- Kari Norman

Economist

Economic News

Canada: Home Sales and Homebuilding Were Both Strong in May

June 16, 2025

Highlights

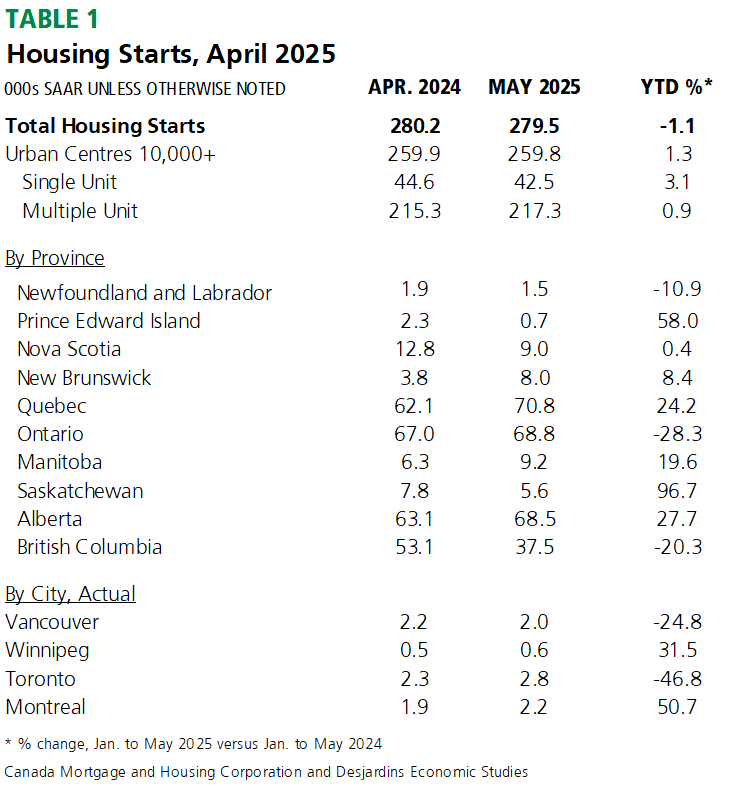

- The pace of housing starts in Canada remained strong at 279.5k (saar) in May, while April was revised up slightly to 280k. Table 1 summarizes key data points.

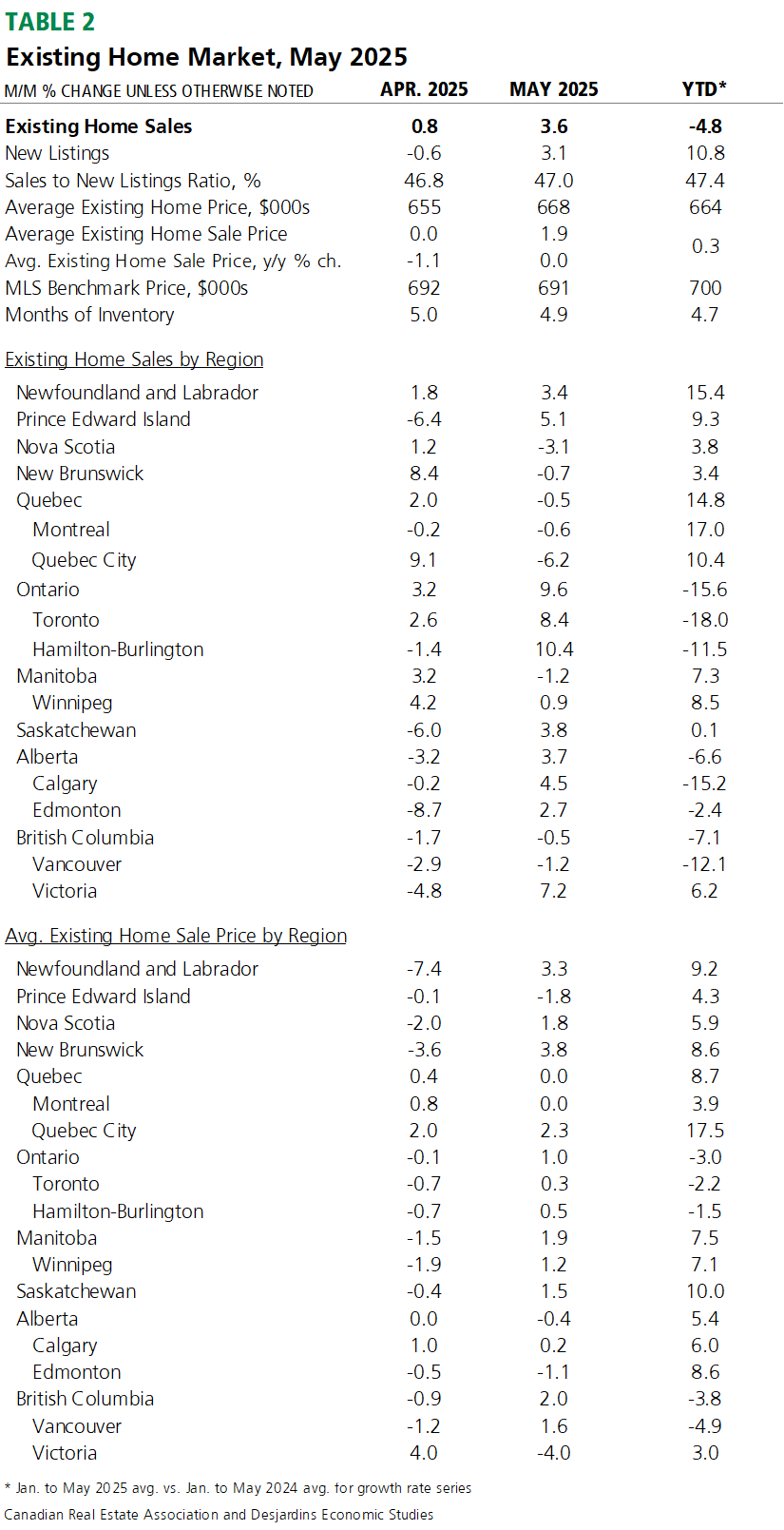

- In the resale market, home sales in Canada picked up, growing 3.6% m/m in May. The average sale price rose 1.9% while the benchmark price fell marginally. Both remain well below their historic peaks reached in 2022. Table 2 summarizes key data points.

- Our tracking is for Q2 2025 real GDP to be essentially unchanged, albeit subject to downside risk.

Implications

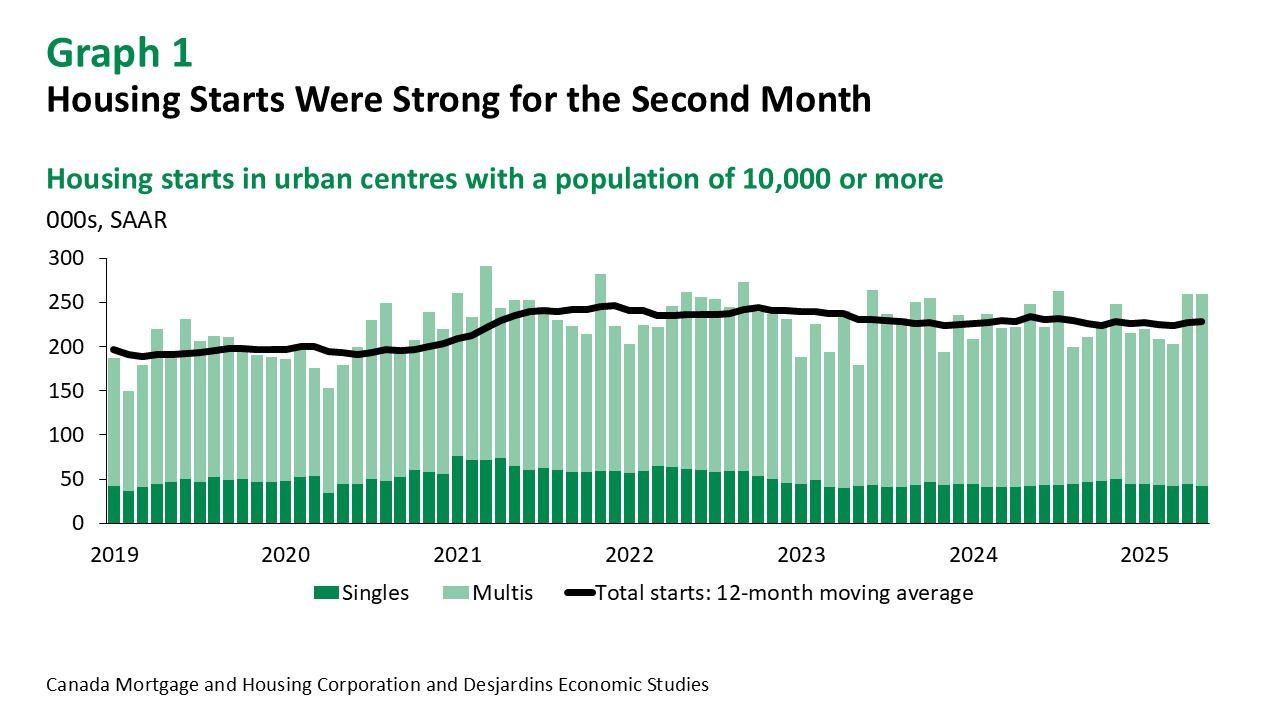

May’s seasonally adjusted housing starts were about 280k for the second month in a row. The strength was once again led by the multi-unit sector, while single family housing starts declined slightly (graph 1). Nevertheless, we remain firm in the belief that large swings in month-to-month data speak to natural fluctuations of multi-unit starts, rather than an indication of a turnaround in the sector. Indeed, year-to-date housing starts were down marginally from the same period a year ago.

Provincially, home construction continued to see strong gains in Quebec to levels not seen since early 2022. The Prairie provinces are also experiencing strong starts to the year. On the other hand, homebuilding continued to pull back in BC following a burst of activity in April. Ontario housing starts picked up slightly, posting their second-best month in the past year.

The First-Time Homebuyers GST Rebate External link. on newly built homes took effect for purchase agreements dated on or after May 27. This may bring some additional buyers into sales offices, but it’ll be a while before those projects break ground and show up in the housing starts statistics.

In the resale market, May saw the first signs of optimism in home sales in six months, but sales remain at the low end of seasonal norms. While trade war uncertainty still looms, average and benchmark prices have fallen to about 17% below their early 2022 peaks. For some buyers, the opportunity may have been too good to pass up.

New listings picked up about 3% from April, while inventory held steady at nearly five months. With this excess supply in the market, average sale prices ticked up only slightly in May but remain flat over the past year, while the benchmark price declined marginally.

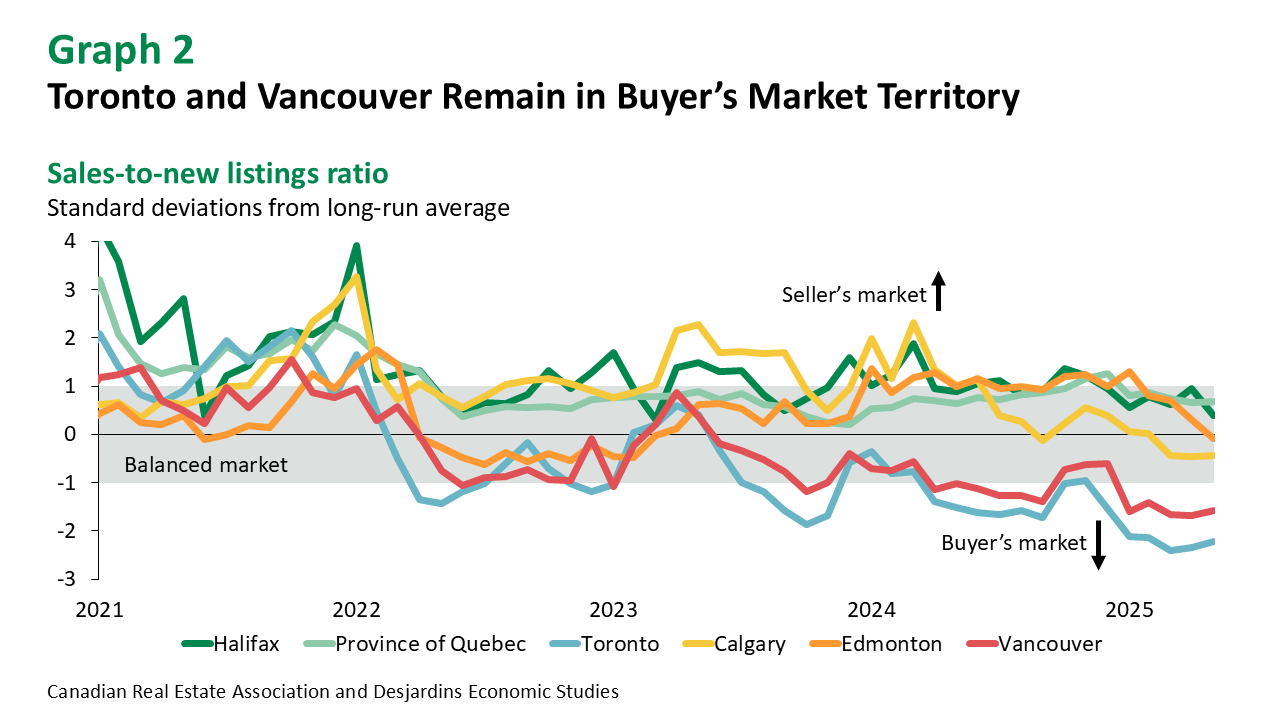

Regional differences remained significant. Home sales reversed course in Quebec City but the average selling price continued to increase, reaching a new high. Despite stronger sales in Toronto, both Toronto and Vancouver remained deep in buyer’s market territory (graph 2).

While one good month of home sales doesn’t make a trend, there may be signs of cautious optimism for the resale market for those buyers who remain little affected by the ongoing trade war. The combination of lower prices, more inventory and less economic uncertainty may continue to entice more homebuyers back into the market this summer.