- Randall Bartlett

Deputy Chief Economist

Economic News

Canada: Rate Cuts Imminent as Inflation Remains Below the BoC’s 2% Target

September 16, 2025

Highlights

- Headline CPI rose 1.9% y/y in August, up from 1.7% y/y in July, but slightly below the consensus expectation of economists (2.0%). Prices moved down 0.1% month‑over‑month but rose 0.2% after adjusting for seasonal effects. Table 1 summarizes the key data points.

Comments

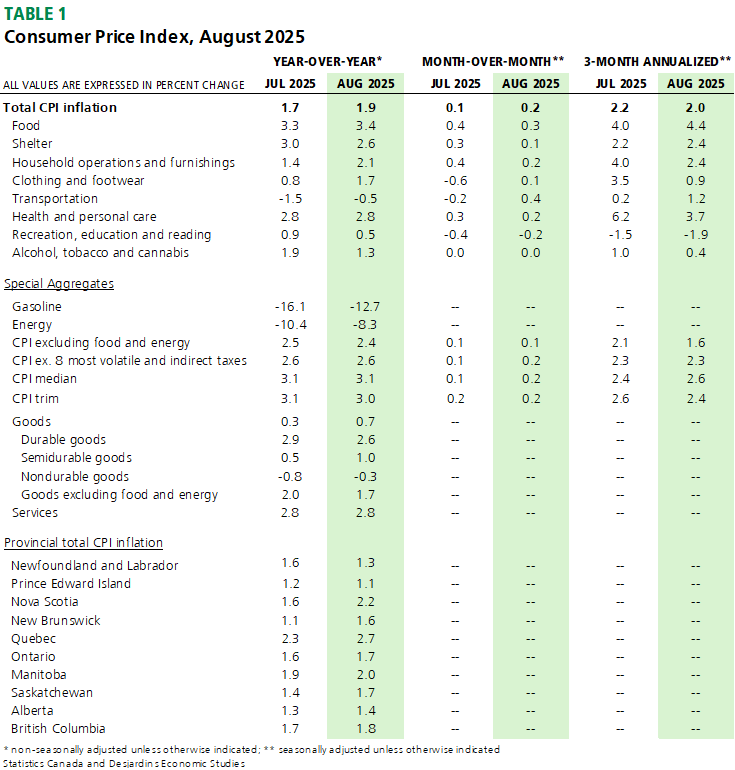

Headline inflation came in below the Bank of Canada’s (BoC’s) 2% inflation target for the fifth consecutive month in August. This was again in large part because of lower energy prices than a year ago thanks to the elimination of the federal consumer carbon tax in April (graph 1). Without this tax cut, total CPI inflation would have been closer to 2.4% in August, after increasing by 2.5% in each of the prior three months. That said, gasoline prices rose 1.4% m/m relative to July due to higher refining margins offsetting lower crude oil prices. (See our analysis External link. on the inflationary impact of eliminating the federal price on pollution.)

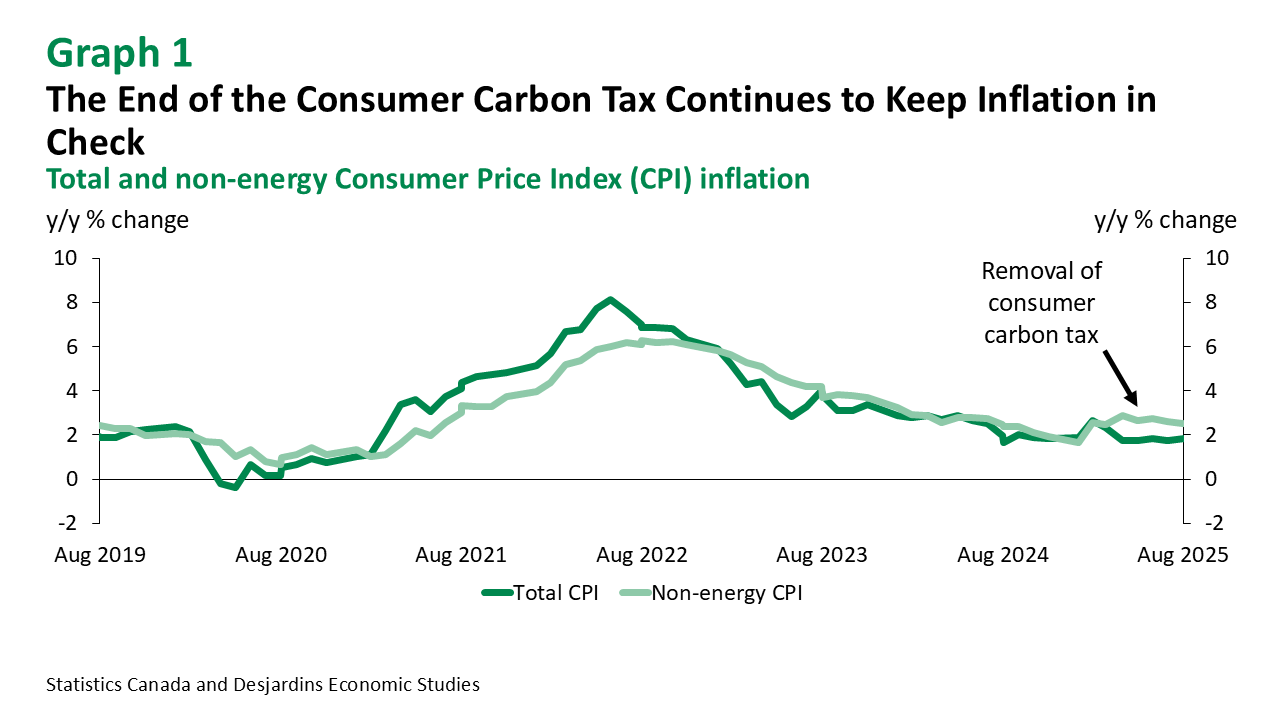

While lower energy prices continued to keep a lid on inflation in August, changes in other price categories were more mixed. The price of food edged higher in August (to 3.4% y/y from 3.3% in July), as the pace of price growth for meat accelerated while the cost of fresh fruit was lower than a year earlier. The price of cellular services also remained below year‑ago levels as did the price of travel tours on lower demand for destinations in the US. And while tariffs continued to play a role in keeping inflation more elevated than it would be otherwise, their contribution to rising core non‑shelter inflation should fade more quickly given they were significantly reduced on September 1 (see our analysis External link.). Shelter inflation also slowed in August as rents and utility price growth turned lower while homeownership inflation continued its downward trend (graph 2).

But key for the upcoming Bank of Canada rate announcement is core CPI inflation. The BoC’s preferred measures of core inflation—CPI median and trimmed mean—were broadly unchanged in August, at around 3.0 to 3.1% y/y. The annualized 3‑month moving average of these core seasonally adjusted series were similarly stable at around 2.5%, following an abrupt move lower in July (graph 3).

Implications

While underlying inflation proved somewhat sticky in August, the trend is undoubtedly its friend. With the removal of retaliatory tariffs on over $44B in imports from the US, CPI inflation is expected to gradually track lower going forward. We now anticipate that it will be consistently below the Bank of Canada’s 2% target in 2026. And when combined with a weak economy and labour market, the case for policymakers to remain on the sidelines is an increasingly tough one to make. As such, we maintain our long‑held call the the Bank of Canada will cut the policy rate by 25 basis points tomorrow, with two more cuts of the same magnitude likely before the end of the year.