- Kari Norman

Economist

Economic News

Canada: Back-to-back Monthly Job Losses Top 100k

September 5, 2025

Highlights

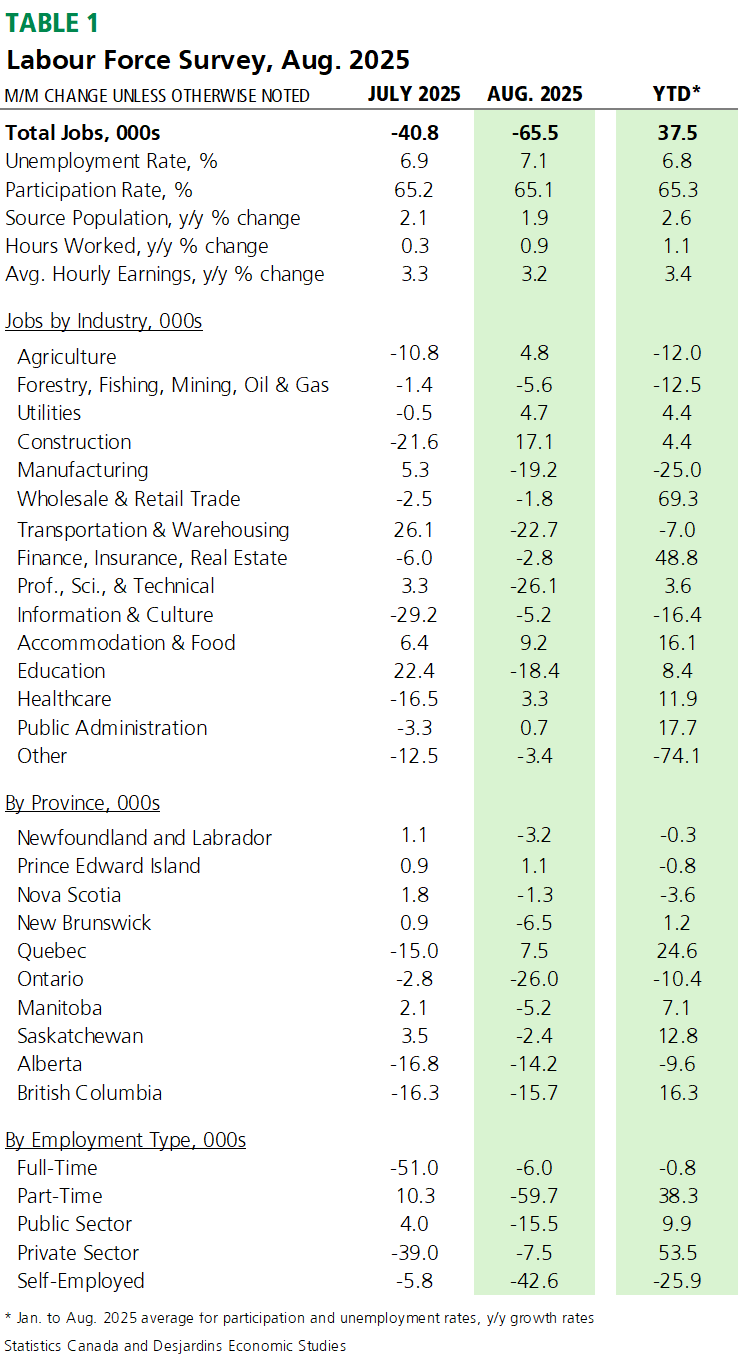

- Canadian employment declined in August 2025 by 65.5k jobs. The disappointing result came on the back of July’s decline of 41k jobs. Today’s print surprised economic forecasters who anticipated growth of 5k. The unemployment rate rose two ticks to 7.1%, also worse than expected.

- Total hours worked in August were little changed, at +0.1% month-over-month and +0.9% year-over-year. Average hourly wage growth increased 3.2% y/y in August, a slight slowdown from July. Table 1 summarizes key data.

- Our early tracking suggests that real GDP growth will be broadly unchanged in Q3 2025 after a contraction in Q2.

Comments

The Canadian labour market contracted in August for the second month in a row, for the first back-to-back monthly declines in hiring since 2021. While job losses were felt by all employment types, the bulk were in part-time positions and self-employed work. Ontario, BC and Alberta recorded the largest employment declines. Quebec gained 7.5k jobs in the month, and has accounted for almost two-thirds of the total jobs gained this year in Canada.

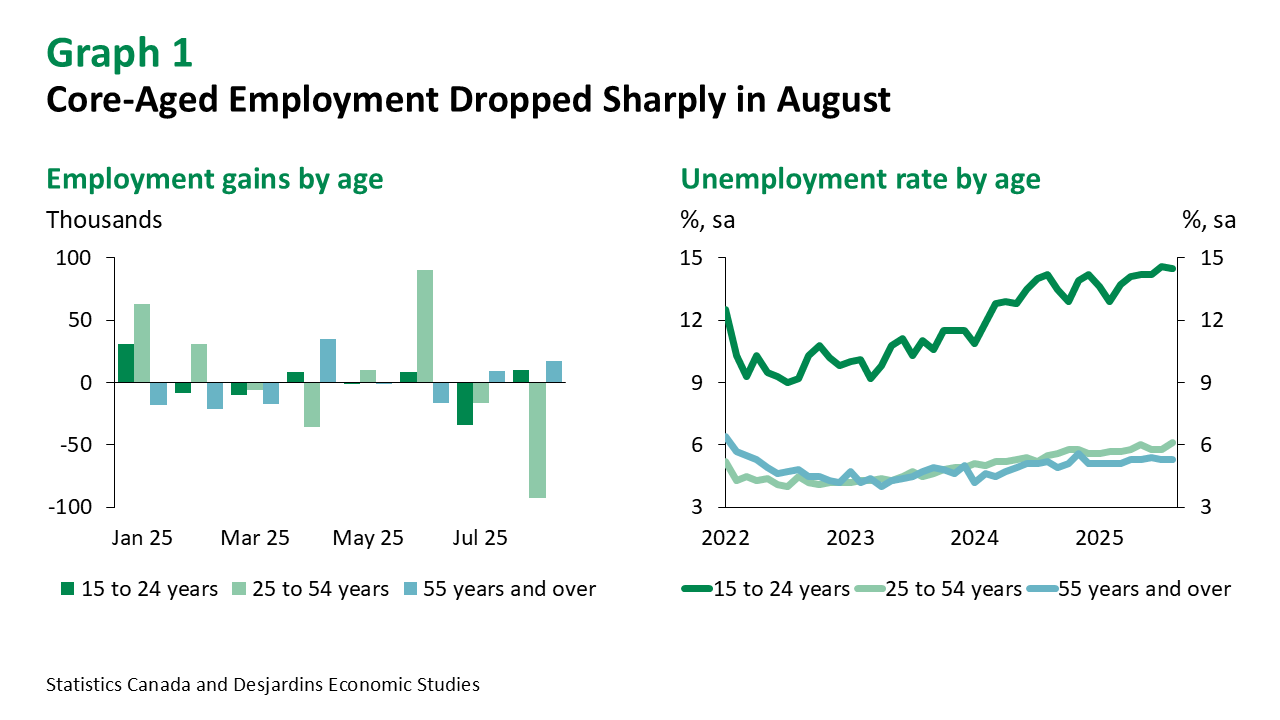

The unemployment rate rose sharply for core-aged workers (ages 25 to 54 years) to 6.1% in August from 5.8% (graph 1). That comes as the full weight of employment losses were borne by core-aged workers at -93k jobs, while an additional 56k dropped out of the labour market. In the final month of the summer job market, youth (ages 15 to 24 years) gained about 10k positions, reversing some of their losses the prior month, while their unemployment rate remained elevated. Our recent report External link. looked at the drivers of high youth unemployment.

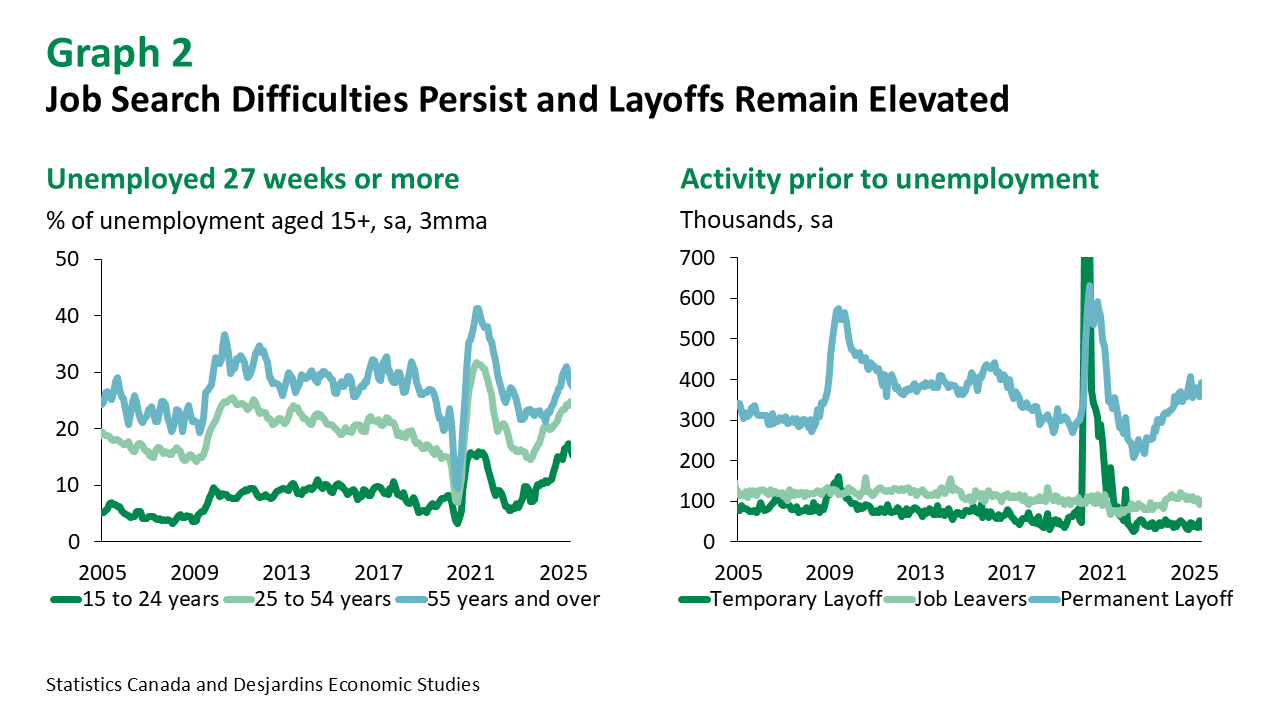

Labour market conditions continue to deteriorate, with the unemployment rate now 2 percentage points higher than the historic low achieved three years ago. Indeed, the jobless rate now sits at its highest point in nearly a decade, outside of the pandemic era. Long-term unemployment continued to rise, with 1 in 4 core-aged job searchers experiencing at least 6 months of unemployment (graph 2). Permanent layoffs also rose, albeit remaining below recessionary levels.

Average wage growth remained broadly unchanged from July at 3.2% year-over-year, albeit well down from the elevated levels of over 5% that characterized the post-pandemic period. Wages are expected to remain subdued through the remainder of 2025 as labour demand weakens. That said, wage gains should continue to outpace inflation, supporting ongoing real earnings growth.

Implications

Looking ahead, despite the removal of retaliatory tariffs External link. on $44B of imports from the US, Canada remains mired in trade uncertainty with USMCA up for renewal soon. Moreover, weakness may be spreading from trade-exposed sectors to those that are less exposed. As a result, concerns about inflation should move to the back burner and the Bank of Canada should resume its rate cutting cycle later this month. We continue to anticipate that the policy rate will need to fall to 2.00% from the current 2.75% to stem the bleeding in the economy.