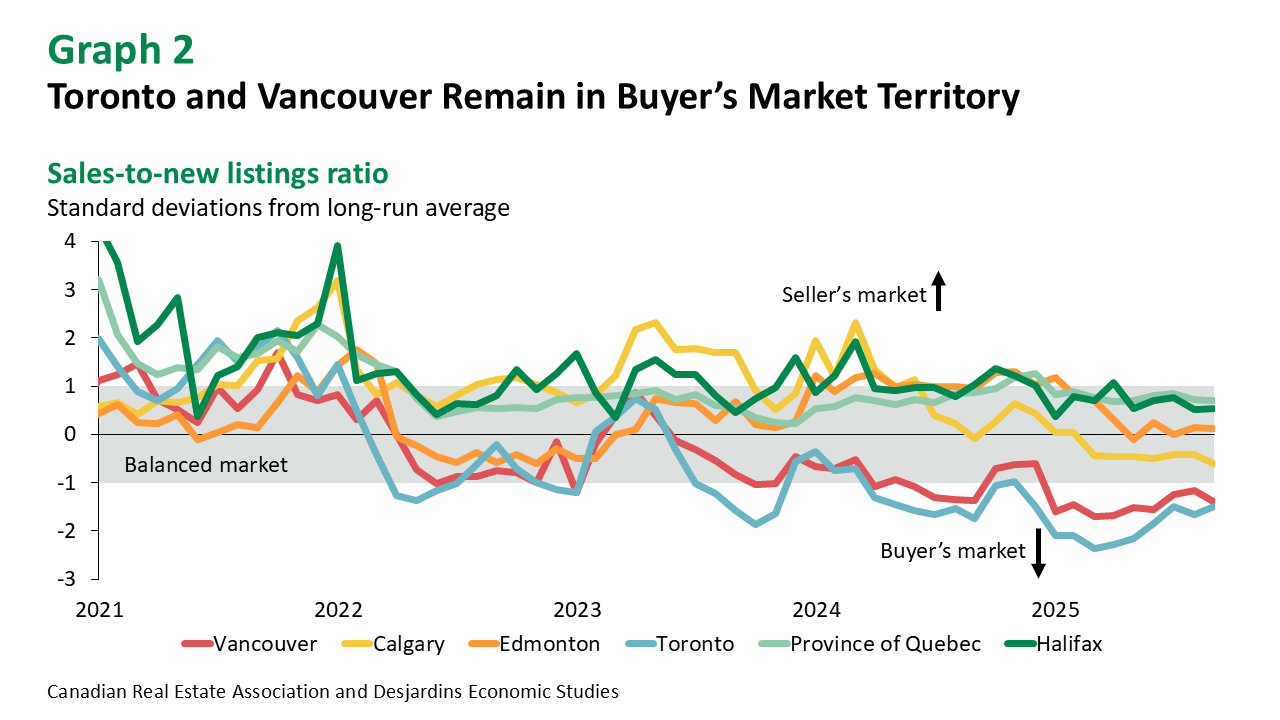

Nationally, new listings dipped nearly 1% and inventory held steady at 4.4 months in September—well above the post-2018 average of 3.7 months. The sales-to-new-listings ratio remained balanced overall, while Toronto and Vancouver continued in buyer’s market territory (graph 2).

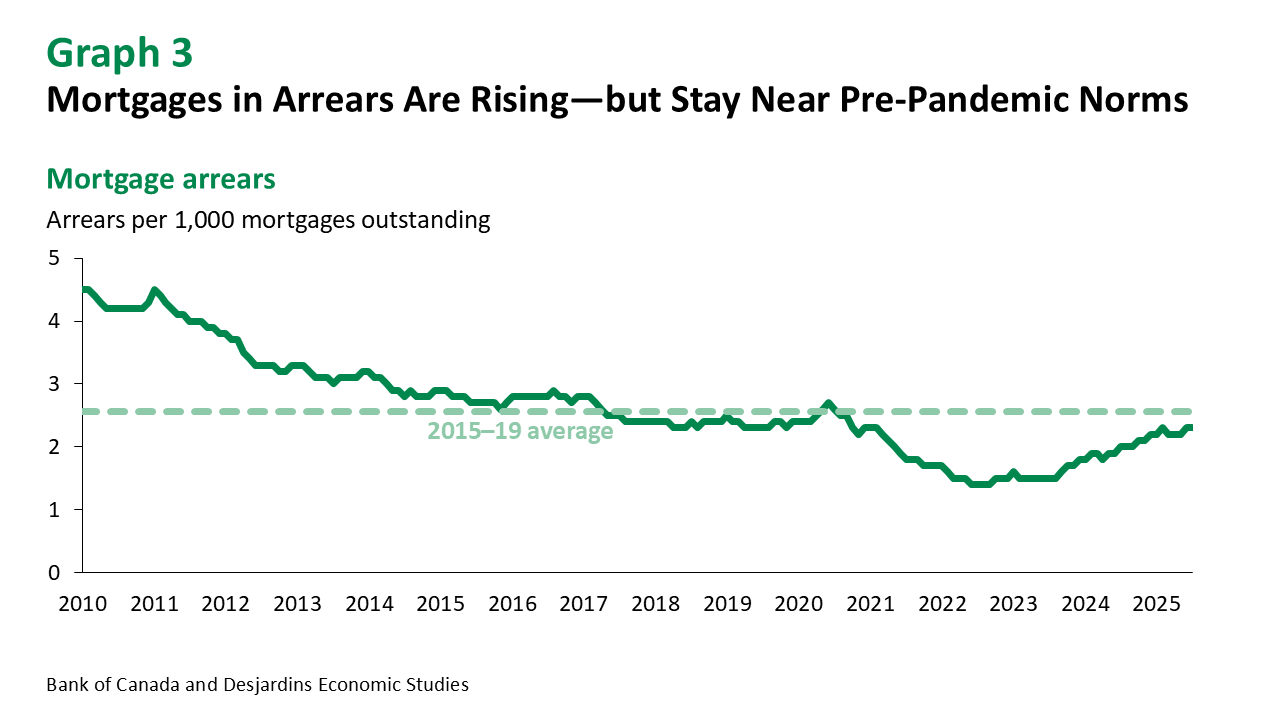

Mortgages in arrears have risen nationally over the past three years, signalling financial pressure on some households. However, the rate remains near pre-pandemic norms and well below early 2010s levels, indicating most borrowers are keeping up with their payments (graph 3). We don’t anticipate a wave of forced home sales from mortgage renewals at higher rates, though this could vary by region.

Implications

The Bank of Canada External link. lowered the policy rate by 25-basis points to 2.50% in September, with limited impact on home sales given the mid-month timing. Looking ahead, we expect another 25-basis point rate cut later this month, followed by one more to support economic activity.

Lower borrowing costs, rising wages and household wealth External link. and more affordable home prices—combined with greater supply of homes listed for sale—could draw sidelined buyers back, though labour market External link. softness and trade uncertainty remain risks.

The housing starts outlook External link. is mixed. Record Q1 permits suggest strength, but unsold inventory in the multi-unit sector, weak rent growth and financing hurdles likely weigh on projects. The sharp decline in net non-permanent residents External link. may slow population growth, dampen rental demand and constrain new construction.