- Laura Gu, Senior Economist • LJ Valencia, Economic Analyst

Economic News

Canada: An April Reprieve Does Little to Counter Labour Markets Slowdown

May 9, 2025

Highlights

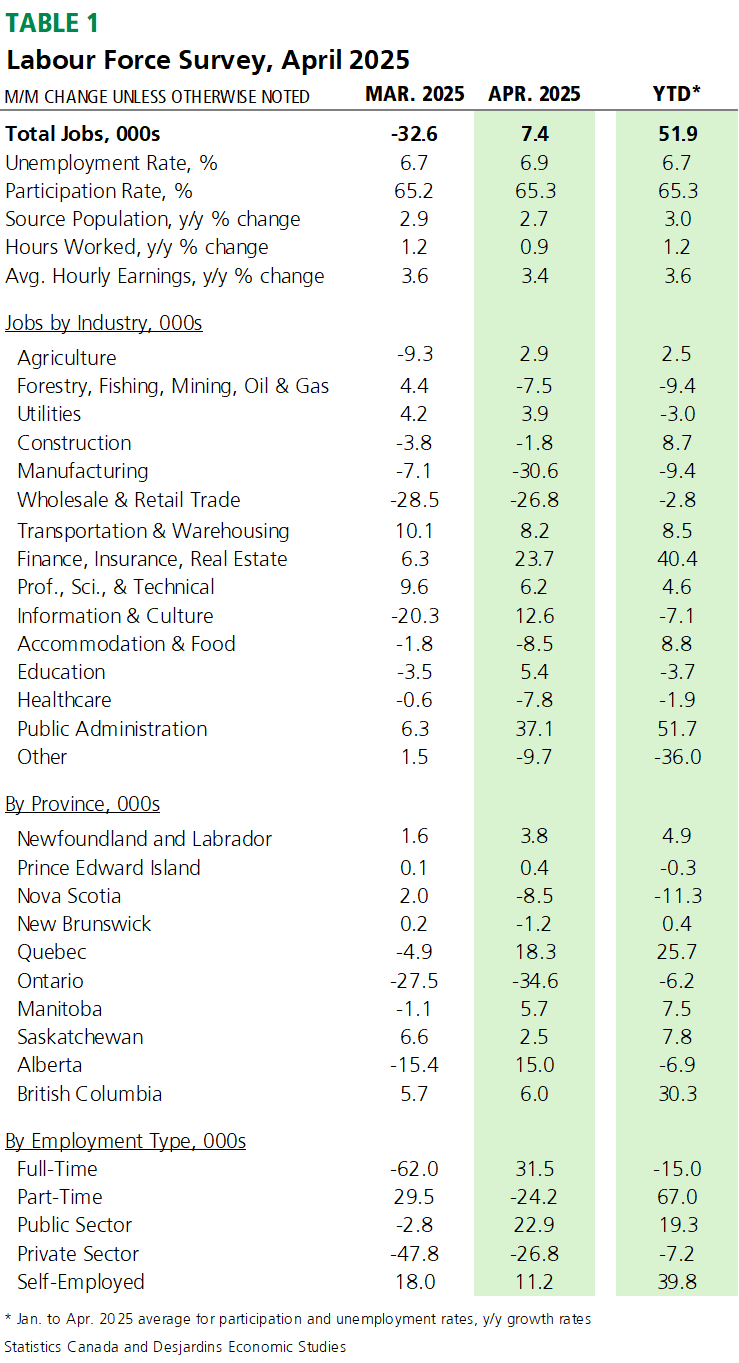

- Total Canadian employment held steady in April 2025 after March’s decline, adding 7.4k jobs, broadly in line with the 5k expected by economic forecasters. Without the temporary federal election hiring, April employment would have experienced another contraction similar to March. The unemployment rate moved up two ticks to 6.9%, returning to the peak seen in November 2024.

- Total hours worked rose 0.4% month-over-month in April, following similar growth in March, and were up 0.9% compared to the previous year. Average hourly wage growth slowed to 3.4% y/y, marking the slowest pace since February 2022. Table 1 summarizes the key data points.

- Our Q1 2025 real Canadian GDP growth forecast is tracking at 1.7% q/q annualized following the April employment data, roughly in line with the forecast in the Bank of Canada’s (BoC) most recent Monetary Policy Report (MPR).

Implications

The Canadian job market posted a modest gain of 7.4k jobs in April, amid somewhat easing trade tensions and a federal election, reversing some of the contraction experienced in March. Job gains were driven by an increase in full-time (+31.5k) and public sector (+22.9k) positions, while the private sector experienced a loss of 26.8k jobs. Overall labor demand has been softening, with few industries showing consistent demand for workers in recent months.

Job gains were predominantly seen in public administration (+37k), largely due to the hiring of temporary workers for federal election-related activities. The finance, insurance, real estate, rental, and leasing sector also saw an increase (+24k). Employment declined significantly in manufacturing (-31k) and wholesale and retail trade (-27k), as Ontario experienced the largest provincial employment drop (-35k).

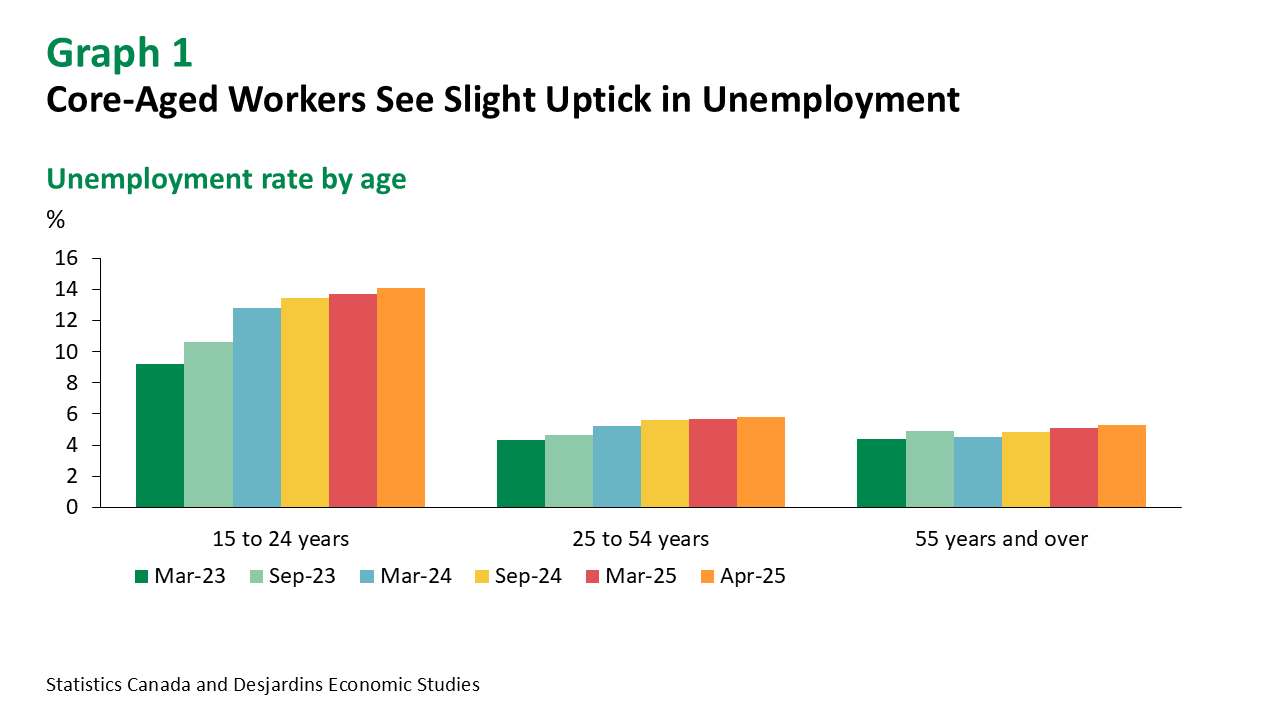

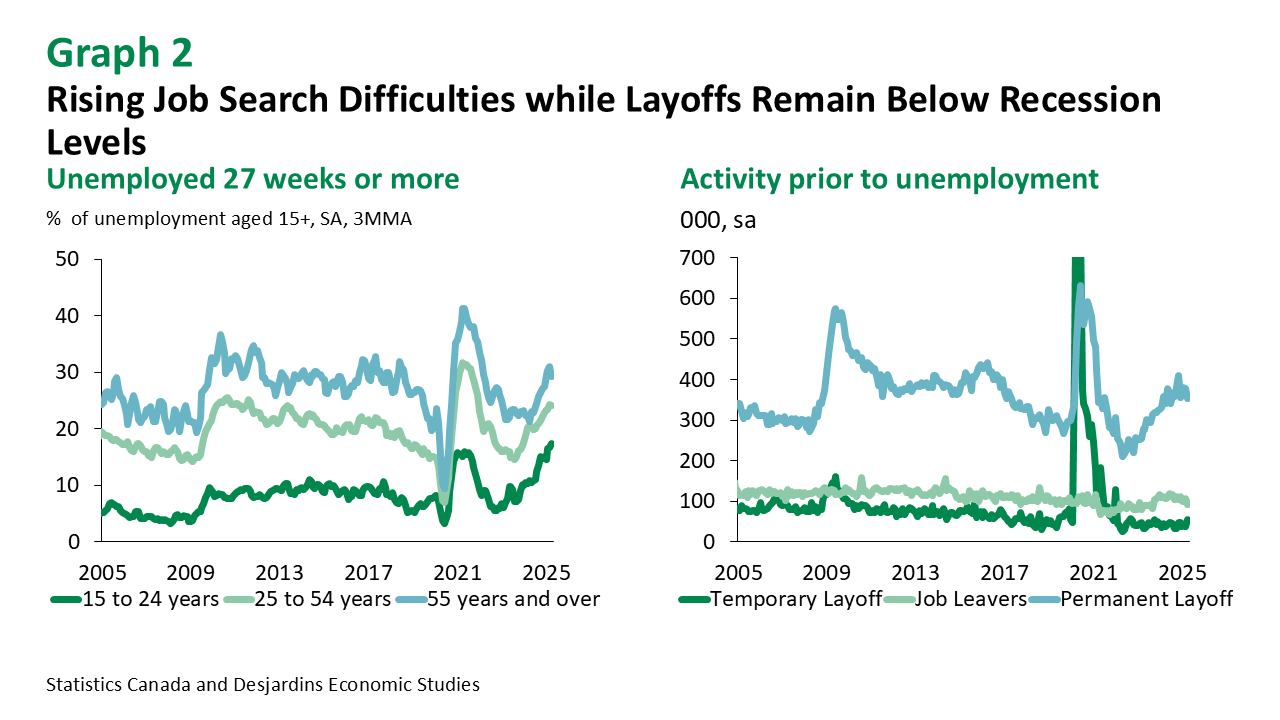

The unemployment rate returned to its November 2024 peak, the highest level since January 2017 (excluding the COVID-19 pandemic), increasing across all age groups, but only inched up slightly among the economically important prime-aged workers (25 to 54 years) from 5.7% to 5.8% in April (graph 1). Labor market conditions are deteriorating under the hood, with weakened demand primarily affecting job seekers through reduced hiring. Long-term unemployment has risen significantly, with the proportion of people searching for work for 27 weeks or more increasing markedly from a year ago, especially among youth (15 to 24 years). Although permanent layoffs are gradually rising, they remain well below levels seen in previous recessions (graph 2).

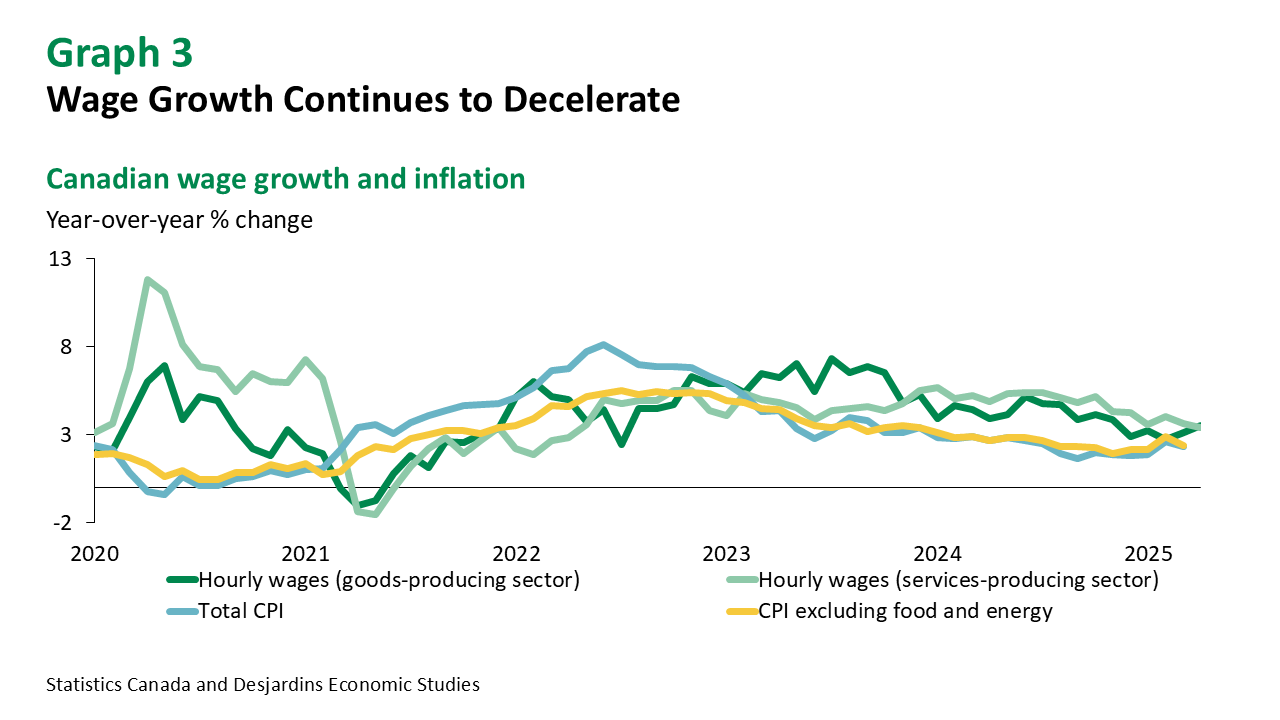

Average wage growth inched down to 3.4% year-over-year in April, continuing the downward trend from 5.0% in October 2024 and marking the slowest pace since February 2022 (graph 3). Wage growth is expected to remain subdued throughout 2025 as labour demand weakens amid heightened uncertainty.

Although Canada continues to benefit from CUSMA exemptions post "Liberation Day", downside risks External link. remain elevated. The labor market is softening with decelerating wage growth, while inflation and inflation expectations face downward pressure External link. due to the removal of federal pollution pricing, leaving room for significant action from the Bank of Canada as early as June.