- Royce Mendes

Managing Director and Head of Macro Strategy

Weekly Commentary

Market Volatility and the Canadian Economy

October 24, 2025

A recent article External link. by former IMF First Deputy Managing Director Gita Gopinath warned that an equity market correction could wipe out $20 trillion in wealth for American households. As she notes, that’s equivalent to roughly 70% of US GDP and could reduce economic activity by as much as 2 full percentage points. Gopinath based her calculations on a market drawdown of similar magnitude to the dotcom crash of the early 2000s.

A correction of that scale would hurt Canadian households too, but the economic fallout might not be as severe. Our analysis suggests that a dotcom-style drawdown in Canada would erase household wealth equivalent to about 45% of GDP. The more muted impact stems from two key factors.

First, Canadian portfolios are more skewed toward domestic equities, which have historically been—and still are—less exposed to the tech sector. Second, households north of the border hold a smaller share of their wealth in publicly listed equities. While headline data on equity and mutual fund holdings might suggest Americans and Canadians have similar stock exposure, the comparison is misleading. Canadians tend to access fixed income through mutual funds, whereas Americans more often hold bonds directly.

This lower exposure to tech and equities means Canadian households haven’t fully participated in the recent bull market—but it also means they’re less vulnerable to a correction. That said, Canadian households aren’t necessarily facing any less risk. Their portfolios are heavily tilted toward an asset class that’s already under pressure.

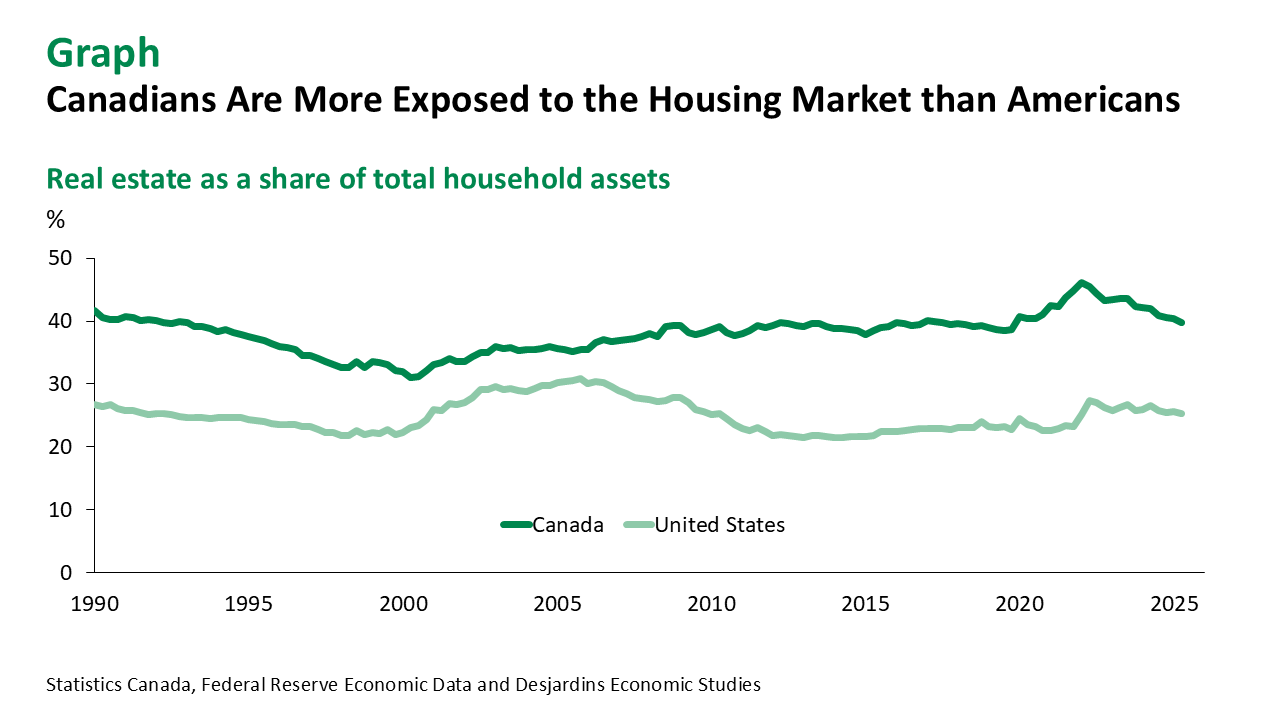

Falling home prices in many provinces have constrained wealth accumulation in Canada. Since the first quarter of 2022, Canadian household net worth has risen just 7%, well below the 16% growth American households have enjoyed. Despite the decline in home prices and gains in equities, real estate still accounts for roughly 40% of household assets in Canada, in contrast to 25% in the United States (graph).

While the central bank has limited influence over equity markets, the Bank of Canada should be paying close attention to the housing market. Most homeowners still have substantial equity, but that cushion is shrinking each month. After several years of declines, stabilizing house prices should be a priority for monetary policymakers aiming to restore the economy to full health.