- Randall Bartlett

Deputy Chief Economist

Economic News

Canada: Surging Job Gains in December Won’t Derail a January Rate Cut

January 10, 2025

Highlights

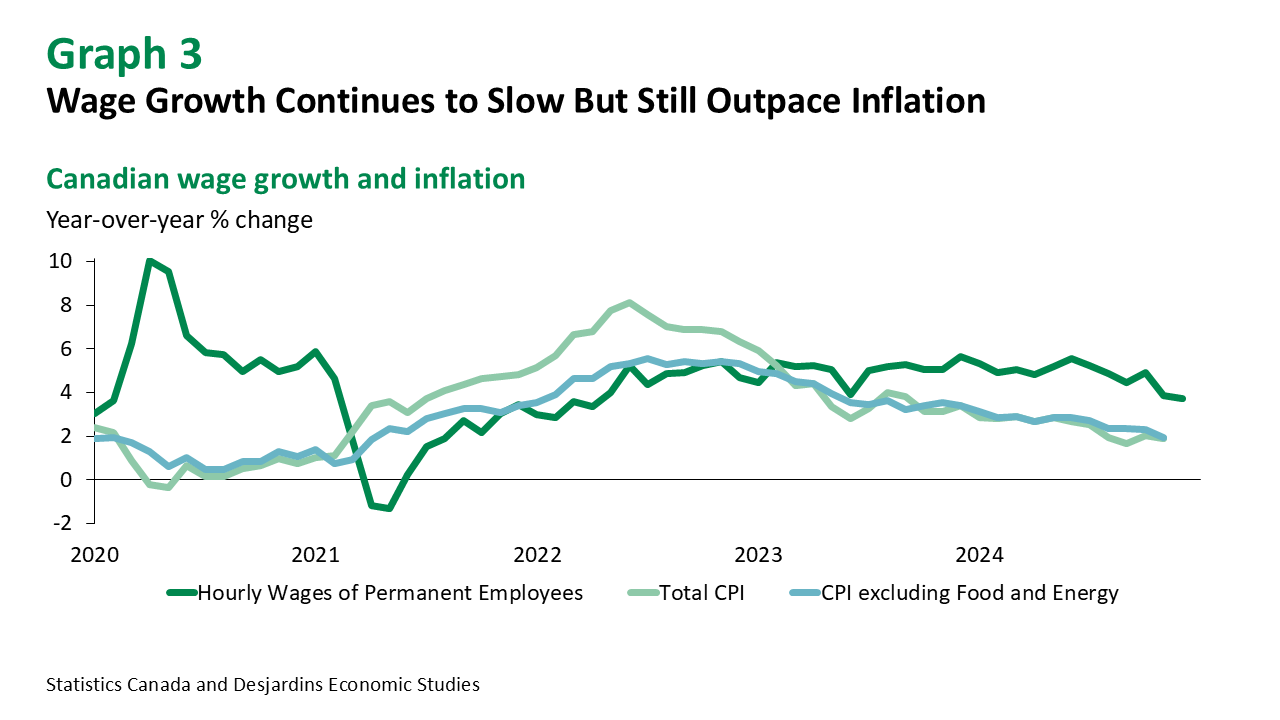

- Total Canadian employment surged by more than 90k jobs in December 2024, blowing the doors off the expectation of economic forecasters (+25k). The unemployment rate fell back slightly to 6.7%, after hitting its highest level since 2021 in November. Total hours worked rose in December (0.5% m/m) and were up 2.1% y/y over the prior year—the strongest advance since mid-2023. Meanwhile, average hourly wage growth cooled to 3.8% y/y—the slowest pace since May 2022. Table 1 summarizes key data points.

- Our Q4 2024 forecast for real Canadian GDP growth edged closer toward 2.5% annualized following the December employment data, in line with but slightly better than the forecast in the Bank of Canada’s (BoC) most recent Monetary Policy Report (MPR).

Implications

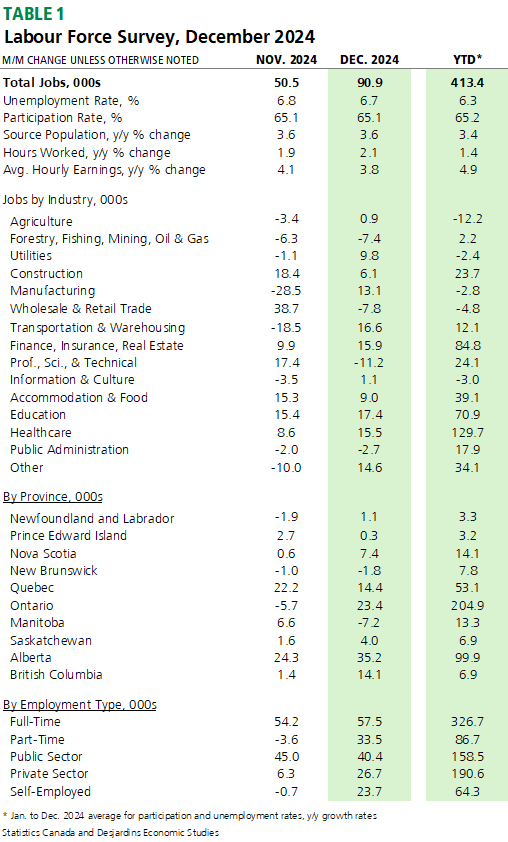

It’s tough to find much in the way of bad news in December 2024 employment report. Job gains surged, the majority of which were full time. Eight out of 10 provinces saw advances in hiring. Most industries experienced job gains as well. Hours worked were up. Wage growth slowed toward a more typical pace. And the unemployment rate fell, largely driven by fewer unemployed prime-aged (25-54 years) workers and newcomers to Canada (graph 1).

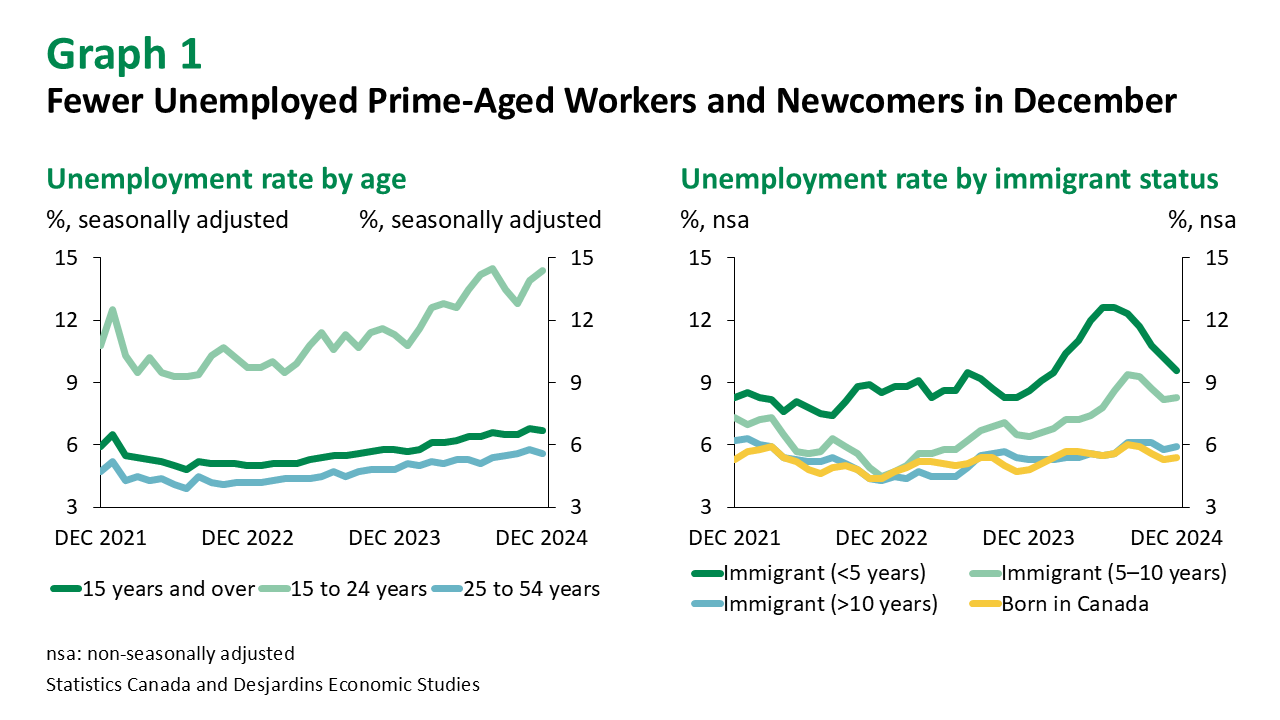

Muddying the message from the labour market in December is the ongoing slowdown in population growth. Concentrated in younger (15-24 years) and prime-aged workers, these groups led the gains in Canada’s population over the past couple of years but are now slowing quickly (graph 2). Motivated by a surge in non-permanent residents, the federal government has committed to reducing the population share of this group from 7.3% in Q2 2024 to 5% over the next three years. At the same time, the Government of Canada has also reduced its target for permanent resident admissions. While we’re skeptical External link. the federal government will achieve these ambitious goals, population growth is likely to respond to these measures and slow considerably even if they are only partially achieved.

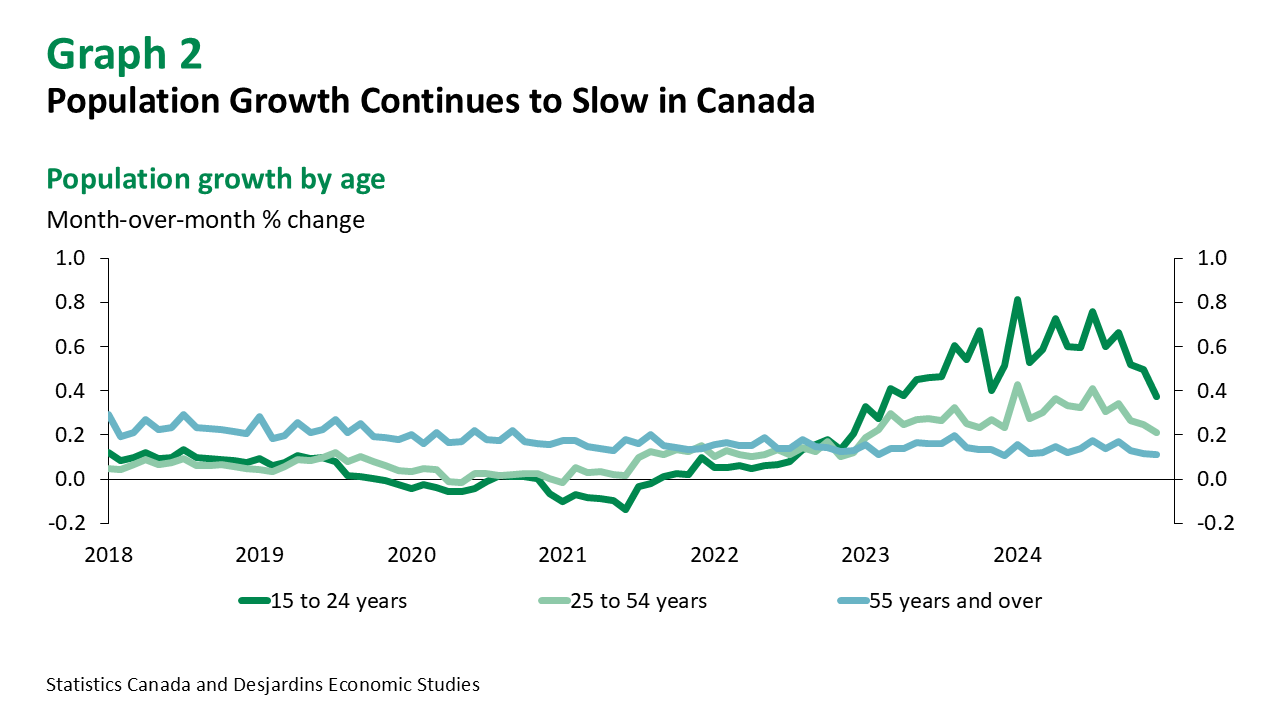

With population growth expected to slow, per capita real GDP and labour productivity should arrest their decline and start to edge higher. This should support further real wage gains, continuing a trend that has been observed for the better part of two years. And while average wage growth, as measured in the Labour Force Survey, has started to slow in recent months (graph 3), a tighter labour market in the coming months should ensure it continues to outpace inflation.

While December’s solid labour market print has reinforced our tracking for Q4 real GDP growth above the Bank of Canada’s forecast, the mounting economic headwinds on the horizon are likely to keep the Bank on a rate cutting path. As we outlined in our December 2024 Economic and Financial Outlook External link., potential tariffs from the incoming US administration, sharply slower population growth and the impending wall of mortgage renewals should weigh on economic activity in 2025. As such, we remain of the view that the Bank will cut the overnight policy rate by another 25 basis points later this month, then take a break in March. After that, it should continue a gradual pace of rate cuts through the rest of the year.