- Randall Bartlett

Deputy Chief Economist

Weekly Commentary

Canada’s Economy Is Weak, but a Recession Isn’t a Foregone Conclusion

September 19, 2025

What a week in Canada’s economy! The release of Canadian inflation External link. data for August was shortly followed by rate cuts from the Bank of Canada External link. and the Federal Reserve External link. after a prolonged period of staying on the sidelines. And this came after a leak from a senior official that the Government of Canada’s deficit could reach $100B this year when the long‑overdue federal budget is released on November 4. The reason for this firehose of monetary and fiscal policy support is that North American economies and labour markets are weak and risk getting weaker.

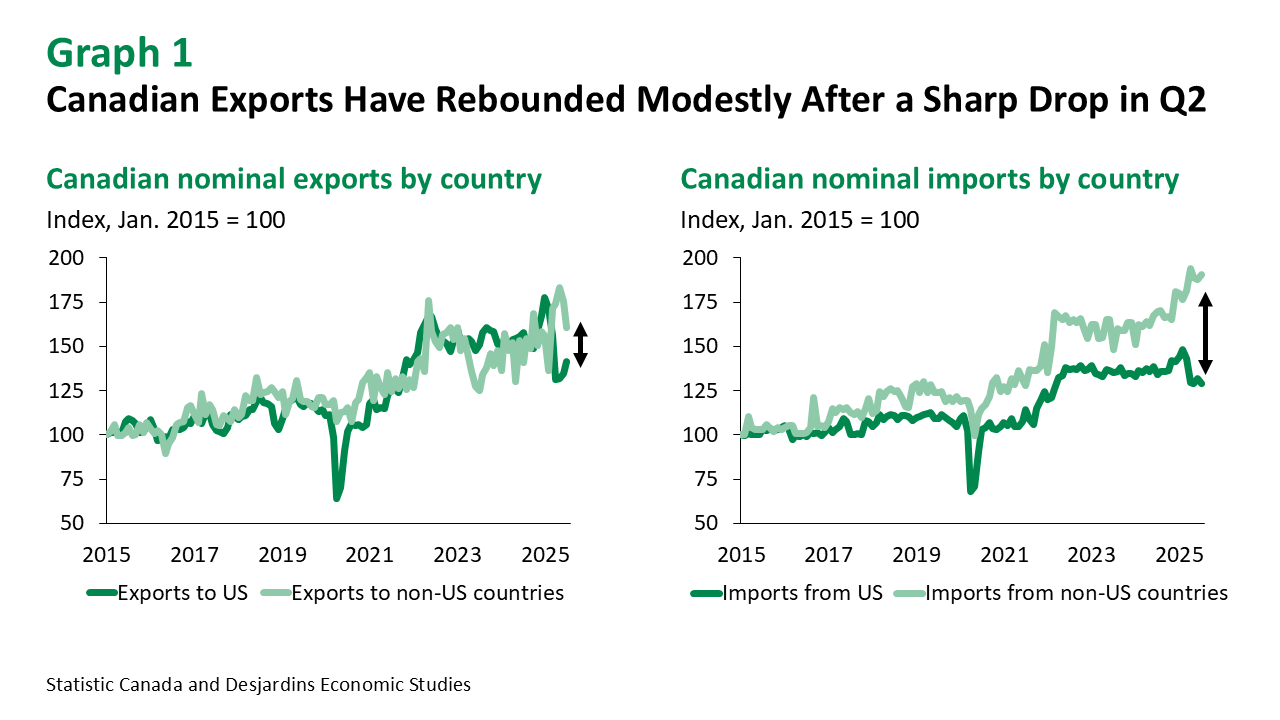

But what we’re seeing in the data gives a little more reason for cautious optimism regarding the Canadian economy. For instance, manufacturing sales volumes increased in July for the first time since January. Wholesale trade volumes also rose in the month, following an outsized advance in June. This corresponds with the turn in export volumes External link. observed in July (graph 1), which fits with our finding External link. that manufacturing and wholesale trade were among the sectors most vulnerable to shifting trade flows with the US. Sharply higher car and truck production likely contributed to the advance in July, after adjusting for seasonality. Seasonally adjusted data show railcar loadings and volumes of crude oil exports to the US picked up in the month as well, with each moving higher again in August. And that’s in spite of crude oil production likely having taken a dip over the summer resulting from the second‑worst wildfire season on record. Activity in Canada’s housing market also looks to be improving, with home sales External link. in August reaching their highest level in 2025 and housing starts remaining elevated despite recently slipping from a nearly three‑year peak reached in July.

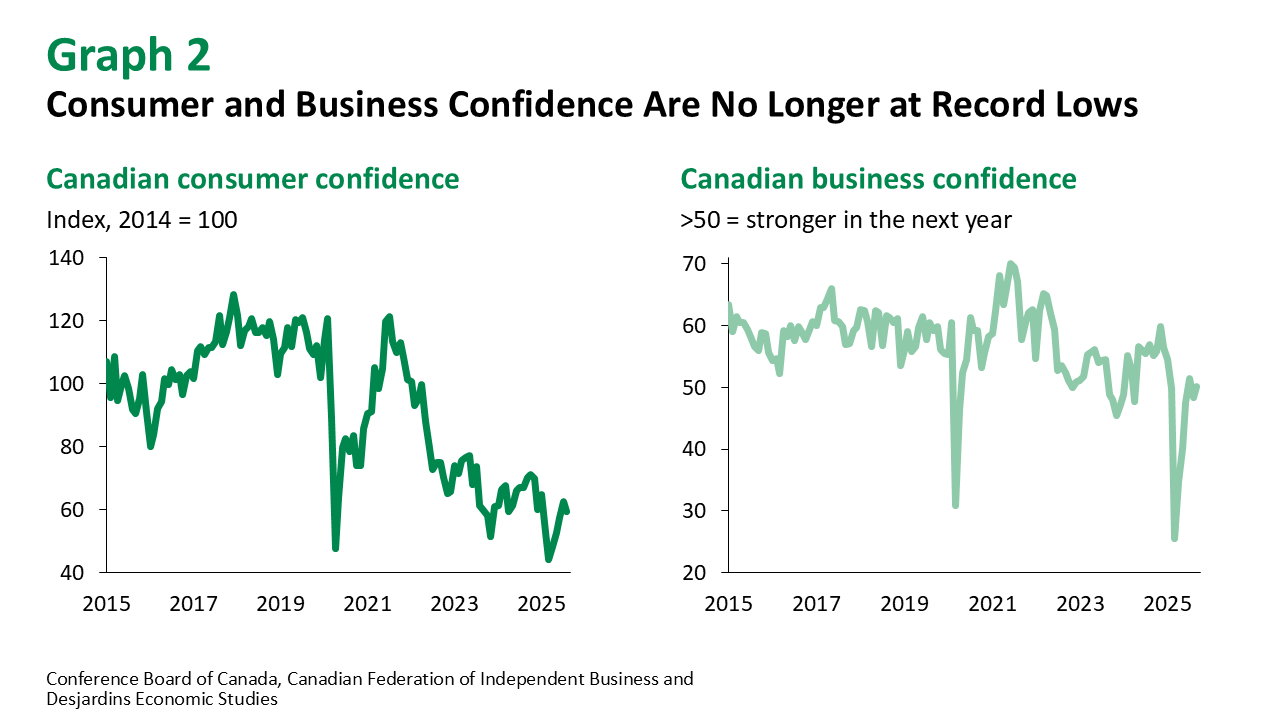

However, the Canadian economy isn’t out of the woods yet. While some sectors seem to have found a firmer footing, the labour market data External link. was notably soft in July and August. Retail sales External link. indicate consumers pulled back on spending in July, even when adjusting for inflation, although Statistics Canada’s flash estimate suggests retail sales may have moved higher in August. The recent weakness in consumer activity doesn’t come as a huge surprise, as much of the strength earlier in the year probably reflected a desire to get ahead of tariffs and to buy local. Indeed, the solid pace of consumer activity recorded last spring came just as consumer confidence in Canada reached its record low—an uncommon pairing (graph 2). Fundamentally, headwinds to household consumption growth remain, and they extend beyond the trade war uncertainty to encompass domestic factors such as rising monthly mortgage payments at renewal, still‑stretched housing affordability and rapidly slowing population gains. Business investment is also likely to be weak in the third quarter despite business sentiment that is well above its March lows. Ongoing hesitancy to invest in machinery and equipment resulting from US trade policy uncertainty, combined with the completion of a one‑off energy sector investment in an oil project off the coast of Newfoundland, should lead business investment to reverse its Q2 advance in the third quarter.

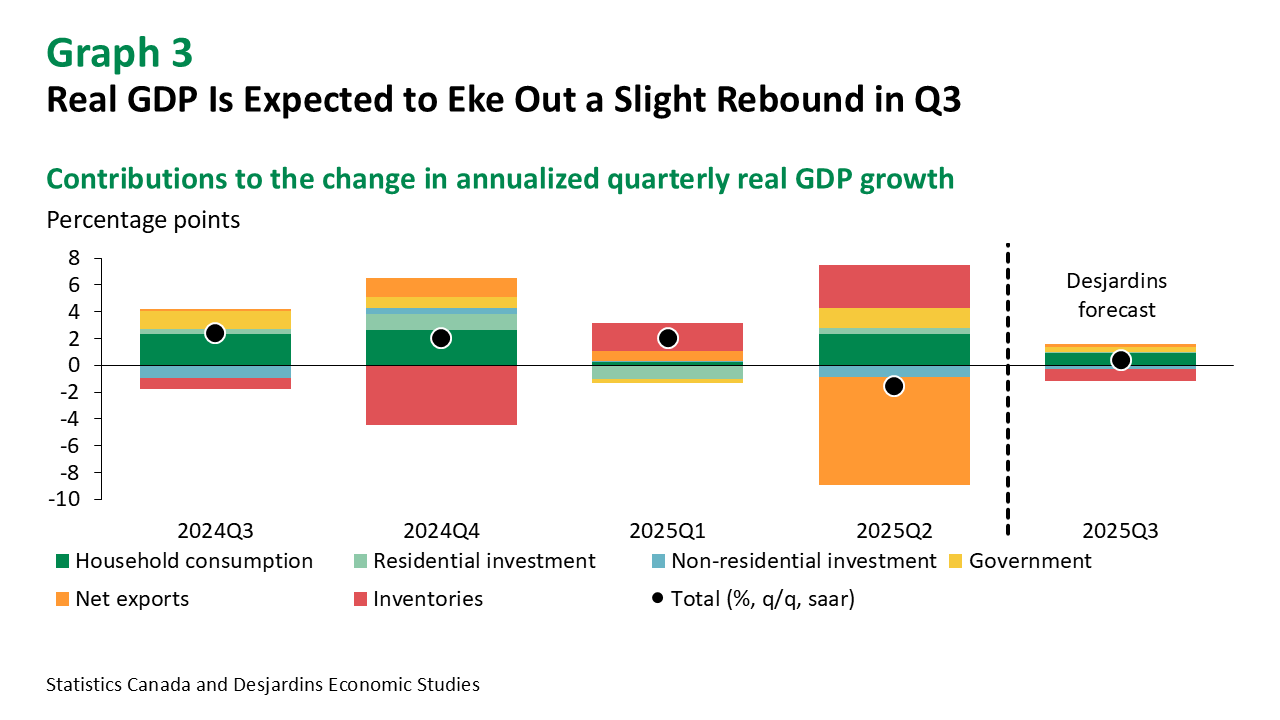

So where does that leave our outlook for economic growth in Q3? We’re currently tracking a 0.1% print for growth in real GDP by industry in July, in line with the flash estimate published by Statistics Canada. Accounting for this, as well as broader data so far in the third quarter and the elimination of tariffs on most consumer goods imports from the US as of September 1, we’re currently projecting Q3 real GDP growth to be in the range of 0.0%–0.5% annualized (graph 3). This is below the Bank of Canada’s baseline forecast of 1% in the third quarter, published in its July 2025 Monetary Policy Report External link., but we’re currently forecasting real GDP to end 2025 roughly in line with the Bank’s summer outlook. While not an economic rebound to write home about, it does suggest that a 2025 recession in Canada isn’t a foregone conclusion.