- Randall Bartlett

Deputy Chief Economist

Weekly Commentary

Mixed Signals on the Budget Risk Eroding Canada’s Federal Fiscal Credibility

May 23, 2025

Last week, word came down from Canada’s newly minted Prime Minister that there will be no Budget 2025 until the fall. That followed some mixed messages from the Finance Minister as to whether it would be a full budget or just a fall update. Save for the pandemic and post‑9/11, this will be the first time Canada won’t have a fiscal plan published in the spring going back to at least 1968. And when a spring budget wasn’t tabled in the past, it was because an emergency budget was passed either earlier (as in the case of December 2001’s “security budget”) or not long after (as in the case of the pandemic’s July 2020 Economic and Fiscal Snapshot).

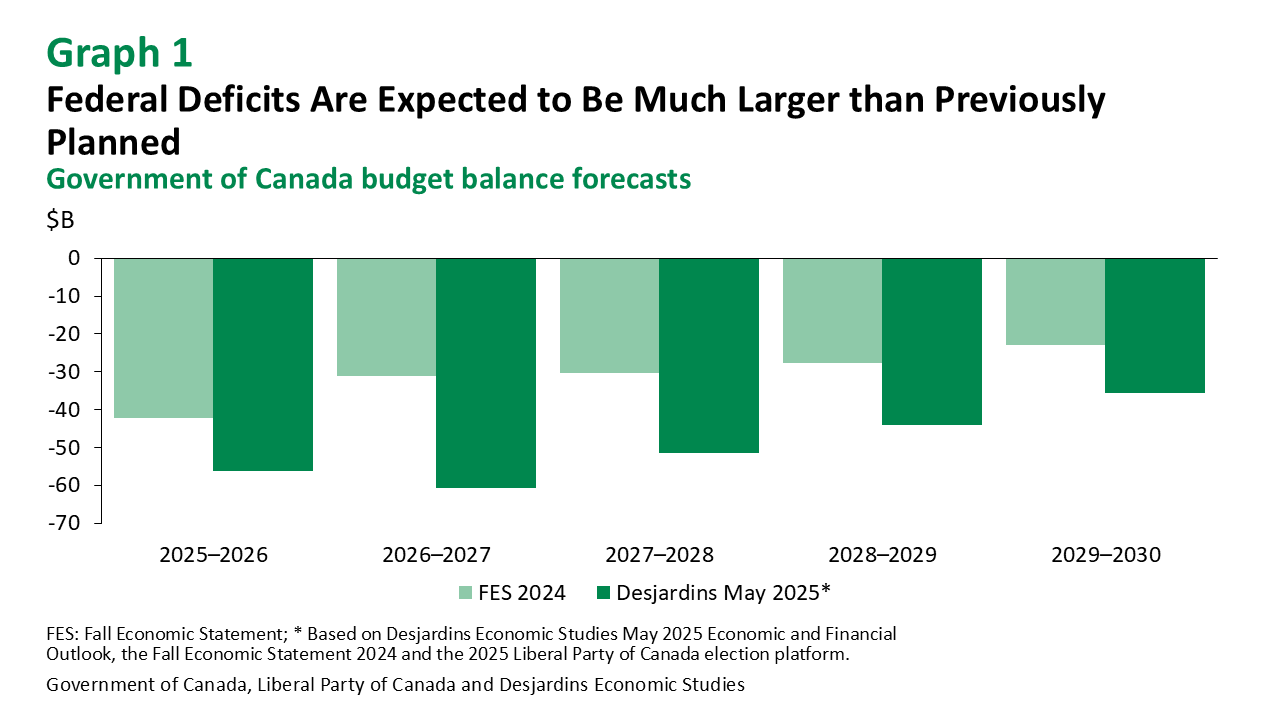

The decision by the Government of Canada to not publish a spring budget is surprising given the scale of electoral commitments. The Liberal Party of Canada’s 2025 election platform contained more than 100 new measures, totalling about $130B in new spending and tax cuts. Beyond $20B in income from retaliatory tariffs, offsetting revenues and savings were estimated at only $32B and came from the often elusive “increasing penalties and fines” and “savings from increased government productivity.” Even if these were realized, federal deficits are still planned to be about $20B larger on average annually over the next four years than those published in the Fall Economic Statement 2024 (graph 1).

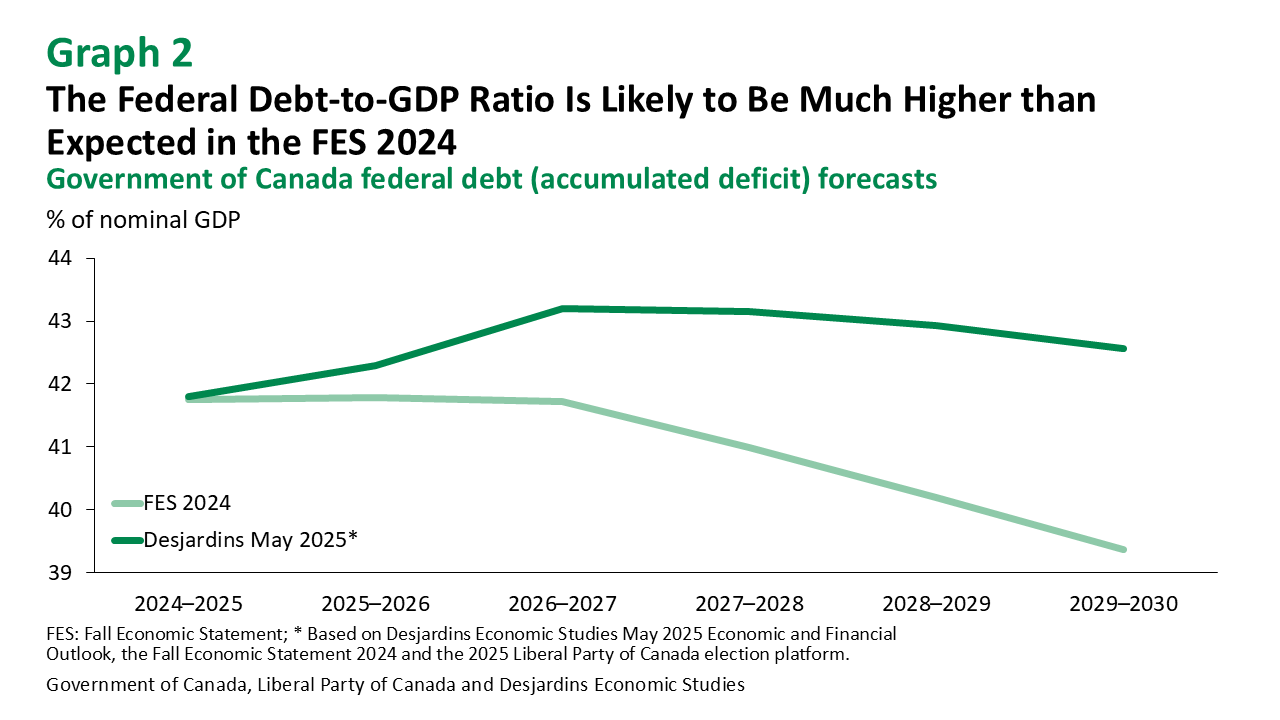

Under these optimistic assumptions, the debt-to-GDP ratio is set to rise (graph 2). But the Canadian economy could easily underperform the Parliamentary Budget Officer’s economic outlook used for election platform costing as risks to that forecast are very much tilted to the downside. (See our May 2025 Economic and Financial Outlook External link., published yesterday.) The deficit in the 2024–2025 fiscal year is also on track to be larger than was assumed at the time of the 2025 election. As such, if the federal government follows through with its election platform, the debt-to-GDP ratio could easily be even higher than currently projected.

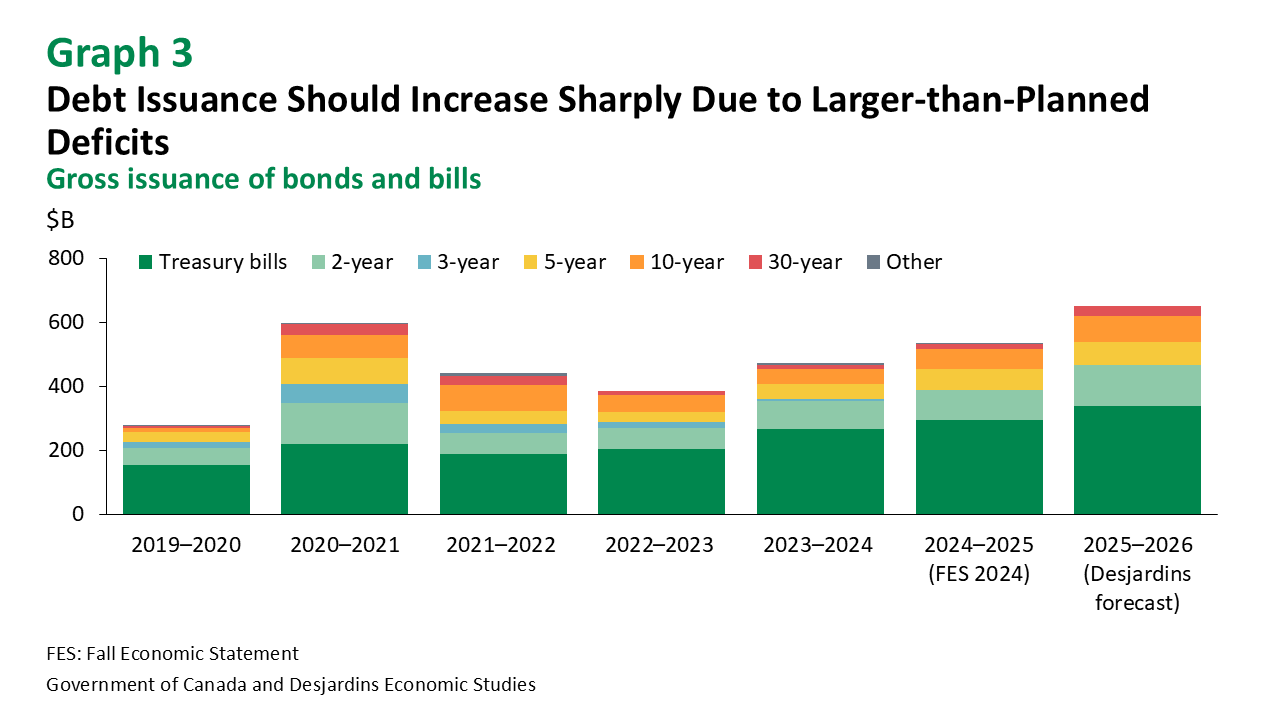

However, while deficit forecasts were published in the federal election platforms, debt projections were not. As a result, Canadians have been left guessing what ballooning deficits will mean for outstanding debt, the cost of which will be shouldered by current and future taxpayers. And without the publication of a Debt Management Strategy, markets are left guessing how much debt the federal government will issue in the 2025–2026 fiscal year and at what maturities. Our analysis puts the estimate for gross issuance this fiscal year at well over $600B, but no one knows for sure (graph 3).

The delay in publishing a comprehensive fiscal plan introduces a degree of opacity at a time when global markets are likely to scrutinize sovereign balance sheets. The Government of Canada risks having its credit rating downgraded as a result. Fitch, a rating agency, raised this concern even before it was announced that there would be no budget this spring. And this comes on the heels of the US government debt downgrade by Moody’s late last week.

The previous federal government was often criticized for regularly missing its “fiscal anchors,” and rightly so. But the current administration doesn’t appear to feel the need to publish a deficit and debt forecast in a timely manner, let alone fiscal targets. That is concerning. This is especially true as the current administration plans to introduce legislation that will cut taxes and increase spending without providing parliamentarians and Canadians with a sense of what it means for the Government of Canada’s bottom line.

Canada is at a unique moment in its history, when exceptional economic threats from south of the border call for exceptional measures. But along with exceptional measures must come exceptional transparency and accountability. Delaying Budget 2025 until the fall does not meet that standard. The Government of Canada’s hard-won fiscal credibility could be at stake as a result.